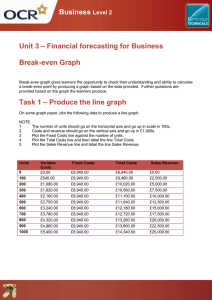

BREAK-EVEN ANALYSIS • Break-even refers to the identifying of the point where the revenue of the company starts exceeding its total costs for example, the point when the project or company under consideration will start generating the profits by the way of studying the relationship between the revenue of the company, its fixed cost and variable costs. • It determines what level of sales is required to cover the total cost of business ( Fixed as well as variable cost) • It shows us how to calculate the point or juncture when a company would start make a profit. • Therefore, Breakeven Analysis is a decision-making aid that enables a manager to determine whether a particular volume of sales will result in losses or profit THE THEORY BEHIND THE BREAKEVEN ANALYSIS • Made up of four basic concepts • Fixed costs- costs that do not change • Variable costs- costs that rise in propitiation to sales • Revenue- the total income received • Profit- the money you have after subtracting fixed and variable cost from revenue BREAKEVEN FORMULA • P(X) = f + V(X) • F = fixed costs • V = variable costs per unit • X = volume of output (in units) • P = price per unit THIS CHART SHOWS THAT THE BREAKEVEN POINT IS WHERE THE INCOME AND COSTS ARE EQUAL BREAKEVEN FORMULA CONT. • If we rearrange the formula where the breakeven is X then the formula look like this. X = F /( P – V) • This formula says that the breakeven point is where the number of sales needed to make the cost equal to the revenue USES OF BREAK-EVEN POINT • Helpful in deciding the minimum quantity of sales • Helpful in the determination of tender price • Helpful in examining effects upon organization’s profitability • Helpful in deciding about the substitution of new plants • Helpful in sales price and quantity • Helpful in determining marginal cost ASSUMPTIONS OF BREAK-EVEN ANALYSIS • The total costs may be classified into fixed and variable costs. It ignores semi-variable cost. • The cost and revenue functions remain linear. • The price of the product is assumed to be constant. • The volume of sales and volume of production are equal. • The fixed costs remain constant over the volume under consideration. • It assumes constant rate of increase in variable cost • It assumes constant technology and no improvement in labour efficiency. • The price of the product is assumed to be constant. • The factor price remains unaltered. • Changes in input prices are ruled out. • In the case of multi-product firm, the product mix is stable MANAGERIAL USES OF BREAK-EVEN ANALYSIS • To the management, the utility of break-even analysis lies in the fact that it presents a microscopic picture of the profit structure of a business enterprise. The break-even analysis not only highlights the area of economic strength and weakness in the firm but also sharpens the focus on certain leverages which can be operated upon to enhance its profitability. • It guides the management to take effective decision in the context of changes in government policies of taxation and subsidies THE BREAK-EVEN ANALYSIS CAN BE USED FOR THE FOLLOWING PURPOSES • Safety Margin: The break-even chart helps the management to know at a glance the profits generated at the various levels of sales. The safety margin refers to the extent to which the firm can afford a decline before it starts incurring losses. • The formula to determine the sales safety margin is: Safety Margin= (Sales – BEP)/ Sales x 100 TARGET PROFIT • The break-even analysis can be utilized for the purpose of calculating the volume of sales necessary to achieve a target profit. • When a firm has some target profit, this analysis will help in finding out the extent of increase in sales by using the following formula: Target Sales Volume = Fixed Cost + Target Profit / Contribution Margin per unit CHANGE IN PRICE • The management is often faced with a problem of whether to reduce prices or not. Before taking a decision on this question, the management will have to consider a profit. A reduction in price leads to a reduction in the contribution margin. • This means that the volume of sales will have to be increased even to maintain the previous level of profit. The higher the reduction in the contribution margin, the higher is the increase in sales needed to ensure the previous profit • The formula for determining the new volume of sales to maintain the same profit, given a reduction in price, will be as follows: New Sales Volume = Total Fixed Cost + Total Profit/ New Selling price – Average Variable Cost CHANGE IN COSTS: When costs undergo change, the selling price and the quantity produced and sold also undergo changes. Changes in cost can be in two ways: (i) Change in variable cost, and (ii) Change in fixed cost. VARIABLE COST CHANGE: • An increase in variable costs leads to a reduction in the contribution margin. This reduction in the contribution margin will shift the break-even point downward. Conversely, with the fall in the proportion of variable costs, contribution margins increase and break-even point moves upwards. Under conditions of changing variable costs, the formula to determine the new quantity or the new selling price is: (a) New Quantity or Sales Volume = Contribution to Margin/ Present Selling Price – New Variable Cost Per Unit (b) New Selling Price = Present Sale Price +New Variable Cost-Present Variable Cost FIXED COST CHANGE • An increase in fixed cost of a firm may be caused either due to a tax on assets or due to an increase in remuneration of management, etc. It will increase the contribution margin and thus push the break-even point upwards. Again to maintain the earlier level of profits, a new level of sales volume or new price has to be found out. • New Sales Volume = Present Sale Volume + (New Fixed Cost + Present Fixed Costs)/ (Present Selling Price-Present Variable Cost) • New Sale Price = Present Sale Price + (New Fixed Costs – Present Fixed Costs)/ Present Sale Volume LIMITATIONS 1. In the break-even analysis, we keep everything constant. The selling price is assumed to be constant and the cost function is linear. In practice, it will not be so. 2. In the break-even analysis since we keep the function constant, we project the future with the help of past functions. This is not correct. 3. The assumption that the cost-revenue-output relationship is linear is true only over a small range of output. It is not an effective tool for long-range use. 4. Profits are a function of not only output, but also of other factors like technological change, improvement in the art of management, etc., which have been overlooked in this analysis. 5. Selling costs are specially difficult to handle break-even analysis. This is because changes in selling costs are a cause and not a result of changes in output and sales. 6. When break-even analysis is based on accounting data, as it usually happens, it may suffer from various limitations of such data as neglect of imputed costs, arbitrary depreciation estimates and inappropriate allocation of overheads. It can be sound and useful only if the firm in question maintains a good accounting system. 7. The simple form of a break-even chart makes no provisions for taxes, particularly corporate income tax. 8. It usually assumes that the price of the output is given. In other words, it assumes a horizontal demand curve that is realistic under the conditions of perfect competition. 9. Matching cost with output imposes another limitation on break-even analysis. Cost in a particular period need not be the result of the output in that period. 10. Because of so many restrictive assumptions underlying the technique, computation of a break- even point is considered an approximation rather than a reality CONCLUSION • A Breakeven Analysis is a simple tool to use to determine if you have priced your product correctly • A Breakeven Analysis helps you calculate how much you need to sell before you begin to make a profit. You can also see how fixed costs, price, volume, and other factors affect your net profit EXAMPLE Lets say you own a business manufacturing sneakers. • It costs $65 to make one pair of sneakers • That’s your V or Variable cost • You sell each pair for $95 • That’s your P or price per unit • Your cost for rent, utilities, overhead, etc… is $474,000 per month That’s your F or fixed cost • V = $65.00 P = $95.00 • F = $474,000 Break-even units = X = F /( P – V) • X = 474,000 / ( 95 – 65 ) • X = 474,000 / ( 30 ) • X = 15,800 • To breakeven you would need to sell 15,800 sneakers. EXAMPLE CONT. • Break-even sales = unit sales x break-even units = $95 x $15,800 =$1,501,000 EXAMPLE CONT. • Other method of calculating breakeven • Breakeven value = fixed costs . ( contribution Margin) price per unit units sold for a desired profit = (Fixed Costs + Desired Profit) Contribution Margin EXAMPLE CONT. • A1 (Pvt) has the following CVP data • Selling price =$5/unit • Fixed costs per month = $30,0000 • Semi variable costs = $10,000 • Variable elements per unit = $3 • Calculate the following 1. The Break even value 2. How many units that must be sold to make a profit of $5,000 EXAMPLE CONT. • Breakeven value = fixed costs + Semi Variable Costs ( contribution Margin) price per unit contribution margin = selling price per unit – variable costs per unit = $5 - $3 = $2 break even value = ($30,000+$10,000) 0.4 = $100,000 . . EXAMPLE CONT. • Units to be sold to make a profit of $5,000 units sold for a desired profit = (Fixed Costs +Semi Variable Costs + Desired Profit) Contribution Margin • = ($30,000 + $10,000 + $5,000) . $2 • • = 20,000 units