Financial Econometrics

Topic 5: Cointegration

Dr. Aidil Rizal Shahrin

May 1, 2021

Department of Banking & Finance

Faculty of Business and Accountancy

1/49

Contents

1. Present Value Model

1.1 Econometric Model

2. Cointegration

2.1 Two-step Engle-Granger

3. Cointegration Tests for Structural Change

3.1 Gregory-Hansen Tests

4. Error Correction Models (ECM )

4.1 The Long-Run Compositions

4.2 The Short-Run Compositions

5. Vector ECMs

5.1 Granger Representation Theorem

2/49

Contents

5.2 Relationship between V AR and V ECM

5.3 Estimating the V ECM

5.4 Johansen Tests for Cointegration

3/49

Present Value Model

Present Value Model

i. Let Pt be the price of a share measured at the end of the

period (ex-dividend price), i.e., the purchase of the stock this

period entitles you to a claim to next period’s dividend per

share Dt+1

ii. The net simple stock return (end-of-period observations) of

the stock held from time t to time t + 1 is:

Rt+1 =

Pt+1 + Dt+1

−1

Pt

(1)

iii. Assume that expected returns is a constant:

Et [Rt+1 ] = r

(2)

4/49

Present Value Model

iv. Rearrange Eq.1 to get model of stock price:

Pt = E t

Pt+1 + Dt+1

1+r

(3)

v. Using the law of iterated expectation, i.e.,

Et [Et+1 [X]] = Et [X]

(4)

we can solve Eq.3 by repeatedly substituting out future prices.

vi. Solving K periods forward we have:

"K #

"

#

i

K

X

1

1

Pt = E t

Dt+i + Et

Pt+K

1+r

1+r

i=1

(5)

5/49

Present Value Model

vii. The first term on the RHS of Eq.5 is the expected DPV of

dividends while the second term is the expected discounted

value of the stock price K periods from now

viii. Assuming that the second term goes to zero as K increases

(i.e., the transversality condition)

"

lim Et

K→∞

1

1+r

K

#

(6)

Pt+K = 0

we obtain a model which defines the stock price as the

expected present value of future dividends out to infinity,

discounted at a constant rate:

"

Pt = PDt = Et

i

∞ X

1

Dt+i

1+r

i=1

#

(7)

6/49

Present Value Model

ix. If dividends are assumed to grow at a constant rate g

Et [Dt+i ] = (1 + g)Et [Dt+i−1 ]

= (1 + g)i Dt

(8)

x. Hence the stock price model with constant discount rate r and

dividend growth rate g , where g < r (for finite stock price) is

Pt =

Et [Dt+1 ]

(1 + g)Dt

=

r−g

r−g

(9)

and it is also known as the Gordon growth model

7/49

Present Value Model

Econometric Model

Econometric Model

i. To test a model of the type described by Eq.8 and Eq.9,

consider a system of equations which includes

Pt = β1 Dt + ut

(10)

a linear equation between price and dividends

Dt = β2 Dt−1 + wt

(11)

a data-generating AR(1) process for dividends and where the

errors are white noise processes.

8/49

Econometric Model

ii. Tests of the time-series properties of Dt and Pt (see Topic 2)

show that they are nonstationary variables, so Eq.10 should be

tested and estimated using the econometric techniques of

cointegration

9/49

Cointegration

Cointegration

i. Cointegration captures the idea of a long-run dynamic

economic model such that

a. Each variable is nonstationary

b. But, they do not drift too far apart from each other

ii. Reasons for understanding cointegration

a. There is strong evidence that financial time series are

nonstationary

b. For noncointegrated systems, it can be shown that t-tests and

F -tests are inflated in size upwards. This means that the null

hypothesis that the parameter is zero will be rejected more often

even when the null hypothesis is true (Type I error). For this

reason, a noncointegrated system is referred to as a spurious

regression

10/49

Cointegration

c. A cointegrated system can be decomposed into a long-run

(fundamental) part and a short-run (dynamic) part.

iii. Variables (Yt , Xt ) are said to be cointegrated if

a. Yt ∼ I(1) and Xt ∼ I(1) and

b. The residuals ut from the model

Yt = βXt + ut

are stationary, i.e., ut ∼ I(0)

c. The cointegrating vector is (1 − β).

d. More generally, if Yt and Xt are I(d) and Yt − βXt is I(d − b)

then Yt and Xt are cointegrated and d > b > 0.

e. The cointegrating equation can be decomposed into the

• Long-run: βXt

• Short-run: ut

11/49

Cointegration

Two-step Engle-Granger

Two-step Engle-Granger

i. According to the present value model above, the relationship

between share price (Pt ) and dividends (Dt ) is:

Pt = βDt + ut

where ut is a disturbance term

ii. We have established that the two series are nonstationary

variables, i.e., they are I(1) variables.

iii. However, if theory holds, then the two series are not expected

to drift too far apart. That is, the error term ut is I(0)

iv. If this holds, then Pt and Dt are said to be cointegrated

12/49

Two-step Engle-Granger

v. A natural way to test this is to apply the 2-step approach of

Engle-Granger (1987)

• Step 1: Perform an OLS regression. Note that although β̂ is

superconsistent, the standard errors (and hence t-stats) are not

correct except when residuals are white noise

• Step 2: Test stationarity property of the regression residuals

(always regress ∆ût on ût−1 (+ lags of ∆û) without the

constant term). The critical values for the Dickey-Fuller

t-statistics when applied to residuals from a spurious regression

is attached. (Note: Case 1 is when the Cointegrating equation

(CE) contains NO constant term, case 2 when the CE includes

a constant term, and Case 3 when the CE includes a constant

and time-trend).

If residuals are I(1) − (Pt , Dt ) are said to be spuriously related

If residuals are I(0) − (Pt , Dt ) are said to be cointegrated.

13/49

Cointegration Tests for Structural

Change

Cointegration Tests for Structural

Change

Gregory-Hansen Tests

Gregory-Hansen Tests

i. The cointegrating relationship between two variables {Y, X}

with no structural change is typically

Yt = µ + βXt + εt

The standard residual-based test for cointegration is an ADF

on the OLS residuals

ii. Cointegration tests can also be conducted in the presence of

deterministic structural breaks

iii. This is achieved by augmenting the standard cointegrating

equation between Y and X with dummy variables

iv. Both intercept and slope dummies can be included

14/49

Gregory-Hansen Tests

v. The Gregory-Hansen (GH ) cointegration tests are also ADF

tests on the residuals, but they are associated with

cointegrating models with structural break

vi. They are designed to test the null of no cointegration against

the alternative of cointegration in the presence of a structural

change

H0 : no cointegration

H1 : cointegration with a one-time regime shift

15/49

Gregory-Hansen Tests

vii. There are three tests. For convenience define a dummy variable

Dt = 0, if t ≤ λT

= 1, otherwise

• GH(1): the cointegrating equation allows for a mean-shift:

Yt = µ0 + µ1 Dt + β1 Xt + ε1t

• GH(2): the cointegrating equation allows for a mean-shift with

trend:

Yt = µ0 + µ2 Dt + β1 Xt + δt + ε2t

16/49

Gregory-Hansen Tests

• GH(3): the cointegrating equation allows for a regime shift,

i.e., shift in mean and slope coefficients:

Yt = µ0 + µ3 Dt + β1 Xt + β2 Dt Xt + ε3t

viii. The approach is to compute the usual t-statistics associated

with an ADF regression on the residuals obtained from

estimating the augmented cointegrating equation over all

possible breakpoints and choosing the smallest value

ix. As with the unit root case, new tables of critical values are

needed for conducting cointegration tests. These are given in

Gregory A.W. and Hansen, B. E. (1996)

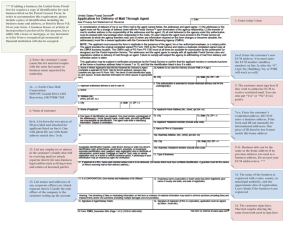

x. The critical values are given in the Table below. (m is the

regressors excluding constant and/or trend terms)

17/49

Gregory-Hansen Tests

18/49

Error Correction Models (ECM )

Error Correction Models (ECM )

i. The cointegrating relationship between the variables Yt and Xt

is a long-run relationship

ii. However, unless adjustment is instantaneous, Yt and Xt are

more likely to be related dynamically

iii. A general dynamic economic model (where ut is a disturbance

term) is as follows:

Yt = ρYt−1 + φ0 Xt + φ1 Xt−1 + ut

(12)

iv. Eq.12 can be rearranged into an error correction representation

(ECM hereafter) and shown to contain the long run

cointegrated relationship between Yt and Xt as well as other

short-run components.

19/49

Error Correction Models (ECM )

v. To show the relationship between an ECM and cointegration,

subtract Yt−1 from both sides of Eq.12

Yt − Yt−1 = (ρ − 1)Yt−1 + φ0 Xt + φ1 Xt−1 + ut

Add and subtract φ0 Xt−1 on the right hand side

Yt − Yt−1 = (ρ − 1)Yt−1 + φ0 (Xt − Xt−1 ) + (φ0 + φ1 )Xt−1 + ut

Rearrange the RHS

∆Yt = α(Yt−1 − βXt−1 ) + φ0 (∆Xt ) + ut

(13)

where

β=

φ0 + φ1

1−ρ

α = (ρ − 1)

(14)

(15)

20/49

Error Correction Models (ECM )

vi. Eq.13 is a single-equation error-correction model with long run

parameter β and error-correction term α

21/49

Error Correction Models (ECM )

The Long-Run Compositions

The Long-Run Compositions

i. The long-run is given by setting

a. Yt = Yt−1 = Y

b. Xt = Xt−1 = X

c. ut = 0

ii. Substituting these restrictions into the dynamic model Eq.12

and rearranging gives the long-run relationship between Yt and

Xt as

Y =

φ0 + φ1

X

1−ρ

iii. Notice that the coefficient on X , namely the long-run

multiplier, is equal to β in Eq.13

22/49

Error Correction Models (ECM )

The Short-Run Compositions

The Short-Run Compositions

i. The short-run movements in Yt are represented by Yt − Yt−1

ii. These movements can be decomposed into two types of

adjustments

a. φ0 (Xt − Xt−1 )

which occurs because of (short-run) movements in Xt

b. α(Yt−1 − βXt−1 )

which occurs when the variables are not in equilibrium

iii. This decomposition highlights the name given to the model

(ECM )

23/49

The Short-Run Compositions

iv. In particular, the second type of adjustment is known as the

error correction term since if Yt drifts above its long-run value,

thus making Yt−1 − βXt−1 positive, then providing that α is

negative and 0 < |α| < 1, the overall effect is to slow down, or

even decrease, Yt

v. This forces Yt back, that is error correct, to its long-run

position

24/49

Vector ECMs

Vector ECMs

i. The analysis above is based on a single equation representation

of the ECM

ii. But, that is only appropriate if dividends are (strongly)

exogenous (uni-directional causality)

iii. In general, for modelling economic systems which exhibit

long-run relationships it is more appropriate to estimate a

multivariate ECM (that is assume feedback causality)

iv. To move from the univariate to the multivariate case, we need

to understand

• the Granger Representation Theorem

• the relationship between a VAR with nonstationary variables

and its VECM representation

25/49

Vector ECMs

• Johansen’s test for the number of cointegrating relationship(s)

• Estimating a VECM

26/49

Vector ECMs

Granger Representation Theorem

Granger Representation Theorem

i. Suppose that Yt and Xt are I(1) and cointegrated with vector

(1, −β)

ut = Yt − βXt

ii. The Granger representation theorem states that Yt and Xt can

be expressed as an error-correction model (ECM ) such that

each equation contains the “common” long-run component

(Yt−1 − βXt−1 ) plus other short-run terms

∆Yt = α1 (Yt−1 − βXt−1 ) + lags(∆Yt , ∆Xt ) + ε1,t

∆Xt = α2 (Yt−1 − βXt−1 ) + lags(∆Yt , ∆Xt ) + ε2,t

27/49

Granger Representation Theorem

• Constants, time trends, dummies can be added as required

• Cointegration requires that at least one of the α’s be non-zero.

If α1 = α2 = 0 then the system is not cointegrated

• Signs of the α’s are important to capture adjustments in the

right direction (i.e., mean-revert)

• Size gives the speed of adjustment; α close to zero (one)

implies slow (fast) adjustment

iii. Consider again the econometric specification of the P V model:

Pt = β1 Dt + ut

(16)

Dt = β2 Dt−1 + ωt

(17)

This set of equations implies that:

• D has a data-generating process (DGP ) exogenous to P

28/49

Granger Representation Theorem

• D cause P , and

• P and D are cointegrated with cointegrating vector (1, −β1 )

iv. To write Eq.16 and Eq.17 in the ECM form (ignoring other

lags) but assuming bilateral causality, manipulate equations as

follows:

∆Pt = −Pt1 + β1 Dt−1 + β1 (Dt − Dt−1 ) + ut

∆Dt = β2 Dt−1 − Dt−1 + ωt

Now rearrange terms to factor-out the common cointegration

component

∆Pt = α1 (Pt−1 − βDt−1 ) + δ1 ∆Dt + ε1t

∆Dt = α2 (Pt−1 − βDt−1 ) + δ1 ∆Dt + ε2t

29/49

Granger Representation Theorem

v. Note that the significance of the error-correction terms (α1 , α2 )

is informative about causality/(weak) exogeneity.

vi. For our case study, if Eq.16 and Eq.17 are “true”

representations of behaviour in the stock market, (that is D is

weakly exogenous) we expect to find α1 to be negative and

significant and to find α2 to be not significantly different from

zero

vii. If on the other hand, P and D are both endogenously

determined, we expect to find α1 to be negative and significant

and to find α2 to be positive and significant.

viii. Both α’s must be between 0 and 1 (in absolute terms)

30/49

Vector ECMs

Relationship between V AR and V ECM

Relationship between V AR and V ECM

i. To derive the multivariate ECM , it is convenient to start with

a V AR

y t = A1 y t−1 + · · · + Ap y t−p + εt

•

•

•

•

y t is a vector of endogenous variables

p is the lag length

A1 , . . . , Ap are matrices of coefficients to be estimated

εt is a vector of disturbance terms that are contemporaneously

correlated, but not

♦ serially correlated

♦ or correlated with y t−1 , . . . , y t−p , xt

31/49

Relationship between V AR and V ECM

ii. The V AR can be written as a vector error correction model

y t − y t−1 = Πy t−1 + C 1 (y t−1 − y t−2 ) + · · · + C p−1 (y t−p+1 − y t−p )

+ εt

∆y t = Πy t−1 +

p−1

X

C i ∆y t−i + εt

i=1

• C 1 , . . . , C p−1 are matrices which are function of the Ai

matrices of the V AR

• Π is a matrix which contains the

♦ cointegrating vectors

♦ error correction coefficients

• Note that the VECM has one less lag in the ∆y t ’s than there

were in the y t ’s from the original VAR.

32/49

Relationship between V AR and V ECM

iii. Consider a bivariate {Y1 , Y2 } set of nonstationary variables.

Assume that the true model contains data-generating

processes as follows

Y1t = 0.4Y1t−1 + 0.3Y2t−1 + 0.24Y2t−2 + ε1t

Y2t = Y2t−1 + ε2t

iv. The V AR form (note here with non-stationary variables) is:

" #

Y1t

Y2t

"

=

0.4

0

#"

#

0.3 Y1t−1

1

Y2t−1

+

"

0

0.24

0

0

#"

#

Y1t−2

Y2t−2

+

" #

ε1t

ε2t

(18)

Note also that this is a VAR with lag-order 2

33/49

Relationship between V AR and V ECM

v. The V AR of nonstationary variables can be transformed into a

V ECM as follows (Note that we are assuming cointegration

between {Y1 , Y2 }

• First subtract the first-order lag from both sides

∆Y1t = (0.4 − 1)Y1t−1 + 0.3Y2t−1 + 0.24Y2t−2 + ε1t

∆Y2t = (1 − 1)Y2t−1 + ε2t

• Add and subtract 0.24Y2t−1 for the first equation

∆Y1t = −0.6Y1t−1 + (0.3 + 0.24)Y2t−1 − 0.24(Y2t−1 − Y2t−2 ) + ε1t

∆Y2t = ε2t

34/49

Relationship between V AR and V ECM

• Rearrange terms in ECM form

∆Y1t = −0.6(Y1t−1 − 0.9Y2t−1 ) − 0.24∆Y2t−1 + ε1t

∆Y2t = ε2t

• Write in matrix form as:

#"

#

"

# "

∆Y1t

−0.6 −0.6 × −0.9 Y1t−1

=

∆Y2t

0

0

Y2t−1

"

#"

# " #

0 −0.24 ∆Y1t−1

ε1t

+

+

0

0

∆Y2t−1

ε2t

(19)

Notice that the VAR in Eq.18 is lag 2 while VECM in Eq.19 is

lag of 1 in ∆

35/49

Relationship between V AR and V ECM

• Factorise out the “common” long-run relationship:

#

#

"

"

# "

i Y

∆Y1t

−0.6 h

1t−1

=

1 −0.9

Y2t−1

∆Y2t

0

# " #

#"

"

ε1t

0 −0.24 ∆Y1t−1

+

+

ε2t

∆Y2t−1

0

0

h

i

• Note that this is V ECM with long-run vector 1 −0.9 and

"

#

−0.6

error-correction vector

. Note too that the V AR of

0

"

#

∆Y1t

stationary variables

is now of order ONE.

∆Y2t

36/49

Relationship between V AR and V ECM

vi. EViews allows for five different specifications of the vector

error correction model depending upon whether or not

intercepts and or time trends are included in the

• Cointegrating equation (CE)

• ECM , or what EViews calls the test vector autoregression

(V AR)

• In Eviews, in the lag interval, if you type ”1 2” in the edit field,

the test VAR regresses ∆yt on ∆yt−1 , ∆yt−2

• In Gretl, in the cointegration test of Johansen, the lag order p

of the V AR(p). Thus, if the lag in VECM is 3, in the lag order

window set it to 4.

37/49

Relationship between V AR and V ECM

a. Case 1

• No intercept and no trend in CE

• No intercept and no trend in test VAR

Y1,t − Y1,t−1 = α1 (Y1,t−1 − βY2,t−1 ) + ε1,t

Y2,t − Y2,t−1 = α2 (Y1,t−1 − βY2,t−1 ) + ε2,t

In this example, the number of lags in the V AR is N = 0, and

!

α1 Π=

1, −β

α2

b. Case 2

• Intercept and no trend in CE

38/49

Relationship between V AR and V ECM

• No intercept and no trend in test V AR

Y1,t − Y1,t−1 = α1 (Y1,t−1 − βY2,t−1 − µ) + ε1,t

Y2,t − Y2,t−1 = α2 (Y1,t−1 − βY2,t−1 − µ) + ε2,t

c. Case 3

• Intercept and no trend in CE

• Intercept and no trend in test V AR

Y1,t − Y1,t−1 = δ1 + α1 (Y1,t−1 − βY2,t−1 − µ) + ε1,t

Y2,t − Y2,t−1 = δ2 + α2 (Y1,t−1 − βY2,t−1 − µ) + ε2,t

d. Case 4

• Intercept and trend in CE

39/49

Relationship between V AR and V ECM

• Intercept and no trend in test V AR

Y1,t − Y1,t−1 = δ1 + α1 (Y1,t−1 − βY2,t−1 − µ − φt) + ε1,t

Y2,t − Y2,t−1 = δ2 + α2 (Y1,t−1 − βY2,t−1 − µ − φt) + ε2,t

e. Case 5

• Intercept and trend in CE

• Intercept and trend in test V AR

Y1,t − Y1,t−1 = δ1 + θ1 t + α1 (Y1,t−1 − βY2,t−1 − µ − φt) + ε1,t

Y2,t − Y2,t−1 = δ2 + θ2 t + α2 (Y1,t−1 − βY2,t−1 − µ − φt) + ε2,t

40/49

Vector ECMs

Estimating the V ECM

Estimating the V ECM

i. The above vector error correction models can be easily

estimated as a system of equations with a common long-run

relationship

ii. If the residuals are “well-behaved”, the procedure also

generates t-statistics which are distributed asymptotically as

N (0, 1)

41/49

Vector ECMs

Johansen Tests for Cointegration

Johansen Tests for Cointegration

i. As seen above there is a close association between an ECM

and V AR with nonstationary time-series

ii. This has been exploited by Johansen to test for the number of

cointegrating relationships for systems with more than 2

variables

iii. To illustrate, consider a bivariate study of (Yt , Xt ) both I(1)

variables and cointegrated with vector (1, −β). The bivariate

ECM is:

∆Yt = α1 (Yt−1 − βXt−1 ) + ε1,t

∆Xt = α2 (Yt−1 − βXt−1 ) + ε2,t

42/49

Johansen Tests for Cointegration

which can be expressed as

yt =

Yt

Xt

!

∆y t = Πy t−1 + εt

!

ε1t

α1

, εt

, Π=

ε2t

α2

−α1 β

!

−α2 β

iv. The system can also be rearranged as:

Yt = (1 + α1 )Yt−1 − α1 βXt−1 + ε1,t

Xt = α2 Yt−1 + (1 − α2 β)Xt−1 + ε2,t

43/49

Johansen Tests for Cointegration

v. As a bivariate V AR:

y t = Ay t−1 + εt

A=

!

(1 + α1 )

−α1 β

α2

(1 − α2 β)

Thus we see that an ECM can be viewed as a V AR with

restrictions

Π = A − I2

44/49

Johansen Tests for Cointegration

vi. In general, V AR(p) can be transformed into a ECM with

(p − 1) lags of ∆y t−j

y=

p

X

Ai y t−i + ε

j=1

∆y t = Πy t−1 +

p−1

X

C i ∆y t−i + εt

i=1

Notice the lag of is V AR(p) while V ECM (p − 1)

vii. Notice that Π has reduced rank. It can be shown that it is the

reduced rank property that generates the nonstationary and

cointegration. In general for k variables, the rank of Π

determines how many cointegrating vectors there are:

45/49

Johansen Tests for Cointegration

• rank(Π) = 0, then y t ∼ I(1) but not cointegrated

• rank(Π) = r, 0 < r < k, then y t ∼ I(1) with r linearly

independent cointegrating vectors

• rank(Π) = k, then y ∼ I(0)

viii. If Π has reduced rank, then Π is the product of error

correction terms and the cointegrating vector

Π = αβ 0

ix. There exist a number of cointegration tests. The cointegration

test presented in EViews is known as the Johansen likelihood

ratio cointegration test

46/49

Johansen Tests for Cointegration

x. Large values of the Likelihood ratio relative to the critical

value result in rejection of the null hypothesis. The

cointegration test proceeds sequentially.

• Stage 1

H0 : No cointegrating vectors

H1 : At least one cointegating vectors

If the null is rejected proceed to the next stage, else stop and

do not reject the null hypothesis

47/49

Johansen Tests for Cointegration

• Stage 2

H0 : One cointegrating vectors

H1 : At least two cointegating vectors

If the null is rejected proceed to the next stage, else stop and

do not reject the null hypothesis of one cointegrating vector. If

the number of cointegrating vectors chosen equals the number

of variables, then the variables are all I(0).

xi. Although the Johansen test is the most popular test reported

in the literature, many Monte Carlo tests have shown that the

Johansen test to be very sensitive to mispecification of

lag-length and sample sizes.

48/49

Johansen Tests for Cointegration

xii. The Engle-Granger single equation test is more robust to

misspecification. In practice, one should report a number of

tests.

49/49