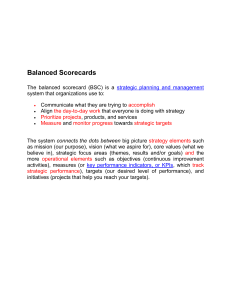

Performance Measures 1. Learning and Growth: recruiting, wellness/safety, skills development, job satisfaction, compensation and advancement and retention. 2. Internal Business Process: innovation, cost, product and service quality, time, agility and lean resource management. 3. Customer: satisfaction, loyalty, acquisition/retention, service, lifetime value and value proposition. 4. Financial: sales, profits, profitability ratios. Trend performance, cash flows and market performance. The balanced scorecard framework rejects the notion that improving process-oriented measures automatically leads to financial success. Including a financial perspective serves the purpose of holding organizations accountable for translating improvements in nonfinancial performance to “bottom-line” results. If favorable trends in a company's learning and growth, internal business processes, and customer measures do no translate to financial results, the balanced scorecard is designed to force the organization to re-examine its strategy for differentiating itself from competitors. Costs incurred to prevent defects or that result from defects in products are known as quality costs. Many companies are working hard to reduce their quality costs. Prevention Costs: support activities whose purpose is to reduce the number of defects. (quality training and circle, statistical process control activities) Appraisal Costs: incurred to identify defective products before the products are shipped to customers. (testing and inspecting incoming materials, final product testing, depreciation of testing equipment) Internal Failure Costs: incurred as a result of identifying defects before they are shipped. (scrap, spoilage, rework) External Failure Costs: incurred as a result of defective products being delivered to customers. (cost of field servicing and handling complaints, warranty repairs, lost sales) Quality cost reports provide an estimate of the financial consequences of the company’s current defect rate. Quality cost information help managers: 1. See the financial significance of defects 2. Identify the relative importance of the quality problems 3. See whether their quality costs are poorly distributed. Limitations of Quality Cost Information: 1. Simply measuring and reporting quality cost problem does not solve quality problems 2. Results usually lag behind quality improvement programs 3. The most important quality cost, lost sales, is often omitted from quality cost reports. Throughput (Manufacturing Cycle) Time = Process + Inspection + Move + Queue Times Delivery Cycle Time (DCT) = Throughput + Wait Times Process time is the only value-added time. Manufacturing Cycle Efficiency (MCE) = Value-Added Time / Manufacturing Cycle Time Overall Equipment Effectiveness (OEE): measures the productivity of a piece of equipment in terms of three dimensions—utilization, efficiency, and quality. Utilization Rate = Actual Run Time / Machine Time Available Efficiency Rate = Actual Run Time / Ideal Run Rate Quality Rate = Defect-Free Output / Total Output A company’s employees need to continuously learn and grow in order to improve internal business processes. Improving business processes is necessary to improve customer satisfaction. Improving customer satisfaction is necessary to improve financial results. Incentive compensation should be linked to balanced scorecard performance measures. Managers must be confident that the performance measures are reliable, sensible, understood by those who are being evaluated, and not easily manipulated. Corporate Social Responsibility (CSR) is a concept whereby organizations consider the needs of all stakeholders when making decisions beyond those that produce financial results to satisfy stockholders. Many of the world’s largest companies prepare corporate social responsibility performance reports (also called sustainability reports) that are shared with their external stakeholders. The Global Reporting Initiative (GRI) is a leading organization in the field of social and environmental performance measurement. The balanced scorecard provides a useful framework for organizing and managing the types of social and environmental performance measures that companies often include in their sustainability reports.