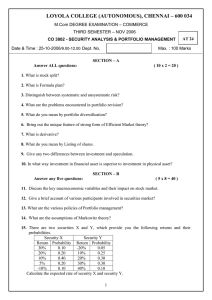

BU283: Financial Management I Taught by: Matthew Civello Hrishi Lariya cive1970@mylaurier.c lari5080@mylaurier.ca a SOS Exam Aid products are created from the experience and insights from students who have previously excelled in the course. Instructors draw upon their own notes and successful study practices to provide an engaging opportunity for students to learn from their peers. Did you know more than 100,000 students have been helped by our Exam-AIDs on 25 University campuses? • SOS has raised $2.5 MILLION DOLLARS for educational projects in Latin America. • With more than 2,000 active volunteers, SOS is one of the largest student organizations in Canada. See your donation in action! Want to experience two exciting weeks in Latin America, building the education project THIS session is funding? To give you a taste, here’s a video from Windsor SOS’ trip to Guatemala. Instructor Profile – Matthew Civello Program: 2nd Year BBA Involvement: Instructor Profile – Hrishi Lariya Program: 3rd Year BBA Involvement: SOS Exam Aid products are created from the experience and insights from students who have previously excelled in the course. Instructors draw upon their own notes and successful study practices to provide an engaging opportunity for students to learn from their peers. Did you know more than 100,000 students have been helped by our Exam-AIDs on 25 University campuses? • SOS has raised $2.5 MILLION DOLLARS for educational projects in Latin America. • With more than 2,000 active volunteers, SOS is one of the largest student organizations in Canada. Youtube: Make a Real World Impact, Gain RealWorld Experience See your donation in action! Even through COVID-19, SOS is still funding projects in Latin America to support learning through the pandemic. Watch this video to get a glimpse of what we do at SOS! Youtube: We Are Students Offering Support Agenda 1. Chapter 07 - Interest and Bonds 1. Chapter 05 - Risk and Return 1. Chapter 06 - Portfolio Theory 1. Chapter 08 - Stock Valuation and Market Efficiency Bond Qs - Key Points ● Bond yields and bond prices are inversely related ○ ● Yield is the return received by an investor. Cheap bonds mean better returns (higher yields) Longer term bonds have higher yields ○ ○ Long term → more risk → higher yields When longer term bonds don’t have higher yields, the yield curve is “inverted” Bond Qs - Key Points ● Real vs Nominal interest rates ○ ○ ● Prices of longer term bonds are more sensitive to changes in yield ○ ● Real interest rate: interest rate if inflation was nonexistent Nominal interest rate: interest rate adjusted for inflation Longer term bonds → more interest rate risk Bond returns come from 2 sources (bondholder perspective) ○ ○ Capital gains/losses (comes from changes in the bond price) Interest (coupons + interest on reinvested coupons) Coupon Bond Question Springfield Nuclear Energy Inc. bonds are currently trading at $903.55. The bonds have a face value of $1,000, a coupon rate of 8.5% with coupons paid annually, and they mature in 15 years. What is the yield to maturity of the bonds? Coupon Bond Question Consider an annual coupon bond with a face value of $100, 14 years to maturity, and a price of $92. The coupon rate on the bond is 6%. If you can reinvest coupons at a rate of 2.5% per annum, then how much money do you have if you hold the bond to maturity? Coupon Bond Question Iron Maiden became the first heavy-metal band to sell bonds when it arranged a $30 million deal in February 1999. The collateral on the bonds (and source of cash flow for interest and principal payments) consisted of future royalties from the band's albums like "The Number of the Beast." Each bond in the issue had a face value of $1,000, a term of 11 years and paid semiannual coupons at the rate of 8.5%. The yield to maturity on the bond was 7.5%. At what price did each of the bonds sell? Chapter 05 Introduction to Risk and Return The Risk-Return Relationship Investors study the characteristics of assets to determine the likelihood of its actual cash flows meeting projections. The uncertainty regarding the assets cash flows constitutes risk. Once perceived riskiness is established, the market will determine a sufficient expected return to induce investors to purchase the asset. Risk is determined by: 1. Determined by the uncertainty of future cash flows 2. Uncertainty is the result of factors peculiar to each asset Return on a Single Asset Return on an asset comes from two sources: 1. Capital Gain 2. Dividend Yield Holding Period Return (HPR) - The percentage return on an asset for the period that you have held/are holding for. - The holding period return on an asset is the sum of its capital gain and dividend yield HPRi = (Ending Price - Beginning Price + Dividends) / (Beginning Price) HPRi = [(Ending Price - Beginning Price)/Beginning Price] + (Dividend / Beginning Price) Return on a Single Asset Return on an asset comes from two sources: 1. Capital Gain 2. Dividend Yield Holding Period Return (HPR) - The percentage return on an asset for the period that you have held/are holding for. - The holding period return on an asset is the sum of its capital gain and dividend yield HPRi = (Ending Price - Beginning Price + Dividends) / (Beginning Price) HPRi = [(Ending Price - Beginning Price)/Beginning Price] + (Dividend / Beginning Price) Capital Gain Dividend Yield Example: Return on a Single Asset (Pearson Revel: Practice Section 5.2, Question 1) Suppose that you purchased 2,000 shares of Pan Am Airlines at the beginning of the year for $15.32. By the end of the year, the stock price had appreciated to $18.57. At the end of the year, Pan Am paid a dividend of $0.87 per share. Calculate the return on your investment over the year. Example: Return on a Single Asset (Pearson Revel: Practice Section 5.2, Question 1) Suppose that you purchased 2,000 shares of Pan Am Airlines at the beginning of the year for $15.32. By the end of the year, the stock price had appreciated to $18.57. At the end of the year, Pan Am paid a dividend of $0.87 per share. Calculate the return on your investment over the year. HPRi = [(Ending Price - Beginning Price) / Beginning Price] + (Dividends / Beginning Price) HPRi = [(18.57 - 15.32) / 15.32] + (0.87 / 15.32) HPRi = 0.21 + 0.06 = 27% Simple Average vs. Compound Average Arithmetic (Simple) Average Return - The return calculated where compounding is ignored Average Return = 1/n (∑ ki) Geometric (Compound) Average Return - The return calculated that recognizes interest or earnings paid on accumulated interest or earnings Geometric Return = (Ending Value / Beginning Value) (1 / n) - 1 Example: Average vs. Geometric Return Consider the following price and return information. Year Price 1 $10 2 $20 100% 3 $10 - 50% (i) Calculate the arithmetic return (ii) Calculate the geometric return Return Example: Average vs. Geometric Return Consider the following price and return information. (i) Year Price Return 1 $10 2 $20 100% 3 $10 - 50% Calculate the arithmetic return k = (100% + (-50%)) / 2 k = 25% (ii) Calculate the geometric return k = ($10 / $10) (1/3) - 1 k = 0% The compound return is the annual return that would have made $10 grow into $10 over two years with compounding. If you invested $10 and it became $10 in two years, that is a 0% return This shows why geometric return is a better measure of investment return. Expected Return Expected Return (E(k)) - The return that is expected to be earned each period on a given asset in the future. Note: Expected return is the weighted average of all possible future returns on an asset E(k) = Pr1(ki) + Pr2(k2) + … + Prn(kn) Where: ki = ith state of nature Pri= Probability of the ith occurrence n = Number of possible outcomes Example: Expected Return (Pearson Revel: Practice Section 5.2, Question 4) What is the expected return for a security if there's a 39% probability of returning 8% and a 61% probability of returning 22%? E(k) = Pr1(ki) + Pr2(k2) + … + Prn(kn) E(k) = (0.39 * 0.08) + (0.61 * 0.22) E(k) = 0.1654 = 16.54% Risk of a Single Asset Standard Deviation of returns on an asset measures the risk of that asset. Greater deviations from the mean is a greater standard deviation. Therefore, a higher standard deviation indicates higher risk. Standard Deviation (𝞼) = [∑(ki - E(k))2 x Pri]1/2 Where: E(k) = Expected return ki = Return of the ith outcome Pri = Probability of the ith occurrence n = Number of outcome evaluated Note: You should do this in your calculator. Excel does not account for differing probabilities across states of nature and so will give you an incorrect answer when these probabilities do in fact differ. Risk of a Single Asset Standard Deviation of returns on an asset measures the risk of that asset. Greater deviations from the mean is a greater standard deviation. Therefore, a higher standard deviation indicates higher risk. Steps: 1. 2. 3. 4. 5. Compute the expected return Subtract each return from expected value Square each deviation to eliminate negative signs Multiply each squared deviation by states of nature and sum Compute the square root Note: You should do this in your calculator. Excel does not account for differing probabilities across states of nature and so will give you an incorrect answer when these probabilities do in fact differ. Example: Risk of a Single Asset (Pearson Revel: Practice Section 5.3, Question 1) You believe that next year there is a 25% probability of a recession and 75% probability that the economy will be normal. If your stock will yield -12% in a recession and 20% in a normal year, what is the standard deviation of the stock? Example: Risk of a Single Asset (Pearson Revel: Practice Section 5.3, Question 1) You believe that next year there is a 25% probability of a recession and 75% probability that the economy will be normal. If your stock will yield -12% in a recession and 20% in a normal year, what is the standard deviation of the stock? E(k) = (0.25 * -0.12) + (0.75 * 0.20) E(k) = 0.12 Standard Deviation (𝞼) = [∑(ki - E(k))2 x Pri]½ Standard Deviation (𝞼) = [(-0.12 - 0.12)2 * 0.25 + (0.20 - 0.12)2 * 0.75)]½ Standard Deviation (𝞼) = 0.1386 = 13.86% Example: Risk of a Single Asset It costs $1,000 to play the following game. If it rains tomorrow, you win $1,100, which is a 10% rate of return. If it does not rain tomorrow, you win $900, which is a -10% rate of return. Assume that there is a 50% chance of rain. What is the variance of the returns? Example: Risk of a Single Asset It costs $1,000 to play the following game. If it rains tomorrow, you win $1,100, which is a 10% rate of return. If it does not rain tomorrow, you win $900, which is a -10% rate of return. Assume that there is a 50% chance of rain. What is the variance of the returns? Standard deviation is the square root of the variance. So, variance is the standard deviation squared. E(k) = (0.50 * 0.10) + (0.50 * -0.10) E(k) = 0% Variance (𝞼2) = ∑(ki - E(k))2 x Pri Variance (𝞼2) = [(0.10 - 0)2 * 0.50] + [(-0.10 - 0)2 * 0.50] Variance (𝞼2) = 0.01 Expected Return of a Portfolio The expected return for a portfolio is the weighted average of the expected returns of each individual security within that portfolio, where weights are the weight of the security within the portfolio. Portfolio Weight (Wi) = Amount invested in i / Total amount invested Expected Return (E(kp)) = w1E(k1) + … + wnE(kn) Where: w1 = Portfolio weight of asset i E(ki) = Expected return of asset i Example: Expected Return on a Portfolio Your portfolio has an expected return of 13.25%. The portfolio includes two stocks. The first stock has a weight of 0.65 and the second has a weight of 0.35. If the expected return on the first stock is 15%, then what is the expected return on the second stock in percentage terms? Example: Expected Return on a Portfolio Your portfolio has an expected return of 13.25%. The portfolio includes two stocks. The first stock has a weight of 0.65 and the second has a weight of 0.35. If the expected return on the first stock is 15%, then what is the expected return on the second stock in percentage terms? E(kp) = w1E(k1) + w2E(k2) 0.1325 = (0.65 * 0.15) + (0.35 * X) 0.1325 - 0.0975 = 0.35X 0.035 = 0.35X X = 0.10 = 10% Risk of a Portfolio The risk of a portfolio of assets cannot be calculated with a weighted average of each asset’s standard deviation. Why? If asset A and asset B both have a standard deviation of 1, any combination of these assets two assets would yield a weighted average standard deviation of 1. But... Risk of a Portfolio The risk of a portfolio of assets cannot be calculated with a weighted average of each asset’s standard deviation. Why? If asset A and asset B both have a standard deviation of 1, any combination of these assets two assets would yield a weighted average standard deviation of 1. The standard deviation of this portfolio is 0, not 1: Both assets have a standard deviation of 1, the returns exactly offset each other (perfect negative correlation). Risk of a Portfolio The risk of a portfolio is driven by the correlation of the assets within it: Correlation - A predictable relationship between observations in which the movement over time of one item is related (correlated) to the movement of of another. The degree of correlation (r) can vary from -1 (perfect negative) to 1 (perfect positive) Positive Correlation - Correlated movement in the same direction Negative Correlation - Correlated movement in the opposite direction Correlation between assets is a tool for investors to limit the risk within their portfolio. By combining multiple risky assets, we can create a portfolio with less risk than each of the assets within it. This is called diversification. Note: Diversification can reduce risk, but never completely eliminate it. Let’s take a break. See you in 15 minutes! Chapter 06 Portfolio Theory Risk of a Portfolio Cont... The risk of a portfolio of assets is found by computing its standard deviation, which is driven by the individual variances and correlation between the assets. Where: wi = Weight of asset i 𝝈2 = Variance of asset i 𝝈 = Standard deviation of asset i Many-asset portfolio risk is driven by the average covariance of the assets. Example: Risk of a Portfolio Consider the data provided in the table for portfolio of assets A and B. The portfolio weights and variances are given in the table. The variances are expressed in decimal form. For example, if standard deviation is 50% then the variance is 0.502 = 0.25. The correlation of returns of the two assets is 0.39. What is the standard deviation of the portfolio? Asset A Asset B Portfolio Weight 0.53 0.47 Variances 0.1369 0.4096 Standard Deviation 0.37 0.64 Example: Risk of a Portfolio Consider the data provided in the table for portfolio of assets A and B. The portfolio weights and variances are given in the table. The variances are expressed in decimal form. For example, if standard deviation is 50% then the variance is 0.502 = 0.25. The correlation of returns of the two assets is 0.39. What is the standard deviation of the portfolio? Asset A Asset B 𝝈 = [(0.532*0.372 + 0.472*0.642.+ 2*0.53*0.47*0.39*0.37*0.64]2 Portfolio Weight 0.53 0.47 𝝈 = 0.4535 Variances 0.1369 0.4096 Standard Deviation 0.37 0.64 Types of Risk Risk can be divided into two types: 1. Diversifiable Risk (Unsystematic) - Risk that can be eliminated through diversification - Affects one or few assets For example, loss of a major customer, death of a CEO 1. Non-Diversifiable Risk (Systematic) - Risk that cannot be eliminated through diversification - Affects all assets to some extent For example, war, sudden change in monetary policy Total Risk = Non-diversifiable risk + Diversifiable risk Example: Types of Risk Categorize each of the following as systematic or unsystematic risk: 1. ABC Corporation is being investigated by the SEC for fraudulent behaviour 1. Samsung is forced to recall the Galaxy Note because of a flammable battery 1. The economy faces a major downturn 1. XYZ Corporation’s biggest competitor successfully launches a new product line 1. There is a significant hike in the corporate tax rate Example: Types of Risk Categorize each of the following as systematic or unsystematic risk: 1. ABC Corporation is being investigated by the SEC for fraudulent behaviour (Unsystematic) 1. Samsung is forced to recall the Galaxy Note because of a flammable battery (Unsystematic) 1. The economy faces a major downturn (Systematic) 1. XYZ Corporation’s biggest competitor successfully launches a new product line (Unsystematic) 1. There is a significant hike in the corporate tax rate (Systematic) The Efficient Set Efficient Set (Markowitz) - The set of all efficient portfolios across all standard deviations. This is a collection of portfolios with the highest possible return at each level of standard deviation. New Efficient Set (Sharpe) - The set of all portfolios formed by combining the risk free asset and the market portfolio. - According to Sharpe’s model, all investors optimally hold the same assets in the same proportion Risk Free Asset - An asset with no variation in its return, and no risk of default. 1. Standard deviation of returns is zero 2. The correlation of returns with any other asset is 0 Market Portfolio - The portfolio that includes every capital asset held in proportion to its market value relative to market value of all assets in total The market portfolio is very large and diversified, it thus has no unsystematic risk. Example: Value-Weighted Portfolio Value-Weighted Portfolio - A portfolio in which the weights of each asset are equal to the value of each asset relative to the total value of all assets in the portfolio kp = w1k1 + … wiki Asset # Shares Price Value Weight Stock A 5 Shares $100 $500 500/600 = 83.33% Stock B 5 Shares $20 $100 100/600 = 16.67% Note: The weight is not based on shares held, it is based on value. The market portfolio is value-weighted → The weights are the relative values of each asset in the portfolio Example: Value-Weighted Portfolio A value-weighted index is made of shares in two companies. On Day 1 you build a portfolio to mimic the index with 15% invested in Company 1 and 85% invested in Company 2. On Day 2, what trades do you need to make to adjust your portfolio weights so that your portfolio earns the same return as the index from Day 2 to Day 3? Company 1 Company 1 Company 2 Company 2 Day Price Shares Outstanding Price Shares Outstanding 1 6.62 400 10.00 1,500 2 7.53 400 10.54 1,500 3 8.82 400 11.07 1,500 Example: Value-Weighted Portfolio A value-weighted index is made of shares in two companies. On Day 1 you build a portfolio to mimic the index with 15% invested in Company 1 and 85% invested in Company 2. On Day 2, what trades do you need to make to adjust your portfolio weights so that your portfolio earns the same return as the index from Day 2 to Day 3? Day Company 1 Company 1 Company 2 Company 2 Price Shares Outstanding Price Shares Outstanding 1 6.62 400 10.00 1,500 2 7.53 400 10.54 1,500 3 8.82 400 11.07 1,500 You do not need to make any trades. Because your portfolio mimics the index on day 1, the weights will change in the same proportion as the value of the shares change. Example: Value-Weighted Portfolio A value-weighted index is made of shares in the two companies. In order for your portfolio to earn the same return as the index from Day 2 to Day 3, what portfolio weight do you need for Company 1 on Day 2? Company 1 Company 1 Company 2 Company 2 Day Price Shares Outstanding Price Shares Outstanding 1 6.62 400 10.00 1,500 2 7.53 400 10.54 1,500 3 8.82 400 11.07 1,500 Example: Value-Weighted Portfolio A value-weighted index is made of shares in the two companies. In order for your portfolio to earn the same return as the index from Day 2 to Day 3, what portfolio weights do you need on Day 2? Day Company 1 Company 1 Company 2 Company 2 Price Shares Outstanding Price Shares Outstanding 1 6.62 400 10.00 1,500 2 7.53 400 10.54 1,500 3 8.82 400 11.07 1,500 To mimic the index, your weights must be the same as the index: Total Value = 7.53*400 + 10.54*1500 Total Value = $18,822 C1 Weight = (7.53*400) / 18882 C1 Weight = 16% C2 Weight = (10.54*1500) / 18822 C2 Weight = 84% Stock Market Indices Sharpe’s Market Portfolio would be impossible to mimic for most people because it composed of thousands of assets. This problem is avoided using a proxy for the market portfolio: Stock Market Index - A statistical indicator showing the relative value of a basket of stocks compared to the value in a base year - Example: Standard & Poor's 500 (S&P500), NASDAQ Exchange Traded Fund (ETF) - A basket of securities that mimics the composition of a target index seeking to achieve the same return as that target index. Systematic Risk and Beta Recall: The market portfolio does not contain unsystematic risk. Therefore, investors who hold the market portfolio are only concerned with systematic risk. Beta measures: 1. The amount of systematic risk in an individual asset 2. The marginal risk that an individual asset adds to the market portfolio Where: COV(ki,kM) = Covariance of returns between asset i and the market portfolio 𝝈2M = Variance of the market portfolio Intuition Behind Beta Recall: The market portfolio does not contain unsystematic risk. Therefore, investors who hold the market portfolio are concerned only with systematic risk. Beta = Market Risk Beta is telling us how much the return on a stock changes in response to a change in the return of the market: - Beta = 0.5 → The return on a stock changes 50% as much as the market Beta = 1.0 → The return on a stock changes the same amount as the market Beta = 1.5 → The return on a stock changes 150% as much as the market Therefore, a higher beta signals higher risk because the stock is volatile relative to the market. Example: Beta ABC Corporation stock has a correlation with the market of 0.55. ABC's standard deviation of returns is 40% and standard deviation of the market is 15%. What is ABC Corporation's beta? Example: Beta ABC Corporation stock has a correlation with the market of 0.55. ABC's standard deviation of returns is 40% and standard deviation of the market is 15%. What is ABC Corporation's beta? COV = 0.55 * 0.40 * 0.15 COV = 0.033 ß = COV / 𝞂2M ß = 0.033 / 0.152 ß = 1.47 Example: Beta Last year the market's return was 4% and ABC Corporation earned 6%. This year the market yielded 14%. If ABC Corporation's Beta is 1.50, what is its return this year? Example: Beta Last year the market's return was 4% and ABC Corporation earned 6%. This year the market yielded 14%. If ABC Corporation's Beta is 1.50, what is its return this year? Beta is the change in return of the stock in response to the change in return on the market. 1.5 means that ABC will change 1.5x the change in the market. The change in the market return was 10% → The change in ABC is 15% (10% * 1.50) The return on ABC is their return last year plus the change in their return this year: k = 6% + 15% k = 21% Estimating Beta To estimate beta, we must plot the asset against the returns on the market portfolio. The slope of the line of best fit is the beta of the asset. Characteristic Line - Line of best fit when the return of an asset is plotted against the return on the market portfolio Recall: Beta is the change in the return on a stock in response to change in return in the market by 1. The slope tells us the vertical change (return on the stock) in response to a one unit change on the x-axis (return on the market) Example: Estimating Beta Use the following price information to find the beta of XYZ Corporation: S&P500 XYZ Corporation January 1844.93 40.36 February 1863.38 41.97 March 1919.28 43.23 Example: Estimating Beta Use the following price information to find the beta of XYZ Corporation: S&P500 Return XYZ Return January 1844.93 40.36 February 1863.38 (1863.38 -1844.93) / 1844.93 = 1% 41.97 (41.97-40.36) / 40.36 = 4% March 1919.28 (1919.28 - 1863.38) / 1863.38 = 3% 43.23 (43.23 - 41.97) / 41.97 = 3% Beta is the slope (rise over run) of the characteristic line: ß = (∆XYZ) / (∆S&P500) ß = (0.03 - 0.04) / (0.03 - 0.01) ß = -0.01 / 0.02 ß = -0.5 Properties of Beta Three fundamental properties of beta: 1. Beta of the market portfolio is 1 Beta measures returns against returns of the market portfolio. The return of the market portfolio changes in direct proportion to itself. 1. Beta of the risk free asset is 0 Return on the risk free asset is constant. It does change in in any proportion to the market portfolio (no covariance). 1. Beta of a portfolio is a weighted average of each individual beta within it Example: Properties of Beta Consider the following historic information on the market, the risk-free rate (T-Bills) and two mutual funds, Templeton and Fidelity. If you had invested 56.64% of your wealth in Fidelity and the remainder in Templeton, what was your portfolio’s beta? Example: Properties of Beta Consider the following historic information on the market, the risk-free rate (T-Bills) and two mutual funds, Templeton and Fidelity. If you had invested 56.64% of your wealth in Fidelity and the remainder in Templeton, what was your portfolio’s beta? Bp = w1B1 + w2B2 Bp = (0.4336 * 1.3) + (0.5664 * 0.5) Bp = 0.85 Example: Properties of Beta (Pearson Revel: Practice Section 6.3, Question 4) You are building a portfolio out of a risk-free asset and a risky asset. The risk-free rate is 3.9% and the expected return on the risky asset is 12.5%. The beta of the risky asset is 0.709. You want your portfolio to have an expected return of 20.6% and a beta of 1.221. You have $1,000 of your own money to invest. What is the dollar value of your investment in the risky asset and what are the portfolio weights on the risky and risk-free assets? Example: Properties of Beta (Pearson Revel: Practice Section 6.3, Question 4) You are building a portfolio out of a risk-free asset and a risky asset. The risk-free rate is 3.9% and the expected return on the risky asset is 12.5%. The beta of the risky asset is 0.709. You want your portfolio to have an expected return of 20.6% and a beta of 1.221. You have $1,000 of your own money to invest. What is the dollar value of your investment in the risky asset and what are the portfolio weights on the risky and risk-free assets? ßp = w*ß1 + (1-w)*ß2 1.221 = 0.709w + (1-w)*0 1.221 = 0.709w w1 = 1.722 → $1,722 w2 = - 0.772 Chapter 08 Stock Valuation and Market Efficiency Stocks Stocks: A security that represents ownership in an incorporated company (Attend general meetings, review financial statements and elect members to the board of directors) Common Shares Preferred Shares (Hybrid) Typically give owner one vote per share • Pay a fixed amount of dividends • Typically do NOT have voting rights • Have a claim on assets and income after all liabilities (Residual Claimant) • • Receive anything left after all liabilities have been covered If Board of Directors choose to suspend dividends (hard to do), they must pay dividends to preferred before common (Cumulative Dividends) • In areas of liquidation receive par value • • Profit can be distributed through dividends or stock repurchases Capital Structure Paid First Bonds Paid Last Preferred Common Stock Markets Primary Market: Market where securities are traded for FIRST time Initial Public Offering (IPO): Where a firm first offers shares to the public and the firm becomes a public company Secondary Market: Market for trading securities after they have been issued (Exg, NASDAQ and NYSE) Seasoned Offering: An issue of stock that was offered in the past and has been traded since Public Company: Traded publicly on stock exchange Private Company: Not actively traded and not listed on exchange Long Positions Long Position: An investment where ownership is taken before the security is sold. (Purchase Precedes Sale) (Buy Low, Sell High) Exg: Buying a house and hoping price of house will rise and you sell at higher price Sell Buy Calculation: Bought: $903,800 Sold: $970,000 Capital Gain: $66,200 BUY ONLY IF YOU EXPECT INCREASE IN ASSET PRICE Short Selling Short Position: Investor borrows security. It is then sold. Later the security is bought back to repay the loan. Profitable only if you buy High and sell low. Borrow Buy Calculation Borrowed: $9,817 Bought: $8,567 Capital Gain: $1,250 SHORT ONLY IF YOU EXPECT DECREASE IN ASSET PRICE Valuation of Preferred Stock Simple preferred stock that is assumed to pay dividends in a perpetuity (forever) Practice Problem 2 If a preferred stock sold for $62 a share and $2.11 dividends were paid annually, what would be the required rate of return? Practice Problem Answers If a preferred stock sold for $62 a share and $2.11 dividends were paid annually, what would be the required rate of return? Algebraically Valuation of Common Stock Using Dividend Discount Model Calculate current price of stocks using Dividends and returns, allows you to see if you want to invest or not dependent on assumptions Practice Problem 3 An investor plans to buy a share of stock today, which will be held for 1 year. The stock will pay a $1.85 dividend and should sell for $50. If the required return is 11%, how much should investor pay for the stock? Practice Problem Answers An investor plans to buy a share of stock today, which will be held for 1 year. The stock will pay a $1.85 dividend and should sell for $50. If the required return is 11%, how much should investor pay for the stock? Practice Problem 4 Solution Constant Growth Model Assume that dividends grow at a constant periodic rate forever THE GROWTH RATE IS ASSUMED TO BE LESS THAN REQUIRED RETURN Constant Growth Model Cont’d ● ● ● FV = most recently occurring dividend PV = earliest occurring dividend n = # intervals during which dividends can grow ● First term = dividend yield ○ ● High yield stocks pay a relatively high portion of their income in form of dividends Second term = capital gain yield ○ Zero / Low yield stocks pay out a low percentage of income as dividends, instead investing in growth Constant Growth Model Practice (Q5) Pan American Airlines pays annual dividends on December 31. Today is January 1. Yesterday, PAN AM paid a dividend of $1.86. Dividends are expected to increase by 27% this coming year and then drop a long-run (perpetual) growth rate of 2.5%. Investors expect a return of 8.1% on PAN AM shares. What is the fair price for PAN AM? a. b. c. d. $29.53 $25.31 $33.74 $42.18 Constant Growth Model Answers Practice Problem 6 Solution Practice Problem 7 with non-constant growth Solution Problem 8 with non-constant growth The last dividend paid was $2 per share. They are expected to grow at a 20% rate for the next 3 years, then at a constant 10% thereafter. The required return of shareholders is 15%. What is the most you would be willing to pay for this stock? Solution McNally’s Solution Stock Repurchases and Total Payout Model Stock Repurchase: The repurchase of stock by a firm from its existing stockholders. It is a method to distribute cash without paying dividends Open Market Share Repurchase: A company instructs its broker to buy shares on the open market prevailing market prices. The shares are then cancelled and no longer outstanding. (Most Common) Fixed-Price Tender Offer: A one-time offer by a company looking to acquire another company that includes desire to purchase a certain number of shares at a fixed price. (Premium Price) Dutch Auction Share Repurchase: A company announces a target repurchase quantity and invites shareholders to offer their sales for sale. Total Payout Model: Provides an estimate of stock price by discounting dividends and share repurchases Total Payout Model TPM values a company’s total equity Total Payout Model Practice Problem (Q9) Analysts expect Sturk Industries to make payouts of $2.00 billion at the end of this year. Assume that all payouts occur annually at the end of the year and that we are at the beginning of the year. Analysts forecast that Sturk’s payouts will grow at 2.5% in perpetuity. Sturk stockholders required a return of 12%. Sturk has 1.44 billion shares outstanding. What is the fair price for Sturk’s shares today? Total Payout Model Answers Analysts expect Sturk Industries to make payouts of $2.00 billion at the end of this year. Assume that all payouts occur annually at the end of the year and that we are at the beginning of the year. Analysts forecast that Sturk’s payouts will grow at 2.5% in perpetuity. Sturk stockholders required a return of 12%. Sturk has 1.44 billion shares outstanding. What is the fair price for Sturk’s shares today? Practice Problem Q10 Solution Price Earnings Valuation Method The Price/Earnings (P/E): measure of how much the market is willing to pay for $1 of earnings from a firm It can be used to estimate the value of a firm’s stock Alternative valuation model when dividend and repurchase data is not available Typically going to use an industry P/E constant in calculations P/E Theory Question (Q11) Answer P/E Question (Q12) Company Z is currently priced at $29. They just reported earnings per share of $0.75. What is the P/E ratio that investors are willing to pay for a share of Company Z’s stock? P/E Question Answers Company Z is currently priced at $29. They just reported earnings per share of $0.75. What is the P/E ratio that investors are willing to pay for a share of Company Z’s stock? PE Question (Q13) Powell Motors has a P/E constant of 15 and 121 million shares outstanding. Analysts forecast net income to be $257.7 million in the next year. What is the fair price for a share of Powell Motors? PE Question (14) Powell Motors has a P/E constant of 15 and 121 million shares outstanding. Analysts forecast net income to be $257.7 million in the next year. What is the fair price for a share of Powell Motors? Thank you! Good luck on your midterm :) Extra Practice Extra Practice: Bonds Extra Practice: Bonds Extra Practice: Bonds Extra Practice: Beta Extra Practice: Beta Extra Practice: Beta Extra Practice: Beta Extra Practice: Beta Extra Practice: Beta Extra Practice: Valuation Extra Practice: Valuation STAY IN THE LOOP! @lauriersos @lauriersos