- No category

Wang Lab Financial Analysis: Memorandum & Recommendations

advertisement

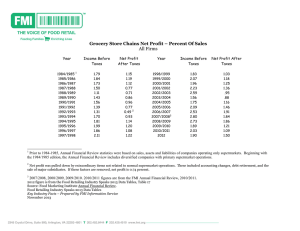

To: Professor Jamshed J. Mistry From: Team 4 Subject: Memorandum for Wang Lab’s Date: December 7, 2020 We, the undersigned students, analyzed the above case and prepared the attached memorandum on our own. We neither sought nor received outside assistance of any kind in analyzing the case or preparing the memorandum. Nor did we engage in discussions or exchanges of information of any kind, including electronic, with anyone either in the course or outside it, concerning the case study, our analysis of it, and our preparation of the attached memorandum. In signing this, each of us not only is stipulating that his/her hours are accurate, but also that he/she has reviewed the hours spent by other team members, and agree that they are accurate. This statement is signed in full recognition of the Policy on Academic Conduct of Rensselaer Polytechnic Institute, Lally School of Management. Team Member Signature Hours Spend on this Assignment Allison Hunt 5 Eric Zeppa 4 Evan Dunn 4 Justin Miklos 4 Jack Vaccari 2 Charisse Stakutis 2 Nessa Costa 2 Joey Gutowski 2 Memorandum From: Team 4 To: Wang President Richard Miller Ref: Financial Problems Recommendation: We recommend that in order to avoid bankruptcy certain steps should be taken. These steps include reducing the labor force, restructuring the organization with a focus on research and development, and the assurance that IBM is not taking advantage of them. Looking over the financial statements the financial problems had become apparent in 1987. In order to come to this conclusion the team analyzed the Income Statement and Balance Sheet (Exhibit 1), the Additional Information from Annual Reports (Exhibit 2), and the Consolidated Statement of Cash Flows (Exhibit 3) in order to calculate the Profitability, ShortTerm Liquidity Risk, and Long-Term Liquidity Ratios as seen in Exhibit 4. What makes Year 1987 stick out was how both the return on equity and return on assets both being negative. Some causes that led to Wang’s financial problems were the changes in leadership, the alliance with IBM, the economic recession, and the restructuring of the company. In late 1986 Frederick Wang became President of Wang Laboratories. During his two years revenue increased, but expenses grew faster. This may have resulted due to the interest attached to the debt, both long-term and short, that the company incurred. By the end of 1987, the company’s net income dropped by $121.6 million compared to the previous fiscal year, with the profit margin ratio dropping from 2.12 to -1.82. 1989 was also the start of a national economic recession which resulted in rapid changes to technology. After a recovery year in 1988 where Wang Laboratories saw an increase in net income to $90.7 million by years’ end, 1989 brought about major obstacles as the company saw their long term debt rise to $627.4 million. Even though the IBM alliance was supposed to benefit both sides, IBM took advantage of Wang Labs in 1990 and capitalized on the first five deals instead of sharing the wealth. In order to avoid bankruptcy Wang Labs should have followed the steps that Richard Miller took to save the company. In August 1989 Richard Miller took Frederick’s place as President and Wang Labs started to turn Wang Labs around financially. Miller sold fixed assets, reduced the labor force, restructured the organization, and refocused its product lines. He split the company into three divisions, Wang Information Systems, OFFICE 2000, and Personal Computer Systems, which allowed each unit to focus on their respective roles and regain leadership. Miller also placed an importance on Research and Development which allowed Wang Labs. Placing importance on customers and quality would be how Wang Labs would regain their footing that they almost lost. His partnership with IBM will also prove to be for the best, but the company needs to make sure that IBM is not taking advantage of them and taking all of the deals. These actions should have taken place in 1985 when the numbers started to go south, but the change in presidency only made matters worse. In conclusion, Wang Laboratories started to do poorly financially in 1987. This was caused by the interest attached to the debt, both long-term and short, that the company incurred. In order to avoid bankruptcy management should reduce the labor force, restructure the organization with a focus on research and development, and assure that IBM is not taking advantage of them. These steps should have taken place in 1987. Exhibit 1: Selected Date from Financial Statements, 1982-1991 (In Millions of Dollars) Income Statement Accounts 1982 Total Revenues $1,15 $1,53 $2,18 $2,35 $2,64 $2,83 $3,06 $2,86 $2,46 $2,09 9.30 8.00 4.70 1.70 2.50 6.70 8.40 8.80 1.10 1.50 Total Expenses $1,02 $1,34 $1,92 $2,40 $2,58 $2,88 $2,94 $3,07 $2,96 $2,42 3.20 8.30 3.50 6.20 6.60 8.40 9.70 4.40 6.70 5.30 Operating Income $136. $189. $261. $54.5 $55.9 $51.7 $118. $205. $505. $333. 10 70 20 0 0 0 70 60 60 80 Income Tax Provision $29.0 $37.7 $51.0 $70.0 $19.0 $26.0 $218. $210. $51.7 0 0 0 0 -$5.00 0 0 70 30 0 Net Income $107. $152. $210. $15.5 $50.9 $70.7 $92.7 $424. $715. $385. 10 00 20 0 0 0 0 30 90 50 Per Share Income $0.90 $1.20 $1.50 $0.10 $0.40 -$0.40 $0.60 -$2.60 -$4.40 -$2.30 Balance Sheet Data 1982 Cash and Equivalents $70.1 $232. $73.0 $48.3 $157. $179. $154. $258. $169. $233. 0 80 0 0 70 60 90 70 10 20 Accounts Receivables $281. $320. $445. $479. $530. $576. $532. $536. $473. $316. 30 90 20 40 10 10 60 10 50 00 Inventories $258. $316. $562. $469. $448. $412. $387. $359. $245. $162. 30 20 80 40 40 10 60 60 50 70 Other Current Assets $40.7 $57.7 $46.9 $52.2 $68.0 $82.5 $102. $172. $187. $109. 0 0 0 0 0 0 50 90 60 60 Total Current Assets $650. $927. $1,12 $1,04 $1,20 $1,25 $1,17 $1,32 $1,07 $821. 40 60 7.90 9.30 4.20 0.30 7.60 7.30 5.70 50 Other Assets $537. $754. $1,12 $1,32 $1,44 $1,56 $1,66 $1,40 $863. $596. 50 20 4.00 6.60 5.10 2.10 0.40 4.00 80 40 Total Assets $1,18 $1,68 $2,25 $2,37 $2,64 $2,81 $2,83 $2,73 $1,93 $1,41 7.90 1.80 1.90 5.90 9.30 2.40 8.00 1.30 9.50 7.90 Current Liabilities $243. $308. $541. $455. $537. $653. $709. $973. $865. $727. 30 70 90 00 90 40 20 10 40 20 Long-Term Debt $328. $363. $358. $666. $656. $667. $537. $627. $556. $499. 50 30 60 60 50 50 10 40 10 50 Other Liabilities $39.0 $72.0 $102. $103. $138. 0 0 00 $6.00 $7.30 $5.30 $5.60 $0.00 10 50 1983 1983 1984 1984 1985 1985 1986 1986 1987 1987 1988 1988 1989 1989 1990 1990 1991 1991 Total Liabilities $610. $744. $1,00 $1,12 $1,20 $1,32 $1,25 $1,60 $1,52 $1,36 80 00 2.50 7.60 1.70 6.20 1.90 0.50 4.60 5.20 Common Stock $274. $494. $612. $617. $788. $923. $962. $952. $952. $976. 60 40 00 40 70 50 60 00 80 10 Retained Earnings $302. $443. $637. $630. $658. $562. $629. $178. $537. $923. 50 40 40 90 90 70 10 80 90 40 Total Shareholders' Equity $577. $937. $1,24 $1,24 $1,44 $1,48 $1,59 $1,13 $414. $52.7 10 80 9.40 8.30 7.60 6.20 1.70 0.80 90 0 Total Liabilities and Equity $1,18 $1,68 $2,25 $2,37 $2,64 $2,81 $2,84 $2,73 $1,93 $1,41 7.90 1.80 1.90 5.90 9.30 2.40 3.60 1.30 9.50 7.90 Exhibit 2: Additional Information from Annual Reports, 1982-1991 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 High 37.88 42.50 41.00 31.88 22.88 19.13 19.13 11.13 8.00 5.00 Low 24.00 12.31 23.75 15.00 14.88 10.50 9.63 7.13 3.75 2.00 Dividends 0.12 0.16 0.16 na na Average Shares Outstanding (millions) 121.7 130.6 138.1 141.1 146.6 159.8 165.7 163.6 na na Average Number of Employees 17700 21700 27700 31700 31000 29700 29300 29200 22300 18100 Stock Prices: 0.09 0.12 0.16 0.16 0.16 Exhibit 3: Consolidated Statement of Cash Flows, 1982-1991 (In Millions of Dollars) 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 High 37.88 42.50 41.00 31.88 22.88 19.13 19.13 11.13 8.00 5.00 Low 24.00 12.31 23.75 15.00 14.88 10.50 9.63 7.13 3.75 2.00 Dividends 0.12 0.16 0.16 na na Average Shares Outstanding (millions) 121.7 130.6 138.1 141.1 146.6 159.8 165.7 163.6 na na Average Number of Employees 17700 21700 27700 31700 31000 29700 29300 29200 22300 18100 Stock Prices: 0.09 0.12 0.16 0.16 0.16 Operating Activities 1982 1983 1984 1985 1986 1987 1988 Net Income (loss) 107.1 152.0 210.2 15.5 50.9 (70.7) 92.7 Depreciation 62.8 1989 1990 1991 (320.6 (623.5 (377.9 ) ) ) 108.2 139.9 177.3 223.2 253.6 276.2 253.3 220.1 168.4 Amortization of Capitalized Software 39.1 Gain from Sale of Investments and Other Assets 58.2 41.4 (119.0 ) (16.6) Restructuring and Other Unusual Items 125.3 384.1 135.5 Changes in Other Accounts Affecting Operations: Accounts Receivable (45.2) 73.4 160.8 Inventory (3.0) 100.9 80.2 Other Current Assets (13.0) (1.2) 17.0 Accounts Payable and Other Current Liabilities Change in Working Capital 41.0 (59.8) (74.9) (285.1 ) 87.6 56.5 113.5 80.8 1.3 (2.0) 0.3 Deferred Income Taxes 20.2 33.0 30.0 96.0 Other (1.1) 1.7 (5.7) 2.7 Net Cash Provided by Continuing Operations 129.2 220.0 89.3 9.0 379.1 331.9 303.4 450.0 66.4 Net Cash Provided (Used) by Discontinued Operations Net Cash Provided by Operating Activitites (10.5) (29.7) 129.2 220.0 89.3 379.1 331.9 303.4 450.0 36.7 (21.3) (91.3) 14.1 2.8 85.8 120.3 3.5 4.9 89.3 125.2 Investing Activities Investment in Depreciable (146.4 (132.9 (265.5 (282.5 (133.8 (128.0 (156.8 (303.6 (174.4 (129.7 Assets ) ) ) ) ) ) ) ) ) ) Proceeds from Disposals of Depreciable and Other Assets 23.6 94.1 242.0 157.0 Spare Parts and Rentals (10.3) (85.0) (117.7 (119.5 (107.2 (116.8 ) ) (99.8) ) ) Proceeds from the Sale of Discontinued Operations 407.3 Investment in Capitalized Software (20.3) (38.5) (176.3 ) Other (13.9) (30.8) 52.9 19.3 (19.3) (8.5) 25.3 (43.1) (59.5) (43.1) (27.8) (25.8) (41.1) (25.1) (28.3) 14.2 (13.0) (6.0) Net Cash Provided (Used) (190.9 (287.2 (506.6 (408.5 (294.0 (245.2 (345.0 (254.8 by Investing Activities ) ) ) ) ) ) ) ) 418.8 18.8 Financing Activities Proceeds from Long-Term Debt 4.9 20.2 151.4 (132.9 ) (27.6) 84.3 174.8 95.2 311.9 Payment of Long-Term Debt (69.5) (41.8) Proceeds from Sale of Common Stock 9.6 Purchase of Treasury Stock Dividends Paid Other 22.2 (222.6 ) (2.6) 305.0 167.7 44.4 139.8 (145.3 (544.8 (126.5 ) (91.7) ) ) 205.7 122.8 25.1 198.1 15.9 22.5 17.5 8.7 5.0 (3.0) (4.0) (2.7) (9.0) (7.1) (7.5) (5.0) (18.8) (0.6) (0.3) (6.8) (9.5) (15.3) (20.6) (22.4) (25.1) (26.2) (26.0) (7.2) 7.7 Net Cash Provided (Used) by Financing Activities 96.7 (157.3 ) (93.9) 22.2 0.0 229.9 257.5 196.7 71.5 0.0 0.0 (129.7 (598.8 (36.3) ) 325.8 ) (80.0) Effect of Changes in Foreign Exchange Rates Increase (Decrease) in Cash and Equivalents 24.3 (3.9) 1.1 0.1 162.7 (159.8 ) (24.7) 109.4 21.9 Cash and Equivalents at Beginning of Year 70.1 232.8 157.7 179.6 154.9 258.7 169.1 Cash and Equivalents at End of Year 70.1 232.8 73.0 35.0 73.0 48.3 Exhibit 4: Financial Statement Ratios, 1982-1991 48.3 (24.7) 103.8 (89.6) 64.1 157.7 179.6 154.9 258.7 169.1 233.2 Profitability Ratios 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 Return on Equity 0.14 0.14 0.17 0.01 0.03 -0.05 0.07 -0.55 -3.06 -7.31 Return on Assets 0.07 0.08 0.09 0.01 0.02 -0.03 0.03 -0.18 -0.43 -0.27 11.74 12.33 11.96 -2.32 2.12 -1.82 3.87 -7.17 -20.54 -15.96 Profit Margin Various Expense Ratios 0.86 0.80 0.85 1.01 0.98 1.03 1.04 1.13 1.53 1.71 Fixed-Asset Turnover Ratio 0.98 0.91 0.97 0.99 1.00 1.01 1.08 1.05 1.27 1.48 Financial Leverage Ratio 1.06 0.79 0.80 0.90 0.83 0.89 0.79 1.42 3.67 25.91 Current Ratio 2.67 3.00 2.08 2.31 2.24 1.91 1.66 1.36 1.24 1.13 Quick or Acid Test Ratio 1.61 1.98 1.04 1.27 1.41 1.28 1.11 0.99 0.96 0.91 Liabilities to Assets Ratio 0.51 0.44 0.45 0.47 0.45 0.47 0.44 0.59 0.79 0.96 Long-Term Debt Ratio 0.28 0.22 0.16 0.28 0.25 0.24 0.19 0.23 0.29 0.35 Debt-Equity Ratio 0.57 0.39 0.29 0.53 0.45 0.45 0.34 0.55 1.34 9.48 Cash Flow from Operations to Total Liabilities Ratio 0.19 0.25 0.08 0.33 0.26 0.24 0.32 0.02 0.06 0.09 Short-Term Liquidity Risk Ratios Long-Term Liquidity Ratios

0

0

advertisement

Download

advertisement

Add this document to collection(s)

You can add this document to your study collection(s)

Sign in Available only to authorized usersAdd this document to saved

You can add this document to your saved list

Sign in Available only to authorized users