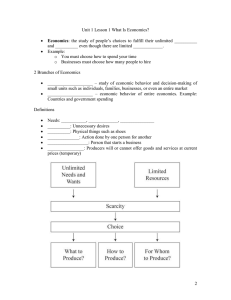

COURSE SYLLABUS Subject: Managerial Economics Course: BS Accounting Information System Unit Credits: 3 units Time Allotment: 3 Hours / Week Modalities: Modular Approach/ Online Learning COURSE DESCRIPTION : This course provides about the introductory knowledge about the principles, theory and applications of economics as a social science. This includes the relationship of studying economics and the real world. Period Topic PRELIM Chapter 1 Introduction to Economics Chapter 2 Elements of Demand and Supply Chapter 3 Concept of Elasticity Chapter 4 Theory of Consumer Behavior Chapter 5 Theory of Production Chpater 6 Analysis of Cost, Profit and Total Revenue Chapter 7 Market Structure Chapter 8 Business Cycle, Unemployment and Inflation MIDTERM PREFINAL FINAL COURSE REQUIREMENT: GRADING SYSTEM: *Class Standing o Attendance o Oral Participation o Written Output o Examinations TOTAL *Equivalent/ Transmuted Grades Written Reports, Computations, Oral Presentation, Examinations and Case Study 30% 30% 20% 20% 100% Transmutations/Equivalent 1.00 98-100 Excellent 1.25 95-97 1.50 92-94 Very Satisfactory 1.75 89-91 2.00 86-88 Satisfactory GWH/INC Grade Withheld/Incomplete 2.25 2.50 2.75 3.00 5.00 DRP. 83-85 80-82 Fairly Satisfactory 77-79 75-76 Passed 74- Below Dropped References: Managerial Economics Principles (v. 1.0). Economics: Its Concepts and Principles, Bon Kristoffer G. Gabay et. Al . Managerial Economics: Theory and Practice, Thomas J. Webster PREPARED BY: MR. RHEYJHEN M. CADAWAS, LPT, MAEd Instructor PRELIMINARY PERIOD INTRODUCTION TO ECONOMICS The main objective of Chapter I is to provide you an introduction to the basic concept of economics and managerial economics. It will help you to strengthen your knowledge about the subject. Pre-Activity: 1. Why Economics Is Dry And Difficult Subject? _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ ______________________. 2. Do you believe that economics has been closely related to our daily lives? Yes or No? Why? _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ ______________________. GOALS OF ECONOMICS • To strengthen economic freedom • Promote economic efficiency • Promote economic stability • To improve economic security • Attaining high level of growth in economy DEFINITION OF ECONOMICS Economics is a study of human activity both at individual and national level. Any activity involved in efforts aimed at earning money and spending this money to satisfy our wants such as food, Clothing, shelter, and others are called “Economic activities”. It was only during the eighteenth century that Adam Smith, the Father of Economics, defined economics as the study of nature and uses of national wealth’. Definition: Dr. Alfred Marshall, one of the greatest economists of the nineteenth century, writes “Economics is a study of man’s actions in the ordinary business of life: it enquires how he gets his income and how he uses it”. Prof. Lionel Robbins defined Economics as “the science, which studies human behavior as a relationship between ends and scarce means which have alternative uses”. • • • • Other Definitions: It is a social science that deals with just allocation of resources and efficient use of scarce resources in order to satisfy the needs and wants. It is concern with managing the problem of economic activities. It is a wealth getting and wealth using activities of man It is the art of making living ECONOMICS AS RELATED TO OTHER SOCIAL SCIENCES. ACTIVITY 1. Direction: Using the Web Diagram. List down other social sciences related to economics. ECONOMICS In connection with previous activity, how do you say so? Other Sciences 1. 2. 3. 4. 5. Social Explanations CONCEPTS OF ECONOMICS • Wealth—anything that has value • Consumption—refers to the process of direct utilization of goods and services by the household sector, business sector and the rest of the world • Production---refers to the creation of utility or a process by which economic are created. • Exchange---is the process of trading of good and services for money, goods for goods, goods for services and services for services. • Distribution—is the process of allocating scarce resources to both household, and business sector and the rest of the world BRANCHES OF ECONOMICS Microeconomics ➢ The study of an individual consumer or a firm is called microeconomics. ➢ Micro means ‘one millionth’. ➢ Microeconomics deals with behavior and problems of single individual and of micro organization. ➢ It is concerned with the application of the concepts such as price theory, Law of Demand and theories of market structure and so on. Macroeconomics ➢ The study of ‘aggregate’ or total level of economic activity in a country is called macroeconomics. ➢ It studies the flow of economics resources or factors of production (such as land, labor, capital, organization and technology) from the resource owner to the business firms and then from the business firms to the households. ➢ It is concerned with the level of employment in the economy. ➢ It discusses aggregate consumption, aggregate investment, price level, and payment, theories of employment, and so on. ACTIVITY 2. Directions. Identify whether the given economic activity is MICROECONOMICS or MACROECONOMICS. _____________1. Demand and Supply of commodities & determination of price by a firm. _____________2. Aggregate Demand and Aggregate Supply analysis. _____________3. Study of revenue of a firm. _____________4. Inflation, deflation and controlling the situation. _____________5. Employment and unemployment. _____________6. Study of costs of producing a good by a firm. _____________7. Determining producer's equilibrium (cost & revenue). _____________8. Money supply. _____________9. Interest rates. _____________10. Utility of a consumer: satisfaction from consumption. METHODS OF FORMULATING ECONOMIC THEORY 1. Data Gathering or Gather data about a problem or situations through interviews, observations, content analysis. 2. Economic Analysis or Organization of the data for analysis. 3. Economic Conclusions or Application of the economic theory on the problem situation. THEORY, MODEL and PRINCIPLE A theory, principle and model are basically the same, it is simplified description or explanation for reality. It is in forms of GRAPHS, WORDS, MATHEMATICS, or NUMERICAL TABLES Some data are constant or static. It is referred as “CETERIS PARIBUS”. ELEMENTS OF ECONOMIC THEORY VARIABLES– considered as a basic element of theories. (Value, Data, Numbers etc.) ASSUMPTIONS—creating possible explanation and prediction by taking other possibilities that affect it. HYPOTHESIS—is a conditional statement about how variable becomes related to another. PREDICTIONS—are statement that follows assumptions and hypothesis of a theory. METHODOLOGIES OF ECONOMICS • • Normative Economics- “What ought to be?” o It involves ethics and values judgement. It cannot be settled by a mere appeal. However, It does not mean that they are unimportant. It values judgment of what is good or bad, what is true or false. o It describes what is happening to the economy and why, without making any recommendation unless positive economics is made. o Example: To know if today’s bloated budget deficit can be raising VAT to 12%. This case needs a moral judgment which can be agreed upon and can only resolved through political decision. Positive Economics—“What is?” o It has something to do with “What is”. It describes facts and data in the economy. o It gives policy recommendation as basis for normative economics. o Example: If we want to know what percent of SY 2019-2020 graduates of BCC are unemployed?, We are talking about POSITIVE ECONOMICS. For it has available data and factual evidence. TYPES OF ECONOMICS 1. Household Economics – most common use of economics is for the family. At this level, anyone who knows the economic principles will be able to improve the running of the household. 2. Business Economics – when a person or group of persons begins to work, they come under the system of business economics in their workplace. In this type, you deal with the rent, salary, profits and others. 3. National Economics – Economic factors of problems affecting the whole nation. Deals with the management of income, expenditures, wealth or resources of a nation. 4. International Economics – The highest stage of economic activities involving the business of one country with other countries like trade, tourism, exchange rates. MANAGERIAL ECONOMICS Managerial Economics refers to the firm’s decision making process. It could be also interpreted as “Economics of Management” or “ Industrial economics “ or “Business economics”. NATURE OF MANAGERIAL ECONOMICS 1. Close to microeconomics: Managerial economics is concerned with finding the solutions for different managerial problems of a particular firm. Thus, it is more close to microeconomics. 2. Operates against the backdrop of macroeconomics: The macroeconomics conditions of the economy are also seen as limiting factors for the firm to operate. In other words, the managerial economist has to be aware of the limits set by the macroeconomics conditions such as government industrial policy, inflation and so on. 3. Normative statements: • A normative statement usually includes or implies the words ‘ought’ or ‘should’. They reflect people’s moral attitudes and are expressions of what a team of people ought to do • Such statement are based on value judgments and express views of what is ‘good’ or ‘bad’, ‘right’ or ‘ wrong’. • One problem with normative statements is that they cannot to verify by looking at the facts, because they mostly deal with the future. Disagreements about such statements are usually settled by voting on them. 4. Prescriptive actions: • Prescriptive action is goal oriented. • Given a problem and the objectives of the firm, it suggests the course of action from the available alternatives for optimal solution. • It also explains whether the concept can be applied in a given context on not. For instance, the fact that variable costs are marginal costs can be used to judge the feasibility of an export order. 5. Applied in nature: • ‘Models’ are built to reflect the real life complex business situations and these models are of immense help to managers for decision-making. •The different areas where models are extensively used include inventory control, optimization, project management etc. • In managerial economics, we also employ case study methods to conceptualize the problem, identify that alternative and determine the best course of action. 6. Offers scope to evaluate each alternative: • Managerial economics provides an opportunity to evaluate each alternative in terms of its costs and revenue. • The managerial economist can decide which is the better alternative to maximize the profits for the firm. 7. Interdisciplinary: • The contents, tools and techniques of managerial economics are drawn from different subjects such as economics, management, mathematics, statistics, accountancy, psychology, organizational behavior, sociology and etc. SCOPE OF MANAGERIAL ECONOMICS Managerial economics refers to its area of study. Managerial economics, Provides management with a strategic planning tool that can be used to get a clear perspective of the way the business world works and what can be done to maintain profitability in an ever-changing environment. Managerial economics is primarily concerned with the application of economic principles and theories to five types of resource decisions made by all types of business organizations. a. The selection of product or service to be produced. b. The choice of production methods and resource combinations. c. The determination of the best price and quantity combination d. Promotional strategy and activities. e. The selection of the location from which to produce and sell goods or service to consumer. The scope of managerial economics covers two areas of decision making: • Operational or Internal issues • Environmental or External issues A. OPERATIONAL ISSUES Operational issues refer to those, which are within the business organization and they are under the control of the management. Those are: 1. Theory of demand and Demand Forecasting 2. Pricing and Competitive strategy 3. Production cost analysis 4. Resource allocation 5. Profit analysis 6. Capital or Investment analysis 7. Strategic planning 1. Demand Analyses and Forecasting: ➢ Demand analysis also highlights for factors, which influence the demand for a product. This helps to manipulate demand. Thus demand analysis studies not only the price elasticity but also income elasticity, cross elasticity as well as the influence of advertising expenditure with the advent of computers. ➢ Demand forecasting has become an increasingly important function of managerial economics. A firm can survive only if it is able to the demand for its product at the right time, within the right quantity. Understanding the basic concepts of demand is essential for demand forecasting 2. Pricing and competitive strategy: ➢ Pricing decisions have been always within the preview of managerial economics. Price theory helps to explain how prices are determined under different types of market conditions. ➢ Competitions analysis includes the anticipation of the response of competitions the firm’s pricing, advertising and marketing strategies. Product line pricing and price forecasting occupy an important place here. 3. Production and cost analysis: ➢ Production analysis is in physical terms. ➢ While the cost analysis is in monetary terms cost concepts and classifications, cost-out- put relationships, economies and diseconomies of scale and production functions are some of the points constituting cost and production analysis. 4. Resource Allocation: ➢ Managerial Economics is the traditional economic theory that is concerned with the problem of optimum allocation of scarce resources. ➢ Marginal analysis is applied to the problem of determining the level of output, which maximizes profit. ➢ In this respect linear programming techniques has been used to solve optimization problems. In fact lines programming is one of the most practical and powerful managerial decision making tools currently available. 5. Profit analysis: ➢ Profit making is the major goal of firms. There are several constraints here an account of competition from other products, changing input prices and changing business environment hence in spite of careful planning, there is always certain risk involved. ➢ Managerial economics deals with techniques of averting of minimizing risks. Profit theory guides in the measurement and management of profit, in calculating the pure return on capital, besides future profit planning. 6. Capital or investment analyses: ➢ Capital is the foundation of business. Lack of capital may result in small size of operations. Availability of capital from various sources like equity capital, institutional finance etc. may help to undertake large-scale operations. ➢ Hence efficient allocation and management of capital is one of the most important tasks of the managers. ➢ The major issues related to capital analysis are: 1.The choice of investment project 2.Evaluation of the efficiency of capital 3.Most efficient allocation of capital. Knowledge of capital theory can help very much in taking investment decisions. This involves, capital budgeting, feasibility studies, analysis of cost of capital etc. 7. Strategic planning: ➢ Strategic planning provides a long-term goals and objectives and selects the strategies to achieve the same. . The perspective of strategic planning is global. ➢ strategic planning has given rise to be new area of study called corporate economics. B. Environmental or External Issues: They refer to general economic, social and political atmosphere within which the firm operates. A study of economic environment should include: The type of economic system in the country. a. The general trends in production, employment, income, prices, saving and investment. b. Trends in the working of financial institutions like banks, financial corporations, insurance companies c. Magnitude and trends in foreign trade; d. Trends in labour and capital markets; e. Government’s economic policies viz. industrial policy monetary policy, fiscal policy, price policy etc. ➢ The social environment refers to social structure as well as social organization like trade unions, consumer’s co-operative etc. ➢ The Political environment refers to the nature of state activity, chiefly states’ attitude towards private business, political stability etc. ➢ The environmental issues highlight the social objective of a firm i.e.; the firm owes a responsibility to the society. Private gains of the firm alone cannot be the goal. LEARNING ENHANCEMENT Task A. REFLECTION # 1 Summarize Chapter 1. Discuss what have you learned from this chapter. _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ __________________________________________________________________________________________. Rubrics for Reflections: Features 15 12 Quality of Writing It was written in extraordinary style, very informative and well organized It was written in interesting style, somewhat informative and organized Grammar Usage No wrong spelling, punctuations Few wrong spelling, or grammatical errors. punctuations or grammatical errors. 8 7 It was written in little It was written in style, little informative poor style, not and poorly organized informative and poorly organized A number of wrong So many wrong spelling, punctuations spelling, or grammatical errors punctuations or grammatical errors Task B. Cite an example on how you can use managerial economics in a real life situation. _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ __________________________________________________________________________________. Rubrics for Task B: Features 5 4 3 2 Quality of Writing It was written in extraordinary It was written in style, very informative and interesting style, well organized somewhat informative and organized It was written in little It was written in style, little informative poor style, not and poorly organized informative and poorly organized Grammar Usage No wrong spelling, punctuations or grammatical errors. A number of wrong So many wrong spelling, punctuations spelling, or grammatical errors punctuations or grammatical errors Few wrong spelling, punctuations or grammatical errors. Task 3. Research Activity. List down names of economist from ancient, medieval, classical, neo-classical and modern period in the development of economic thought. Give their major contributions. Use additional sheet/s to comply the activity. Rubrics for Task C. Features Quality of Output 25 20 It was written in extraordinary It was written in style, very informative and interesting style, well organized. somewhat informative and organized. 15 10 It was written in little It was written in style, little informative poor style, not and poorly organized informative and poorly organized ELEMENTS OF DEMAND AND SUPPLY Every economy must somehow solve the basic economic problems; what should be produced, how goods and services should be produced, and for whom are the goods and services produced. Hence, every managers, entrepreneurs or business men must make decisions to address the problems. The main objective of Chapter II is to show how demand and supply work in a competitive market. Also in this part, the basic concept of market equilibrium will be discussed. Pre-Activity: Interpret. Write your observation using the table/schedule below. Table 1 Table 2 Price Quantity Price Quantity 1 100 1 20 2 80 2 40 3 60 3 60 4 40 4 80 5 20 5 100 _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ _______________________________________________________________________________________ ____________________________________________________________________________________. DEMAND • • • Demand in common parlance means the desire for an object This means that the demand becomes effective only it if is backed by the purchasing power in addition to this there must be willingness to buy a commodity. Thus demand has three essentials – price, quantity demanded and time. DEMAND VS QUANTITY DEMANDED “Demand means the various quantities of goods that would be purchased at a particular price and not merely the desire of a thing.” “Quantity demanded is the amount of goods/services are willing and able to buy/purchase at a given price, place and at a given period of time.” DETERMINANTS OF DEMAND: 1. Price of the Commodity: The relation between price and demand is called the Law of Demand. It is not only the existing price but also the expected changes in price, which affect demand. 2. Income of the Consumer: The second most important factor influencing demand is consumer income. IThe demand for a normal commodity goes up when income rises and falls down when income falls. But in case of Giffen goods the relationship is the opposite. 3. Prices of related goods: The demand for a commodity is also affected by the changes in prices of the related goods also. Related goods can be of two types: (i). Substitutes which can replace each other in use; for example, tea and coffee are substitutes. The change in price of a substitute has effect on a commodity’s demand in the same direction in which price changes. The rise in price of coffee shall raise the demand for tea; (ii).Complementary foods are those which are jointly demanded, such as pen and ink. If the price of pens goes up, their demand is less as a result of which the demand for ink is also less. The price and demand go in opposite direction. The effect of changes in price of a commodity on amounts demanded of related commodities is called Cross Demand. 3. Tastes of the Consumers: The amount demanded also depends on consumer’s taste. Tastes include fashion, habit, customs, etc. A consumer’s taste is also affected by advertisement. If the taste for a commodity goes up, its amount demanded is more even at the same price. This is called increase in demand. The opposite is called decrease in demand. 4. Population: Increase in population increases demand for necessaries of life. A change in composition of population has an effect on the nature of demand for different commodities. 5. Government Policy: Government policy affects the demands for commodities through taxation. Taxing a commodity increases its price and the demand goes down. Similarly, financial help from the government increases the demand for a commodity while lowering its price. 6. Expectations Price in the future: If consumers expect changes in price of commodity in future, they will change the demand at present even when the present price remains the same. Similarly, if consumers expect their incomes to rise in the near future they may increase the demand for a commodity just now. 7. Climate and weather: The climate of an area and the weather prevailing there has a decisive effect on consumer’s demand. In cold areas woolen cloth is demanded. During hot summer days, ice is very much in demand. On a rainy day, ice cream is not so much demanded. LAW OF DEMAND Review Table 1 in Pre-Activity, It simply shows the relationship between price and quantity demanded of a commodity in the market. In the words of Marshall, the Law of Demand states “the amount demand increases with a fall in price and diminishes with a rise in price”. EXCEPTIONS TO THE LAW OF DEMAND: 1. Giffen Paradox: The Giffen good or inferior good is an exception to the law of demand. When the price of an inferior good falls, the poor will buy less and vice versa. For example, when the price of maize falls, the poor are willing to spend more on superior goods than on maize if the price of maize increases, he has to increase the quantity of money spent on it. 2. Veblen or Demonstration effect: ‘Veblan’ has explained the exceptional demand curve through his doctrine of conspicuous consumption. Rich people buy certain good because it gives social distinction or prestige for example diamonds are bought by the richer class for the prestige 3. Ignorance: Sometimes, the quality of the commodity is Judge by its price. Consumers think that the product is superior if the price is high. As such they buy more at a higher price. 4. Speculative effect: If the price of the commodity is increasing the consumers will buy more of it because of the fear that it increase still further, Thus, an increase in price may not be accomplished by a decrease in demand. 5. Fear of shortage: During the times of emergency of war People may expect shortage of a commodity. At that time, they may buy more at a higher price to keep stocks for the future. 6. Necessaries: In the case of necessaries like rice, vegetables etc. people buy more even at a higher price. DEMAND FUNCTION There are 2 forms to show the relationship between the quantity of good demanded and the price of that good, the Demand Schedule, if it is in a tabular form and Demand Curve if it is graphically illustrated. The mathematical expression of the Law of Demand or the relationship between price and quantity demanded is called Demand Function. The Demand Function Equation is Qd = a – bP, it was derived from the factors effecting the demand. Qd stands for Quantity demanded, where a is the intercept and b is the slope of the functions representing the determinants of demand and P stands for Price. Steps in finding the demand function of a given goods/services. Table 1. Demand Schedule for Shoes Price 1 2 3 4 5 Quantity Demanded 1000 800 600 400 200 1. Find the value of “b”. /𝑏 = ∆𝑄 ∆𝑃 / Where, ∆ means difference, Q is for quantity and P is for Price. Solutions: 𝑏= 𝑏= 800−1000 2−1 −200 1 𝑏 =/−200/ Therefore, the value of b is an absolute value of 200. Step 2. Using the demand function equation, Find the value of “a”. Just substitute the given price, quantity, and value of “b” for shoes. Solutions: Qd 1000 1000 1000+200 1200 = a – bP = a – 200 (1) = a – 200 =a =a Therefore, the value of c is 0. Step 3. Substitute the value of “a and b” to the demand function equation. Therefore, If the value of a is 1200 and b is 200. The demand function for shoes is Qd = 1200 – 200P. Step 4. To check if the demand function is correct. Substitute each price from the table to letter “P” in the demand function equation. Price 1 2 3 4 5 Solutions: Supposing the price is 5. Qd = 1200 – 200 (5) Qd = 1200 – 1000 Qd = 200 Quantity Demanded 1000 800 600 400 200 Practice 1: A. Find the Demand Function of the given data below. Find the missing value and show the solutions at the back of this paper. Price 30 25 20 15 10 5 Quantity Demanded 5 15 ? ? ? ? SUPPLY • Supply means the goods and services to produce. • This means that the supply becomes effective only it if is backed by producer in addition to this there must be willingness to create a commodity. • Thus supply has three essentials – price, quantity supplied, and time. SUPPLY vs QUANTITY SUPPLIED “Supply is defined as the maximum units/quantity of goods/services producers can offer.” “Quantity Supplied refers to the amount or quantity of goods/services producers are willing and able to supply at a given price, at a given period of time.” DETERMINANTS OF SUPPLY: 1. Technology - Better technology leads to higher productivity. This would lead to an INCREASE in supply. - When technology breaks or becomes unavailable, it leads to a DECREASE in supply. 2. Input Costs - Input costs refer to the costs of production inputs. (Think factors of production.) - If the cost of inputs rise, supply will DECREASE - If the cost of inputs falls, supply will INCREASE. 3. Prices of Other Goods that Could be Produced - Keep in mind that entrepreneurs seek to maximize profit. - If they see that the prices they can charge for other products are rising, they will have more incentive to produce those other products. What will happen to the supply of the products they are currently making? Supply will DECREASE. - An example: FARMING… If a farmer thinks he can sell soybeans for a higher price, he will DECREASE his supply of peanuts by planting more land in soybeans. 4. Taxes, Subsidies, and Regulations – all refer to the government’s impact on supply - Higher taxes – supply will DECREASE - Lower taxes – supply will INCREASE - Subsidies to businesses – supply will INCREASE - Subsidies to businesses removed – supply will DECREASE - More regulations – supply will DECREASE - Fewer regulations – supply will INCREASE 5. Expectation of Prices - If you think you can get a higher price in the future, CURRENT SUPPLY will DECREASE. - If you think you will get a lower price in the future, CURRENT SUPPLY will INCREASE. - Example: You make Christmas ornaments. You think you can get a higher price for your items in November and December. In February, your supply of ornaments will DECREASE but in November, your supply of ornaments will INCREASE. 6. Number of Sellers - More sellers in the market – supply will INCREASE - Some sellers go out of business and leave the market – supply will DECREASE. LAW OF SUPPLY Review Table 2 in Pre-Activity, It simply shows the relationship between price and quantity supplied of a commodity in the market. In the words of Marshall, the Law of Supply states “the amount supply increases with a rise in price and diminishes in supply, fall in price”. EXCEPTIONS TO THE LAW OF SUPPLY 1. Closure of business When a business is on the verge of closure, the seller may sell the goods even at low prices in order to clear the stock. Thus, in this case, the law of supply shall not hold true. 2. Agricultural products We know that land is a limited resource and thus the agricultural produce can also not be increased beyond a certain level. Hence, even if the prices increase the supply cannot be increased. 3. Monopoly Monopoly is a situation where there is only a single seller of a commodity. Thus, he is the price maker and has control over the prices. In such a case, the law of supply may not apply as he may not be willing to increase the supply even if the prices are high. 4. Competition When there is a cut-throat competition in the market, the sellers may sell more quantity of goods even at low prices. This is a situation where the law of supply will not apply. 5. Perishable Goods A seller is willing to sell more goods that are perishable in nature even at low prices because if they remain unsold they will yield only loss. 6. Rare goods The goods that are rare such as artistic or precious goods have a limited supply. The supply of these goods cannot be increased according to their demand or rising prices. Thus, even if their price increases their supply cannot be increased. In this case, also the law of supply shall not apply. 7. Out of fashion goods The latest goods that are in fashion have high prices. But, the out of fashion goods have low prices. The sellers may sell them out of fashion goods even at low prices. As these will become dead inventory and also in order to realize the amount invested in the inventory. SUPPLY FUNCTION There are 2 forms to show the relationship between the quantity of good supplied and the price of that good, the Supply Schedule, if it is in a tabular form and Supply Curve if it is graphically illustrated. The mathematical expression of the Law of Supply or the relationship between price and quantity supplied is called Supply Function. The Supply Function Equation is Qs = c + dP, it was derived from the factors effecting the supply. Qs stands for Quantity supplied, where c is the intercept and d is the slope of the functions representing the determinants of supply and P stands for Price. Steps in finding the supply function of a given goods/services. Table 2. Supply Schedule for Shoes Price 1 2 3 4 5 Quantity Supplied 200 400 600 800 1000 1. Find the value of “b”. ∆𝑄 /𝑑 = ∆𝑃 / Where, ∆ means difference, Q is for quantity and P is for Price. Solutions: 𝑏= 𝑏= 400−200 2−1 200 1 𝑏 =/200/ Therefore, the value of d is an absolute value of 200. Step 2. Using the supply function equation, Find the value of “c”. Just substitute the given price, quantity, and value of “d” for shoes. Solutions: Qs 200 200 200 - 200 0 = c + dP = c + 200 (1) = c + 200 =c =c Therefore, the value of c is 0. Step 3. Substitute the value of “c and d” to the supply function equation. Therefore, If the value of a is 1200 and b is 200. The demand function for shoes is Qs = 0 + 200P. Step 4. To check if the supply function is correct. Substitute each price from the table to letter “P” in the supply function equation. Price 1 2 3 4 5 Solutions: Supposing the price is 5. Qs = 0 + 200 (5) Qs = 0 + 1000 Qs = 1000 Quantity Supplied 200 400 600 800 1000 Practice 2: A. Find the Supply Function of the given data below. Find the missing value and show the solutions at the back of this paper. Price 30 25 20 15 10 5 Quantity Supplied 60 50 ? ? ? ? DETERMINATION OF MARKET EQUILIBRIUM A condition which implies a balance between demand and supply is known as Market Equilibrium. It is determined by the intersection of the demand and supply curves. Let us combine the hypothetical data used in the pre-activity. Price Quantity Supplied 20 Status of Market Pressure in Price 1 Quantity Demanded 100 (-80) Shortage Upward 2 80 40 (-40) Shortage Upward 3 60 60 (0) Equal Neutral/Equal 4 40 80 (40) Surplus Downward 5 20 100 (80) Surplus Downward Market Equilibrium of Demand and Supply 120 100 Surplus 80 Equilibrium 60 40 Shortage 20 0 1 2 Quantity Demanded 3 Quantity Supplied 4 5 Column1 As discussed earlier, market is in equilibrium when quantity demanded equals quantity supplied or the Qd intersects with Qs at a particular point. Given the demand and supply function, the equilibrium price and quantity can derived. Let is examine the equilibrium point in the previous examples of demand and supply schedule for shoes and equate the two, that is; Qd = Qs 1200 – 200P = 0 + 200P Transposing the similar terms, 1200 – 200P = 0 + 200P 1200 1200 400 = 200P + 200P = 400P 400 3 = P Hence, the equilibrium price is 3. By substituting the equilibrium price into the demand and supply function, equilibrium quantity can be derived. Qd = Qs 1200 – 200(3) = 0 + 200(3) 1200 – 600 = 0 + 600 600 = 600 Hence, the equilibrium quantity is 600. Price 1 2 3 4 5 Quantity Demanded 1000 800 600 400 200 Quantity Supplied 200 400 600 800 1000 Market Status Shortage (-800) Shortage (-400) Equilibrium (0) Surplus (400) Surplus (800) Practice 3: A. Using the demand and supply function you discovered from Practice 1 and 2. Find the equilibrium Price and Quantity of the given data below and show the solutions at the back of this paper. Price Quantity Demanded Quantity Supplied 30 25 5 15 60 50 LEARNING ENHANCEMENT Task A. REFLECTION # 2 Summarize Chapter 2. Discuss what have you learned from this chapter. _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________ __________________________________________________________________________________________. Rubrics for Reflection: Features 15 12 8 Quality of Writing It was written in extraordinary style, It was written in interesting It was written in little very informative and well organized style, somewhat informative style, little informative and organized and poorly organized Grammar Usage No wrong spelling, punctuations or grammatical errors. 7 It was written in poor style, not informative and poorly organized Few wrong spelling, A number of wrong So many wrong punctuations or grammatical spelling, punctuations or spelling, errors. grammatical errors punctuations or grammatical errors Task B. Using the hypothetical table below, Complete the table and solve the following: a. Demand and Supply Function b. Equilibrium Quantity and Price c. Plot the table. Price QD QS 5 60 20 10 50 30 (per ballpen) 15 20 25 State of Market Pressure of Price