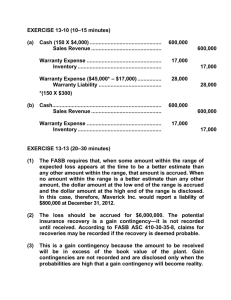

Extended Warranty Co. S sells televisions for $900 and offers a three year extended warranty for $90. During 2017 300 televisions and 270 warranties contracts for cash. Estimated warranty costs--$20 parts and $40 labor. Warranty revenue recognized on a straight line basis. 2017 warranty costs= $2,000 for parts and $4,000 for labor. (a) (b) Cash 294,300 Sales Revenue (300 X $900) .............................................. 270,000 Unearned Warranty Revenue (270 X $90) ............................. 24,300 Current Liabilities: Unearned Warranty Revenue ($24,300/3) ......................... $ 8,100 Long-term Liabilities: Unearned Warranty Revenue ($24,300 X 2/3) ............................................................... (c) Unearned Warranty Revenue ......................................................... $16,200 8,100 Warranty Revenue .............................................................. Warranty Expense .......................................................................... 8,100 6,000 Inventory ............................................................................ 2,000 Salaries and Wages Payable ............................................... 4,000 (d) Current Liabilities: Unearned Warranty Revenue ............................................. $ 8,100 Long-term Liabilities: Unearned Warranty Revenue ............................................. $ 8,100 Compensated Absences Co. X began operations on Jan. 1, 2016. It employs 9 individuals who work 8 hours a day and paid hourly. Each employee earns 10 paid vacation days and 6 paid sick days annually. Vacation days are taken the year after earned. Sick days taken when earned; unused sick days accumulate. Hourly rate—2016-$10; 2017-$11 Vacation Days used—2016-0; 2017—9 Sick days used-2016—4; 2017—5 (a) 2016 To accrue expense and liability for vacations Salaries and Wages Expense ................................................... 7,200 Salaries and Wages Payable ........................................ 7,200 (1) To accrue the expense and liability for sick pay Salaries and Wages Expense ................................................... Salaries and Wages Payable ........................................ To record payment for compensated time when used by employees 4,320 (2) 4,320 Salaries and Wages Payable .................................................... 2,880 (3) Cash ............................................................................. 2,880 2017 To accrue the expense and liability for vacations Salaries and Wages Expense ................................................... 7,920 Salaries and Wages Payable ........................................ 7,920 (4) To accrue the expense and liability for sick pay Salaries and Wages Expense ................................................... 4,752 Salaries and Wages Payable ........................................ 4,752 (5) To record vacation time paid Salaries and Wages Expense ................................................... Salaries and Wages Payable .................................................... 648 6,480 (6) Cash ............................................................................. 7,128 (7) To record sick leave paid Salaries and Wages Expense ................................................... Salaries and Wages Payable .................................................... Cash ............................................................................. 144 3,816 (8) 3,960 (9) (1) 9 employees X $10.00/hr. X 8 hrs./day X 10 days = $7,200 (2) 9 employees X $10.00/hr. X 8 hrs./day X 6 days = $4,320 (3) 9 employees X $10.00/hr. X 8 hrs./day X 4 days = $2,880 (4) 9 employees X $11.00/hr. X 8 hrs./day X 10 days = $7,920 (5) 9 employees X $11.00/hr. X 8 hrs./day X 6 days = $4,752 (6) 9 employees X $10.00/hr. X 8 hrs./day X 9 days = $6,480 (7) 9 employees X $11.00/hr. X 8 hrs./day X 9 days = $7,128 (8) 9 employees X $10.00/hr. X 8 hrs./day X (6–4) days = 9 employees X $11.00/hr. X 8 hrs./day X (5–2) days (9) 9 employees X $11.00/hr. X 8 hrs./day X 5 days $1,440 = $2,376 = $3,816 $3,960 Current/ Noncurrent Classification of Debt On February 10, 2014, after issuance of its financial statements for 2013, Higgins Company entered into a financing agreement with Cleveland Bank, allowing Higgins Company to borrow up to $6,000,000 at any time through 2016. Amounts borrowed under the agreement bear interest at 2% above the bank's prime interest rate and mature two years from the date of loan. Higgins Company presently has $2,250,000 of notes payable with Star National Bank maturing March 15, 2014. The company intends to borrow $3,750,000 under the agreement with Cleveland and liquidate the notes payable to Star National Bank. The agreement with Cleveland also requires Higgins to maintain a working capital level of $9,000,000 and prohibits the payment of dividends on common stock without prior approval by Cleveland Bank. From the above information only, the total short-term debt of Higgins Company as of the December 31, 2013 balance sheet date is $2,250,000. On December 31, 2014, Isle Co. has $4,000,000 of short-term notes payable due on February 14, 2015. On January 10, 2013, Isle arranged a line of credit with Beach Bank which allows Isle to borrow up to $3,000,000 at one percent above the prime rate for three years. On February 2, 2015, Isle borrowed $2,400,000 from Beach Bank and used $1,000,000 additional cash to liquidate $3,400,000 of the short-term notes payable. The amount of the short-term notes payable that should be reported as current liabilities on the December 31, 2014 balance sheet which is issued on March 5, 2015 is: $4,000,000 - $2,400,000 = $1,600,000 Use the following information for next two questions Posner Co. is a retail store operating in a state with a 7% retail sales tax. The retailer may keep 2% of the sales tax collected. Posner Co. records the sales tax in the Sales Revenue account. The amount recorded in the Sales Revenue account during May was $251,450. The amount of sales taxes (to the nearest dollar) for May is: 251,450/1.07 = 235,000; $251,450 - $235,000 = 16,450 The amount of sales taxes payable (to the nearest dollar) to the state for the month of May is16,450 x .98 = 16,121 Sales revenue………….16,450 Cash……………………………………..............16,121 Revenue from collection of taxes …….. 329 Valley, Inc., is a retail store operating in a state with a 5% retail sales tax. The state law provides that the retail sales tax collected during the month must be remitted to the state during the following month. If the amount collected is remitted to the state on or before the twentieth of the following month, the retailer may keep 3% of the sales tax collected. On April 10, 2014, Valley remitted $135,800 tax to the state tax division for March 2014 retail sales. What was Valley's March 2012 retail sales subject to sales tax? .05S x .97 = 135,800; 135,800/.0485 = 2,800,000 . Jump Corporation has $2,500,000 of short-term debt it expects to retire with proceeds from the sale of 85,000 shares of common stock. If the stock is sold for $20 per share subsequent to the balance sheet date, but before the balance sheet is issued, what amount of short-term debt could be excluded from current liabilities? 8,500 x 20 = 2,500,000 - 1,700,000 =800,000 Current Liability and1,700,000 noncurrent In 2014, Pollard Corporation began selling a new line of products that carry a two-year warranty against defects. Based upon past experience with other products, the estimated warranty costs related to dollar sales are as follows: First year of warranty 3% Second year of warranty 5% Sales and actual warranty expenditures for 2014 and 2015 are presented below: 2014 Sales Actual warranty expenditures 2015 $500,000 $700,000 30,000 50,000 What is the estimated warranty liability at the end of 2015?(assume the accrual method) 2014 Warranty expense………30,000 Parts Inventory…………………..25,000 Salaries payable……………………5,000 Warranty expense (40,000-30,000)……..10,000 Est. Warranty Liability………………………………………10,000 500,000 x .08 = 40,000 – 30,000 = 10,000 beg liability 2015 + 700,000 x .08 – 50,000 = 16,000 Flavor Food Company distributes to consumers coupons which may be presented (on or before a stated expiration date) to grocers for discounts on certain products of Flavor. The grocers are reimbursed when they send the coupons to Flavor. In Flavor's experience, 50% of such coupons are redeemed, and generally one month elapses between the date a grocer receives a coupon from a consumer and the date Flavor receives it. During 2014 Flavor issued two separate series of coupons as follows: Consumer Amount Disbursed Total Value Expiration Date as of 12/31/14 1/1/14 $500,000 6/30/14 $236,000 7/1/14 720,000 12/31/14 300,000 Issued On The only journal entry recorded to date is: debit to coupon expense and credit to cash of $715,000. The December 31, 2014 balance sheet should include a liability for unredeemed coupons of: $720,000 x .5 = 360,000 – 300,000 = 60,000 During 2014, Eaton Co. introduced a new product carrying a two-year warranty against defects. The estimated warranty costs related to dollar sales are 2% within 12 months following sale and 3% in the second 12 months following sale. Sales and actual warranty expenditures for the years ended December 31, 2014 and 2015 are as follows: Actual Warranty Sales Expenditures 2014 $ 800,000 $12,000 2015 1,000,000 35,000 $1,800,000 $47,000 At December 31, 2015, $1,800,000 x .05 = 90,000 – 47,000 = 43,000 In March 2015, an explosion occurred at Kirk Co.'s plant, causing damage to area properties. By May 2015, no claims had yet been asserted against Kirk. However, Kirk's management and legal counsel concluded that it was reasonably possible that Kirk would be held responsible for negligence, and that $4,000,000 would be a reasonable estimate of the damages. Kirk's $5,000,000 comprehensive public liability policy contains a $400,000 deductible clause. In Kirk's December 31, 2014 financial statements, for which the auditor's fieldwork was completed in April 2015, how should this casualty be reported? As a note disclosing a possible liability of $400,000. Neer Co. has a probable loss that can only be reasonably estimated within a range of outcomes. No single amount within the range is a better estimate than any other amount. The loss accrual should be: the minimum of the range.