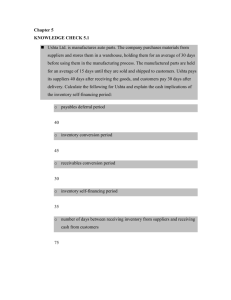

Question (1) Menzzies Ltd provided the following information for the year ended 31 March 2017. Additional information • • • • On 31 March 2017 inventory was valued at $5 175 000. This included damaged inventory of $200 000. The damaged inventory can be sold for $150 000 after repairs at a cost of $40 000 Depreciation policy • The depreciation on buildings was to be charged at 5% per annum on a straight line basis. • Land is not depreciated. During the year, land costing $2 000 000 was revalued to $2 500 000. This had not been included in the books. • The depreciation on plant and machinery was to be charged at 20% per annum on a reducing (diminishing) balance basis. • Depreciation was to be apportioned equally between distribution costs and administrative expenses. Trade receivables included a debt of $10 000, which was to be written off. At 31 March 2017: • distribution costs of $8 000 were owing • administrative expenses included prepaid insurance of $15 000 • interest on the 5% bank loan was owing for the year • tax for the year was $400 000 Required: (a) State which accounting standard must be followed when preparing a statement of profit or loss. (b) Prepare the statement of profit or loss for the year ended 31 March 2017. Question (2) Shopton Ltd provided the following information for the year ended 30 June 2017 $ At 1 July 2016 Land and Buildings Cost 450,000 Accumulated Depreciation 50,000 Motor Vehicles Cost 375,000 Accumulated Depreciation 209,880 Retained earnings 121,651 General reserves 26,000 At 30 June 2017 15% Bank loan (2022) 50,000 Allowance for doubtful debts 12,500 Cash and Cash equivalents 12,325 Closing inventory 45,000 Dividend paid 25,000 Profit for the year 44,920 Share capital (Ordinary share at $1 each) 350,000 Trade and other payables 50,000 Trade and other receivables 92,500 Depreciation for the year ended 30 June 2017 was charged as follows: Non-Current Assets Land and Buildings Depreciation Method 5% per annum straight line. Land is not depreciated Motor Vehicles 20% per annum reducing (diminishing) balance Adjustment Land originally costing $250,000 was revalued to $300,000. A motor vehicle costing $50,000 with accumulated depreciation of $18,000 was sold for $33,250. A motor vehicle costing $75,000 was purchased. A full year’s depreciation is charged in the year of acquisition and none in the year of disposal. • $15,000 was transferred to general reserve. • Profit for the year ended 30 June 2017 did not account for the following: • Damaged goods, included in the inventory, costing $5,000, which could be sold for $4,500 after repairs at a cost of $350. • Three months’ interest on the 15% bank loan owing. • Profit and loss on disposal of motor vehicle. Required: (a) Calculate the adjusted profit for the year ended 30 June 2017. (b) Prepare the statement of financial position as at 30 June 2017.