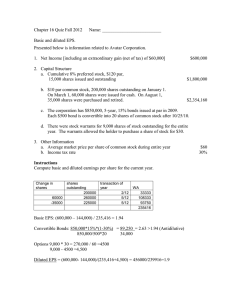

Intermediate Accounting, 16e Chapter 16 Homework Dilutive Securities and Earnings Per Share ACTG 382

advertisement

Brief Exercise 16-1 Indigo Inc. issued $4,190,000 par value, 7% convertible bonds at 95 for cash. If the bonds had not included the conversion feature, they would have sold for 95. Prepare the journal entry to record the issuance of the bonds. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Cash 3,980,500 Discount on B 209,500 Bonds Payable Credit 4,190,000 Brief Exercise 16-2 Bonita Corporation has outstanding 1,800 $1,000 bonds, each convertible into 60 shares of $10 par value common stock. The bonds are converted on December 31, 2017, when the unamortized discount is $26,900 and the market price of the stock is $21 per share. Record the conversion using the book value approach. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Bonds Payable Debit Credit 1,800,000 Paid-in Capital 693,100 Common Stock 1,080,000 Discount on B 26,900 Common Stock = (1,800 × 60 × $10) = $1,080,000 Brief Exercise 16-3 Blossom Corporation issued 2,200 shares of $10 par value common stock upon conversion of 1,100 shares of $50 par value preferred stock. The preferred stock was originally issued at $56 per share. The common stock is trading at $27 per share at the time of conversion. Record the conversion of the preferred stock. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Preferred Stoc 55,000 Paid-in Capital 6,600 Credit Common Stock 22,000 Paid-in Capital 39,600 Preferred Stock = (1,100 × $50) = $55,000 Paid-in Capital in Excess of Par—Preferred Stock = ($56 – $50) × 1,100 = $6,600 Common Stock = (2,200 × $10) = $22,000 Paid-in Capital in Excess of Par—Common Stock = ($56 × 1,100) – (2,200 × $10) = $39,600 Brief Exercise 16-4 Larkspur Corporation issued 2,200 $1,000 bonds at 103. Each bond was issued with one detachable stock warrant. After issuance, the bonds were selling in the market at 98, and the warrants had a market price of $45. Use the proportional method to record the issuance of the bonds and warrants. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Round intermediate calculations to 5 decimal places, e.g. 1.24687 and final answers to 0 decimal places, e.g. 5,125.) Account Titles and Explanation Debit Cash 2,266,000 Discount on B 33,483 Credit Paid-in Capital 99,483 Bonds Payable 2,200,000 Discount on Bonds Payable = ($2,200,000 – $2,166,517) = $33,483 Fair value of bonds (2,200 × $1,000 × 0.98) Fair value of warrants (2,200 × $45) $2,156,000 99,000 Aggregate fair value $2,255,000 Allocated to bonds [($2,156,000/$2,255,000) × $2,266,000] $2,166,517 Allocated to warrants [($99,000/$2,255,000) × $2,266,000] 99,483 $2,266,000 Brief Exercise 16-5 Waterway Corporation issued 1,800 $1,000 bonds at 101. Each bond was issued with one detachable stock warrant. After issuance, the bonds were selling separately at 98. The market price of the warrants without the bonds cannot be determined. Use the incremental method to record the issuance of the bonds and warrants. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Cash 1,818,000 Discount on B 36,000 Credit Paid-in Capital 54,000 Bonds Payable 1,800,000 Discount on Bonds Payable = [$1,800,000 × (1 – 0.98)] = $36,000 Paid-in Capital—Stock Warrants = [$1,800,000 × (1.01 – 0.98)] = $54,000 Brief Exercise 16-6 On January 1, 2017, Splish Corporation granted 5,300 options to executives. Each option entitles the holder to purchase one share of Splish’s $5 par value common stock at $50 per share at any time during the next 5 years. The market price of the stock is $60 per share on the date of grant. The fair value of the options at the grant date is $160,000. The period of benefit is 2 years. Prepare Splish’s journal entries for January 1, 2017, and December 31, 2017 and 2018. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date Account Titles and Explanation Debit Credit 1/1/17 No Entry 0 No Entry 12/31/17 Compensation 0 80,000 Paid-in Capital 12/31/18 Compensation 80,000 80,000 Paid-in Capital 80,000 Brief Exercise 16-7 On January 1, 2017, Riverbed Corporation granted 2,200 shares of restricted $5 par value common stock to executives. The market price (fair value) of the stock is $63 per share on the date of grant. The period of benefit is 2 years. Prepare Riverbed’s journal entries for January 1, 2017, and December 31, 2017 and 2018. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date 1/1/17 12/31/17 Account Titles and Explanation Unearned Com Debit 138,600 Common Stock 11,000 Paid-in Capital 127,600 Compensation 69,300 Unearned Com 12/31/18 Credit Compensation Unearned Com 69,300 69,300 69,300 1/1/17 Common Stock = (2,200 × $5) = $11,000 Paid in Capital in Excess of Par—Common Stock = [($63 – $5) × 2,200] = $127,600 Unearned Compensation = (2,200 × $63) = $138,600 Brief Exercise 16-8 On January 1, 2017 (the date of grant), Pronghorn Corporation issues 2,000 shares of restricted stock to its executives. The fair value of these shares is $102,000, and their par value is $10,000. The stock is forfeited if the executives do not complete 3 years of employment with the company. Prepare journal entries for January 1, 2017, and on December 31, 2017, assuming the service period is 3 years. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date 1/1/17 12/31/17 Account Titles and Explanation Unearned Com Debit Credit 102,000 Common Stock 10,000 Paid-in Capital 92,000 Compensation 34,000 Unearned Com 34,000 12/31/17 Unearned Compensation = ($102,000 ÷ 3) = $34,000 Brief Exercise 16-9 Sheridan Corporation had 2017 net income of $1,017,000. During 2017, Sheridan paid a dividend of $2 per share on 244,500 shares of preferred stock. During 2017, Sheridan had outstanding 176,000 shares of common stock. Compute Sheridan’s 2017 earnings per share. (Round answer to 2 decimal places, e.g. 3.56.) Earnings per share $ 3.00 per share $1,017,000 – (244,500 × $2) = $3.00 per share 176,000 shares Brief Exercise 16-10 Sandhill Corporation had 116,400 shares of stock outstanding on January 1, 2017. On May 1, 2017, Sandhill issued 63,600 shares. On July 1, Sandhill purchased 9,120 treasury shares, which were reissued on October 1. Compute Sandhill’s weighted-average number of shares outstanding for 2017. Weighted-average number of shares outstanding $ 156,520 Dates Shares Fraction Weighted Outstanding Outstanding of Year Shares 1/1–5/1 116,400 4/12 38,800 5/1–7/1 180,000 2/12 30,000 7/1–10/1 170,880 3/12 42,720 10/1–12/31 180,000 3/12 45,000 $156,520 Brief Exercise 16-11 Bramble Corporation had 291,000 shares of common stock outstanding on January 1, 2017. On May 1, Bramble issued 31,200 shares. (a) Compute the weighted-average number of shares outstanding if the 31,200 shares were issued for cash. Weighted-average number of shares outstanding $ 311,800 (b) Compute the weighted-average number of shares outstanding if the 31,200 shares were issued in a stock dividend. Weighted-average number of shares outstanding $ 322,200 (a) (291,000 × 4/12) + (322,200 × 8/12) = $311,800 (b) $322,200 (The 31,200 shares issued in the stock dividend are assumed outstanding from the beginning of the year.) Either add 31,200 to 291,000 and multiply by the fraction of the year or find the percent of the stock dividend. Stock dividend %: (31,200 / 291,000) Dates Outstanding 1/1-5/1 Shares Outstanding 291,000 Fraction of Year 4/12 Stock Dividend Weighted Shares (1+(31,200/291,000)) 107,400 5/1-12/31 322,200 8/12 - 214,800 322,200 Brief Exercise 16-12 The 2017 income statement of Marigold Corporation showed net income of $476,000 and a loss from discontinued operations of $114,000. Marigold had 100,000 shares of common stock outstanding all year. Prepare Marigold’s income statement presentation of earnings per share. (Round answers to 2 decimal places, e.g. 3.55.) Marigold Corporation Income Statement For the Year Ended December 31, 2017 Earnings Per Share $ Income from Continuing Operations 5.90 Discontinued Operations (Loss) 1.14 $ Net Income / (Loss) 4.76 Income from continuing operations = ($590,000/100,000) = $5.90 Discontinued operations (loss) = ($114,000/100,000) = ($1.14) Net income = ($476,000/100,000) = $4.76 Brief Exercise 16-13 Crane Corporation earned net income of $370,000 in 2017 and had 108,000 shares of common stock outstanding throughout the year. Also outstanding all year was $840,000 of 9% bonds, which are convertible into 20,000 shares of common. Crane’s tax rate is 40 percent. Compute Crane’s 2017 diluted earnings per share. (Round answer to 2 decimal places, e.g. 3.55.) Diluted earnings per share Net income $ 3.25 $370,000 Adjustment for interest, net of tax [$75,600* × (1 – 0.40)] 45,360 Adjusted net income $415,360 Weighted-average number of shares outstanding adjusted for dilutive securities (108,000 + 20,000) ÷128,000 Diluted EPS $3.25 *$840,000 x 0.09 Brief Exercise 16-14 Wildhorse Corporation reported net income of $338,000 in 2017 and had 54,200 shares of common stock outstanding throughout the year. Also outstanding all year were 5,400 shares of cumulative preferred stock, each convertible into 2 shares of common. The preferred stock pays an annual dividend of $5 per share. Wildhorse’s tax rate is 30%. Compute Wildhorse’s 2017 diluted earnings per share. (Round answer to 2 decimal places, e.g. 3.55.) Diluted earnings per share $ 5.20 Net income $338,000 Weighted-average number of shares adjusted for dilutive securities (54,200 + 10,800) ÷ 65,000 Diluted EPS $5.20 Net income=$338,000-27,000+27,000 Brief Exercise 16-15 Marigold Corporation reported net income of $374,500 in 2017 and had 198,000 shares of common stock outstanding throughout the year. Also outstanding all year were 48,000 options to purchase common stock at $10 per share. The average market price of the stock during the year was $15. Compute diluted earnings per share. (Round answer to 2 decimal places, e.g. 3.55.) Diluted earnings per share $ 1.75 Proceeds from assumed exercise of 48,000 options (48,000 × $10) $480,000 Shares issued upon exercise 48,000 Treasury shares purchasable ($480,000 ÷ $15) Incremental shares Diluted EPS = $374,500 198,000 + 16,000 (32,000) 16,000 = $1.75 Exercise 16-1 For each of the unrelated transactions described below, present the entries required to record each transaction. 1. Pronghorn Corp. issued $20,300,000 par value 10% convertible bonds at 98. If the bonds had not been convertible, the company’s investment banker estimates they would have been sold at 95. 2. Stellar Company issued $20,300,000 par value 10% bonds at 97. One detachable stock purchase warrant was issued with each $100 par value bond. At the time of issuance, the warrants were selling for $5. 3. Suppose Sepracor, Inc. called its convertible debt in 2017. Assume the following related to the transaction. The 11%, $9,500,000 par value bonds were converted into 950,000 shares of $1 par value common stock on July 1, 2017. On July 1, there was $50,000 of unamortized discount applicable to the bonds, and the company paid an additional $79,000 to the bondholders to induce conversion of all the bonds. The company records the conversion using the book value method. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) No. Account Titles and Explanation 1. Debit Cash 19,894,000 Discount on B 406,000 Bonds Payable 2. 3. Credit 20,300,000 Cash 19,691,000 Discount on B 1,624,000 Paid-in Capital 1,015,000 Bonds Payable 20,300,000 Bonds Payable 9,500,000 Debt Conversi 79,000 Paid-in Capital 8,500,000 Common Stock 950,000 Cash 79,000 Discount on B 50,000 1. Cash = ($20,300,000 × 0.98) = $19,894,000 2. Value of bonds plus warrants ($20,300,000 × 0.97) $19,691,000 Value of warrants (203,000 × $5) (1,015,000) Value of bonds $18,676,000 3. Paid-in Capital in Excess of Par—Common Stock = [($9,500,000 – $50,000) – $950,000] = $8,500,000 Exercise 16-4 On January 1, 2016, when its $30 par value common stock was selling for $80 per share, Grouper Corp. issued $10,600,000 of 8% convertible debentures due in 20 years. The conversion option allowed the holder of each $1,000 bond to convert the bond into five shares of the corporation’s common stock. The debentures were issued for $11,448,000. The present value of the bond payments at the time of issuance was $9,010,000, and the corporation believes the difference between the present value and the amount paid is attributable to the conversion feature. On January 1, 2017, the corporation’s $30 par value common stock was split 2 for 1, and the conversion rate for the bonds was adjusted accordingly. On January 1, 2018, when the corporation’s $15 par value common stock was selling for $135 per share, holders of 30% of the convertible debentures exercised their conversion options. The corporation uses the straight-line method for amortizing any bond discounts or premiums. (a) Prepare the entry to record the original issuance of the convertible debentures. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Cash Debit Credit 11,448,000 Premium on Bo 848,000 Bonds Payable 10,600,000 (b) Prepare the entry to record the exercise of the conversion option, using the book value method. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Credit Bonds Payable 3,180,000 Premium on Bo 228,960 Common Stock 477,000 Paid-in Capital 2,931,960 (b) Schedule 1 Computation of Unamortized Premium on Bonds Converted Premium on bonds payable on January 1, 2016 $848,000 Amortization for 2016 ($848,000 ÷ 20) $42,400 Amortization for 2017 ($848,000 ÷ 20) 42,400 84,800 Premium on bonds payable on January 1, 2018 Bonds converted Unamortized premium on bonds converted 763,200 × 30% $228,960 Schedule 2 Computation of Common Stock Resulting from Conversion Number of shares convertible on January 1, 2016: Number of bonds ($10,600,000 ÷ $1,000) 10,600 Number of shares for each bond ×5 Stock split on January 1, 2017 Number of shares convertible after the stock split % of bonds converted Number of shares issued Par value/per share Total par value 53,000 ×2 106,000 × 30% 31,800 × $15 $477,000 Exercise 16-9 On May 1, 2017, Nash Company issued 2,500 $1,000 bonds at 102. Each bond was issued with one detachable stock warrant. Shortly after issuance, the bonds were selling at 98, but the fair value of the warrants cannot be determined. (a) Prepare the entry to record the issuance of the bonds and warrants. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Cash 2,550,000 Discount on B 50,000 Credit Paid-in Capital 100,000 Bonds Payable 2,500,000 (b) Assume the same facts as part (a), except that the warrants had a fair value of $28. Prepare the entry to record the issuance of the bonds and warrants. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Round intermediate calculations to 5 decimal places, e.g. 1.24687 and final answers to 0 decimal places, e.g. 5,125.) Account Titles and Explanation Debit Cash 2,550,000 Discount on B 20,833 Credit Paid-in Capital 70,833 Bonds Payable 2,500,000 (a) Cash = ($2,500,000 × 1.02) = $2,550,000 Discount on Bonds Payable = [(1 – 0.98) × $2,500,000] = $50,000 Paid-in Capital—Stock Warrants = $2,550,000 – ($2,500,000 × 0.98) = $100,000 (b) Market value of bonds without warrants ($2,500,000 × 0.98) $2,450,000 Market value of warrants (2,500 × $28) 70,000 Total market value $2,520,000 $2,450,000 $2,520,000 × $2,550,000 = $2,479,167 Value assigned to bonds $70,000 $70,833 Value assigned to warrants × $2,550,000 = $2,520,000 $2,550,000 Total value assigned Exercise 16-11 On January 1, 2018, Oriole Inc. granted stock options to officers and key employees for the purchase of 17,000 shares of the company’s $10 par common stock at $23 per share. The options were exercisable within a 5-year period beginning January 1, 2020, by grantees still in the employ of the company, and expiring December 31, 2024. The service period for this award is 2 years. Assume that the fair value option-pricing model determines total compensation expense to be $363,600. On April 1, 2019, 1,700 options were terminated when the employees resigned from the company. The market price of the common stock was $34 per share on this date. On March 31, 2020, 10,200 options were exercised when the market price of the common stock was $39 per share. Prepare journal entries to record issuance of the stock options, termination of the stock options, exercise of the stock options, and charges to compensation expense, for the years ended December 31, 2018, 2019, and 2020. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date Jan. 1, 2018 Account Titles and Explanation No Entry Debit 0 No Entry Dec. 31, 2018 Compensation 0 181,800 Paid-in Capital April 1, 2019 Paid-in Capital 181,800 18,180 Compensation Dec. 31, 2019 Compensation 18,180 163,620 Paid-in Capital Mar. 31, 2020 163,620 Cash 234,600 Paid-in Capital 218,160 Common Stock Credit 102,000 Paid-in Capital 350,760 12/31/18 Paid-in Capital—Stock Options = ($363,600 × 1/2) 4/1/19 Compensation Expense = $181,800 = ($181,800 × 1,700/17,000) = $18,180 12/31/19 Paid-in Capital—Stock Options = ($363,600 × 1/2 × 18/20) 3/31/20 = $163,620 Cash = (10,200 × $23) = $234,600 Paid-in Capital—Stock Options = ($363,600 × 10,200/17,000) = $218,160 Note: There are 5,100 options unexercised as of March 31, 2020 (17,000 – 1,700 – 10,200) Exercise 16-13 Sandhill Company issues 4,200 shares of restricted stock to its CFO, Dane Yaping, on January 1, 2017. The stock has a fair value of $131,000 on this date. The service period related to this restricted stock is 4 years. Vesting occurs if Yaping stays with the company for 4 years. The par value of the stock is $6. At December 31, 2018, the fair value of the stock is $143,000. (a) Prepare the journal entries to record the restricted stock on January 1, 2017 (the date of grant), and December 31, 2018. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date 1/1/17 12/31/18 Account Titles and Explanation Unearned Com Debit Credit 131,000 Common Stock 25,200 Paid-in Capital 105,800 Compensation 32,750 Unearned Com 32,750 (b) On March 4, 2019, Yaping leaves the company. Prepare the journal entry to account for this forfeiture. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Date Account Titles and Explanation Debit Credit 3/4/19 Common Stock 25,200 Paid-in Capital 105,800 Compensation 65,500 Unearned Com 65,500 (a) 1/1/17 Common Stock = (4,200 × $6) = $25,200 12/31/18 Unearned Compensation = ($131,000 ÷ 4) = $32,750 (b) 3/4/19 Compensation Expense = (2 × $32,750) = $65,500 Exercise 16-23 On June 1, 2015, Shamrock Company and Bridgeport Company merged to form Indigo Inc. A total of 769,000 shares were issued to complete the merger. The new corporation reports on a calendar-year basis. On April 1, 2017, the company issued an additional 580,000 shares of stock for cash. All 1,349,000 shares were outstanding on December 31, 2017. Indigo Inc. also issued $600,000 of 20-year, 8% convertible bonds at par on July 1, 2017. Each $1,000 bond converts to 40 shares of common at any interest date. None of the bonds have been converted to date. Indigo Inc. is preparing its annual report for the fiscal year ending December 31, 2017. The annual report will show earnings per share figures based upon a reported after-tax net income of $1,577,000. (The tax rate is 40%.) Determine the following for 2017. (a) The number of shares to be used for calculating: (Round answers to 0 decimal places, e.g. $2,500.) (1) Basic earnings per share 1,204,000 shares (2) Diluted earnings per share 1,216,000 shares (b) The earnings figures to be used for calculating: (Round answers to 0 decimal places, e.g. $2,500.) (1) Basic earnings per share (2) Diluted earnings per share $ 1,577,000 $ 1,591,400 (a) (1) Number of shares for basic earnings per share. Shares Fraction Weighted Outstanding of Year Shares Jan. 1–April 1 769,000 3/12 192,250 April 1–Dec. 31 1,349,000 9/12 1,011,750 Weighted-average number of shares outstanding 1,204,000 Dates Outstanding OR Number of shares for basic earnings per share: Initial issue of stock 769,000 shares April 1, 2017 issue (3/4 × 580,000) 435,000 shares Total 1,204,000 shares (2) Number of shares for diluted earnings per share: Dates Outstanding Shares Fraction Weighted Outstanding of Year Shares Jan. 1–April 1 769,000 3/12 192,250 April 1–July 1 1,349,000 3/12 337,250 July 1–Dec. 31 1,373,000* 6/12 686,500 Weighted-average number of shares outstanding 1,216,000 *1,349,000 + [($600,000 ÷ 1,000) × 40] = $1,373,000 (b) (1) Earnings for basic earnings per share: After-tax net income $1,577,000 (2) Earnings for diluted earnings per share: After-tax net income $1,577,000 Add back interest on convertible bonds (net of tax): Interest ($600,000 × 8% × 1/2) $24,000 Less income taxes (40%) 9,600 14,400 Total $1,591,400