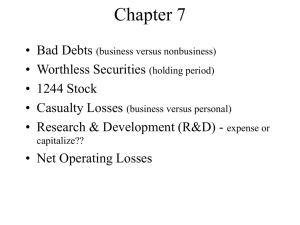

Chapter 6: Losses and Loss Limitations Brief Introduction Notes: Losses are treated as negative gains There are five reasons congress treats losses and gain differently: o Congress often seeks to prevent taxpayers from sheltering certain types of income or gains with other types of deductions or losses o Some loss limitations deny deductions to higher-income taxpayers out of fairness idea o Congress attempts to prevent excessive income shifting across tax years o Denying losses increases government revenues o The measure of taxable income for individuals generally excludes personal losses I. Bad Debts What is a bad debt? o It is a debt that is not repaid An accrual basis taxpayer can deduct a bad debt; however, a cash basis taxpayer cannot because no income is reported until the cash has been collected. If you permitted a deduction to a cash basis taxpayer, then that would essentially be a double deduction because the expenses are not inputted until cash has been received. A cash basis taxpayer cannot deduct a bad debt expense because income was never recognized. a. Specific Charge-off Method i. Using this method, you can claim the business debt when it becomes either partially or wholly worthless. 1. If a business debt that was claimed at partially worthless was deducted in the year prior, it can be completely deducted for the remaining portion if it became worthless in the current year. ii. A nonbusiness debt must be wholly worthless to deduct it iii. For both types of charge-off’s the taxpayer must have proof of the insolvency a. Examples of specific charge of method i. If a debt is owed to a company, but it is never repaid then you can deduct the entire amount of the loan ii. If a bankruptcy occurs and the loan is expected to be settled for 20 cents on the dollar you would calculated it as follows (amount of loan – (amount of loan x .20) = deduction. 1. If that same loan received 10 cents per dollar instead, you would deduct the remaining amount not paid. iv. If a receivable is deducted as uncollectible, but paid back during the same tax year, the write-off is reversed. v. If a receivable is deducted, but paid back in a later year, then it will need to be recognized as income. vi. CONCEPT SUMMARY Business Bad Debts Nonbusiness Bad Debts Timing of deduction A deduction is allowed when the A deduction is allowed only when the debt becomes either partially or debt becomes wholly worthless wholly worthless Character of The bad debt may be deducted as The bad debt is classified as a short deduction an ordinary loss term capital loss, subject to the $3000 capital loss limitation for individuals Recovery of If the account recovered was written If the account recovered was written amounts previously off during the current tax year, the off during the current tax year, the deducted write-off entry is reversed. If the write-off entry is reversed. If the account was written off in a previous tax year, income is created subject to the tax benefit rule II. account was written off in a previous tax year, income is created subject to the tax benefit rule b. Business vs. Nonbusiness Bad Debts i. The nature of a debt determines whether the lender is engaged in the business of lending money or whether there is a proximate relationship between the creation of the lender’s trade or business 1. If true, the debt is classified as a business bad debt 2. If these conditions are not met, it is classified as nonbusiness ii. If a loan is made to a friend for his business and is not repaid, then it is a nonbusiness bad debt because it was not your business and you are not a lender iii. Any loans made by a business entity (corporation or partnership) are considered business bad debts because any loan made by these entities are automatically assumed to be trade or business related 1. If you own a business and extend credit, but the credit becomes insolvent, it is considered a business bad debt iv. The distinction between the two is important 1. A business bad debt is deductible as an ordinary loss in the year incurred 2. A nonbusiness bad debt is always treated as a short term capital loss a. It is limited benefit due to the $3,000 capital loss limitation for individuals c. Loans between Related Parties i. Loans between related parties are questioned for their validity because it is difficult to distinguish whether the loan was bona fide 1. A bona fide debt is one between a debtor-creditor base on valid and enforceable obligations to pay a fixed or determinable sum of money 2. Considerations for loans between related parties are: a. Was a note properly executed? b. Was there a reasonable rate of interest? c. Was collateral provided? d. What collection efforts were made? e. What was the intent of the parties? ii. If a loan from a shareholder is made to his corporation at a low interest it will most likely be treated as a contribution to capital rather than a liability. Thus, it cannot be deducted as a bad debt. Worthless Securities and Small Business Stock Losses a. Worthless Securities i. A loss is allowed for securities that become completely worthless during the year 1. These securities are a. Stock b. Bonds c. Notes d. Other evidence of indebtedness issued by a corporation or government ii. The losses are treated as capital losses deemed to have occurred on the last day of the tax year 1. Doing so allows a loss that would have been deemed short-term to be classified as long-term b. Small Business Stock Losses (§ 1244 Stock) i. Congress created rules that encourage taxpayers to form and operated small businesses 1. Such as § 1244 ii. The general rule for losses from the sale or exchange of corporate stock is that shareholder receive capital loss treatment III. iii. However, it is possible to avoid capital loss limitation if the loss is sustained on small business stock (§ 1244 stock) 1. Loss can be from sale of the stock or from the stock becoming worthless a. Only individuals who acquired stock from the issuing corporation qualify for ordinary loss treatment b. §1244 limits the ordinary loss to $50,000 ($100,000 for married individuals filing jointly) per year i. Any loss in excess is treated as capital losses iv. The issuing corporation must meet certain requirements under §1244 for the loss on the stock to be treated as an ordinary loss rather than capital 1. The principle requirement is that the total capitalization of the corporation must not exceed $1 million a. This limit includes all money and other property received by the corporation for stock and all capital contributions made to the corporation b. The $1 million test is made at the time the stock is issued v. §1244 stock can be either common or preferred vi. This section only applies to losses, if anything in §1244 sells at a gain, the provision does not apply and the gain is capital gain (which, for individuals, may be subject to preferential tax treatment) 1. §1244 only applies to stock sold to an individual from the issuing corporation, NOT STOCK SOLD BY AN OUTSIDE PARTY. vii. KEEP IN MIND, if you lost more than 50,000 you can spread the loss over more than one year to avoid capital loss limitations! Casualty and Theft Losses a. Definition of Casualty i. Generally, includes fire, storm, shipwreck, and theft. ii. Also, losses from other casualties are all deductible if the losses result from an event that is 1. Identifiable 2. Damaging to property 3. Sudden, unexpected, and unusual in nature a. A sudden event is an event that is swift and precipitous and not gradual or progressive i. Like a hail storm that damages your vehicle b. An unexpected event is one that is ordinarily unanticipated and occurs without the intent of the taxpayer who suffers the loss c. An unusual even is an event that is extraordinary and nonrecurring and does not commonly occur during the activity in which the taxpayer was engage when the destruction occurred d. Circumstances that may arise under these circumstances: i. A taxpayer can take a deduction for a casualty loss from an automobile accident if the accident is not attributable to the taxpayer’s willful act or willful negligence ii. Weather that causes damage must be unusual and sever for the region to qualify as a casualty 1. Furthermore, damage must be to the taxpayer’s property to be deductible iii. The term also includes accidental loss of property provided the loss qualifies under the same rules as any other casualty. iv. EVENTS THAT ARE NOT CASUALTIES 1. Progressive deterioration is not a casualty because it is not sudden 2. Losses resulting from a decline in value rather than an actual loss are not allowed b. Deduction of Casualty Losses i. Can usually deduct in the year the loss occurs unless a reimbursement claim with a reasonable prospect of full recovery exists ii. If there is a partial claim, then only the part not covered by the claim can be deducted and the rest in the year the claim is settled. iii. If a taxpayer receives reimbursement for a claim previously deducted, then they will need to report it as gross income in the year it is received 1. Disaster Area Losses a. Casualties or business losses in an area determined to be a disaster area by the president of the US b. The taxpayer can claim the loss in the year following the year of the loss c. If the extended due date for the prior years return has not passed, the taxpayer can elect to include the loss on the prior year’s tax return. d. If a disaster area is designated after the prior years return has been filed, the return can be amended or a refund claim i. Either way it is the taxpayer’s responsibility to show clearly that the election is being made c. Definition of Theft i. Theft includes larceny, embezzlement, and robbery. ii. Theft losses are deducted in the year of the discovery, it may not be the year of the loss iii. If an insurance claim is put in place and a reasonable recovery is expected, then no deduction is permitted iv. If in the year of the settlement the recovery is less than the assets adjusted base, then a deduction may be available 1. If the recovery exceeds the assets adjusted base, casualty gain may be recognized d. Loss Measurement i. If business or investment property is completely destroyed, the loss equals the adjusted basis (typically cost less depreciation) of the property at the time of destruction ii. For partial business and partial/complete personal losses, the loss is the lesser of: 1. The adjusted basis of the property, or 2. The difference between the fair market value of the property before the event and the fair market value immediately after the event iii. Any insurance reimbursement reduces the loss for business, investment and personal property 1. A special rule applies to personal insured property: a. Not allowed to deduct a casualty loss unless a claim is placed b. This applies whether a full or partial reimbursement occurs i. Generally, an appraisal before and after will need to occur or the cost of repairs will usually suffice iv. Multiple losses 1. When multiple losses occur in a year, each loss will need to be computed separately e. Casualty and Theft Losses of Individuals i. Casualty and theft losses for a business or with rental and royalty activities are deductible for adjusted gross income and are limited only by the rules previously stated. ii. Investment casualty and theft losses are classified as other misc. itemized deductions. 1. Casualty and theft losses of personal use property are subject to special limitations a. Personal Use Property i. Individual taxpayer’s face three limitations on their ability to deduct personal casualty losses 1. After 2017, individuals can only deduct a casualty loss if it occurs in a federally declared disaster area 2. Taxpayers must reduce each casualty loss by a $100 floor a. Applies to all damaged property, not each 3. The individual taxpayer can deduct only the portion of the total of all personal casualty losses the exceeds 10 percent of AGI ii. If casualty and theft gains exceed losses during the year, the gain and losses are treated as capital gains and losses iii. IV. V. VI. VII. VIII. IX. Net Operating Losses a. Introduction b. General Rules The Tax Shelter Problem At Risk Limitations Passive Activity Loss Limits a. Classification and impact of passive activity income and loss b. Taxpayers subject to the passive activity loss rules c. Rules for determining pass activities d. Material participation e. Rental activities f. Interaction of at risk and passive activity loss limits g. Special rules for real estate h. Disposition of passive activities Excess Business Losses a. Definition and rules b. Computing the limit