BAV-ASSIGNMENT-1

advertisement

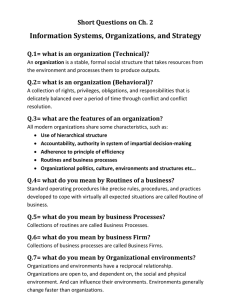

Application of Michael E. Porter's Five Competitive Forces and Generic Strategy for TELECOMMUNICATION INDUSTRY Company- VERIZON BY: P.V.S. CHANDANA, 2016A1PS0635H, MADHURA BANERJEE, 2016A7PS0087H, ANIKA BAIRATHI, 2016A5PS0733H. INDUSTRY ANALYSIS Michael Porter’s Five Forces Model Rivalry among the existing companies: (Strong Force) The US telecommunication industry has matured. It has attained saturation levels in core services. Telecommunication companies don’t have the opportunity to gain access to new untapped customers hence they compete aggressively to gain their peers’ market shares in their customer segments. The concentration should be on the quality of the final products also there is a balance among the competitors which is predicting that there is a very high competition between the firms. In this process price competition is usually high. Wireless telecom is dominated by consumers. In wireline, businesses—especially medium and large enterprises—are a significant customer segment. They aren’t very sensitive to prices. Integrated national carriers compete effectively in both of these customer segments. The largest integrated telecom companies—AT&T (T) and Verizon (VZ)—represented 69% of the industry at the end of 2013. This component of Porter’s Five Forces analyzes the intensity of competition against Verizon Communications. Competitive rivalry affects the telecommunications industry environment by imposing challenges on companies in the aspects of growing and maintaining their market shares. The following external factors affect the competition against Verizon is based on: · Low product differentiation (strong force) · High aggressiveness of firms (strong force) · High exit barriers (strong force) The telecommunications industry has a low product differentiation because competing products are highly similar, with small differences based on some variables. Low product differentiation is a crucial factor that strengthens the competitive rivalry by making it easier for customers to consider changing their service providers. Verizon Wireless attracts customers through the high quality of its services, but these services are highly similar to competing services from other firms. On the other hand, the high aggressiveness of firms creates the competitive nature in the market. Verizon Wireless competes with other firms aggressively through marketing campaigns and innovative technological. Also the economies of scale for this industry is very high which means for any company to enter needs to produce more and sell more which is really tough. Not only has this but also there exist high exit barriers, which include the high cost of telecommunications infrastructure. This won’t let established firms leave the information and communications technology and services industry, thereby keeping competition high. Added to this Brand Image is one of the major non-price dimensions that is letting Verizon to stand apart from the other major players in the market. Thus, this component shows that competitive rivalry is a major force that shapes the strategies of the business. Threat of substitute products: TCP/IP based infrastructures bring cost savings to the carriers and also allow them to abstract key value-added services from the physical layer. But substitutes are also being built on top of the IP protocol, commoditizing the incumbents’ own infrastructure and services. Today we find OTT-based substitutes for all core offerings. Voice communication is being threatened by SIP and proprietary offerings (e.g. Skype) and by asynchronous voice messages (e.g. WhatsApp) that are very popular among millennials. Traditional DSL broadband, which has enforced “customer loyalty” in the past, is seeing growing competition from TV-cable as well as from wireless technologies such as LTE and future 5G networks. Cable TV companies are faced with the threat of fast growing IPTV and VOD offerings, often contending for budgets (ads and subscription) and for customer attention (viewing time.) Even mobile businesses are being threatened by the growing number of market participants offering IP based alternatives to text messaging and to traditional long distance calling. The main substitutes in the ng cards, internationally- or foreign-managed VoIP services, satellite internet,satellite phones and NGNs. In order to analyze the threat of substitutes, it is essential to look at the price-performance trade-off between the substitute and the industry's product. Porter himself, for example, highlights the suffering of conventional long distance telephone service providers following the introduction of inexpensive internet-based phone services such as Vonage and Skype (Porter, 2008). It is also vital to look at each substitute individually and determine the buyers’ switching cost. Substitutes offer the greatest threat when they can provide buyers with better service at lower costs through changes that improve the value of their products or services. Under the Telecommunications Law, the unlicensed provision of international phone calls using VoIP is illegal and punishable with a jail term of up to According to a report by a local English-language newspaper, the Times of Oman, in early November 2009 over 200 people had been arrested following raids on more than 100 homes and shops. Omantel also blocked the popular Skype VoIP internet site in an effort to Satellite phone and satellite internet remain a threat for the future. However, until better service provision and lower rates can be guaranteed, the threat from this kind of substitution remains low. The overall impact of substitutes, however, is driving prices down and remains appreciable, due to VoIP and other alternatives such as online voice chatting and international video conferencing. Bargaining power of suppliers: The analysis of supplier power typically focuses on: The relative size and concentration of suppliers relative to industry participants. The degree of differentiation in the inputs supplied. The importance of suppliers product to the industry. Switching cost of the buyer to change the supplier. The Suppliers to this industry typically are: The manufacturers of telephone switching /switchboard equipment, Fiber optic cables, network equipment, and billing software makers. The prominent names in the supplier industry include Cisco, Alcatel-lucent, Nokia, Nortel ,Motorola and Tellabs etc . After the deregulation of downstream service providers and the technological breakthrough in IP networks, Telecom equipment makers began to ramp up manufacturing in order to meet the huge anticipated demand, however aftermath the dot com bubble, demand did not pan out as expected and led to overcapacity and eventually demise of several firms. The evidence of decline can be gauged from the fact that the telecommunications industry Association (TIA) reported that in 2016, a cumulative decline of $30.5 billion in revenues. Services of the companies in the industry require virtual network operators .There are large suppliers that offer wireless telecom services and network services to providers, usually through long term contracts. Switching costs are then very high, since firms cannot easily exit such a contract. But, due to excess capacity and falling demand, the suppliers do not have the power and clout to negotiate with the telecom behemoths. However with the demand in recent years has started to pick up with fixed line providers deciding to install fiber based networks to provide faster data and video services. Bargaining Power of Consumers: Impact: Moderate The intensity of customers’ impact is evaluated in this component of the Five Forces analysis of Telecom Industry. The most important determinants of buyer power are the size and the concentration of customers. Other factors are the extent to which the buyers are informed and the concentration or differentiation of the competitors. They have different standards therefore the buying power across demographics is different. Customers or buyers affect the company’s revenues, profit margins, and business value. The following external factors contribute to the moderate bargaining power of customers on the telecommunications industry environment: Low information asymmetry (strong force) Moderate switching costs (moderate force) Moderate price sensitivity (moderate force) The low level of information asymmetry corresponds to the high quality of information that customers can access to know about products in the market. Low information asymmetry also affects buying power. Customers have access to more products that perform in the same way. However, some consumers still lack information on specifics. Other customers can evaluate the product when placed alongside competing products. This external factor strengthens the intensity of the bargaining power of buyers or customers, based on variables like customers’ ability to evaluate and compare the services of a company to its competitors. In the context of US telecom industry we can say that, with increased choice of several technologies and means of communication available and entrance of several new firms buyer power is been increasing. The consumer now has access to several means of communication like email, instant messaging which are diminishing the importance voice services. Residential consumer also benefits with local number portability (A regulation from FCC which mandates the carriers to move the phone number when the customer switches to a different carrier). This feature makes switching costs negligible. The business segment however is prone to significant switching costs as they rely on more customized products which are tailored to their businesses and most times are locked into long-term contracts. Consequently, this component of the Porter’s Five Forces shows that customers’ demands and expectations exert a moderate force on the business and the industry environment. The low differentiation between the services provided by the telecom operators and low cost of switching for retail customers backed by Mobile Number Portability has resulted in the services being treated by customers as a commodity. Although the customers are price takers in the market, their bargaining power is moderate on account of the ease of switching. The business customers will however find it difficult to switch to alternative service provider. Threat of new entrants: Overall Effect: Moderate Factor Absolute Cost Advantage Degree Reasoning Low No firm has any absolute cost advantage in the industry. Proprietary learning curve Low Major technology invention is very less in telecom industry. Access to inputs High Towers and optical fibres are the major inputs of telecom industry. Accessing them is very difficult because the major players own most of them and charge high amount for using them. Government policy Low Telecommunications markets tend towards monopolies or oligopolies because of the investments needed to construct networks and economies of scale. So, the FCC(Federal Communications Commission) rules are in such a way to encourage new competitors. FCC Still gives telecom licenses. Economies of Scale Low Network externalities and cost structures that lead to economies of scale and scope are not unique to network industries. Capital requirements High Setting up towers and optical fibres require very high capital. Brand identity High Almost 70% of the users belong to the top 3 companies in the market. This shows that there is a high brand identity. Switching Costs Low Customers can easily switch from one firm to another firm. The costs involved are very less. Access to distribution channels High Most of the suppliers in the industry are dedicated to the firms. So accessing them is very difficult. Expected retaliation High The ability of competitors to control access to resources, key suppliers and market channels is high. The major firms are well established with 50 years of experience. Proprietary products Low Patented products used in telecom industry are less COMPETITIVE STRATEGY ANALYSIS (VERIZON) Michael Porter’s Generic Strategy Cost Leadership Verizon follows the differentiation rather than cost leadership. Its products are priced at a higher level than its competitors but then they make sure that their customers are treated very well. It follows a very unique strategy i.e if few customers are happy, they in turn will get more customers which in turn generates more profits. Despite its goal to maintain stable average revenue per user, it is willing to be more aggressive on pricing under the right circumstances. Also, Family plans, for example, offer higher customer lifetime value and lower average customer acquisition cost. As such, it regularly runs promotions where customers can add a line for free, because it makes it harder to switch and lowers the average customer acquisition cost focusing on product design. Differentiation: Differentiation is a strategy that involves providing unique and desirable features in the hope of persuading customers to purchase goods or services at a premium price. Verizon follows this strategy through reliable wireless coverage and excellent customer care. Verizon has been able to earn higher market share, increase profitability, and maintain the lowest level of customer disappointment. Differentiation builds competitive advantage on the basis of product uniqueness. Uniqueness is developed through a number of possible variables. In this case, Verizon uses quality as the most significant factor to stand out from the competition. Quality is emphasized in each and every aspect of company’s sales and marketing. For instance, advertisements for Verizon Wireless typically highlight quality of wireless services, especially connectivity quality based on infrastructure quality. Intensive growth strategies and related strategic objectives are developed to capitalize on and support such uniqueness of products. However, because of this differentiation generic strategy, the company cannot readily build competitive advantage on the basis of price, considering the costs of higher-quality infrastructure in the information and communications technology industry. As such, services as those from Verizon Wireless are priced higher compared to competitors. Though their prices are somewhat higher than their competitors they ensure their customers are treated to the best of their ability. Customer service is a significant factor, especially because of rampant customer service issues and complaints experienced in the telecommunications industry. Thus, high quality ensures customer satisfaction which generates more customers who in turn, create greater growth in profits. A strategic objective based on the differentiation generic strategy is to develop competitive advantage through further investment in infrastructure. For example, to maintain high-quality service, Verizon Wireless must implement new and advanced information and communications technologies to improve its current infrastructure. References: Laffont, J. J., Tirole, J. (2000). “Competition in Telecommunications”. Ewan Sutherland , (2014),"Lobbying and litigation in telecommunications markets – reapplying Porter’s five forces", info, Vol. 16 Iss 5 pp. 1 - 18. Bourdeau de Fontenay, Alain and Liebenau, Jonathan and Savin, Brian (2005): A New View of Scale and Scope in the Telecommunications Industry: Implications for Competition and Innovation.Published in: International Journal of Digital Economics No. 60 (December 2005): pp. 85-103. Business disruption in the telecommunication market – a five forces analysis on OTT : Featured new, Telecommunications. An analysis of the telecommunication industry using Michael Porter's competitive strategy model. [Sep 08 2018]. Daniel W. Baack,David J. Boggs,(2008) "The difficulties in using a cost leadership strategy in emerging markets", International Journal of Emerging Markets, Vol. 3 Issue: 2, pp.125-139 https://seekingalpha.com/instablog/1019942-pgrim/1016221-at-and-t-strategic-analysis Verizon, <https://strategicmanagementverizongina.wordpress.com/page/1/>(accessed on sept 08-2018) https://www.businessinsider.com/tmobile-verizon-att-sprint-customers-loyalty-2017-8?IR=T http://www.acs.com/2009/12/att-vs-verizon/ https://www.cnbc.com/2018/07/13/unlimited-data-plan-caps-verizon-att-tmobile-sprint.html