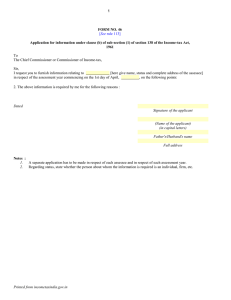

april 2016 - Institute of Cost Accountants of India

advertisement