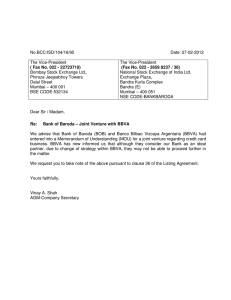

BBVA BANCO FRANCÉS S.A.

advertisement