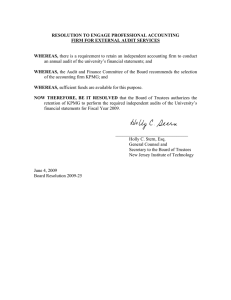

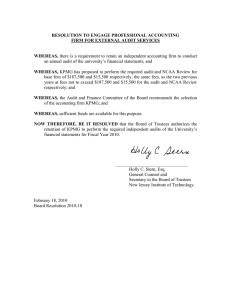

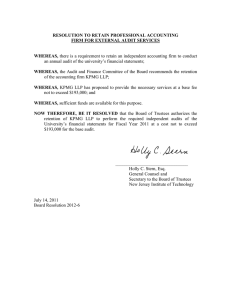

In re ShengdaTech, Inc. Securities Litigation 11-CV-01918

advertisement