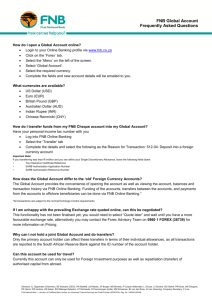

FNB Cheque Account

advertisement