Benchmarking and Knowledge

Management Within Finance

April 2012

What we’ll cover today

Welcome/Introductions

Who we are

Getting Started

Defining your process

Selecting your measures

Execute the benchmarking project

Interpret the results and apply experience

Discover the best practices

Knowledge Management/Sharing Tools

©2012 APQC. ALL RIGHTS RESERVED.

2

Welcome and Introductions

…this is where you get to participate.

©2012 APQC. ALL RIGHTS RESERVED.

3

Introduce Yourself

Name

Company

Role/Job Title

Experience with benchmarking or best

practice research?

What do you hope to learn today? Why are

you here?

©2012 APQC. ALL RIGHTS RESERVED.

4

Your APQC Team

Ron Webb

Executive Director, Research

Services

APQC

713-685-4634

rwebb@apqc.org

@rwebb_apqc

©2012 APQC. ALL RIGHTS RESERVED.

Mary Driscoll

Senior Research

Fellow

APQC

713-685-7255

mdriscoll@apqc.org

5

Who We are…

…and why you should care.

©2012 APQC. ALL RIGHTS RESERVED.

6

Who we are

APQC is a member-based, 501(c)3 nonprofit

specializing in benchmarking, knowledge

management, measurement, and process

improvement.

Our mission is to work with organizations

around the world to improve productivity and

quality by:

discovering effective methods of improvement,

broadly disseminating findings, and

connecting individuals with one another and with

the knowledge they need to improve.

©2012 APQC. ALL RIGHTS RESERVED.

7

APQC’s core competencies

Frameworks and maturity models

Benchmarking and best practices

Knowledge Management

Process improvement and measurement

Metrics and measures

©2012 APQC. ALL RIGHTS RESERVED.

8

APQC highlights

1977

• APQC opens its doors as APC

1985

• Co-founded the Malcolm Baldrige National Quality Award

1991

• International Benchmarking Clearinghouse made it’s debut

1992

• APQC develops business taxonomy with The Process Classification

FrameworkSM (PCF)

1995

• Partners with Arthur Anderson to sponsor the 1st Knowledge

Imperative Symposium, now known as the KM Conference

1996

• Chairman Grayson again set course to improve performance and

productivity with a major education initiative

2001

• Recipients of the 100 Companies That Matter in Knowledge

Management, by KMWorld magazine

2010

• Only 10-year recipient of the 100 Companies That Matter in

Knowledge Management, by KMWorld magazine

©2012 APQC. ALL RIGHTS RESERVED.

9

Getting Started…

…some key definitions.

©2012 APQC. ALL RIGHTS RESERVED.

10

Discussion Point

Who would offer up a definition for:

A benchmark

Benchmarking

A best practice or practice

Knowledge Management

©2012 APQC. ALL RIGHTS RESERVED.

11

Where Did the Word “Benchmark”

Come From?

First used by cobblers to measure people's

feet for shoes.

They would place someone's foot on a "bench"

and mark it out to make the pattern for the

shoes.

You can see how this term has evolved to

be used in business today.

Source: Wikipedia

©2012 APQC. ALL RIGHTS RESERVED.

12

Benchmarks and Benchmarking

Benchmark

Benchmarking

Standards and/or

Best practices

and/or what works

measures

How much to

improve

©2012 APQC. ALL RIGHTS RESERVED.

How to improve

13

Informal Definition

Benchmarking is the practice of being

humble enough to admit that others are

better at something and being wise enough

to learn how to match, and even surpass,

them at it.

©2012 APQC. ALL RIGHTS RESERVED.

14

Best Practice/Practice

Methods and techniques that

have consistently shown results

superior than those achieved with

other means

Used as benchmarks to strive for,

however:

There is no practice that is best for

everyone or in every situation

No best practice remains best for

very long as people keep on finding

better ways of doing things

©2012 APQC. ALL RIGHTS RESERVED.

15

Typical Benchmarking Life Cycle

Metrics

Practices

“I want to see how I compare.”

“I don’t believe it, let’s

compare again.”

Wash, rinse, repeat. (for the

really stubborn)

“OK, I give up, how are they

able to perform that

way!?!?!?!”

©2012 APQC. ALL RIGHTS RESERVED.

16

Knowledge Management

Knowledge management (KM)

connects employees to each

other, to knowledge assets,

and to those with useful

experience.

These actions accelerate the

rate of learning and cut down

the risks of not knowing and

repeating mistakes.

These actions solve business

problems!

©2012 APQC. ALL RIGHTS RESERVED.

17

More on this KM Thing…

…what is it, really?

(psst, you’ve been doing this for years)

©2012 APQC. ALL RIGHTS RESERVED.

18

Knowledge Management Components

People

Processes

Content

Technology

Knowledge is “STICKY” . . .

The Knowledge Flow Process ©

Without a systematic process and organizational environment,

it WILL NOT MOVE!

©2012 APQC. ALL RIGHTS RESERVED.

19

Successful KM Uses a Blend of KM

Approaches

©2012 APQC. ALL RIGHTS RESERVED.

20

Some Examples of KM in F&A

Communities of Practice

Focused on key issues or processes

After-Action-Reviews

Focused on significant events

Closing the books

Merger/Acquisition

Site/Location consolidation

See, you have been doing this!

Expertise Location

Very specific situations

Closing the books (monthly/annually)

Reporting

Order-to-Cash

Sales & Operations Planning/Demand Forecasting

Local/Regional tax experts

Specific regulations

Legal counsel

Content Management/Process Management

Documenting and automation of “back office” duties

AP, AR, expense report submissions, etc.

Use of ERP systems for standard work and data capture

©2012 APQC. ALL RIGHTS RESERVED.

21

Discussion Point

What are some examples from F&A that might

be knowledge management or knowledge

sharing activities?

Content management

Communities of practice

Facilitated best practice transfer

Portals/Repositories

Expertise location

Project reviews/after-action reviews

Others

©2012 APQC. ALL RIGHTS RESERVED.

22

Let’s Get Started…

©2012 APQC. ALL RIGHTS RESERVED.

23

Who Do You Trust?

If you had a business problem, who would

you trust to help solve it?

A subject matter expert?

The “group think” or “conventional

wisdom”?

A group of your industry peers?

Your boss?

A consultant?

A college professor?

This guy on the right?

©2012 APQC. ALL RIGHTS RESERVED.

24

This Isn’t A Commercial

for APQC

If it sounds like it, it’s because:

This is the approach our members asked us to

develop to help them benchmark their key

organizational processes.

Fine-tuned by our members and network of

advisors over many years.

For benchmarking and best practices, our

members have done a lot of work to make

your life easier.

Go make new mistakes!

©2012 APQC. ALL RIGHTS RESERVED.

25

Defining Your Process…

…how you get work done.

©2012 APQC. ALL RIGHTS RESERVED.

26

Process – The Big Picture

People

Technology

Process

Process is how we do work!

Processes are enabled through people and

technology

We improve performance by improving

processes

©2012 APQC. ALL RIGHTS RESERVED.

27

Discussion Point

Who has documented any, most, or all of

their key finance or accounting processes?

Who uses an external process or business

frameworks?

©2012 APQC. ALL RIGHTS RESERVED.

28

Process Classification Framework

APQC’s Process Classification FrameworkSM (PCF) is a

taxonomy of business processes that allows organizations

to objectively track and compare their performance

internally and externally with organizations from any

industry.

Built and regularly updated through collaboration with

experts, practitioners, consultants, and academicians.

Most downloaded document.

Developed in the early 1990s

Used for many purposes

Benchmarking

Standardization and measurement

Governance and accountability

Managing key functions and entire

organizations

©2012 APQC. ALL RIGHTS RESERVED.

29

Easy Access and Use

©2012 APQC. ALL RIGHTS RESERVED.

30

PCF Details

©2012 APQC. ALL RIGHTS RESERVED.

31

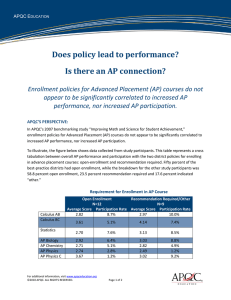

APER Example

What is the

value in this

type of

inventory?

©2012 APQC. ALL RIGHTS RESERVED.

32

Value Really Shows When You Make It

Yours

REALLY VALUABLE!

©2012 APQC. ALL RIGHTS RESERVED.

33

Key Takeaways!

Know your process

Use a process framework.

Collaborate

Bring the key staff together to agree on a standardized

view of how work is done.

Adapt it

Agree on the activities that are being examined.

Make it your own and use it to govern, measure, and

improve.

This approach will work for any process area.

AP is just an example.

©2012 APQC. ALL RIGHTS RESERVED.

34

Selecting Measures…

…I don’t have a cool tag line for this slide.

©2012 APQC. ALL RIGHTS RESERVED.

35

Key Performance Indicators and

Metrics

Key Performance Indicators (KPI)

Explicitly tied to operational objectives and

strategy.

Central to measuring progress toward the

achievement of business goals.

Categories of Metrics

Cost Effectiveness

Process Efficiency

Staff Productivity

Cycle time

©2012 APQC. ALL RIGHTS RESERVED.

36

Cost Effectiveness

Provides information concerning how well

operating cost are managed. Key performance

indicators usually include:

Cost per unit (e.g., invoice, check, and square foot)

Cost as a percentage of revenue

Cost as a percentage of total budget (e.g.,

accounts payable cost as a percentage of total F&A

cost)

Actual cost versus budgeted cost

Supporting indicators usually include cost

components as a percentage of total.

©2012 APQC. ALL RIGHTS RESERVED.

37

Staff Productivity

Provides insights into how much output each

full-time equivalent (FTE) employee has

produced. Key performance indicators usually

include:

Units of output (e.g., invoices and purchase

orders) per FTE

Workload (e.g., customers and general ledger

accounts) per FTE

Supporting indicators usually focus on factors

that influence staff productivity such as hours

of training per FTE and employee tenure.

©2012 APQC. ALL RIGHTS RESERVED.

38

Process Efficiency

Provides insights into how well procedures and

systems support operations. Key performance

indicators usually include:

Error rate (i.e., rework rate)

Forecast accuracy rate (e.g., actual vs. forecast and

non-cost measures)

Supporting indicators usually focus on factors

that influence process efficiency such as

system downtime rate and the degree of

process automation.

©2012 APQC. ALL RIGHTS RESERVED.

39

Cycle Time

Indicates the duration to complete a task.

These Key performance indicators are

measured in units of time (e.g., hours, days,

and months) and usually include:

Processing time

Time to resolve customer inquiry

Supporting indicators usually focus on

factors that influence cycle time such as the

frequency of system breakdowns.

©2012 APQC. ALL RIGHTS RESERVED.

40

Subjective Ratings

Metrics

With subjective ratings, we lack a reliable reference

point or benchmark.

How tall is President Obama? (Circle one)

1

Very Short

2

3

4

5

6

7

Very Tall

Subjective ratings invite potential bias, and solicit

perception rather than reality.

How great of a presenter am I?

1

2

Most Excellent

3

4

5

6

7

Supreme

How would you rate your average cycle time performance for your

core job responsibility?

1

Very Slow

©2012 APQC. ALL RIGHTS RESERVED.

2

3

4

41

5

6

7

Very Fast

Discussion Point

Who’s familiar with working with

normalized data?

Benefits?

What are some of the key variables used to

normalize data?

©2012 APQC. ALL RIGHTS RESERVED.

42

KPI List for AP

Cycle time in days to approve and schedule T&E

reimbursements

Percentage of disbursements that are first time

error free

Percentage of discounts available that are taken

Percentage of invoice line items paid on time

Percentage of invoice line items received

electronically

Percentage of invoice line items that are matched

the first time

Total cost to perform the process "process accounts

payable" per $1,000 revenue

©2012 APQC. ALL RIGHTS RESERVED.

43

Examples of Definitions

©2012 APQC. ALL RIGHTS RESERVED.

44

Key Takeaways

Be clear on your measures and metrics.

Use definitions.

Make sure your measures are tied to

activities and the outcomes you want to

know.

You can’t compare what you don’t ask.

There are tradeoffs with every data point

you will collect.

Weigh the tradeoff vs. not acting.

Apply judgment.

©2012 APQC. ALL RIGHTS RESERVED.

45

Executing a Benchmarking

Project…

…focus on the basics, you can “complex it up” later.

©2012 APQC. ALL RIGHTS RESERVED.

46

Decision Time and

Trade-Offs

Do it yourself.

Customize project to your specifications.

You can ask what you want to who you want.

Labor intensive. You have a day job.

Not a core competency.

Survey design, data validation, contacting/screening, etc.

Confidentiality.

Use available resources.

You have to use what is there.

Faster turnaround.

Addresses core competency issues.

Someone else does all the leg work. You focus on

value-added activities.

©2012 APQC. ALL RIGHTS RESERVED.

47

If You Want to Do-It-Yourself

Still use APQC resources. It is our Mission!

Standard Processes/Activities (PCF)

Standard Definitions

Measures/Metrics

But, you’ll need to address the following

issues…

©2012 APQC. ALL RIGHTS RESERVED.

48

Benchmarking Success Components

©2012 APQC. ALL RIGHTS RESERVED.

49

Benchmarking Methodology

©2012 APQC. ALL RIGHTS RESERVED.

50

Planning Phase

©2012 APQC. ALL RIGHTS RESERVED.

51

Collecting Phase

©2012 APQC. ALL RIGHTS RESERVED.

52

Analyzing Phase

©2012 APQC. ALL RIGHTS RESERVED.

53

Adapting Phase

©2012 APQC. ALL RIGHTS RESERVED.

54

APQC’s 24/7 Metric Benchmarking

Process

©2012 APQC. ALL RIGHTS RESERVED.

55

Keep an open mind about peers

You want to be better than your industry

peers!

©2012 APQC. ALL RIGHTS RESERVED.

56

Discussion Point

Who would you choose as a benchmarking

peer?

Why?

What criteria make a good benchmarking

peer?

©2012 APQC. ALL RIGHTS RESERVED.

57

When to choose different peers?

Competitor? Same industry?

Industry leader?

Similar size?

Transactional peer?

Executes similar number of Invoices per year?

Similar “buy” volume?

Similar business model?

Number of employees?

Annual sales revenue?

Complexity? Global vs. Local vs. Regional?

Shared Service vs. Decentralized?

Located near you?

Part of your supply chain or value chain?

Suppliers? Partners?

©2012 APQC. ALL RIGHTS RESERVED.

58

Interpreting and Using Data and

Information

…context is critical to ensure appropriate action

©2012 APQC. ALL RIGHTS RESERVED.

59

Data Reporting

Synthesizes analysis

into concise and

relevant findings.

Display findings using

graphs, tables, and

narration.

Measurement

reporting should be

clear, concise, and

most of all visual.

©2012 APQC. ALL RIGHTS RESERVED.

60

I Can Save You a Lot of Grief Now!

“The Number” doesn’t

exist.

The data isn’t the story;

the impact on your

organization is the story.

You have to give data

context for it to be useful.

The results of metric

benchmarking combined

with best practice

information and your (and

your teams’) experience is

the real power of

benchmarking.

©2012 APQC. ALL RIGHTS RESERVED.

61

Benchmarking Peer Groupings

©2012 APQC. ALL RIGHTS RESERVED.

62

Picking Your “Number”

©2012 APQC. ALL RIGHTS RESERVED.

63

Applying Judgment and Experience

©2012 APQC. ALL RIGHTS RESERVED.

64

Discussion Point

What are some of the most creative

displays of data and information you’ve

seen?

What reports have you found most useful?

How would you go about determining your

“gut” factor for theoretical cost savings?

©2012 APQC. ALL RIGHTS RESERVED.

65

Key Takeaways!

Pick your approach and dedicate the time

required of the task.

Be open to different peer groups.

Sometime a “process peer” is a better choice

than an industry peer.

Give the information context and a gut

check.

©2012 APQC. ALL RIGHTS RESERVED.

66

Discover Best Practices…

…the “how” is just as important as the “how much”.

©2012 APQC. ALL RIGHTS RESERVED.

67

Qualitative Information

Tells the “how” story

Focuses on the critical success factors

What allows companies to perform in a stellar

manner?

People?

Process?

Technology?

Culture/Leadership?

How companies close the

gap in performance

©2012 APQC. ALL RIGHTS RESERVED.

68

Financial Management:

The Quest for Excellence

Mary C. Driscoll

©2012 APQC. ALL RIGHTS RESERVED.

69

CFOs are Investing in

Financial Process Improvement

“We see more robust analytics and

decision support being provided

internally, which is contributing to the

increased size and scope of consulting

engagements focused on finance and

accounting processes and

technology.”

- Kennedy Information, LLC

©2012 APQC. ALL RIGHTS RESERVED.

70

Currently pursuing a major

process improvement in FM?

19%

Yes

No

81%

Source: APQC Research, March 2012:

Finance Improvement Programs Now Aim at Both Value and Cost

©2012 APQC. ALL RIGHTS RESERVED.

71

Top Priority?

1%

Both efficiency and effectiveness

11%

Efficiency (improve finance

cost/productivity profile, accelerate

cycle speed, reduce error rates)

16%

Effectiveness (deliver more effective

analytical support to the business)

Don’t know

72%

Source: APQC Research, March 2012:

Finance Improvement Programs Now Aim at Both Value and Cost

©2012 APQC. ALL RIGHTS RESERVED.

72

Making Progress?

Where is your finance organization today on the road to

becoming a more highly valued partner to the business?

Where's the road?

12%

4%

Recently started and hopeful

22%

Making some progress but facing

obstacles

30%

Gaining traction and overcoming some

obstacles

32%

©2012 APQC. ALL RIGHTS RESERVED.

Rolling along with confidence and

learning more about this journey

73

Strategic Imperatives Behind

the Investment Surge

Sustainable, profitable growth is elusive

Products and services must be customized

allocate the right resources at the right times

deliver profitability analyses and scenario modeling

Growing regulatory scrutiny

improve accuracy, transparency, accountability, and auditability

©2012 APQC. ALL RIGHTS RESERVED.

74

Finance Improvement Imperatives

Better access to reliable operating data to

speed and improve planning/forecasting

Insightful—and curious!—decision-support

Reduce risk of accounting/reporting errors

Pay for change with more cost-efficiency

Put the right talent with the right tools in

well-defined roles

Deploy new service delivery models

Deploy process owners to drive

change

©2012 APQC. ALL RIGHTS RESERVED.

75

Hasn’t Finance Already Been

“Re-engineered” Like Crazy?

A look at APQC metrics reveals the truth

©2012 APQC. ALL RIGHTS RESERVED.

76

Total Cost of Finance as a Percentage

of Revenue – All Participants

2.5%

n=421

2.2%

2.0%

1.5%

1.2%

1.0%

0.6%

0.5%

0.0%

Bottom Performer

Median

Top Performer

Source: APQC Open Standards Benchmarking

©2012 APQC. ALL RIGHTS RESERVED.

77

This alarming situation is unending!

©2012 APQC. ALL RIGHTS RESERVED.

78

Cycle Time in Days to Complete

the Annual Budget Cycle

100

90

90

80

60

60

47.5

40

30

29.5

20

0

Bottom Performers

Median

All Participants

N=416

Top Performers

Durable Goods

N=16

Source: APQC Open Standards Benchmarking

©2012 APQC. ALL RIGHTS RESERVED.

79

Cycle Time in Days to Complete

the Financial Forecast

20

17.25

15

10

8

8

5

4

4

2.5

0

Bottom Performers

Median

All Participants

N=403

Top Performers

Durable Goods

N=16

Source: APQC Open Standards Benchmarking

©2012 APQC. ALL RIGHTS RESERVED.

80

Cycle Time in Days between Completion

of Annual Consolidated Financial

Statements and the Release of Earnings

45

40

40

35

30

25

25

20

20

15

13.75

15

10

10

5

0

Bottom Performers

Median

All Participants

N=164

Top Performers

Revenue > 5 Billion

N=50

Source: APQC Open Standards Benchmarking

©2012 APQC. ALL RIGHTS RESERVED.

81

Case Study: General Mills

How corporate strategy drives finance

priorities and metrics

Hybrid service delivery model puts the right

people in the right jobs

Leverage IT to drive efficiencies

P-card for indirect spending

Win-win terms and discount options

©2012 APQC. ALL RIGHTS RESERVED.

82

Virtuous Capital Cycle at General Mills

Strong ROC delivers:

- Expected return to investors (WACC)

- Excess capital to return to equity

investors (return in excess of WACC)

Share

Repurchase

Equity and

Credit

Investors

Improving

ROC

- Earnings

growth

- Efficient use

of capital

Equity and credit investors provide

capital to GMI

Working

Capital

Dividends

CAPEX

Debt Service

M&A

GMI invests in efficient growth of

business (ROC)

©2012 APQC. ALL RIGHTS RESERVED.

83

Ensuring Effective Capital Mgt.

General Mills’ Monthly Working Capital Check-up:

Working capital metrics versus the plan and last year,

Receivables performance,

Payables performance,

Review of business unit current assets and current

liabilities,

Overview of business performance and impact on

inventories,

Quarterly working capital

implications versus targets, and

Discussion of potential actions to

achieve targets.

©2012 APQC. ALL RIGHTS RESERVED.

84

General Mills Mgt. Incentive Metrics

Performance ratings and incentive pay are

tied to shareholder value drivers such as:

Net sales growth

Segment operating profit growth

Diluted earnings per share growth

Return on Capital improvement

©2012 APQC. ALL RIGHTS RESERVED.

85

General Mills Rigorous Tracking of

AR Performance Metrics

4

100%

100%

95%

3

96%

90%

2

92%

85%

1

88%

80%

0

84%

75%

Avg. Days Delinquent

Collection Effectiveness

GMI

50% Quartile

©2012 APQC. ALL RIGHTS RESERVED.

25% Quartile

75% Quartile

86

Percentage Current

General Mills AP Best Practices

Hybrid service delivery model puts the right

people in the right jobs

Leverage IT to drive efficiencies

P-card for indirect spending

Win-win terms and discount options

©2012 APQC. ALL RIGHTS RESERVED.

87

General Mills Annual

Working Capital Benchmarking

©2012 APQC. ALL RIGHTS RESERVED.

88

Survey Results:

Current Trends in FP&A

©2012 APQC. ALL RIGHTS RESERVED.

89

©2012 APQC. ALL RIGHTS RESERVED.

90

Biggest Barriers to Progress

Most frequently cited by 1/3 of respondents:

Lack of:

system integration

common data model

common data repository

operating data for advanced modeling

alternative to spreadsheets as primary tool

©2012 APQC. ALL RIGHTS RESERVED.

91

Biggest Frustrations:

Finance talent is analytical but

not curious

Organizational resistance and

data hoarding

Senior mgt. ignores the model and lets Wall Street

dictate budgets and forecasts

Senior mgt. prefers to make decisions “from the

gut” than allow models to drive choices

Blind focus on short-term goals means models

and analyses get ignored

Planning process not standardized

©2012 APQC. ALL RIGHTS RESERVED.

92

What is FP&A Excellence?

Mastery of

systems,

analytical tools,

and data

management

Can design

reports and selfservice tools

business

managers will use

Strong grasp of

business strategy,

functions,

markets and risks

Deep knowledge

of accounting and

performance

management

©2012 APQC. ALL RIGHTS RESERVED.

Versatile and

polished

communication

skills

Customer service

orientation

FP&A Excellence

93

Insatiable desire

to solve business

puzzles

Key Takeaways!

Turn over more stones to find

new ways to boost productivity

Reducing costs without re-investing in

analytical power may mean relevance

lost

Business managers need faster, better,

more granular insights on rewards/risks

Don’t just purchase fancy planning

software

Develop a strategy for building analytical

capability and influencing your culture

©2012 APQC. ALL RIGHTS RESERVED.

94

Question & Answer

If you think of others, just contact us.

Your APQC Team

Ron Webb

Executive Director, Research

Services

APQC

713-685-4634

rwebb@apqc.org

@rwebb_apqc

©2012 APQC. ALL RIGHTS RESERVED.

Mary Driscoll

Senior Research

Fellow

APQC

713-685-7255

mdriscoll@apqc.org

96