Dataline

A look at current financial reporting

issues

No. 2013-22

November 21, 2013

What’s inside?

Overview .......................... 1

The main details ..............2

Quantifying errors ................. 2

Evaluating whether the

financial statements are

materially misstated ............ 2

Determining how to

correct the errors ................. 3

Evaluation framework

and practical example ......... 5

Questions ......................... 5

Appendix A:

Framework for

evaluating errors

in previously-issued

financial statements .....6

Appendix B:

Practical example ......... 7

Evaluating errors in previously-issued

financial statements

Applying the "dual method"

Overview

Errors in US GAAP financial statements filed with the SEC must be evaluated using

both the "iron curtain" method and the "rollover" method. Many companies whose

financial statements are not filed with the SEC (or that file local GAAP financial

statements with the SEC) also evaluate errors using both of these methods. The use of

both methods is commonly referred to as the "dual" method of evaluating errors.

If the previously-issued financial statements are materially misstated, they should be

corrected promptly.

-

For a public company, the correction of a material misstatement is ordinarily

accomplished by amending prior filings (e.g., filing Form 10-K/A and/or Form 10Q/A).

-

For a private company, the correction of a material misstatement is ordinarily

accomplished by the company issuing corrected financial statements which

indicate that they have been restated and including its auditor’s re-issued audit

report. Users of the financial statements also must be notified that they should no

longer rely on the previously-issued financial statements.

If the previously-issued financial statements are not materially misstated, then the

error may be corrected prospectively.

Materiality analyses require significant professional judgment. The materiality

analysis must consider all relevant qualitative and quantitative factors (including

company/industry-specific factors).

Note: This Dataline updates and supersedes Dataline 2009-21 by providing

clarifications based on questions received since Dataline 2009-21 was issued.

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

1

The main details

Quantifying errors

.1 When errors in previously-issued financial statements are identified, they must be

assessed to determine whether the affected financial statements are materially misstated.

The starting point for any materiality analysis is to quantify the errors. SEC Staff

1

Accounting Bulletin No. 108 (SAB 108) provides guidance to consider when quantifying

errors.

.2 SAB 108 requires that errors be evaluated under both the "rollover" method and the

"iron curtain" method. The principal difference between these two methods lies in how

income statement errors are quantified.

The "rollover" method quantifies income statement errors based on the amount by

which the income statement is actually misstated — including the reversing effect of

any prior errors. Identified misstatements in the previous period that were not

corrected need to be considered to determine the "carryover effects".

The "iron curtain" method quantifies income statement errors based on the amount

by which the income statement would be misstated if the accumulated amount of

the errors that remain in the balance sheet were corrected through the income

statement of that period.

PwC observation:

The above discussion is focused on how the "rollover" and "iron curtain" methods are

applied when evaluating materiality with respect to the financial statements.

However, it is important to note that the quantified materiality of an error must be

evaluated with respect to each affected financial statement, as well as the impact on

financial statement line items and financial statement disclosures. For instance, in

addition to considering the income statement, a materiality evaluation under the

"rollover" method would also include consideration of whether any cumulative

unadjusted error(s) in the balance sheet(s) resulted in a material misstatement of the

balance sheet(s) or the statement(s) of stockholders' equity. Similarly, the evaluation

under the "rollover" method for each impacted period would include consideration of

whether the rollover impact of the error(s) would materially impact the statement(s)

of cash flows or disclosures.

Evaluating whether the financial statements are materially misstated

.3 After the errors have been quantified, the previously-issued financial statements

should be evaluated to determine whether they are materially misstated. SEC Staff

Accounting Bulletin No. 99 (SAB 99) provides guidance to consider when evaluating

materiality.

.4 SAB 99 should be used as a "guide" rather than a "checklist." Not all of the factors in

SAB 99 are relevant to every situation. Additionally, some factors that are relevant to the

analysis may not be specifically listed in SAB 99 (e.g., industry-specific considerations).

All relevant qualitative and quantitative factors (including company-specific factors)

must be considered. Materiality analyses require significant professional judgment.

1

Codified in ASC 250-10-S99 SEC Materials

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

2

.5 In a December 2008 speech, an Associate Chief Accountant in the SEC's Office of the

2

Chief Accountant clarified the SEC staff's view of how SAB 108 should be applied to

previously-issued financial statements. The Associate Chief Accountant indicated that if

the effect of a correction would not materially affect the previously-issued financial

statements, those financial statements may still be relied upon, and the correction may

be made in future filings (i.e., without requiring an amendment to prior filings).

If the errors are material when evaluated under the "rollover" method, then the

previously-issued financial statements are considered materially misstated (i.e.,

they should no longer be relied upon).

If the errors are not material when evaluated under the "rollover" method, then the

previously-issued financial statements are not considered materially misstated (i.e.,

they can continue to be relied upon). However, if the impact of the errors to the

current period financial statements would be material when evaluated under the

"iron curtain" method, then the errors need to be corrected even though the

previously-issued financial statements are not materially misstated.

PwC observation:

When considering whether previously-issued financial statements are materially

misstated, the key principle to focus on is whether the corrected financial statements

would be materially different from the previously-issued financial statements. The

"rollover" method is used to evaluate whether previously-issued financial statements

are materially misstated. The "rollover" method is used because, as discussed above,

the "rollover" method quantifies the actual financial statement errors for each period.

If an error is not material to previously-issued financial statements under the

"rollover" method, then those financial statements can continue to be relied upon.

Errors evaluated under the “rollover” method are compared to the “as reported”

amounts in previously-issued financial statements.

The "iron curtain" error analysis does not drive the decision regarding whether or not

previously-issued financial statements are materially misstated. The error in the

previously-issued financial statements should be quantified and evaluated under the

"iron curtain" method to determine how the error needs to be corrected. In other

words, if an error in previously-issued financial statements is not material under the

"rollover" method, but would be material under the "iron curtain" method, then the

error must be corrected by revising the previously-issued financial statements the

next time they are filed. An error that would be material to the previously-issued

financial statements under the "iron curtain" method cannot remain as an unadjusted

difference.

Determining how to correct the errors

.6 Once the materiality analysis is complete, the company must determine how to

correct the errors.

Correcting financial statements that are materially misstated

.7 If the previously-issued financial statements are materially misstated (under the

"rollover" method), then they should be corrected promptly. For a public company, the

correction of a material misstatement is ordinarily accomplished by amending prior

filings (e.g., filing Form 10-K/A and/or Form 10-Q/A). For a private company, the

2

http://www.sec.gov/news/speech/2008/spch120808mm.htm

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

3

correction of a material misstatement is ordinarily accomplished by the company issuing

corrected financial statements which indicate that they have been restated.

The corrected financial statements should include the disclosures required by ASC

250, Accounting Changes and Error Corrections. These disclosures include the

nature of the error and the quantitative effects of correction on each affected

financial statement line item (including per share amounts). Affected column

headings should be labeled "Restated" (or something comparable).

An audit report on the corrected financial statements should include an explanatory

paragraph indicating that the previously-issued financial statements have been

restated to correct a misstatement. The explanatory paragraph should also include a

reference to the company's disclosure of the correction. Refer to PCAOB AU 508,

paragraphs 18A-18C or AICPA AU 420.12 (as appropriate) for the audit reporting

requirements.

Business entities may present historical, statistical-type summaries of financial data

for a number of periods—commonly 5 or 10 years. Whenever error corrections have

been recorded during any of the periods included, a quantitative and qualitative

analysis of the error should be performed for these years.

Management should consult with its counsel to determine the appropriate steps and

timing for providing notice that the materially misstated financial statements

should no longer be relied upon (e.g., by filing a Form 8-K under Item 4.02). The

auditor should consider the guidance in PCAOB AU 561 or AICPA AU-C 560 (as

appropriate).

Management and/or the auditor should also consider how the error impacts their

respective conclusions regarding internal control over financial reporting and/or

disclosure controls and procedures, as appropriate. This analysis of the control

implications should be for the current and prior period end.

Correcting financial statements that are not materially misstated

.8 If the previously-issued financial statements are not materially misstated, then the

errors may be corrected prospectively. Prospective correction may be accomplished in

one of two ways (depending on the circumstances).

3

Correction as an "out-of-period" adjustment: Errors may be corrected as an "outof-period" adjustment if the correction would not result in a material misstatement

of the estimated income/loss for the year in which the adjustments are made or to

the trend in earnings. This is true even if the "out-of-period" adjustment is material

to the interim financial statements in which it is recorded unless the error

originated in the current year. An "out-of-period" adjustment that is material to the

interim financial statements in which it is recorded (but not material with respect to

the estimated income for the full fiscal year or to the trend of earnings) should be

3

separately disclosed (in accordance with ASC 250-10-45-27 ).

Revising financial statements the next time they are filed: If the errors cannot be

corrected as an "out-of-period" adjustment without causing a material

misstatement of the estimated income/loss for the year in which the adjustment is

made or to the trend in earnings, then the errors must be corrected by revising the

previously-issued financial statements the next time they are filed (e.g., for

comparative purposes). This is commonly termed as a “revision” of previouslyissued financial statements. The revised financial statements should include

Pre-codification APB 28, Interim Financial Reporting, paragraph 29

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

4

transparent disclosure regarding the nature and amount of the errors being

corrected. The disclosure should provide insight into how the errors affect all

relevant periods. For instance, if the first filing to be corrected is a Form 10-Q,

management should consider disclosing how the error will affect all interim and

annual periods that will ultimately be revised.

PwC observation:

Management should consult with its counsel to determine whether the company

should provide disclosure of prospective corrections (other than in the financial

statements that reflect the prospective correction). We do not believe it would

ordinarily be necessary to file a Form 8-K under Item 4.02 because the previouslyissued financial statements are not materially misstated (i.e., they can continue to be

relied upon). However, there may be other situations in which separate disclosure

would be appropriate. For instance, if securities are to be offered based on the

uncorrected financial statements, the prospectus/offering materials may need to

include additional disclosure (including quantification) of the impending correction.

We do not believe an auditor’s report on the revised financial statements would need

an explanatory paragraph referring to the revision (although dual date may be

required as described in PCAOB AU 530.08 and AICPA AU-C 560.A16). This is

because a conclusion has been reached that the previously-issued financial

statements are not materially misstated (i.e., they can continue to be relied upon).

Evaluation framework and practical example

.9 Appendix A summarizes the process for evaluating errors in previously-issued

financial statements. Appendix B is a practical example of the process.

Questions

.10 PwC clients that have questions about this Dataline should contact their engagement

partners. Engagement teams that have questions about this Dataline should contact any

member of SEC Services or Risk Management in the National Professional Services

Group.

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

5

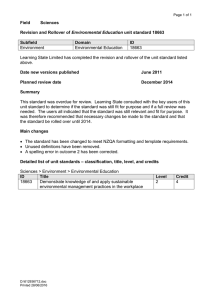

Appendix A: Framework for evaluating errors in previouslyissued financial statements

Start

Is the error material* to the previouslyissued financial statements under the

“ROLLOVER” method?**

Yes

The previously-issued financial

statements must be corrected promptly.

For a public company, this is usually

accomplished by amending prior filings

(e.g., Form 10-K/A and/or Form 10-Q/

A). For a private company, this is

ordinarily accomplished by issuing

corrected financial statements.

No

The error CANNOT be corrected as an

“out-of-period” adjustment. The previouslyissued financial statements must be

revised the next time they are filed.

The previously-issued financial statements may continue to be relied upon. The

error may be corrected PROSPECTIVELY.

Would correction as an “out-ofperiod” adjustment materially*

misstate the YEAR in which it

would be corrected or the trend in

earnings?

Yes

No

Would the “out-of-period”

adjustment be material* to the

INTERIM PERIOD in which it

would be corrected?

The error may be corrected as

an “out-of-period” adjustment with

transparent disclosure regarding the

nature and effect of the adjustment.

Alternatively, the financial statements

may be revised the next time

they are filed.

Yes

No

The error may be corrected as an “outof-period” adjustment. Management should

consider disclosure of the “out-of-period”

adjustment. Alternatively, the financial

statements may be revised the next time they

are filed. Under certain circumstances, the

amount may remain on the SUM, however, we

encourage our clients to correct all errors.

*The materiality evaluation requires significant professional judgment and should consider all relevant qualitative and quantitative factors. The

evaluation may need to include factors that are not specifically mentioned in SAB 99.

**The "rollover" method is used to evaluate whether previously-issued financial statements are materially misstated. The “rollover method”

involves an analysis of the error(s) on all of the financial statements. The "iron curtain" error analysis does not drive the decision regarding

whether or not previously-issued financial statements are materially misstated.

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

6

Appendix B: Practical example

Company X is a calendar year-end SEC registrant. In early April 2013, Company X identified a long-term incentive

compensation obligation for one of its salespeople which it had inadvertently neglected to record since 2009. If

Company X had properly accounted for the plan, it would have recorded an additional $30 of compensation expense in

each of the years 2009 through 2012.

Company X's reported income in each of the years 2009 through 2012 was $1,000.

Company X projects its 2013 income will be $1,000.

Note: Income tax effects are ignored for purposes of this example. Additionally, this example assumes that there are no

other errors affecting any of the years. If there were additional errors (whether unadjusted or recorded as "out-ofperiod" adjustments), those errors would also need to be considered in the materiality analysis.

Quantifying the errors in the previously-issued financial statements

Company X has quantified the errors under both the "rollover" and the "iron curtain" methods as follows:

Reported income

Rollover method

Iron curtain

method

2009

$1,000

$30 (3%)

$30 (3%)

2010

$1,000

$30 (3%)

$60 (6%)

2011

$1,000

$30 (3%)

$90 (9%)

2012

$1,000

$30 (3%)

$120 (12%)

2013

$1,000 (Projected)

N/A

N/A

Year

Evaluating whether the affected financial statements are materially misstated

Company X should consider whether the errors quantified under the "rollover" method (i.e., $30 or 3% of income per

year) are material to the financial statements for any of the years 2009 through 2012. In making this analysis, Company

X should consider all relevant qualitative and quantitative factors.

Note: The above analysis focuses on the effects of the errors on the income statement. However, the analysis must

consider the impact of the error on the full financial statements (including disclosures).

Determining how to correct the errors

If Company X determines that any of the years 2009 through 2012 are materially misstated when the errors are

evaluated under the "rollover" method, then those years must be promptly corrected. The usual method of correcting

materially misstated financial statements would be by filing amended filings (e.g., Form 10-K/A and/or Form 10-Q/A).

If Company X determines that none of the years 2009 through 2012 (or quarters for 2012) are materially misstated

when the errors are quantified under the "rollover" method, then the errors can be corrected prospectively. Prospective

correction may be accomplished in one of two ways (depending on the circumstances).

Company X may correct the errors as an "out-of-period" adjustment in its 1st quarter 2013 interim financial

statements if the correction would not result in a material misstatement of the estimated fiscal year 2013

earnings ($1,000) or to the trend in earnings. This is true even if the "out-of-period" adjustment is material to the

1st quarter 2013 interim financial statements. If the "out-of-period" adjustment is material to the 1st quarter

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

7

2013 interim financial statements (but not material with respect to the estimated income for the full fiscal year

2013 or to the trend of earnings), then the correction should be separately disclosed (in accordance with ASC

250-10-45-27).

If Company X cannot correct the errors as an "out-of-period" adjustment without causing a material

misstatement of the estimated fiscal year 2013 earnings ($1,000) or to the trend in earnings, then the errors must

be corrected by revising the previously-issued financial statements the next time they are filed (e.g., for

comparative purposes). For instance, the quarterly financial statements for the 1st quarter of 2012 and the

December 31, 2012 balance sheet presented in Company X's March 31, 2013 Form 10-Q should be revised to

correct the error. The revised financial statements should include transparent disclosure regarding the nature

and amount of each error being corrected. The disclosure should provide insight into how the errors affect all

relevant periods (including those that will be revised in subsequent filings).

National Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com

Dataline

8

Authored by:

John May

Partner

Phone: 1-646-471-3527

Email: john.a.may@us.pwc.com

Marc Anderson

Partner

Phone: 1-646-471-3527

Email: marc.e.anderson@us.pwc.com

Sarah Fitch

Director

Phone: 1-973-236-4404

Email: sarah.fitch@us.pwc.com

Declan Byrne

Senior Manager

Phone: 1-973-236-7962

Email: declan.m.byrne@us.pwc.com

Datalines address current financial-reporting issues and are prepared by the National Professional Services Group of PwC. They are for general

information purposes only, and should not be used as a substitute for consultation with professional advisors. To access additional content on

financial reporting issues, register for CFOdirect Network (www.cfodirect.pwc.com), PwC’s online resource for financial executives.

© 2013 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. PwC refers to the United States member firm, and

may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.