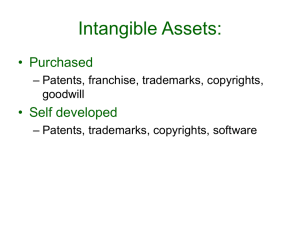

Intangible Assets

advertisement