Chapter 17 Time series: Measurements taken over time. i.e. every

advertisement

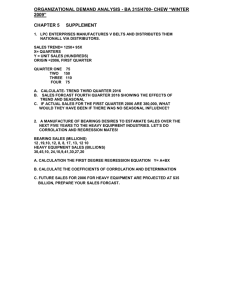

Chapter 17 Time series: Measurements taken over time. i.e. every hour, day, week, month or year. 17.1 Time series components or patterns TREND COMPONENT (T) The gradual shifting of the time series over longer period of time is referred to as the trend in the time series. It has a smooth pattern and is longer than a year. CYCLICAL COMPONENT (C) Any recurring sequence of points above and below the trend line lasting more than one year can be attributed to the cyclical component of the time series. For example: Levels of pessimism or optimism in the economy, trade unions, world organisations etc. Volume Trend and cyclical components of a time series with data points one year apart 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Time Copyright Reserved 1 SEASONAL COMPONENT (S) Identical variation patterns repeating daily, monthly, quarterly. The time series show a regular pattern within one-year periods. For example: Traffic flow/volume during week days, special occurring events e.g. Rand Easter Show, school holidays etc. IRREGULAR COMPONENT (I) The irregular component is caused by the unpredictable occurrences like one-off events such as natural disasters (floods, fires etc.) or man-made disasters (strikes, boycotts or accidents). 17.3 Smoothing Methods Moving Average Forecast • Can only be used for stable time series – no significant trend, cyclical or seasonal effects. In other words, using the moving average forecast approach, the time series must consist of only the irregular component. Copyright Reserved 2 • 3-week moving average Moving Sales Average (in 1000) Forecast Week 1 17 2 21 3 19 4 23 5 18 6 16 7 20 8 18 9 22 10 20 11 15 12 22 Total Squared Forecast Forecast Error Error − − 0 92 = ∑ − = • Average of the sum of squared errors (MSE) = • How many values should be included in the moving average? Copyright Reserved 3 • 5-week moving average Moving Sales Average Forecast (in 1000) Forecast Error − Week 1 17 2 21 3 19 4 23 5 18 6 16 7 20 8 18 9 22 10 20 11 15 12 22 Total -1.2 Squared Forecast Error − 51.84 • Average of the sum of squared errors: = • The MSE of the 5-weekly moving average is the smallest • Hence the 5-weekly moving average is the best for forecasting Copyright Reserved 4 • Use Excel’s AVERAGE function for section 17.3; selfstudy [also see Assignment Book] 17.4 Trend Projection • Estimating the long term linear trend = + = trend value of the time series in period t = y-intercept of the trend line = slope of the trend line t = time • Time scale t = 1: time of the first observation on the time series data t = 2: time of the second observation on the time series data = value of the time series at period t. Year t 1994 1995 1996 1997 1998 1 2 3 4 5 Sales (in 1000) 13 15 20 21 23 Copyright Reserved 5 • Formulas for calculating the trend line = ∑ − − ∑ − ∑ − ∑ ∑ / = ∑ − ∑ / and = − Copyright Reserved 6 • Calculating the trend line Year Sales − t (in 1000) 1 13 2 15 3 20 4 21 5 23 15 92 = = − − − − = ∑ !! ∑! " = = − = • Estimated trend line: = + = • Interpretation: = The estimated number of items sold has increased by ________ per year. = The estimated number of items sold during 1993 was __________. Copyright Reserved 7 • Forecasting: The estimated number of items to be sold during the next year: Set: t = 6 Calculating the slope with the “calculation” formula Year (t) 1 2 3 4 5 15 = Sales in 1000 (Yt) 13 15 20 21 23 92 ∑ !∑ ∑ /# ∑ " !∑ " /# = t Yt t2 13 30 60 84 115 302 1 4 9 16 25 55 $!%&/% %%!%" /% = • Note : The answer is the same MULTIPLICATIVE MODEL The multiplicative time series model: = × × ( We will illustrate the use of the multiplicative model with the two examples below. Copyright Reserved 8 EXAMPLE (ODD) A movie theatre wants to determine the popularity of specific weekdays of moviegoers in order to formulate an advertising campaign during busier periods. The number of people (in hundreds) visiting the movie theatre daily is summarised in the table below: Estimate of Week t Day 1 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 Mon Tues Wed Thurs Fri Mon Tues Wed Thurs Fri Mon Tues Wed Thurs Fri Mon Tues Wed Thurs 2 3 4 Number of moviegoers (in hundreds) Yt 5 15.2 7.4 6.7 21 4.1 14.9 6.7 6 19 2.1 14.2 6.5 6.1 18 ( 5-day moving average Seasonal Irregular Value 10.68 10.54 10.14 9.74 9.6 9.56 9.58 9.38 0.66 0.62 1.98 0.22 *** 0.69 ) Deseasonalised moviegoers (in hundreds) 9.68 9.69 7.00 9.79 9.70 9.84 9.18 Calculation for Question 7 Copyright Reserved 9 Seasonal irregular values (* + values): Monday Tuesday Wednesday Thursday Friday Average seasonal irregular values: Monday Tuesday Wednesday Thursday Friday Correction factor: No correction factor is needed, since the sum of the average seasonal irregular values = Seasonal indices: Monday Tuesday Wednesday Thursday Friday Note: The trend line fitted to the deseasonalised series is: Copyright Reserved 10 Question 1: The 5-day moving average for Friday Week 1 is: Question 2: The seasonal irregular value for a Tuesday Week 2 is: Question 3: The seasonal irregular value for a Tuesday Week 3 is: Question 4: The seasonal index for Tuesday is: Question 5: The deseasonalised number of moviegoers (in hundreds) for Wednesday Week 2 is: OR The seasonally adjusted number of moviegoers (in hundreds) for Wednesday Week 2 is: Copyright Reserved 11 Question 6: The interpretation of the slope of the trend line is: Question 7: According to the seasonal index for Wednesday the number of moviegoers is: Question 8: The trend value of the number of moviegoers for Wednesday Week 4 is: Question 9: The estimated number of moviegoers (in hundreds) for Thursday Week 4 is: Hint: Use the multiplicative model = × × ( Copyright Reserved 12 EXAMPLE (EVEN) The quarterly sales data (2000-2002) for the PQR company (in R1000) is given below: Estimate of ( ) Year Quarter t Sales 2000 1 1 54 69.43 2 2 58 *** 3 3 94 1.3598 70.05 4 4 70 1.0054 68.88 1 5 55 *** 70.71 2 6 61 0.9004 70.59 3 7 87 *** 64.84 4 8 66 1.0154 64.94 1 9 49 0.751 63.00 2 10 55 0.8178 63.65 3 11 95 70.80 4 1 2 3 4 1 2 12 13 14 15 16 17 18 74 72.81 2001 2002 2003 2004 4-quartly Moving Average Centered Moving Average Seasonal Irregular Value Deseasonalised Sales Calculation of Questions 8 and 9 Copyright Reserved 13 Seasonal irregular values: Quarter 1 Quarter 2 Quarter 3 Quarter 4 Average seasonal irregular values (Also called unadjusted seasonal indexes): Quarter 1 Quarter 2 Quarter 3 Quarter 4 Correction factor: The sum of the unadjusted seasonal indexes is Therefore, the correction factor = Seasonal Index: Quarter 1 Quarter 2 Quarter 3 Quarter 4 Given: The trend line fitted for the deseasonalised sales is: Copyright Reserved 14 Question 1: The centered moving average for the third quarter of 2000 is: Question 2: The seasonal irregular value for the first quarter of 2001 is: Question 3: The seasonal irregular value for the third quarter of 2001 is: Question 4: The unadjusted seasonal index for the fourth quarter is: Question 5: If the sum of the unadjusted seasonal indices is 3.977, then the correction factor is: Copyright Reserved 15 Question 6: The adjusted seasonal index for the second quarter is 0.8641. This indicates that: Question 7: The deseasonalised sales (in R1000) for the second quarter of 2000 is: Question 8: The trend value (in 1000) for the third quarter of 2003 is: Question 9: The estimated sales (in 1000) for the second quarter of 2004 is: Copyright Reserved 16