Testing Models on Simulated Data Presented at the CAS Annual Meeting

advertisement

Testing Models on

Simulated Data

Presented at the

CAS Annual Meeting

November 13, 2007

Glenn Meyers, FCAS, PhD

ISO Innovative Analytics

The Application

Estimating Loss Reserves

• Given a triangle of incremental paid losses

– Ten years with 55 observations arranged by

accident year and settlement lag

• Estimate the distribution of the sum of the

remaining 45 accident years/settlement

lags

• Loss reserve models typically have many

parameters

– Examples in this presentation – 9 parameters

Danger – Possible Overfitting!

• Model describes the sample, but not the

population

• Understates the range of results

• The range is the goal!

• Is overfitting a problem with loss reserve

models?

• If so, what do we do about it?

Outline

• Illustrate overfitting with a simple example

– Example – fit a normal distribution with three

observations

– Illustrate graphically the effects overfitting

• Illustrate overfitting with a loss reserve

model

– Reasonably good loss reserve model

– Show similar graphical effects as normal

example

Normal Distribution

• MLE for parameters m and s

1 n

m

ˆ xi and s

ˆ

n i 1

• n = 3 in these examples

1 n

2

xi mˆ

n i 1

Simulation Testing Strategy

• Select 3 observations at random

Population - m = 1000, s = 500

• Predict a normal distribution using the

maximum likelihood estimator

• Select 1,000 additional observations at

random from the same population

• Compare distribution of additional

observations with the predicted distribution

Simulated Fits

Simulation 24

7000

7000

9000

11000

Simulation 91

7000

9000

11000

Loss

Loss

Simulation 132

Simulation 4

9000

Loss

11000

7000

9000

Loss

11000

PP Plots

0.6

0.4

0.2

0.0

Predicted Percentiles

If predicted percentiles

are uniformly

distributed, the plot

should be a 45o line.

0.8

1.0

Plot

Predicted Percentiles x Uniform Percentiles

0.0

0.2

0.4

0.6

Uniform Percentiles

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

0.4

0.8

Simulation 91

0.0

Predicted Percentiles of Outcomes

0.4

0.8

Simulation 24

0.0

Predicted Percentiles of Outcomes

PP Plots

0.0

0.2

0.4

0.6

0.8

Uniform Percentiles

1.0

0.6

0.8

1.0

0.4

0.8

Simulation 4

0.0

Predicted Percentiles of Outcomes

0.4

0.8

Simulation 132

0.0

0.4

Uniform Percentiles

0.0

Predicted Percentiles of Outcomes

Uniform Percentiles

0.2

0.0

0.2

0.4

0.6

0.8

Uniform Percentiles

1.0

Simulated Fits

Simulation 24

7000

7000

9000

11000

Simulation 91

7000

9000

11000

Loss

Loss

Simulation 132

Simulation 4

9000

Loss

11000

7000

9000

Loss

11000

View Maximum Likelihood

As an Estimation Strategy

• If you estimate distributions by maximum

likelihood repeatedly, how well do you do

in the aggregate?

• Consider a space of possible parameters

for a model

• Select parameters at random

– Select a sample for estimation (training)

– Select a sample for post-estimation (testing)

Continuing Prior Slide

• Select parameters at random

– Select a sample for estimation (training)

– Select a sample for post-estimation (testing)

• Fit a model for each training sample

• Calculate the predicted percentiles of the

testing sample.

• Combine for all samples.

• In the aggregate, the predicted percentiles

should be uniformly distributed.

1.0

PP Plots for Normal Distribution (n = 3)

0.6

0.4

0.0

0.2

Predicted Percentiles of Outcomes

0.8

ML

Bias Corrected ML

0.0

0.2

0.4

0.6

0.8

1.0

Uniform Percentiles

S-Shaped PP Plot - Tails are too light!

Problem – How to Fit Distribution?

• Proposed solution – Bayesian Analysis

• Likelihood = Pr{Data|Model}

• We need Pr{Model|Data} for each model in

the prior

Predictive Distribution

Model Distribution Pr Model|Data

Model

Bayesian Fits

• Predictive

distributions are

spread out more

than the MLE’s.

• On individual fits,

they do not always

match the testing

data.

7000

Simulation 24

Simulation 91

Bayes

ML

Bayes

ML

9000

11000

7000

11000

Loss

Loss

Simulation 132

Simulation 4

Bayes

ML

7000

9000

9000

Loss

Bayes

ML

11000

7000

9000

Loss

11000

Bayesian Fits as a Strategy

Combined PP Plot for

0.0

0.2

0.4

0.6

0.8

1.0

Bayesian Fitting Strategy

Predicted Percentiles of Outcomes

• Parameters of model

were selected at

random from the prior

distribution

• Near perfect uniform

distribution of

predicted percentiles

• At least in this

example, the

Bayesian strategy

does not overfit.

0.0

0.2

0.4

0.6

Uniform Percentiles

0.8

1.0

Analyze Overfitting in Loss

Reserve Formulas

• Many candidate formulas - Pick a good one

E Paid LossAY ,Lag PremiumAY ELR Dev Lag

• Paid LossAY,Lag ~ Collective Risk Model

• Claim count distribution is negative binomial

• Claim severity distribution is Pareto

– Claim severity increases with settlement lag

• Calculate likelihood using FFT

Simulation Testing Strategy

• Select triangles of data at random

– Payment pattern at random

– ELR at random

– {Loss|Expected Loss} for each cell in the

triangle from Collective Risk Model

• Randomly select outcomes using the same

payment pattern and ELR

• Evaluate the Maximum Likelihood and

Bayesian fitting methodology with PP plots.

Background on Formula

• Same formula appeared in SessionV2

• Fit a Bayesian model to over 100 insurers

and produced an “acceptable” combined

PP plot on test data from six years later.

• This paper tests the approach to simulated

data, rather than real data.

0.25

Prior Payout Patterns

0.00

0.05

0.10

D ev Lag

0.15

0.20

Fixed Subpopulation

2

4

6

L ag

8

10

Prior Probabilities for ELR

ELR

0.600

0.625

0.650

Prior

3/24

4/24

5/24

ELR

0.675

0.700

0.725

Prior

4/24

3/24

2/24

ELR

0.750

0.775

0.800

Prior

1/24

1/24

1/24

Selected Individual Estimates

Simulation 4

Simulation 6

Bayes

ML

50000

70000

90000

110000

Bayes

ML

50000

70000

90000

Loss

Loss

Simulation 12

Simulation 17

Bayes

ML

50000

70000

90000

Loss

110000

110000

Bayes

ML

50000

70000

90000

Loss

110000

0.6

0.4

0.2

0.0

Predicted Probability

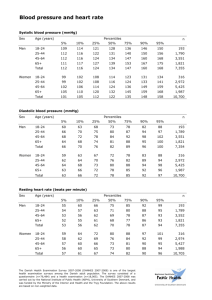

• PP plot reveals

the S-shape that

characterizes

overfitting.

• The tails are too

light

0.8

1.0

Maximum Likelihood Fitting Methodology

PP Plots for Combined Fits

0.0

0.2

0.4

0.6

Uniform Probability

0.8

1.0

0.6

0.4

0.2

0.0

Predicted Probability

Nailed the

Tails

0.8

1.0

Bayesian Fitting Methodology

PP Plots for Combined Fits

0.0

0.2

0.4

0.6

Uniform Probability

0.8

1.0

Summary

• Examples illustrate the effect of overfitting

• Bayesian approach provides a solution

• These examples are based on simulated

data, with the advantage that the “prior” is

known.

• Previous paper extracted prior distributions

from maximum likelihood estimates of

similar claims of other insurers

Conclusion

• It is not enough to know if assumptions are

correct.

• To avoid the light tails that arise from overfitting,

one has to get information that is:

Outside

The

Triangle