Chapter 12 Control Systems: Control Accounts

advertisement

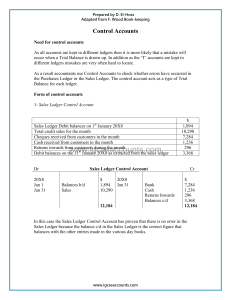

Chapter 12 Control Systems: Control Accounts Control Systems: Control Accounts Accountants use two general ledger accounts to help ensure the accuracy of the sales ledger and the purchases ledger. These two accounts are the: Debtors' control account (also called the Sales ledger control account) and Creditors' control account (also called the Purchases ledger control account) Debtors' Control Account (Sales Ledger Control Account) The debtors' control account is compiled from the general journal, cash book and the totals in the sales and sales returns journals. The balances in this control account should always be equal to the sum of all the balances in the sales ledger. If there is inequality, the accountant will need to find the source of the difference and have this corrected. Debtors' control account (Sales ledger control account) Creditors' Control Account (Purchases Ledger Control Account) The creditors' control account is compiled from the general journal, cash book and the totals in the purchases and purchases returns journals. The balances in this control account should always be equal to the sum of all the balances in the purchases ledger. Creditors' Control Account (Purchases Ledger Control Account)