Solutions to Exam 1 Multiple Choice 1. a

advertisement

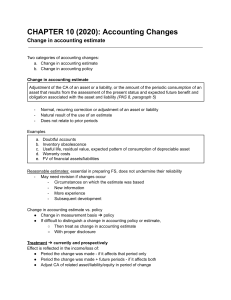

Solutions to Exam 1 Multiple Choice 1. a 2. d 3. c 4. d 5. e 6. b 7. c 8. d 9. a 10. a 11. c 12. a 13. b 14. c 15. a Problem 1: 1. Cash Common Stock 2. Supplies A/P 3. Equipment Cash Note Payable 35000 35000 400 400 6000 2500 3500 4. A/R Revenue 4400 5. Rent Expense Cash 700 6. A/P Cash 200 4400 700 200 7. Advertising Expense A/P 1500 8. Salaries Expense Cash 2200 9. Dividends Cash 1200 10. Cash A/R 3000 1500 2200 1200 3000 Problem 2 The errors are as follows: 1. On the statement of earnings the date should be “for the period ending” 2. On the statement of earnings, Unearned Sales Revenue should just be Revenue 3. Prepaid expenses is an asset and should not be on the statement of earnings 4. The beginning date of the retained earnings should be Dec. 31, 03 5. The ending date of the retained earnings should be Dec 31, 04 6. Patent is not a current asset. It should be in the long term asset or intangible category 7. Accumulated amortization should be subtracted from the equipment 8. Accounts Receivable is a current asset and it should be in the current category 9. the balance sheet does not balance 10. the ending Retained earnings balance has not been put on the balance sheet in the equity section Problem 3 1. A/R Revenue 2. Property Tax Expense A/P 3. Unearned Revenue Revenue 4. Insurance Expense Prepaid insurance 270 270 700 700 600 600 240 240 5. Salaries Expense Salaries Payable 950 950 Short Essay Revenue recognition is the principle in accounting that states that revenue can only be recorded when it has been earned…the service performed or the goods delivered. Matching principle in accounting states that the expenses must be recorded in the same period that the related revenue is earned. You must record the expenses incurred to generate revenue in the same period. These concepts are important to accrual accounting because using both of these concepts ensures that the net earnings or net income stated for a certain accounting period are a fair and accurate representation of the operations of the business.