January 30, 2015

advertisement

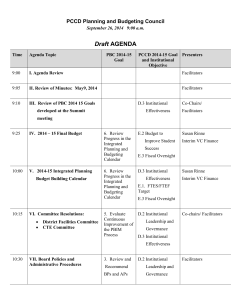

Peralta Community College District PCCD Planning and Budgeting Council___________________ Date of Meeting: January 30, 2015 Present: Norma Ambriz-Galaviz, James Blake, Joi Lin Blake, Fred Bourgoin, Debbie Budd, Paula Coil, Lisa Cook, Matthew Goldstein, Rick Greenspan, Stefanie Harding, Brandi Howard, Sadiq Ikharo, Jennifer Lenahan, Calvin Madlock, Anna O’Neal, Mike Orkin, Tae-Soon Park, Jennifer Shanoski, Cleavon Smith, Sui Song, Elnora Webb Chair/Co-Chair: Susan Rinne, Karolyn van Putten Guests: Nikki Washington, Phyllis Carter, Indra Thadani, Carolyn Martin, Dettie Del Rosario, Tom Wong Facilitator/Recorder: Linda Sanford, Joseph Bielanski Absent: Drew Gephart, Timothy Brice, Carl Oliver, Jeramy Rolley Agenda Item PBC 2014-15 Committee Goal PCCD 2014-15 Strategic Planning Goal and/or Institutional Objective Meeting Called to Order 1. Agenda Review (Facilitator) 2. Review of Minutes: December 12, 2015 (Facilitator) 3. Revised PBC Topics Calendar (Facilitator) Discussion Start: 9:11AM D.3. Institutional Effectiveness Motion (Dr. Webb, Dr. Budd) APPROVED Motion (Dr. Webb, Dr. van Putten) APPROVED Abstain: 1 Informational item Follow-up Action Decisions (Shared Agreement/ Resolved or Unresolved} 4. State Budget Update (VC Rinne) D.3. Institutional Effectiveness E.3 Fiscal Oversight VC Rinne attended the State Chancellor’s budget workshop. VC Rinne will update the PBC once additional information is received from the State Chancellor’s Office. The proposed budget includes $200 million for Student Success and $125 million increase to the base apportionment. There is a new formula for funding growth. Peralta is eligible for 1% of growth. Note: SSSP funding is the former Matriculation funding. It has been in place for decades. Although it is presented as onetime funding, it is ongoing. Per Dr. Budd, we are chasing growth. This year we are budgeted at 5% and will need to jump to 7% for next fiscal year. We have different strategies in place to address it. In regards to MIS reporting, Dr. Blake commented that it is critical as to how Student Services is documenting FTES. There are three types of rates: Credit, Non-credit, and Career Development & College Preparation Program (CDCP). CDCP will be funded at the same rate as credit. We currently don’t report any CDCP, but will look VC Rinne will post the spreadsheet on the webpage. into it. Mr. Blake asked about Professional Development funding for staff and faculty. Mr. Greenspan would like a report on the $500M Adult Education Block Grant. Student Equity Funding Distribution: The administration at the District office is here to serve as an extension to the colleges. The PASS program is a district-wide initiative. When the PASS program was initiated, there were many programs that overlap at the colleges. Rather than having it implemented at each college, it would be implemented districtwide. The PASS program was initially to be funded through the parcel tax. The parcel tax cannot be used for administrator salaries; therefore the administration part of the PASS projects is to be funded by equity funding. It is a district-wide expense housed at the District. Per Dr. Webb, to honor the Chancellor by restating what was said, the Chancellor made it very clear that he didn’t know the particulars of what would occur and that he would be relying on VC Rinne will research it. The PBC will invite Ms. Karen Engel to present at the next PBC meeting. the advisory group to inform him. Someone needs to be assigned to coordinate the PASS initiative. The District individual would be a catalyst to bring all this together and provide administrative leadership, collect data, coordinate activities, convene the group, and advance something that is strategic in order to address the gap that exists in student achievement. Concern was expressed that the advisory group is not part of the shared governance process, but will have the power to come up with a plan/budget recommendation to the Chancellor. Equity dollars are not allocated to the college, the budgets for the equity dollars are. We received a little over $500,000 in November, $100,000 in December, and $68,000 in January. It is not a matter as to when the dollars were received, but how much was to be allocated for budgeting purposes. Originally the State did not allow us to spend the funding until the equity plans were approved, but the State later allowed expenditure. Allocations to the colleges were budgeted at the end of December. Per Dr. Webb the State Chancellor, Brice Harris, conveyed to the CEO Board of the league that it is important for districts to spend 100% of the funds by the deadline. It will signal to the people who approved these funds that we in fact need these funds. The State Chancellor is looking to extend the deadline to the end of September or December. 5. 2013-14 Financial Report (Audit) and Corrective Action Matrix (VC Rinne and Mr. Wong) 6. Monitor Progress in the Integrated Planning and Budgeting Calendar D.3. Institutional Effectiveness E.3 Fiscal Oversight At the January 2015 Board meeting, Vavrinek Trine & Day (VTD) came and presented to the Board. VTD issued an unmodified opinion on our June 30, 2014 audit. We have a clean audit with no audit adjustments. There are a few repeated audit findings. Our Internal Auditor, Tom Wong, has taken a lead on all the audit findings. He is working on financial aid implementation challenges, such as reporting issues. The first finding (new finding) was on how our Other PostEmployment Benefits (OPEB) liability is funded. The District is facing a possible challenge down the road due to the increase liability in our OEPB obligation. Peralta sold $153M in bonds and the bonds were placed it in a revocable trust. The value of the trust is at $216M. There is an OPEB obligation charge, as a percentage of salary, which is based on the actuarial study. At the end of the fiscal year, we take funding out of the trust to reimburse the general fund for retiree medical benefits paid during the year. Over the years, the payments going in are less than the amounts going out because the medical cost for retirees is increasing. In addition, we had to pay the debt service liability that continues to grow. To resolve this issue, based on GASB 45, the investments in the revocable trust with Neuberger Bergman need to be placed into an irrevocable trust. The plan is to put the amount needed to pay for retirees’ medical benefits into the irrevocable trust. The amount that is over and beyond the actuarial amount can be placed into a revocable trust to offset the debt service. At the Retirement Board meeting last night, the deadline to complete the split is by June 30, 2015. AVC Madlock requested that IT be made aware of any audit finding that involves IT so that IT will not be caught off-guard. 6. Updated Budget Assumptions for 2015-16 (VC Rinne) D.3. 6. Monitor Progress in the Institutional Effectiveness This is in draft form and is being shared for the first time. Integrated Planning and Budgeting Calendar The first six are general assumptions. E.3 Fiscal Oversight #8 Access: We are budgeting for 0% growth because 2014/15 is the last year to recapture FTES that were taken from us for workload reduction. We built the budget based on 19,500 FTES. We will need to borrow from the summer to achieve 19,500 FTES and in order for us to be funded at that level for the next fiscal year. #9 COLA: 1.58% #15 Parcel Tax: This will be our fourth year. We have two more years to go. #24 Medical & Dental: We will use the five year average as recommended by Mr. Greenspan. #25 OPEB Contributions: We are in the process of having an actuarial study done. We should have the numbers in the next four weeks and will update the rates accordingly. #27 Utilities: 2% has been the standard rate. Concern was expressed by Ms. Carter that 2% is insufficient to cover the cost increase notifications received from utility companies. Request was made for the PBC to look at increasing the percentage. AVC Sanford suggested that we look into total cost of ownership plan in the next fiscal year. #28 SEIU Backfill & #29 PFT VC Rinne will work Release Time: Concern was with Cabinet expressed by Mr. Greenspan as to members on this. why these two items were chosen while other contractual obligations were not. #30 Workers’ Comp.: Connected to audit finding #2014-001. 7. FTES Targets Status Report (VC Orkin) 6. Monitor Progress in the Integrated Planning and Budgeting Calendar D.3. Institutional Effectiveness E.1. FTES/FTEF Target E.3 Fiscal Oversight FTES/FTEF Worksheet 5th row from the bottom (highlighted) = shortfall. The District is 1209 FTES below target. In order to catch up, we will offer late start classes, intersessions, and borrow from the summer session. A typical summer session at Peralta brings in between 2000 to 2500 FTES. We need to start planning how to meet next year’s target. FTEF numbers are based on FTES numbers. Meetings have been scheduled at each college and the Public Information department had an aggressive advertising campaign to address the shortfall in FTES. The Finance department had discussions with College Presidents about appropriate budgeting. In the past, we dropped students for nonpayment at the $50 threshold. In Cabinet, the threshold was increased to $500. We are also planning to change the policy to allow payment plans for fees owed from prior semesters. Per Dr. Blake, we need to be mindful that we are a District; if one college fails, we all fail. 8. Draft PCCD 2015 Strategic Plan (AVC Sanford) 6. Monitor D.3. Progress in the Institutional Integrated Effectiveness Planning and Budgeting Calendar This is the draft version that was presented at Flex Day. AVC Sanford took what we already had from 2008 and made it current. This is a work in progress. Suggestions were noted and some changes were already. The intent is to reorganize the document and include the mission/goal section in the beginning of the document. The Strategic Plan is going to the Board in March. The Plan will have a new cover and printed in March. 9. Institutional SelfEvaluation Actionable Improvement Plans (AVC Sanford) 7. Receive from the colleges monthly update reports regarding their Institutional Self Evaluation reports . . . . . Informational Only 10. Policies and Administrative 3. Review and Recommend D.3. Institutional Effectiveness Laney is developing an internal college actionable improvement plan. Per Dr. Webb, feedback was received and an action plan was created for those items not related to the standard to insure continuous improvement at Laney. D.2 Institutional AP 6551 Inventory of Property Leadership and and Equipment Please email AVC Sanford if you have any feedback/comments. Laney will share their action plan with the other colleges. Procedures (Dr. Bielanski) Board Policies Governance and Administrative Procedures. The AP was developed in response to an audit finding (#2014-006). The Director of Purchasing, Marie Hampton, took what was used at other districts and added to it. Mr. Blake suggested that for the first #E, we need identify equipment that has been taken home. Concern was expressed by Mr. Greenspan that the Department Chair is personally responsible for “any damage to or loss of equipment” as stated at the bottom of the Inventory Property and Equipment Form. Concern was expressed by Ms. Harding in regards to the manpower needed to implement this procedure at the colleges. Per AVC Madlock, there is an inventory management module in PeopleSoft that we might be able to activate when we upgrade the Finance module. Ms. Coil suggested that we add campus tracking to the form. VC Rinne recommends that we bring back AP 6551 to the next PBC to give Purchasing an opportunity to address the concerns with item #E, the letter, and the form. 11. Adjournment 11:33a.m. Minutes taken by: Sui Song Attachments: All documents and/or handouts for this meeting can be found at: http://web.peralta.edu/pbi/planning-and-budgeting-council/pbc-documents/ http://web.peralta.edu/pbi/planning-and-budgeting-council/minutes/ Next Meeting: February 27, 2015 10:45a.m. – 1:45p.m.