Administration's FY 2015 Budget Proposal All Major Tax Provisions

advertisement

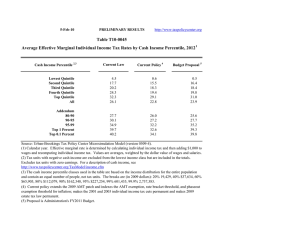

30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2023 ¹ Summary Table Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Tax Units Number (thousands) Percent of Total Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate 5 Change (% Points) Under the Proposal 44,500 37,598 35,272 28,346 25,147 172,542 25.8 21.8 20.4 16.4 14.6 100.0 1.8 0.3 -0.1 -0.3 -1.5 -0.7 -12.4 -3.9 1.1 8.7 106.4 100.0 -333 -124 39 368 5,052 692 -1.7 -0.3 0.0 0.2 1.1 0.5 2.8 8.3 14.8 17.4 26.8 20.8 12,783 6,110 4,968 1,286 130 7.4 3.5 2.9 0.8 0.1 -0.1 -0.5 -1.5 -3.1 -3.5 2.2 6.0 25.5 72.8 35.3 206 1,165 6,116 67,564 323,609 0.1 0.4 1.2 2.1 2.3 19.5 21.7 25.5 35.4 37.6 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). Number of AMT Taxpayers (millions). Baseline: 6.1 Proposal: 5.9 (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2013 dollars): 20% $26,827; 40% $54,460; 60% $95,241; 80% $156,821; 90% $230,152; 95% $304,802; 99% $779,814; 99.9% $4,723,866. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2023 ¹ Detail Table Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 5 Change (% Points) Under the Proposal 1.8 0.3 -0.1 -0.3 -1.5 -0.7 -12.4 -3.9 1.1 8.7 106.4 100.0 -333 -124 39 368 5,052 692 -37.6 -3.0 0.3 1.4 4.2 2.7 -0.4 -0.2 -0.3 -0.2 1.0 0.0 0.5 3.4 10.3 16.5 69.1 100.0 -1.7 -0.3 0.0 0.2 1.1 0.5 2.8 8.3 14.8 17.4 26.8 20.8 -0.1 -0.5 -1.5 -3.1 -3.5 2.2 6.0 25.5 72.8 35.3 206 1,165 6,116 67,564 323,609 0.5 1.7 4.8 6.3 6.4 -0.3 -0.1 0.3 1.1 0.5 12.8 9.5 14.7 32.2 15.3 0.1 0.4 1.2 2.1 2.3 19.5 21.7 25.5 35.4 37.6 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 44,500 37,598 35,272 28,346 25,147 172,542 25.8 21.8 20.4 16.4 14.6 100.0 19,943 48,962 90,176 152,357 466,904 127,159 4.0 8.4 14.5 19.7 53.5 100.0 886 4,182 13,318 26,158 120,213 25,734 0.9 3.5 10.6 16.7 68.1 100.0 19,057 44,780 76,857 126,199 346,691 101,425 4.9 9.6 15.5 20.4 49.8 100.0 4.4 8.5 14.8 17.2 25.8 20.2 12,783 6,110 4,968 1,286 130 7.4 3.5 2.9 0.8 0.1 232,985 326,077 528,443 3,222,719 14,263,796 13.6 9.1 12.0 18.9 8.5 45,260 69,597 128,370 1,073,976 5,032,507 13.0 9.6 14.4 31.1 14.7 187,725 256,479 400,073 2,148,743 9,231,289 13.7 9.0 11.4 15.8 6.9 19.4 21.3 24.3 33.3 35.3 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). Number of AMT Taxpayers (millions). Baseline: 6.1 Proposal: 5.9 (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2013 dollars): 20% $26,827; 40% $54,460; 60% $95,241; 80% $156,821; 90% $230,152; 95% $304,802; 99% $779,814; 99.9% $4,723,866. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Average Federal Tax Rate Under the Proposal Change (% Points) 5 Under the Proposal 2.4 0.4 0.0 -0.1 -1.5 -0.7 -13.7 -4.2 0.4 1.7 115.8 100.0 -452 -138 13 63 4,361 692 -164.2 -4.1 0.1 0.3 4.3 2.7 -0.4 -0.2 -0.2 -0.4 1.1 0.0 -0.1 2.6 7.9 16.1 73.3 100.0 -2.4 -0.3 0.0 0.1 1.1 0.5 -0.9 7.5 13.0 16.9 26.5 20.8 -0.3 -0.6 -1.3 -3.2 -3.6 7.1 8.2 25.2 75.4 38.3 524 1,271 4,639 60,738 301,529 1.4 2.1 4.3 6.4 6.7 -0.2 -0.1 0.2 1.1 0.6 13.9 10.3 16.1 33.1 16.0 0.3 0.5 1.0 2.1 2.4 19.7 21.4 25.0 35.3 37.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 36,160 36,291 33,999 32,725 31,689 172,542 21.0 21.0 19.7 19.0 18.4 100.0 18,975 43,302 81,191 132,960 397,610 127,159 3.1 7.2 12.6 19.8 57.4 100.0 275 3,399 10,550 22,430 101,137 25,734 0.2 2.8 8.1 16.5 72.2 100.0 18,700 39,903 70,641 110,531 296,473 101,425 3.9 8.3 13.7 20.7 53.7 100.0 1.5 7.9 13.0 16.9 25.4 20.2 16,056 7,679 6,472 1,482 152 9.3 4.5 3.8 0.9 0.1 199,688 283,721 454,467 2,883,799 12,799,934 14.6 9.9 13.4 19.5 8.9 38,903 59,560 108,880 957,024 4,514,145 14.1 10.3 15.9 31.9 15.4 160,785 224,161 345,587 1,926,774 8,285,789 14.8 9.8 12.8 16.3 7.2 19.5 21.0 24.0 33.2 35.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). Number of AMT Taxpayers (millions). Baseline: 6.1 Proposal: 5.9 (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table - Single Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Average Federal Tax Rate 5 Share of Federal Taxes Change (% Points) Under the Proposal Change (% Points) Under the Proposal 2.6 0.2 -0.1 -0.3 -2.4 -0.8 -21.0 -3.5 2.2 7.1 115.0 100.0 -350 -63 52 209 4,552 456 -34.8 -2.2 0.7 1.2 7.1 3.6 -0.8 -0.3 -0.3 -0.5 2.0 0.0 1.4 5.5 11.6 20.6 60.6 100.0 -2.4 -0.2 0.1 0.2 1.8 0.7 4.5 8.7 13.2 18.5 27.3 19.4 -1.3 -1.3 -2.3 -5.0 -5.6 20.6 9.9 26.6 57.8 29.7 1,439 1,915 5,484 65,729 331,782 5.0 4.7 7.1 9.4 9.4 0.2 0.1 0.5 1.2 0.6 15.1 7.8 14.1 23.6 12.1 1.0 1.0 1.7 3.3 3.5 21.5 22.2 25.8 38.1 40.9 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 20,234 18,704 14,241 11,410 8,509 73,898 27.4 25.3 19.3 15.4 11.5 100.0 14,557 32,828 59,609 94,226 251,068 67,132 5.9 12.4 17.1 21.7 43.1 100.0 1,004 2,903 7,790 17,177 64,020 12,566 2.2 5.9 12.0 21.1 58.7 100.0 13,553 29,926 51,819 77,049 187,048 54,566 6.8 13.9 18.3 21.8 39.5 100.0 6.9 8.8 13.1 18.2 25.5 18.7 4,827 1,749 1,636 296 30 6.5 2.4 2.2 0.4 0.0 140,001 193,289 321,231 2,015,244 9,446,746 13.6 6.8 10.6 12.0 5.7 28,681 41,009 77,337 702,424 3,532,616 14.9 7.7 13.6 22.4 11.5 111,320 152,280 243,894 1,312,820 5,914,130 13.3 6.6 9.9 9.6 4.4 20.5 21.2 24.1 34.9 37.4 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table - Married Tax Units Filing Jointly Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Average Federal Tax Rate 5 Share of Federal Taxes Change (% Points) Under the Proposal Change (% Points) Under the Proposal 2.1 0.5 0.0 0.0 -1.3 -0.8 -3.4 -2.6 0.0 -0.5 106.5 100.0 -541 -249 1 -27 4,294 1,281 -393.7 -5.3 0.0 -0.1 3.7 2.7 -0.1 -0.1 -0.2 -0.4 0.7 0.0 -0.1 1.3 5.4 13.9 79.4 100.0 -2.0 -0.4 0.0 0.0 0.9 0.6 -1.5 7.6 12.6 16.1 26.3 22.2 -0.1 -0.4 -1.1 -2.8 -3.3 1.5 6.8 23.1 75.1 37.3 127 1,061 4,383 58,705 293,142 0.3 1.6 3.6 5.8 6.1 -0.3 -0.1 0.2 1.1 0.6 13.8 11.4 17.5 36.7 17.3 0.1 0.3 0.9 1.9 2.1 19.1 21.2 24.7 34.8 37.1 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 5,436 9,236 13,569 17,691 21,701 68,289 8.0 13.5 19.9 25.9 31.8 100.0 26,576 58,765 103,303 160,423 458,255 217,501 1.0 3.7 9.4 19.1 67.0 100.0 137 4,707 13,028 25,910 116,082 46,927 0.0 1.4 5.5 14.3 78.6 100.0 26,439 54,058 90,275 134,513 342,173 170,574 1.2 4.3 10.5 20.4 63.8 100.0 0.5 8.0 12.6 16.2 25.3 21.6 10,343 5,634 4,605 1,119 111 15.2 8.3 6.7 1.6 0.2 230,259 314,419 505,519 3,094,372 13,726,125 16.0 11.9 15.7 23.3 10.3 43,864 65,471 120,623 1,019,414 4,804,760 14.2 11.5 17.3 35.6 16.7 186,395 248,948 384,896 2,074,958 8,921,365 16.6 12.0 15.2 19.9 8.5 19.1 20.8 23.9 32.9 35.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table - Head of Household Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Average Federal Tax Rate 5 Share of Federal Taxes Dollars Percent Change (% Points) Under the Proposal Change (% Points) Under the Proposal 2.5 0.4 0.1 0.0 -1.0 0.4 103.0 26.3 6.7 -0.9 -36.2 100.0 -628 -213 -78 21 2,411 -230 53.7 -7.5 -0.7 0.1 3.1 -3.0 -3.3 -0.5 0.7 1.0 2.2 0.0 -9.0 10.0 30.2 31.3 37.4 100.0 -2.6 -0.4 -0.1 0.0 0.8 -0.4 -7.5 5.2 13.6 17.9 26.1 11.7 -0.1 -0.4 -1.1 -2.8 -3.1 -1.1 -2.2 -8.1 -24.8 -11.6 113 855 3,271 47,743 265,862 0.3 1.4 3.4 5.7 5.7 0.4 0.2 0.5 1.2 0.5 10.9 4.9 7.5 14.2 6.6 0.1 0.3 0.8 1.9 2.0 20.9 23.3 25.1 34.7 37.0 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 10,087 7,600 5,258 2,767 923 26,775 37.7 28.4 19.6 10.3 3.5 100.0 23,866 50,782 85,209 127,009 312,466 64,080 14.0 22.5 26.1 20.5 16.8 100.0 -1,170 2,862 11,645 22,741 78,974 7,743 -5.7 10.5 29.5 30.4 35.2 100.0 25,036 47,920 73,564 104,268 233,492 56,337 16.7 24.1 25.6 19.1 14.3 100.0 -4.9 5.6 13.7 17.9 25.3 12.1 577 161 153 32 3 2.2 0.6 0.6 0.1 0.0 180,975 261,097 391,241 2,574,380 13,287,094 6.1 2.5 3.5 4.8 2.1 37,707 60,083 95,030 844,264 4,647,713 10.5 4.7 7.0 13.0 6.0 143,268 201,014 296,211 1,730,116 8,639,381 5.5 2.2 3.0 3.7 1.5 20.8 23.0 24.3 32.8 35.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table - Tax Units with Children Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Share of Federal Taxes Dollars Percent Change (% Points) Average Federal Tax Rate Under the Proposal Change (% Points) 5 Under the Proposal 2.5 0.6 0.1 0.1 -1.3 -0.4 -29.7 -13.4 -2.8 -4.1 150.5 100.0 -682 -340 -72 -111 4,860 525 44.5 -9.1 -0.5 -0.4 3.6 1.7 -0.5 -0.3 -0.2 -0.4 1.3 0.0 -1.6 2.2 9.3 18.0 71.9 100.0 -2.7 -0.6 -0.1 -0.1 0.9 0.3 -8.7 5.8 13.4 16.8 26.9 20.0 -0.1 -0.8 -1.6 -2.5 -2.8 2.5 17.8 39.9 90.2 41.3 163 2,182 7,128 58,714 281,709 0.3 2.8 4.7 4.9 5.0 -0.2 0.1 0.4 1.0 0.5 13.9 10.9 14.9 32.3 14.4 0.1 0.6 1.2 1.7 1.8 19.9 22.0 26.0 35.4 37.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 12,783 11,562 11,260 10,716 9,078 55,806 22.9 20.7 20.2 19.2 16.3 100.0 25,475 58,693 108,192 175,109 518,134 157,555 3.7 7.7 13.9 21.3 53.5 100.0 -1,535 3,742 14,573 29,599 134,237 30,938 -1.1 2.5 9.5 18.4 70.6 100.0 27,010 54,951 93,619 145,510 383,897 126,617 4.9 9.0 14.9 22.1 49.3 100.0 -6.0 6.4 13.5 16.9 25.9 19.6 4,587 2,398 1,642 450 43 8.2 4.3 2.9 0.8 0.1 267,619 364,164 611,192 3,551,563 15,743,917 14.0 9.9 11.4 18.2 7.7 52,955 77,821 151,741 1,199,171 5,599,871 14.1 10.8 14.4 31.3 13.9 214,664 286,343 459,451 2,352,392 10,144,047 13.9 9.7 10.7 15.0 6.2 19.8 21.4 24.8 33.8 35.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income. 30-Jun-14 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T14-0054 Administration's FY 2015 Budget Proposal All Major Tax Provisions Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Detail Table - Elderly Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Average Federal Tax Rate Under the Proposal Change (% Points) 5 Under the Proposal 0.1 0.1 -0.1 -0.3 -2.5 -1.4 -0.2 -0.4 1.0 4.0 95.4 100.0 -20 -24 51 279 6,700 1,320 -12.9 -2.4 0.9 1.8 7.8 6.4 0.0 -0.1 -0.3 -0.6 1.0 0.0 0.1 1.1 6.1 13.5 79.2 100.0 -0.1 -0.1 0.1 0.2 1.9 1.1 0.8 2.7 8.1 13.6 26.0 18.9 -1.2 -0.9 -1.9 -4.9 -5.8 11.8 6.0 17.4 60.2 30.9 1,661 1,731 5,911 85,166 429,476 5.8 3.7 6.5 10.1 10.9 -0.1 -0.3 0.0 1.3 0.8 12.9 10.0 17.0 39.3 18.8 1.0 0.7 1.5 3.3 3.8 17.6 19.7 24.0 35.9 38.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2023 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax Rate 5 5,833 10,414 10,781 8,405 8,262 43,929 13.3 23.7 24.5 19.1 18.8 100.0 17,250 36,841 67,748 114,203 357,289 116,731 2.0 7.5 14.2 18.7 57.6 100.0 153 1,034 5,409 15,266 86,257 20,763 0.1 1.2 6.4 14.1 78.1 100.0 17,097 35,807 62,339 98,937 271,032 95,968 2.4 8.9 15.9 19.7 53.1 100.0 0.9 2.8 8.0 13.4 24.1 17.8 4,122 2,025 1,704 410 42 9.4 4.6 3.9 0.9 0.1 171,828 243,653 403,624 2,590,079 11,326,380 13.8 9.6 13.4 20.7 9.2 28,611 46,264 90,963 843,650 3,934,661 12.9 10.3 17.0 37.9 18.0 143,218 197,388 312,661 1,746,429 7,391,719 14.0 9.5 12.6 17.0 7.3 16.7 19.0 22.5 32.6 34.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0613-3). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law. Proposal would (a) extend ARRA enhancements to the refundable child tax credit and earned income tax credit; (b) replace Hope credit with the American Opportunity Tax Credit; (c) provide incentives for job creation, clean energy, and manufacturing; (d) provide incentives for investment in infrastructure; (e) increase earned income tax credit for taxpayers without qualifying children by doubling maximum credit and expanding age eligibility; (f) implement auto-IRA provision with small employer credit ; (g) expand child and dependent care credit for qualifying children under 5; (h) exclude Pell Grants from income and tax credit calculations; (i) limit the value of itemized deductions and certain other deductions and exclusions to 28 percent; (j) enact the Fair Share Tax (“Buffett rule”); (k) restore 2009 estate tax law (45 percent rate and $3.5 million unindexed exemption); (l) impose a financial crisis responsibility fee; (m) tax carried interests (profits) as ordinary income; (n) limit accrual in tax favored retirement accounts; (o) conform SECA taxes for professional service businesses; (p) reinstate Superfund income and excise taxes; (q) increase tobacco excise taxes and index for inflation; (r) make unemployment insurance surtax permanent and expand FUTA base; (s) eliminate deduction for dividends from employee stock ownership plans; and (t) simplify rules for claiming the childless EITC. For a description of TPC's current law baseline, see: http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2013 dollars): 20% $18,678; 40% $35,821; 60% $60,717; 80% $95,966; 90% $135,210; 95% $184,371; 99% $473,923; 99.9% $2,793,265. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average expanded cash income.