Mean-Dispersion Preferences. 16 April 2008

advertisement

16 April 2008

Mean-Dispersion Preferences.

Abstract

The starting point for this paper is the variational preference model introduced by Maccheroni et

al [2006]), which includes Gilboa-Schmeidler multiple-prior preferences and Hansen-Sargent multiplier

preferences.

First, we show that any variational preferences admit a `primal' representation with a natural interpretation: a `mean' expected-utility of the act minus a `dispersion measure' that depends only on

state-by-state di erences from that mean. The second term can be thought of as re ecting the agent's

dislike of dispersion: it is the premium (in terms of the mean utility) that the individual would be willing

to pay to remove all subjective uncertainty associated with the act. The primal representation thus highlights a key behavioral aspect of all variational preferences: the premium does not depend on the average

utility of an act. That is, variational preferences exhibit constant absolute ambiguity aversion.

Second, we develop a generalization of the variational preference model. The generalization is still

based on a mean utility and a dispersion measure that depends only on the state-wise di erences from the

mean. But the new model is only weakly separable in terms of these two summary statistics. Thus, the

ambiguity premium need not be constant in this model. Mean-dispersion preferences can accommodate

many existing models. We show how these correspond to di erent attitudes toward dispersion. Finally,

we use the model to compare di erent notions of aversion to variation across states such as uncertainty

aversion, second-order risk aversion and issue preference.

Keywords: ambiguity aversion, quasi-linearity, weak-separability

Simon Grant

Department of Economics

Rice University

Ben Polak

Department of Economics & School of Management

Yale University

1

Introduction

In a beautiful paper, Maccheroni, Marinacci & Rustichini (2006a) (hereafter MMR) de ne and

axiomatize what they call variational preferences. Consider an Anscombe-Aumann setting with a

nite state space S where each act f maps each state s 2 S to lotteries over outcomes. Variational

preferences are de ned by an expected utility function U over such lotteries and by a convex,

grounded1 ambiguity index c over probabilities on the states such that the preferences over acts

are represented by

V (f ) =

min

P

fp2[0;1]n :

s

ps =1g

X

s2S

ps U (f (s)) + c (p) ,

where n is the number of states and, for state-utility vector u,

of u with respect to probability vector p.

P

s

(1)

ps us denotes the expectation

Variational preferences are a generalization of the well-known multiple-prior model of Gilboa

& Schmeidler (1989) but unlike multiple-prior preferences, general variational preferences can be

smooth. An important smooth example are the preferences considered by Hansen & Sargent

(2001) in their model of robust control.

Maccheroni, Marinacci & Rustichini (2006a) interpret the `dual' representation in expression

(1) as if the agent were playing a game against a malevolent nature who chooses probabilities to

minimize the utility of the agent but who, if she chooses probability p, has to pay back to the agent

the utility c (p). But as we show in section 2 below, variational preferences also admit a `primal'

representation with an equally natural interpretation. For each variational preference de ned by

expression (1), we can nd an expected utility function U over lotteries, a probability weighting

on the states and a convex, non-negative function

respect to

is zero, with

(0) = 0, such that the preferences over acts are represented by

V (f ) =

where

is the `mean' utility given by

:=

from that mean given by ds := U (f (s))

1

over state-utility vectors whose mean with

P

s

(d) ,

sU

.

The function c is `grounded' if inf c (p) = 0.

1

(2)

(f (s)) and d is the vector of utility di erences

We can think of the function

as a index of dispersion. The interpretation is that the agent

with these preferences dislikes dispersion. More speci cally, for each act f , let xf be the constant

act such that xf

f . Then, the dispersion measure

(d) for the act f is given by

U (xf ):

it is the reduction in expected utility the agent would be willing to accept in return for removing

all the state-contingent utility uncertainty associated with the act. Drawing an analogy from

choice under risk, we can think of xf as corresponding to a certainty equivalent and of

corresponding to an absolute risk premium. Thus,

(d) as

(d) is an \absolute ambiguity premium".2

The `primal' representation in expression (2) highlights a key behavioral implication of the

variational preference model (including multiple priors and robust control). The premium that

the agent is willing to pay to eliminate ambiguity does not change in response to changes in the

agent's mean utility. That is: variational preferences exhibit constant absolute ambiguity aversion.

A constant ambiguity premium is a restrictive assumption. How plausible we nd this restriction may depend on the stories we use to interpret these models. For example, one could

interpret a multiple-prior set as simply re ecting the set of probabilities over states of the world

that the agent perceives as possible. There is no reason for this perceived set to change as the

agent becomes better o , and so, in this interpretation, a constant ambiguity premium is perhaps

quite plausible. But an alternative interpretation of variational preferences (even in the multipleprior case3 ) is that they re ect not just the agent's perceptions of ambiguity but also the agent's

dislike of any perceived ambiguity. Indeed, the term `ambiguity averse' seems to suggest dislike

rather than just perception. If we believe this dislike-of-ambiguity interpretation then it seems

less plausible that ambiguity premia should be constant: just as agents with higher mean wealth

tend to care less about a given monetary risk, so agents with higher mean utility might tend to

care less about a given utility uncertainty.

With this in mind, in section 3 of the paper, we develop a generalization of the variational2 This `ambiguity premium' is the amount that the agent is willing to pay to ensure that she obtains the same

utility in every state. This premium corresponds to the the notion of ambiguity aversion in Ghirardato & Marinacci

(2002).

3 For example, in one story used to interpret "-perturbation models, the agent is thought of as perceiving a

large set of possible probabilities (for example, the entire simplex) but then only putting weight " on the `worst

probability' from this set with the remaining (1 ") on a particular prior. In this case, the `revealed-preference'

multiple-prior set is obviously much smaller than the entire simplex. If we believe the story, it is not obvious that

the " (and hence the revealed multiple-prior set) should remain constant as the agent becomes better o .

2

preferences model that allows ambiguity premia to vary as we change mean utility. The new

model maintains, however, the tractable feature that preferences can be expressed in terms of

two summary statistics: a mean utility and a dispersion measure that depends only on state-wise

utility di erences from that mean. More precisely, we consider preferences that are de ned by an

expected utility function U over lotteries, a weighting vector

dispersion function

on the states and a non-negative

over state-utility vectors whose mean with respect to

is zero, with (0) = 0,

and a continuous function ' ( ; ) increasing in the rst argument and decreasing in the second

with ' (y; 0) = y for all y, such that the preferences over acts are represented by

V (f ) = ' ( ; (d)) ,

where

is the `mean' utility given by

from that mean given by ds := U (f (s))

:=

P

s

sU

(3)

(f (s)) and d is the vector of utility `di erences'

. As before, we can think of as a measure of dispersion.

Thus, these preferences are weakly separable in terms of the mean and the dispersion. We call

such preferences \mean-dispersion preferences". The closest analog of this model in the context

of risk preferences is that of Quiggin & Chambers (2004).4

We provide a (partial) axiomatization of the mean-dispersion model. Our axioms generalize

MMR's axiomatization of variational preferences. The most important change is to weaken MMR's

weak certainty independence axiom which in turn was a weakening of Gilboa & Schmeidler's

(1989) axiom which in turn was a weakening of Anscombe-Aumann's (1963) axiom. Thus, there

is a natural nesting of the models in terms of their behavioral assumptions. In addition, since we

are not working with a dual representation, we can relax the need for preferences to be convex or

even state-monotonic.

An example may help

x ideas. Variance is a natural candidate for a dispersion measure.

The standard mean-variance model is linear in the mean and the variance just as in expression

2. Indeed MMR show that the standard mean-variance model is almost an example of variational

preferences. (The `almost' is because mean-variance preferences are not monotonic). Epstein

(1985) introduced a more general mean-variance model precisely to capture the idea of decreasing

4 Quiggin and Chambers also impose a homotheticity property on the dispersion index. Since they are working

under risk, they obviously do not need to infer the weights from behavior.

3

absolute risk aversion. His mean-variance functionals are weakly separable just as in expression

3. Thus, we can think of Epstein's model as an example of our more general mean-dispersion

preferences. (In fact, since we do not require monotonicity, we do not require an \almost".)

We show below that mean dispersion preferences encompass many existing models with each

corresponding to a particular attitude toward means and dispersion captured by particular forms of

the functions ' and . These include Choquet models that have a non-empty core (Chatteaneuf &

Tallon [2002]) and invariant biseparable preference models that are ambiguity averse (Ghirardato,

Maccheroni and Marinacci [2004]). The main class of existing models that cannot (except in special

cases) be viewed as mean-dispersion preferences are those arising from Klibano , Marinacci and

Mukerji's (2005) second-order SEU framework.

In addition to the papers already mentioned, there are two important related recent papers.

Strzalecki (2007) axiomatizes the important special case of variational preferences represented

by Hansen-Sargent multiplier preference model. He shows that these are the only variational

preferences that satisfy the Savage axioms (applied to Anscombe-Aumann acts). An intuition

for this result in the terms of this paper is to recall that variational preferences exhibit constant

absolute ambiguity aversion or CAAA. There is a unique (Savage) subjective expected utility

model that satis es constant risk premia, the CARA model. Translated to ambiguity, this model

is exactly the Hansen-Sargent model.

Siniscalchi (2007) axiomatizes a model (`Vector Expected Utility') that, like ours, evaluates acts

in terms of a baseline mean expected utility and an adjustment term that depends on variability

across states, but he has a di erent construction and interpretation. An attractive feature of

Sinischalchi's approach is a new axiom based on a natural symmetry condition that allows him to

identify a unique baseline prior. Given this, Siniscalchi does not need even our weak uncertainty

aversion condition to identify baseline priors. The VEU preferences exhibit constant absolute

ambiguity aversion (or `a nity'), hence the intersection of our two current models are those meandispersion preferences which exhibit CAAA and for which the dispersion function is symmetric,

that is,

(d)

( d). But as Siniscalchi points out, it would be interesting to combine the two

approaches: that is, add his new axiom to ours, and then use his equal-mean sets (i.e., those

4

de ned by his baseline priors) to restrict independence. We hope this will be future research.

Section 2 discusses the MMR model focussing on the `primal' representation of expression (2),

and on our interpretation in terms of constant absolute ambiguity aversion. We show how constant

absolute ambiguity aversion is related to MMR's key axiom, weak certainty independence, thus

suggesting an alternate axiomatization of variational preferences.

Section 3 introduces the main axioms and main representation theorem for our more general

mean-dispersion preferences. We show how the model can accommodate (for example) decreasing

ambiguity aversion. In section 3.4, we provide a partial converse theorem for general meandispersion preferences and a full characterization for mean-dispersion preferences that are `smooth'

around certainty. We also show that if preferences admit two mean-dispersion representations like

expression (3) with two di erent weighting vectors

and

0

, then such preferences must satisfy

constant absolute ambiguity aversion.

Section 4 provides examples and discusses monotonicity and convexity of the preferences. We

also axiomatize a model that sits between general mean-dispersion preferences and variational

preferences in that the representation is fully separable in the mean and dispersion but does not

require the (quasi-)linearity in the mean of expression (2). And we provide conditions under

which mean-dispersion models are probabilistically sophisticated. Finally, we contrast attitudes

to ambiguity as re ected by the function (:) with those in other approaches such as that of Ergin

& Gul (2007).

2

The MMR Model - an interpretation.

We work in a standard Anscombe-Aumann setting. To simplify, let the state space S be nite,

i.e. S = fs1 ; : : : ; sn g.5

Let X be the set of simple probability measures on a set of prizes. An

act is a function f : S ! X. With slight abuse of notation, any x in X will also denote the

constant act that yields x in every state. Let F denote the set of acts and continuing our abuse of

notation, X shall also denote the set of constant acts. Both the sets X and F are mixture spaces.

In particular, for any pair of acts f and g in F, and any

5

in (0; 1), take f + (1

MMR (2006a) work in an in nite state space while MMR (2006b) work in a nite state space.

5

) g to be the

act h 2 F, in which h (s) = f (s) + (1

) g (s), for each s in S.

The decision maker's preferences on F are given by a binary relation %. Let

denote the

denote indi erence derived from % in the usual way. For a xed f in F,

strict preference and

a constant act xf is a `certainty-equivalent' of f if f

xf .

Maccheroni, Marinacci and Rustichini (hereafter MMR) consider the following axioms.

A.1 Weak Order. % is transitive and complete.

A.2 Weak Certainty-Independence. For any pair of acts f and g in F, any pair of constant acts

x and y and any

in (0; 1),

f + (1

) x % g + (1

) x ) f + (1

) y % g + (1

) y.

) g % hg and

A.3 Continuity. For any three acts f; g and h in F, the sets f 2 [0; 1] : f + (1

f 2 [0; 1] : h % f + (1

) gg are closed.

A.4 Monotonicity. For any pair of acts f and g in F, if f (s) % g (s) for all s 2 S then f % g.

A.5 Uncertainty Aversion. For any pair of acts f and g in F and any

f

g ) f + (1

in (0; 1),

)g % f

A.6 Non-degeneracy. For some pair of acts f and g in F, f

g.

If we remove axiom A.5 and substitute the standard independence axiom for A.2, then we

obtain the subjective expected utility model. Gilboa & Schmeidler (1989) obtained their multipleprior model by adding A.5 and weakening independence only to apply to mixtures with constant

acts. Their axiom is equivalent to the following:

A.20 Certainty-Independence. For any pair of acts f and g in F, any pair of constant acts x and

y and any ;

in (0; 1],

f + (1

) x % g + (1

) x ) f + (1

6

) y % g + (1

) y.

MMR's axiom A.2 is a signi cant weakening of this. The key di erence is that the weights in

Gilboa & Schmeidler's axiom,

and , may di er along with the constant acts x and y whereas

in MMR's axiom A.2 the weight

is xed: only the constant act changes. In section 3, we weaken

this axiom still further.

In all these approaches, the rst stage is to show that the axioms induce an expected utility

representation over the set of constant acts (i.e., over lotteries).6 Once we have introduced a utility

function on the constant acts, it is natural to map each act to its corresponding state-utility vector,

and to consider the preference relation over these state-utility vectors induced by the underlying

preferences over acts. Thus, let U : X ! R be a von Neumann-Morgenstern representation of the

preferences on constant acts. Then:

De nition 1 (State Utility Vectors) For each f in F, let U

Rn de ned by [U

f be the state-utility vector in

f ] (s) = U (f (s)).

To avoid confusion, we will use upper-case U to denote a utility function and lower case u, u0 , and

u00 to denote generic state-utility vectors.

n

The set of utility vectors induced by U , that is, (U (X)) := fU

f 2 Rn : f 2 Fg, will gener-

ally not include all of Rn . It is convenient, however, to work with the whole of Rn . MMR achieve

this by adapting an axiom of Kopylov (2007, p.5). We use it in its the original form.

A.6 Unboundedness. For any pair of acts f and g in F and any

in X satisfying g

w + (1

) f and z + (1

)g

2 (0; 1), there exist w and z

f .7

With this in place, we can de ne preferences over all state-utility vectors in Rn as follows.

De nition 2 (Induced Preferences) Let %u be the binary relation on Rn de ned by u0 %u u00

if there exists a corresponding pair of acts f 0 and f 00 in F with U f 0 = u0 and U f 00 = u00 , such

that f 0 % f 00 .

6 In MMR's case, this is achieved by showing that their axioms imply Hernstein & Milnor's (1953) weak version

of independence on the constant acts which (given their strong continuity assumption) is su cient for an expected

utility representation

7 MMR only require one of w or z to exist, not necessarily both. Using the slightly stonger condition slightly

simpli es the exposition. MMR's unboundedness axiom is their A.7. Since Strong Unboundedness trivially implies

non-degeneracy, we number it A.6 .

7

Given monotonicity and unboundedness (axioms A.4 and A.6 ), this induced preference relation

over state-utilities inherits order and continuity. Monotonicity and weak-certainty independence

(axioms A.2 and A.4) imply that %u is monotone in the sense that if u0

u00 then u0

u

u00 .

And the uncertainty aversion, axiom, A.5, implies that %u is convex. Constant acts are mapped

to constant state-utility vectors. Let e = (1; : : : ; 1) 2 Rn . We will refer to the set fke : k 2 Rg as

the constant-utility line. By unboundedness and weak certainty independence, there are constant

acts that correspond to each point in this line. In particular, there is a constant act x0 in X, such

that U

2.1

x0 = 0e.

Primal Representation.

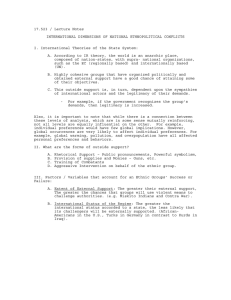

Recall that MMR's key innovation is their new weaker certainty independence axiom (A.2). Figure

1 illustrates this axiom in state-utility space. Let the points on the constant-utility line U x and

U y correspond to the constant acts x and y. Suppose that f +(1

the points U f + (1

) U x and U g + (1

)x

g +(1

) x. Thus,

) U x lie on the same indi erence curve in the

state-utility space.8 Axiom A.2 then implies that U f + (1

) U y and U g + (1

)U y

also lie on the same indi erence curve. More generally, any indi erence set in state-utility space

can be obtained from any other by a translation parallel to the constant-utility line.

The following property formalizes this idea.

De nition 3 (Translation Invariance.) For any pair of utility vectors u0 and u00 in Rn , and

any

2 R, u0 %u u00 ) u0 + e %u u00 + e.

In state-utility space, translation invariance and weak certainty independence are equivalent.

Lemma 1 (Translation Invariance [MMR 2006a]) Given A.1 (weak order), A.3 (continuity), A.4 (monotonicity) and A.6 (unboundedness), the preferences % over acts F satisfy A.2

(weak certainty independence) if and only if the induced preferences %u over state-utility vectors

in Rn satisfy translation invariance.9

8

Recall that the utility function U on X is a ne, so U

9

[ f + (1

) x] = U

f + (1

)U

x.

This result is part of MMR's lemma 28 in appendix B. MMR refer to translation invariance as vertical

invariance.

8

utility in

state 2

0

45 degree line

("constant-utility line")

Uof

αUof +(1−α)Uoy

αUof +(1−α)Uox

Uoy

αUog +(1−α)Uoy

Uog

αUog +(1−α)Uox

Uox

utility in state 1

Figure 1: Weak Certainty Independence implies Translation Invariance in State-Utility Space

The equivalence of weak certainty independence and translation invariance ties down the relationship of MMR's model of ambiguity aversion both to models of risk aversion and to models of

inequality aversion. For example, in social choice, this translation invariance property is known

as \invariance to changes in the common zero".10

We can adapt representation results from these other literatures back to the context of choice

under uncertainty to obtain a `primal' representation corresponding to MMR's `dual' representation. In particular, given translation invariance, we can nd a quasi-linear representation of %u ,

which decomposes into a linear term that can be thought of as a \mean" state-utility minus a

term that depends only on the state-by-state di erences in state-utilities from that \mean". To

make this more precise, for each

2 R and each

constant state-utility vector e with normal vector

2 Rn , let H be the hyperplane though the

; that is, H

= f^

u 2 Rn :

u

^ = g. The

idea for the following representation comes from Roberts's (1980) social choice paper.

10

See, for example, Roberts (1980) Moulin (1988, p.44), and Mas-Colell, Whinston & Green (1995, pp.834-6).

9

Theorem 2 (Primal Representation) A preference relation %u de ned on Rn satis es order, continuity, monotonicity, translation invariance, and convexity if and only if there exist a

monotone function W : Rn ! R that represents %u and takes the form

W (u0 ) =

where

is a vector of non-negative weights (i.e.,

`mean' given by

:=

(d) :

n

2 [0; 1] such that

e = 1),

u0 ; d 2 H 0 is the vector of `di erences' given by d := u0

: H 0 ! R+ is a convex function with

2 R is the

e; and where

(0) = 0.

Notice that, although axiom A.5, uncertainty aversion, by itself only implies quasi-concavity of a

representation, when combined with weak certainty independence it implies that the subtracted

function

(:) is convex not just quasi-convex.

Theorem 2 is written as a representation result for %u , but, of course, we can obtain a representation over the underlying preferences % over acts, by setting V (f ) := W (U

f ). The theorem

tells us that any preference relation on nite-state acts that admits a (dual) representation of the

form of expression (1) { that is, any variational preference | also admits a (primal) representation

of the form of expression (2). Whereas MMR's representation allows us to characterize variational

preferences by a pair (U; c), this representation requires a triple (U; ; ). Notice that, in this

representation, the mean utility

associated with an act f is equal to the utility of the `mean'

P

constant act; i.e., the act that yields s s f (s) in every state.

Some examples of primal and dual representations of variational preferences are given in section

2.4, but rst let us focus on interpretation.

2.2

Interpretations and geometry.

To help understand this representation, consider gure 2 which is drawn for the case where preferences are smooth. Let f be an act with certainty equivalent xf , and let U ( ) be a expected-utility

representation for the constant acts. The primal representation sets V (f ) = U (xf ). Thus, in the

picture, the state-utility vector U

The probability vector

f is indi erent to the constant state-utility vector U (xf ) e.

is chosen to be normal to a tangent hyperplane of this indi erence

curve at U (xf ) e. Since preferences are smooth in this example, this choice is unique, and

10

is

equal to the normalized gradient at U (xf ) e. To see the decomposition in the representation, let

:=

(U

f ). Thus, in the picture, the point

every state gives the mean of U

e is the constant state-utility vector that, in

f according to the probability ; and

=

V (f ) is just the

di erence between this mean utility and the utility of the certainty equivalent.

Mean-dispersion representation

utility in

state 2

0

45 degree line

("constant-utility line")

Uof

U(xf )e

d2

µe

d1

π

µ

ρ

utility in state 1

Figure 2: Illustration of Absolute Ambiguity Premium

We can view the

as a measure of the agent's dislike of dispersed state utilities: it is the

premium (measured in utility) that the agent would be willing to pay to eliminate dispersion of

state utilities. The vector d on which

depends is given by U f

e. By translation invariance,

another act g that induces a state-utility vector with a di erent mean but the same vector d of

di erences from that mean, will have the same `ambiguity premium' . In this sense, the agent

can be thought of as having \constant ambiguity aversion".

In the construction above, we chose

to be normal to the supporting hyperplanes of the upper

contour sets on the constant-utility line. More generally, the representation in theorem 2 requires

11

such a

to be chosen. (This follows from the restriction that

preferences are \smooth", the choice of

0 and

(0) = 0.) Thus, if

in the representation is unique; in fact, smoothness

around the constant-utility line is enough. In this case, the representation is unique up to the

choice of the a ne utility function U ( ). But not all variational preferences are smooth around

the constant-utility line. For example, in the case of multiple prior preferences, any

from the

multiple-prior set admits a representation in this form of expression (2). In this case, the mean

and the dispersion term

(and hence the ambiguity premium) associated with any act will depend

on the choice of . Nevertheless, loosely speaking, the set of ambiguity premia associated with an

act (one for each ) are still independent of the set of mean utilities (one for each ).11

Some readers may be uncomfortable identifying constant ambiguity aversion with a constant

ambiguity premium, especially in cases (like multiple priors) where the premium depends on the

choice of probability vector

in the representation. Therefore, consider an alternative notion.

In the analysis of risk, an alternate de nition of non-increasing absolute risk aversion is (abusing

our notation): for all

~ and degenerate random variables x, if

in (0; 1), all random variables X

~ is weakly preferred to the degenerate random variable x then for

the random variable x + X

any

~ is weakly preferred to the improved

> 0, the `improved' random variable (x + ) + X

degenerate random variable x + . That is, the set of acceptable bets from any given wealth level

is no larger than is the case for a larger wealth level. Non-decreasing absolute risk aversion can

be de ned similarly.

Translating this into the language of acts, we obtain:

De nition 4 (NiAAA and NdAAA) We say that the agent exhibits non-increasing absolute

ambiguity aversion (NiAAA) if, for any act f in F , any

2 (0; 1), and any pair of constant acts

x and y, such that y % x,

f + (1

) x % x ) f + (1

11

) y % x + (1

) y.

(4)

More formally, x a utility representation u on the constant acts. Each vector that admits a representation

of the form of expression (2) maps each act f to a vector ( ; d) where where :=

u f and d := u f

e.

Consider another act g and suppose that, for each admissible vector , the associated vector is ( 0 ; d0 ) . Given

variational preferences, if for each admissible , we have ( 0 ; d0 ) = ( + ; d) for some 2 R, then the set of

ambiguity premia associated with f is equal to the set of premia associated with g.

12

We say the agent exhibits non-decreasing absolute ambiguity aversion (N dAAA) if expression (4)

holds for any act f in F , any

2 (0; 1), and any pair of constant acts x and y, such that x % y.

And we say the agent exhibits constant absolute ambiguity aversion. (CAAA) if it exhibits both

NiAAA and NdAAA.

In expression (4), if the old act f +(1

new act f + (1

) x is weakly preferred to the old constant act x then the

) y (improved by substituting y for x with weight (1

to the new constant act x + (1

)) is weakly preferred

) y (improved by substituting y for x with weight (1

)).

The following proposition con rms our intuition that MMR's axiom A.2 implies constant

absolute ambiguity aversion.

Proposition 3 (A2 and CAAA) Given A.1 (weak order), A.3 (continuity), A.4 (monotonicity) and A.6 (unboundedness), the preferences % satisfy A.2 (weak certainty independence) if and

only if they exhibit CAAA and satisfy independence on the constant acts.

To summarize: theorem 2 tells us that variational preferences have an alternate `primal' representation. This representation decomposes the value of an act into a mean utility and a dispersion

term that only depends on di erences from that mean. We can think of this di erence term as an

(absolute) ambiguity premium, the amount that the agent would pay to eliminate all ambiguity.

MMR's key axiom, weak certainty independence, is equivalent to assuming that this premium is

independent of the mean utility or that the agent exhibits constant absolute ambiguity aversion.

Section 3 extends the variational preference model to allow the ambiguity premium (and ambiguity

aversion) to vary.

2.3

Geometry of the dual representation.

As an aside, we can also use a similar picture to illustrate the construction of MMR's dual

representation of the same preferences. MMR's representation decomposes V (f ) into a mean

utility according to a probability vector p and a term c (p). Again, let f be an act with certainty

equivalent xf , and let U ( ) be a expected utility representation for the constant acts. Again, the

representation will set V (f ) = U (xf ). Thus, in gure 3, the state-utility vector U

13

f is again

indi erent to the constant state-utility vector U (xf ) e. The probability vector p is again chosen

to be normal to a tangent hyperplane of this indi erence set but this time the tangency is at U f

instead of at U (xf ) e. Since preferences are smooth in this example, this choice is unique, and p

is equal to the normalized gradient at U

f . Notice that p, unlike , varies with the act f . To

see the decomposition in the dual representation, let

:= p (U

f ). Thus, in the picture, the

point e is the constant state-utility vector that, in every state, gives the mean of U f according

to the probability p. And, as also shown, c (p) = V (f )

is the di erence between the utility of

the certainty equivalent and the mean utility according to p.

MMR's variational representation

utility in

state 2

0

p

45 degree line

("constant-utility line")

Uof

υe

υ

U(xf )e

c(p)

utility in state 1

Figure 3: Illustration of MMR's Dual Representation

In the dual interpretation, a malevolent nature chooses p to minimize the agent's utility after

the agent's choice of the act f (and hence of the state-utility vector U

f ). The quantity c (p)

is then the amount that nature must pay back to the agent. The agent gets her expected utility

according to p plus this payback. In our smooth case, for any p0 we can nd c (p0 ) as follows. First,

as is illustrated in gure 4, we nd a state-utility vector u0 indi erent to U f such that the normal

14

hyperplane of p0 supports the upper contour set at u0 . We can then compute c (p0 ) = V (f ) p0 u0 .

In gure 4, if nature chooses p0 6= p, then (as shown) the increase in the payback, c (p0 )

is greater than the reduction in the expected utilities, (p

p0 ) (U

c (p),

f ). In this discussion, the

construction of the payback function c (:) was for the particular indi erence set containing the

chosen state utility vector U f . Translation invariance ensures that, if we started from an act in

a di erent indi erence set, the payback function c (:) so generated would be the same.

utility in

state 2

p'

u'

0

p

45 degree line

("constant-utility line")

Uof

υe

(p-p')·(Uof)

U(xf )e

c(p')-c(p)

υ

c(p)

utility in state 1

Figure 4: Malevolent nature's minimization problem.

2.4

Examples

Theorem 2 tells us that any preference relation that admits a representation of the form of expresP

sion (1), minp2 (S) s ps U (f (s)) + c (p), also admits a representation of the form of expression

P

(2),

(d) where

=

. In this section we present

s s U (f (s)) and ds = U (f (s))

well-known examples of preferences that we are used to seeing represented in the dual form, and

show their primal representation. And we present well-known examples of preferences that we are

15

used to seeing represented in their primal form, and show their dual representation. A list of the

examples is given in table 1.

Subjective Expected Utility. The natural benchmark is the subjective expected utility model

P

(SEU), s s U (f (s)). Such preferences can be expressed in the form of expression (1) by setting

c (p) = 1 for any p 6= . They can be expressed in the form of expression (2) by setting (d)

0.

Multiple Priors. The standard Gilboa-Schmeidler (1989) representation for multiple-prior prefP

erences is minp2D s ps U (f (s)) where D is a convex, compact set of probability vectors on S.

MMR (2006) show that this can be expressed in the form of expression (1) by setting c (p) = 0 for

any p in D, and c (p) = 1 otherwise. In appendix B, we show that the same preferences can be

expressed in the form of expression (2) by choosing a

from the multiple-prior set (i.e.,

2 D),

and setting

(d) = maxp2D

P

s

ps d s .

Going in the other direction, one might ask which preferences that can be expressed in the

form of expression (2) also have multiple-prior representations? The answer is a corollary of results

in Safra & Segal (1998), Chambers & Quiggin (1998), and Quiggin & Chambers (2004): if the

dispersion function

(:) is linearly homogenous and convex and the induced preferences %u over

state utility vectors are monotone then the preferences have a multiple-prior representation.

Multiplier Preferences. Hansen & Sargent (2001) introduced this class of variational preferences in the context of robust control. Their standard representation is in the form of expression

(1) with c (p) := R (pj ) where

> 0 and R (pj ) is the relative entropy of the probability p

P

with respect to ; that is, R (pj ) = s ps log (ps = s ) if p

, and 1 otherwise. Maccheroni,

Marinacci and Rustichini (2006b) show that these preferences have a primal representation which

P

can be written as12

ln [ s s exp ( U (f (s)) = )]. But (see appendix B) we can easily convert

this into a representation in the form of expression (2) where

12 See also Dupuis & Ellis (1997, Prop 1.4.2, pp.33-4). We thank Massimo Marinacci for sending helpful notes

on this paper.

16

(d) := ln

hX

s

s

i

exp ( ds = ) .

(5)

Monotone Mean-Variance Preferences. The standard representation of mean-variance preferences appear to take the form of expression (2) with

(d) :=

1 X

s

2

2

s ds .

But mean-variance preferences are not monotone. Nevertheless, MMR (theorem 24, p. 1474-5)

show that, if we restrict the domain of the preferences to the convex set on which monotonicity

holds, then these monotone mean-variance preferences can equivalently be written in the form

of expression (1) with c (p) := G (pj ) =2 where G (pj ) is the Gini concentration index of the

2

P

, and

probability p with respect to the probability ; that is, G (pj ) := s pss 1

s if p

1 otherwise.

Mean-Standard Deviation Preferences. The standard representation of these preferences

take the form of

(d) :=

for some

2

= 1+

X

s

2

s ds

1

2

.

> 0. Grant & Kajii (2007) show these preferences are monotone provided

2

3.1

>

for all s in S. They also show that these preferences have a representation in the

form of expression (1) { in fact, a multiple-prior representation where D := fp : G (pj )

3

s

2

g.

Mean-Dispersion Preferences

The Axioms

The remainder of the paper is concerned with the more general weakly separable, mean-dispersion

preferences of expression (3). In moving in this direction, we will weaken several of MMR's axioms.

The key change, however, is to further weaken their weak certainty independence axiom (A.2.) so

that it only applies when two acts have a \common mean". To do this, we need to have a notion

of a \mean" that can be derived directly from the underlying preferences over acts.

17

De nition 5 (Mean) Fix an act f . A constant act, denoted by m (f ) in X, is de ned to be a

mean of f if there exists an act g and

m (f ); and (ii) f + (1

2 (0; 1], such that (i) for all s in S, f (s)+(1

) g % f + (1

) g for all

2 [0; 1]. Let M (f )

) g (s)

X denote the set of

means of f .

In words, for a constant act to be deemed a mean of the act f , there must exist another act g

and a weight

such that the act f + (1

) g yields in every state a lottery that is indi erent

to that constant act. Moreover, no other convex combination of f and g can be strictly preferred

to f + (1

) g. That is, f + (1

) g is a preference maximum among the set of mixtures of

f and g. Figure 5 illustrates this property in terms of the induced preferences over state-utility

vectors.

45 0 degree line

("constant-utility line")

Uof

U(m(f))e = αUof +(1−α)Uog

U og

Figure 5: For the constant vector m (f ) to be a mean of the act f , it follows from the de nition

of a mean, that the indi erence curve in state-utility space through the constant (state-utility)

vector u (m (f )) e must lie above the chord joining the vectors u f and u g.

The axioms below ensure that each act has a mean. But in general, the mean will not be

unique: in fact, x,y 2 M (f ) does not even imply x

y. We will return to these issues in section

3.4.

Once we have de ned a mean, the de nition of a common mean is follows naturally.

18

De nition 6 (Common Mean) Fix a pair of acts f and g. We say f and g have a common

mean if M (f ) \ M (g) is not empty.

We can now state our axioms.

A.1 Weak Order. % is transitive and complete.

A.2

Common-Mean Weak Certainty-Independence. For any pair of acts f; g in F, any pair of

constant acts x; y in X and any

in (0; 1): if f and g share a common mean then

) x % g + (1

f + (1

) x ) f + (1

) y % g + (1

) y.

A.3 Continuity. For any three acts f; g and h in F, the sets f 2 [0; 1] : f + (1

f 2 [0; 1] : h % f + (1

A.4

A.5

) gg are closed.

Indi erence Substitution. For any pair of acts f and g in F, if f (s)

then f

) g % hg and

g (s) for all s 2 S,

g.

Weak Uncertainty Aversion. For any nite set of indi erent acts f1 ; : : : ; fm in F (that

is, f1

fj for all j = 2; : : : ; m) and any constant act x in X, if the convex combination

a1 f1 + : : : + am fm = x then x % f1 .13

A.6 Unboundedness. For any pair of acts f and g in F and any

in X satisfying g

A.7

w + (1

) f and z + (1

)g

2 (0; 1), there exist w and z

f.

Weak Certainty-Monotonicity. For any pair of acts f and g in F, any pair of constant acts

x and y in X, and any

g + (1

in [0; 1), if f + (1

) x % f + (1

) y then g + (1

)x %

) y.

Axioms A.1 and A.3 are standard and identical to MMR's axioms. Axiom A.4 weakens

MMR's A.4 so that it only pertains to indi erence. Thus, A.4 does not imply monotonicity.

Axioms A.5 and A.7 concern convexity and monotonicity, respectively. Since Gilboa &

Schmeidler (1989), a theme in the literature on ambiguity has been to restrict axioms only to

13 Chateauneuf and Tallon (2002, De nition 4, p516) refer to this axiom as `preference for sure \expected" utility

diversi cation.'

19

apply where constant (that is, unambiguous) acts are involved. Axiom A.5 restricts uncertainty

aversion only to apply where the mixture is a constant act. Axiom A.7 restricts monotonicity

only to apply when mixing with better or worse constant acts.

To compare axiom A.5 with standard axioms, rst consider the following axiom:

A.50 Uncertainty Aversion. For any nite set of indi erent acts f1 ; : : : ; fm in F (that is, f1

fj

for all j = 2; : : : ; m), any convex combination a1 f1 + : : : + am fm % f1 .

Clearly axiom A.50 is stronger than A.5 , since it omits the quali er that the mixed act need be

constant. But lemma 22 in the appendix shows that, given weak order and continuity, axiom A.50

and MMR's axiom A.5 are equivalent. The intuition behind the standard uncertainty aversion

axioms is that mixing indi erent acts provides a hedge against subjective uncertainty. The new

axiom only requires this mixing to be preferred if it provides a `perfect hedge'; that is, if all

subjective uncertainty is removed. It does not require all partial hedges to be preferred.14

Thus, axiom A.5 does not require the induced preferences in state-utility space to be convex.

Nevertheless, we show in section 4.2 that this weak uncertainty aversion axiom is just enough

to ensure that our mean-dispersion preferences are `weakly ambiguity averse' in the sense of

Ghirardato et al (2004). And in section 4.5, we argue that the standard uncertainty aversion

axiom A.5 may be too strong in that it imposes more than just an aversion to variation across

states.

To compare axiom A.7 with the standard axioms, rst notice that, like MMR's axiom A.2,

it involves mixing general acts with constant acts. Roughly, MMR's axiom A.2 says that the

preference between two general acts f and g in such mixtures is maintained as we substitute

constant act x with constant act y. Axiom A.7 says that the preferences between two constant

acts x and y in such mixtures is maintained as we substitute act f for act g. If we add MMR's

axiom A.4. to A.2 then we induce preferences over state-utility vectors that satisfy the following

monotonicity property: if u0

u00 then u0

u

u00 . If we add axiom A.4 to A.7 , then we induce

preferences over state-utility vectors that satisfy the following much weaker monotonicity property:

14 This is somewhat analogous to Yaari's notion of weak risk aversion: the expectation of a lottery is weakly

preferred to the lottery itself, but the agent is not averse to all mean-preserving spreads.

20

if u0 = u00 + ce where c > 0 then u0

u

u00 . In section 4.1, we provide examples of preferences that

seem natural (or at least interpretable) but which only satisfy this weaker monotonicity.

As discussed already, axiom A.2 weakens MMR's certainty independence axiom A.2 so that

it only applies when the underlying acts f and g have a common mean. Recall from proposition

3 that MMR's axiom A.2 forces preferences to have constant ambiguity aversion as we change

mean utility. Our weaker axiom A.2 removes precisely this implication: that is, (see corollary 6

below) strengthening A.2 to A.2 is exactly equivalent to imposing constant ambiguity aversion.

An analogy may be useful here. Gilboa-Schmeidler weakened Anscombe-Aumann's independence

axiom to certainty independence to retain the original axiom's intuitive appeal while shedding it

of its unwanted implication that the agent should be indi erent to hedging. We weaken MMR's

weak certainty independence axiom to retain the original axiom's intuitive appeal while shedding

it of its unwanted implication that the agent should have constant ambiguity aversion. We will

discuss the geometry of this claim in section 3.3 below.

3.2

The main theorem

We can now state our main result. Recall that H 0 is the hyperplane though the constant stateutility vector 0 with normal vector .

Theorem 4 (Main Theorem) Suppose that the preferences % on F that satisfy A.1 (weak order), A.2 (weak common-mean certainty independence), A.3 (continuity), A4 (indi erence substitution), A5 (weak uncertainty aversion), A.6 (unboundedness), and A.7 (weak certaintymonotonicity). Then there exist an unbounded a ne utility function U : X ! R, a vector of

P

weights 2 Rn such that s = 1, a continuous function : H 0 ! R+ with (0) = 0, and a

continuous function ' : R

H 0 ! R increasing in the rst argument and decreasing in the

second with ' (y; 0) = y for all y in R, such that the preferences are represented by

V (f ) = ' ( ; (d))

where

2 R is the `mean' given by

by d := U

f

:=

(U

f ), and d 2 H 0 is the vector of `di erences' given

e.

21

In this representation, the parameter

utility function U ( ) and the weights

represents the \mean utility" of the act f using the

. The vector (d1 ; : : : ; dn ) is a vector of state-by-state

di erences from that mean utility. We can think of the function

representation is weakly separable in the mean

decreasing in the latter. The normalization

The normalization ' ( ; 0) =

as a measure of dispersion. The

and dispersion , increasing in the former and

(0) = 0 ensures that dispersion is always disliked.

is inessential but ensures that the value of a constant act x is equal

to the utility of that act, V (x) = U (x), and hence that the value of a general act f is equal to

the utility of its certainty equivalent, V (f ) = U (xf ).

The theorem above suggests the following de nition.

De nition 7 (Mean-Dispersion Preferences) We say that preferences are mean-dispersion

preferences if they admit a representation in the form given in Theorem 4. We will refer to the

representation ('; ; U; ) as a mean-dispersion representation.

Notice that theorem 4 is not a full characterization of mean-dispersion preferences. In particular, the theorem does not say that all preferences de ned by such a V (:) satisfy all the axioms.

Notice also that theorem 4 does not contain a uniqueness claim. We will return to both these

issues in section 3.4 below. But rst, let us relate the mean-dispersion representation back to our

discussion of variational preferences, in particular in the context of the induced preferences %u

over state-utilities.

3.3

Interpretation and Geometry

Recall that, for a given utility function U and weights

:=

(U

f ) and the di erence vector d := U

f

, an act f induces the mean-utility

e. Furthermore, we can think of the

absolute uncertainty premium associated with the act f as the di erence

U (xf ) between the

mean utility and the utility of the certainty equivalent. For variational preferences, this premium

was just given by the measure of dispersion

and was independent of the mean utility . With

general mean-dispersion preferences, the premium is given by ' ( ; 0)

premium depends not just on the measure of dispersion

the mean utility .

22

' ( ; (d)). Thus, the

but also on ' which in turn depends on

Figure 6 illustrates how the key axiom, common-mean certainty independence, allows ambiguity premia to vary. It is drawn for the case where preferences are smooth and monotonic. As

usual, let U be an expected-utility representation for the constant acts. Let f and g be a pair of

acts with common mean x. In state-utility space, what this means is that U

f and U

g must

both lie in a supporting hyperplane of the (weak) upper contour set of the induced preferences %u

through e, where

= U (x) (see lemma 29 in the appendix for details). In this example, since

preferences are smooth, the supporting hyperplane is unique. Let

denote its normal vector.

αUof +(1−α)U(y)e

Uo f

0

45 degree line

("constant-utility line")

U(y)e

µ'e

µe

αUof +(1−α)U(x)e

αUog +(1−α)U(y)e

V(αf +(1−α)x)e

αUog +(1−α)U(x)e

µ − ϕ(µ,ρ(δ))

µ'− ϕ(µ',ρ(δ))

π

Uog

Figure 6: Illustration of (weakly-separable) mean-dispersion preferences with non-constant absolute ambiguity premium.

Now suppose f + (1

the utility vectors U f +(1

) x is indi erent to g + (1

) x. In the picture, this corresponds to

) U (x) e and U g+(1

) U (x) e lying on the same indi erence

23

curve. By construction, these two utility vectors also lie on the hyperplane with normal vector

through e. Thus each of these two state-utility vectors has the same mean with respect to .

Their certainty equivalent is given by the vector V ( f + (1

) x) e.

Next consider some other constant act y and the two new acts f +(1

) y and g+(1

) y.

Since f and g have a common mean, we can apply axiom A.2 . Hence the the state-utility

vectors

U

f + (1

) U (y) e and

U

g + (1

) U (y) e must lie on the same indi erence

curve. Again by construction the two new state-utility vectors

U

g + (1

U

f + (1

) U (y) e have the same mean with respect to ; in this case

0

) U (y) e and

. In fact, each of

these two new indi erent vectors is obtained from the two old indi erent vectors by the common

translation (1

) (U (y)

U (x)) e (that is, a translation parallel to the constant-utility line).

More generally, lemma 30 in the appendix shows that axiom A.2 implies the following weaker

translation invariance property of the induced preferences that applies only for pairs of state-utility

vectors that share a common mean with respect to .

De nition 8 (Common-Mean Translation Invariance.) Suppose H is a supporting hyperplane of the uppercontour set of %u through e. Then for any pair of utility vectors u0 and u00 in

H , and any

2 R, u0 %u u00 if and only if u0 + e %u u00 + e.

This is weaker than the translation invariance property implied by MMR's axiom A.2. In particular there is no requirement that, if we apply the same common translation (1

to the entire indi erence curve through V ( f + (1

) (U (y)

U (x)) e

) x) e, then all points in the new translated

curve will be indi erent. The reason is that not all the points on the original indi erence curve

had the same mean. In our picture, the actual indi erence curve through U f + (1

) U (y) e

is less bowed toward the origin.

Now consider ambiguity premia. The mean of the rst two vectors was

= ' ( ; 0). Since

they had the same mean and were indi erent, they must have the same dispersion term : that

is, the utility of their certainty equivalent is V ( f + (1

) x) = V ( g + (1

Thus the ambiguity premium associated with the rst two vectors is just

of the second two vectors was

0

) x) = ' ( ; ).

' ( ; ). The mean

. By construction, they had the same vector of di erences from

this mean as the rst two vectors, hence their dispersion term was also . Thus, the utility of

24

their certainty equivalent V ( f + (1

premium is just

0

) y) = V ( g + (1

) y) = ' ( 0 ; ), and their ambiguity

' ( 0 ; ). But, as shown, these premia need not be the same: in the illustrated

case, the ambiguity premium decreased as we increased the mean utility holding the dispersions

xed.

More generally, we can ask under what condition do mean-dispersion preferences exhibit both

non-increasing ambiguity premia as de ned by ' ( ; 0)

' ( ; (d)), and non-increasing absolute

ambiguity aversion (NiAAA) as de ned in section 2. The following proposition provides the

answer.

Proposition 5 (NiAAA) Suppose that the preferences % admit the mean-dispersion representation ('; ; U; ). Then the following three properties are equivalent:

(a) the preferences % exhibit NiAAA

(b) the ambiguity premium, ' ( ; 0) ' ( ; ), is decreasing in

for all

(c) ' ( + ; )

2

'( ; ) +

for all

2 R, all

0, and all

2 R and all

2

H0 ;

H0 .

The following corollary tells us (as the pictures suggest) that mean-dispersion preferences

satisfy MMR's stronger independence axiom A.2 if and only if ambiguity premia are constant.

Corollary 6 Suppose that the preferences % admit the mean-dispersion representation ('; ; U; ).

Then the following are equivalent: (i) preferences satisfy MMR's axiom A.2 (weak certainty independence); (ii) preferences exhibit CAAA; and (iii) ' =

.

One set of examples of mean-dispersion preferences that allow for varying premia are those

that correspond to Epstein's (1985) generalized mean-variance preferences (translated from risk

to uncertainty). But those preferences also violate monotonicity. The following is an example of

mean-dispersion preferences that exhibit decreasing absolute ambiguity aversion but are monotone.

Example 1 (Generalized Multiplier Preferences) Consider the mean-dispersion representation ('; ; U; ) where U is an unbounded a ne utility function;

is a probability; (d) :=

P

ln ( s s exp ( ds = )) (which is weakly greater than zero by Jensen's inequality); and '( ; ) :=

25

( )

lim

where

!(+1)

: R ! R is a di erentiable function with

0

< 0, lim

!( 1)

( ) = 1 and

( ) = 0.

This example may be viewed as a generalization Hansen-Sargent multiplier preferences; indeed

the dispersion function

ences have

( )

takes the same form as expression (5) in section 2.4. Multiplier prefer-

1. Multiplier preferences are additively separable (in fact, quasi-linear) in

and , and have constant ambiguity aversion. The preferences in this example are only weakly

separable since

since the weight

3.4

appears in the term

( ). These preferences have decreasing ambiguity aversion

put on the dispersion is decreasing in .15

Converse theorems, smoothness and uniqueness.

We now consider converses to our main result, theorem 4. We shall show that any preferences

that have a mean-dispersion representation satisfy all our axioms except A.2 (weak commonmean certainty independence). To see why axiom A.2 causes a problem, consider the following

example.

Example 2 (Failure of A.2 ) Let S = fs1 ; s2 g. Let U be an unbounded a ne utility function;

and let

:= (1=2; 1=2). Consider the mean-dispersion preferences ('; ; U; ) where

is given by

one-third of the mean absolute variation, i.e., (d1 ; d2 ) = 31 [(jd1 j + jd2 j) =2]; and ' is given by

8

3

if

0

<

3

3

if 0 <

3 =2 .

' ( ; ) :=

:

if > 3 =2

This is an example of mean-dispersion preferences that are not fully separable in

and . The

example is illustrated in gure 7 in which indi erence sets for the induced preferences %u over

0

R2+ are Leontief in the half-space below the line below the line H(1=2;1=2)

, and constant slope

(1=2) (respectively,

0

2) in the half-space above the line H(1=2;1=2)

in which the utility in state

1 is greater than (respectively, less than) the utility in state 2.

Now consider the probability ^ := (2=3; 1=3). We will show a violation of equal-mean translation invariance with respect to ^ ; that is, axiom A.2 will not apply. Notice that ^ di ers from

the

15

used to de ne the preferences above, but, nevertheless, for any

Since

2 R, the hyperplane H ^

( ) < 1 for all , it follows that the preferences in this example are montonic.

26

is a supporting hyperplane of the uppercontour set of the induced preferences %u through

e.

Therefore, if x is the constant act such that U (x) = , then x satis es the de nition of a mean

for any act f such that U

( 1; 2) and U

f lies in the hyperplane H ^ . Let f and g be acts such that U

g =( 2; 1) (hence U

g =U

f

e). Let x and y be constant acts such that

U x =(0; 0) and U y =( 1; 1) (hence U y = U x

acts are mapped to utility vectors in H ^0 . But, y

[ 1]

utility vectors in H ^

f =

e). By construction f

x and both these

g even though both these acts are mapped to

. That is, common-mean translation invariance fails for acts that have a

common mean with respect to ^ . Since common-mean translation invariance is implied by axiom

A2 , this is a violation of the axiom.

constant-utility line

(-1,2)

(-2,1)

(0,0)

(-1,-1)

Hπ0

H^0

π

Figure 7: Indi erence Map for induced preferences %u corresponding to Example 2.

This example relies on two facts. First, the preferences are not `smooth'. Second, the weights

^ = (2=3; 1=3) used to construct the common mean di er from the weights

= (1=2; 1=2) that are

part of the representation ('; ; U; ). If we restrict attention to acts that have a common mean

27

`with respect to

= (1=2; 1=2)' then translation invariance holds. This motivates the following

de nition.

De nition 9 (Common mean with respect to ) Given an a ne utility function U : X !

P

R and a vector of weights 2 Rn such that s = 1, we say that two acts f; g 2 F have a

common mean with respect to

if

(U

f) =

(U

g).

The idea of example 2 generalizes to give us a partial converse to the main theorem.

Theorem 7 (Partial Converse) Suppose that the preferences % admit the mean-dispersion representation ('; ; U; ). Then the preferences % satisfy the axioms of the main theorem (theorem

4) except axiom A.2 (weak common-mean certainty independence); but the preferences do satisfy

weak certainty independence restricted to pairs of acts f ,g in F that share a common mean with

respect to .

We can obtain a more complete converse theorem by assuming that preferences are `smooth'.

In fact, we only need preferences to be `smooth' around constant acts; and we only need a very

weak notion of `smoothness'.

De nition 10 (Weak smoothness) We say that the mean-dispersion preferences ('; ; U; )

are weakly smooth (with respect to

(U

) at the constant act x if, for all acts f such that

f ) > U (x) there exists a t 2 (0; 1] such that ' (t + (1

as usual, d := U

f

:=

t) U (x) ; (td)) > U (x) (where,

e).

This is equivalent to saying that the induced preferences %u over state-utility vectors have the

property that, for all u0 2 Rn , if

u0 >

then there exists a t 2 (0; 1] such that tu0 +(1

t) e

u

e. This is a very weak smoothness property. In particular, lemma 35 in the appendix shows that

if

is di erentiable at 0 and the function ' is di erentiable at ( ; 0) for all

2 R then the

associated mean dispersion preferences are weakly smooth.

To ensure that mean-dispersion preferences are weakly smooth, we introduce the following

axiom that puts some natural structure on the shape of equal mean sets.

28

A.8* (Convex Equal-Mean Sets) For any pair of acts f and g and any constant act x, if

x 2 M (f ) \ M (g) then x 2 M ( f + (1

) g) for all

2 [0; 1].

In words, this axiom says that if the constant act x is a mean for both the act f and the act g,

then it should also be the mean for any act formed by taking a convex combination of those two

acts.

This axiom allows for a full characterization of weakly smooth mean-dispersion preferences.

Theorem 8 (Weakly smooth preferences) The preferences % on F satisfy the axioms of the

main theorem (theorem 4) plus axiom A.8 (convex equal-mean sets) if and only if there exists

a mean-dispersion representation ('; ; U; ) such that the preferences are weakly smooth (with

respect to this

0

6=

) at all constant acts. Moreover, in this case,

is unique: that is, there is no

for which % admits a mean dispersion representation.

We turn now to consider the issue of uniqueness beyond the case of smooth preferences. Since

mean-dispersion representations ('; ; U; ) have four components, there are several possible issues

of uniqueness. Most of these, however, are relatively mundane. Once we x a

admit a mean-dispersion representation, the normalization ' ( ; 0) =

And similarly, once we

x

; U and ', then the choice of

and U no cardinal restriction can be put on either

; U and

that

ensures that ' is unique.

is unique. But, if we only

x

or ' individually. That is, suppose that

('; ; U; ) de nes a mean-dispersion representation of the given preferences. Let ^ := t ( ) for

any continuous and increasing function t :

H 0 ! R with t (0) = 0. And let '

^ be de ned

by '

^ ( ; t (y)) = ' ( ; y). Then (^

'; ^; U; ) de nes another mean-dispersion representation for the

same preferences. This is a standard feature of representations that are only weakly separable:

changes in the \aggregator" and the \macro" function can be chosen to cancel each other out.

If we only x a

that admits a mean-dispersion representation, then we are of course still free

to choose U up to any positive a ne transformation. For example, suppose ('; ; U; ) de nes a

^ = aU +b for any a > 0 and any b in

mean-dispersion representation of the given preferences. Let U

R. Then, for example, let ^ be de ned by ^ (ad) := (d). And let '

^ be de ned by '

^ (a + b; y)

a' ( ; y) + b for all y in

^;

^ ; ^; U

H 0 . Then '

de nes another mean-dispersion representation

29

for the same preferences. (By the remarks in the previous paragraph, this choice of ^ and '

^ are

not unique.)

The more interesting issue concerns non-uniqueness of the weighting vector . Consider the

case where preferences % admit two mean-dispersion representations ('; ; U; ) and ('0 ; 0 ; U;

where

6=

0

0

)

. In this case, theorem 8 immediately implies that the induced preferences %u are

not `smooth around the constant-utility line', and that the preferences % must satisfy our axiom

A.2 restricted to pairs of acts that have a common mean with respect either to

or to

0

. But, in

fact, we get much more. We get full translation invariance; that is, the preferences satisfy MMR's

A.2.

Theorem 9 (Non-unique

implies CAAA) Suppose that the preferences % admit the two

mean-dispersion representations ('; ; U; ) and ('0 ; 0 ; U;

0

) where

0

6=

. Then the preferences

% satisfy A.2 (weak certainty independence) and hence CAAA.

The following uniqueness condition follows immediately.

Corollary 10 Suppose that the preferences % admit the mean-dispersion representation ('; ; U; ).

If % does not satisfy MMR's axiom A.2 then

is unique: that is, there is no

0

6=

for which %

admits a mean dispersion representation.

The proof of theorem 9 appears in the appendix. But the idea is this: if there are two weighting

vectors

and

0

,

6=

0

then we can nd a utility vector u1 such that

loss of generality suppose 0 is the constant vector such that 0

u

0

00

u1 <

u1 . Without

u1 . We construct a sequence of

points u1 ; u2 ; : : : converging to 0 such that for each j, uj and uj+1 are indi erent and either share

a mean with respect to

and transitivity, 0 + e

or with respect to

u

00

. Thus, by common-mean translation invariance

u1 + e for all ; that is, translation invariance applies to u1 and its

certainty equivalent. Finally, we show that all utility vectors in Rn can be approximated by points

like u1 .

One might think that any induced preferences %u on state-utility vectors that have a kink

at 0 can admit two mean-dispersion representations ('; ; U; ) and ('0 ; 0 ; U;

0

) where

6=

0

and hence that any kink at zero would induce preferences that satisfy CAAA. This conjecture,

30

however, is false. Recall the preferences in example 2. For these mean-dispersion preferences, there

is kink at 0 (indeed there is a kink at all points on the certainty line), but all mean dispersion

representations have the same

= (1=2; 1=2). Indeed, since these preferences do not satisfy

MMR's axiom A.2, theorem 9 shows that no other

0

6=

can form part of a mean-dispersion

representation for these preferences.

4

Properties and examples of mean-dispersion preferences.

In this section, we consider properties of mean-dispersion preferences beyond the fact that they

need not have constant ambiguity aversion. On the way, we show that mean-dispersion preferences

encompass many important families of preferences with each corresponding to a particular attitude

toward means and dispersion captured by particular forms of the functions ' and .

4.1

Monotonicity

Since theorems 4 and 7 do not require MMR's axiom A.4., we do not need to restrict meandispersion preferences to be monotonic. The obvious example of mean-dispersion preferences that

violate monotonicity is the mean-variance model.

Mean-Variance Preferences Mean-variance preferences are those mean-dispersion preferences

('; ; U; ) that satisfy CAAA (hence '( ; ) :=

P

1

2

> 0:

s s ds for some

2

),

is a probability; and

(d) :=

As MMR showed, these preferences satisfy all their axioms except monotonicity. But these preferences satisfy the weaker monotonicity requirements (axiom A7 ) of the general mean-dispersion

model, as do the more general mean-variance models of Epstein (1985).

A second example is given by the following version of mean-standard-deviation preferences.

For expositional purposes, the example is stated for two states, but it is straightforward to extend

the idea.

Example 3 (Extreme Mean-Standard Deviation) Let S = fs1 ; s2 g. Let U be an unbounded

a ne utility function; let

be a probability vector where (without loss of generality)

31

1

2.

Let

the mean-dispersion preferences given by V (f ) =

where is the mean and

p

deviation of the state utilities (with respect to ); and >

1= 2.

is the standard

Again, these preferences satisfy all the MMR axioms except their monotonicity axiom A.4 (see

appendix B for details) but they satisfy our weaker monotonicity axiom A.7 .

Decision theorists often disregard preferences that violate monotonicity arguing that such

preferences are irrational or uninterpretable. The concern is that, if we allow agents to violate

something as basic as monotonicity, then `anything goes'. We share some of these concerns. But

preferences that violate monotonicity in the sense of A.4 but which satisfy the weaker requirement

of A.7 are not uninterpretable. Such an agent still prefers to be given an extra dollar (or utile)

for sure; that is, she prefers to get the same extra payo in all states. But such an agent has an

extreme aversion to dispersion across states. We can think of her as so uncomfortable living with

uncertainty that she would be willing to accept an uncompensated reduction in her wellbeing in

the good states to reduce that anxiety. In the case of mean-variance preferences, this extreme

anxiety (enough to violate monotonicity) only sets in once the dispersion across states is large.

The preferences in example 3 are more extreme in that violations of monotonicity occur even

where there is no initial dispersion.16

While we can interpret such violations of monotonicity, we still might want to exclude them.

Not surprisingly, imposing MMR's monotonicity axiom achieves this. We might also want to allow

examples like the mean-variance preferences but to exclude examples like the extreme meanstandard deviation preferences that violate monotonicity even around certainty. The following

property of the underlying preferences over acts achieves this.

De nition 11 (Local Monotonicity around Certainty) For any acts f , g in F, and any

constant act x in X: (a) if f (s) % x for all s in S, and f (^

s)

exists

2 (0; 1), such that for all

in S, and x

in 0;

,

f + (1

g (^

s) for some s^ in S, then there exists

)x

x for some s^ in S, then there

x; and (b) if x % g (s) for all s

2 (0; 1), such that for all

in 0;

,

16 More precisely, since the mean-variance preferences are smooth, all uncertainty aversion is second order around

certainty. Mean-standard deviation preferences

exhibit rst-order uncertainty aversion around certainty even when

p

they are monotonic (i.e., even when <

s = (1

s ) for all s). In the extreme case where where monotonicity

fails, it does so at certainty.

32

x

g + (1

) x.

Mean-variance preferences satisfy this local monotonicity property but fails the usual global monotonicity. The preferences in example 3 fail even this local monotonicity property. Local monotonicity around certainty also restricts the weights

s

in a mean-dispersion representation to be

non-negative.17

For completeness, we summarize these in the following simple proposition (which we state

without proof).

Proposition 11 (Monotonicity) Suppose that the preferences % admit the mean-dispersion representation ('; ; U; ). Then

(a) the preferences % satisfy A.4 (monotonicity) if and only if the function W (u0 ) := ' (

u0 ; (u0

that represents %u is monotonic; and

(b) if the preferences % satisfy local monotonicity around certainty then

0.

Hereafter, we will refer to mean-dispersion preferences that satisfy MMR's A.4 as monotone.

4.2

Convexity.

Convexity properties of the underlying preferences are often interpreted as re ecting uncertainty

aversion or the desire to hedge (but see section 4.5). Theorem 4 did not require preferences to be

convex; that is, it did not require MMR's axiom A.5. The weaker requirement, axiom A.5 only

requires the agent to prefer complete hedges that remove all dispersion across states. The weak

uncertainty aversion of axiom A.5 is su cient to ensure the following property due to Ghirardato

& Marinacci (2002).

De nition 12 (Weak Ambiguity Aversion) We say that preferences are weakly ambiguity

averse if there exists an SEU preference relation %SEU such that for all constant acts x and

all acts f , x %SEU f =) x % f and x

SEU

f =) x

17

f.

Example 3 shows that local monotonicity around certainty, while su cient, is not necessary for

0. But

(see appendix B) the same preferences admit another mean-dispersion representation in which non-negativity of

the weights fails.

33

u0 ))

Proposition 12 . Suppose that the preferences % admit the mean-dispersion representation

('; ; U; ) where

0. Then the preferences are weakly ambiguity averse

This weak form of ambiguity aversion is satis ed by several important models. Ghirardato et

al (2004) introduced the family of invariant biseparable preferences where the induced preferences

%u over state-utility vectors has a representation W : Rn ! R that satis es monotonicity and

constant linearity; that is, for all u0 2 Rn ,

2 R, and

> 0; W ( u0 + e) =

W (u0 ) + .

Invariant biseparable preferences are examples of mean-dispersion preferences provided they are

weakly ambiguity averse.

Proposition 13 (Biseparable Preferences) (a) Suppose that the preferences % are invariant

biseparable (and unbounded). Then these preferences admit a mean-dispersion representation if

and only if they are weakly ambiguity averse.

(b) Suppose that the preferences % admit the monotone mean-dispersion representation ('; ; U; ).

Then the preferences are invariant biseparable if and only if they exhibit CAAA (hence ' ( ; ) =

for all

2 R and all

2

H 0 ); and the dispersion function

Notice that proposition 13(b) does not require

( ) is linearly homogenous.

(:) to be convex. If we add convexity of

to the

conditions in part (b), then (as we discussed in section 2.4) we obtain multiple-prior preferences

which, of course, are a special case of variational preferences.

A special case of invariant biseparable preferences is the Choquet expected utility (CEU)

model. The variational preference model can accommodate CEU provided the associated capacity

is convex, in which case the preferences are convex and the model reduces to a special case

of multiple priors. Chatteauneuf and Tallon (2002) study a larger set of CEU preferences which

need not be convex but which still have the nice property that the capacity has a non-empty core.

They show a CEU preference relation satis es A.5 (weak uncertainty aversion) if and only if the

core is non-empty.

Proposition 14 (CEU) (a) Suppose that preferences % admit a CEU representation (U; ) (where

U is unbounded). Then these preferences admit a mean-dispersion representation if and only if the

34

core of the capacity

'( ; ) =

is non-empty. The corresponding representation ('; ; U; ) has

R

, and (d) :=

(d) d .

2 core ( ),

(b)Suppose that the preferences % admit the monotone mean-dispersion representation ('; ; U; ).

Then the preferences have a non-empty-core CEU representation (with associated utility index U )

if and only if they exhibit CAAA (hence ' ( ; ) =

and the dispersion function

( d + (1

) d0 ) =

for all

2 R and all

2

H 0 );