6-Aug-10 PRELIMINARY RESULTS Lowest Quintile Second Quintile

advertisement

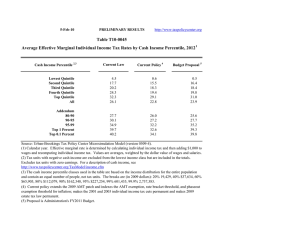

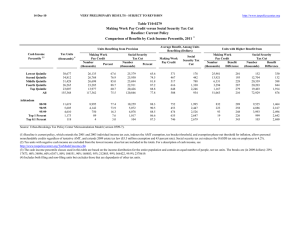

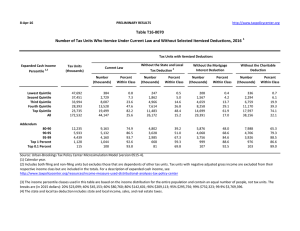

6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T10-0204 Administration Proposal to Extend All 2001-03 Tax Cuts Other than High Income Provisions Distribution of Federal Tax Change by Cash Income Percentile, 2012 1 Summary Table Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate6 Change (% Points) Under the Proposal 24.6 77.9 93.1 98.6 99.1 73.6 0.0 0.0 0.0 0.0 0.3 0.1 0.6 2.3 2.4 3.1 3.0 2.8 1.0 8.0 12.7 22.3 55.9 100.0 -69 -583 -1,016 -2,124 -6,102 -1,616 -0.6 -2.0 -1.9 -2.4 -2.2 -2.1 4.6 10.3 16.4 19.3 26.1 21.4 99.4 99.4 99.3 95.1 82.3 0.0 0.0 0.2 4.4 17.0 3.9 3.8 3.5 1.5 1.1 18.6 12.4 16.1 8.8 2.9 -4,032 -5,508 -8,809 -18,771 -61,510 -2.9 -2.8 -2.6 -1.0 -0.7 21.8 23.0 25.1 31.6 34.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 19.7 Proposal: 4.3 (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,356, 40% $37,493, 60% $65,656, 80% $111,659, 90% $161,739, 95% $226,402, 99% $599,181, 99.9% $2,727,123. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile, 2012 Detail Table Percent of Tax Units 4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent 1 Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 24.6 77.9 93.1 98.6 99.1 73.6 0.0 0.0 0.0 0.0 0.3 0.1 0.6 2.3 2.4 3.1 3.0 2.8 1.0 8.0 12.7 22.3 55.9 100.0 -69 -583 -1,016 -2,124 -6,102 -1,616 -11.5 -16.5 -10.6 -11.0 -7.7 -9.0 0.0 -0.4 -0.2 -0.4 1.0 0.0 0.8 4.0 10.7 17.9 66.5 100.0 -0.6 -2.0 -1.9 -2.4 -2.2 -2.1 4.6 10.3 16.4 19.3 26.1 21.4 99.4 99.4 99.3 95.1 82.3 0.0 0.0 0.2 4.4 17.0 3.9 3.8 3.5 1.5 1.1 18.6 12.4 16.1 8.8 2.9 -4,032 -5,508 -8,809 -18,771 -61,510 -11.8 -10.9 -9.2 -3.2 -2.1 -0.4 -0.2 0.0 1.6 1.0 13.8 10.1 15.8 26.8 13.7 -2.9 -2.8 -2.6 -1.0 -0.7 21.8 23.0 25.1 31.6 34.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile, 2012 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 38,450 34,947 31,868 26,646 23,298 157,348 24.4 22.2 20.3 16.9 14.8 100.0 11,600 28,852 52,224 88,978 280,229 76,169 602 3,545 9,576 19,319 79,171 17,891 10,998 25,307 42,648 69,658 201,058 58,277 5.2 12.3 18.3 21.7 28.3 23.5 3.7 8.4 13.9 19.8 54.5 100.0 4.6 9.6 14.8 20.2 51.1 100.0 0.8 4.4 10.8 18.3 65.5 100.0 11,720 5,734 4,655 1,190 120 7.5 3.6 3.0 0.8 0.1 138,385 196,549 345,574 1,825,188 8,367,274 34,168 50,617 95,612 595,782 2,979,035 104,217 145,932 249,962 1,229,406 5,388,239 24.7 25.8 27.7 32.6 35.6 13.5 9.4 13.4 18.1 8.4 13.3 9.1 12.7 16.0 7.1 14.2 10.3 15.8 25.2 12.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 19.7 Proposal: 4.3 (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,356, 40% $37,493, 60% $65,656, 80% $111,659, 90% $161,739, 95% $226,402, 99% $599,181, 99.9% $2,727,123. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal 6 Average Federal Tax Rate Change (% Points) Under the Proposal 21.2 69.4 88.0 98.3 98.8 73.6 0.0 0.0 0.0 0.0 0.2 0.1 1.1 2.7 2.6 2.9 2.9 2.8 1.5 8.0 12.2 20.6 57.6 100.0 -121 -632 -990 -1,749 -4,894 -1,616 -51.9 -22.2 -12.4 -10.7 -7.4 -9.0 -0.1 -0.5 -0.3 -0.3 1.2 0.0 0.1 2.8 8.5 17.1 71.3 100.0 -1.1 -2.4 -2.1 -2.3 -2.1 -2.1 1.0 8.5 15.1 18.9 25.9 21.4 99.0 99.2 99.1 95.2 83.7 0.0 0.0 0.1 3.9 15.6 3.2 3.5 3.5 1.7 1.2 17.0 12.8 17.7 10.1 3.2 -2,876 -4,328 -7,567 -17,910 -56,785 -10.0 -10.1 -9.4 -3.5 -2.2 -0.2 -0.1 -0.1 1.6 1.0 15.1 11.4 17.0 27.8 14.1 -2.4 -2.6 -2.6 -1.1 -0.8 21.9 23.2 24.9 31.3 34.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Average Federal Tax 6 Rate 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 31,706 32,349 31,237 29,980 29,936 157,348 20.2 20.6 19.9 19.1 19.0 100.0 10,935 26,208 46,322 77,565 235,547 76,169 233 2,849 7,961 16,390 65,872 17,891 10,702 23,359 38,362 61,176 169,676 58,277 2.1 10.9 17.2 21.1 28.0 23.5 2.9 7.1 12.1 19.4 58.8 100.0 3.7 8.2 13.1 20.0 55.4 100.0 0.3 3.3 8.8 17.5 70.1 100.0 15,019 7,540 5,940 1,436 142 9.6 4.8 3.8 0.9 0.1 117,658 167,170 294,212 1,584,726 7,360,192 28,659 43,024 80,705 513,625 2,600,259 88,999 124,146 213,506 1,071,100 4,759,933 24.4 25.7 27.4 32.4 35.3 14.7 10.5 14.6 19.0 8.7 14.6 10.2 13.8 16.8 7.4 15.3 11.5 17.0 26.2 13.2 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 19.7 Proposal: 4.3 (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Single Tax Units Percent of Tax Units 4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 14.5 58.4 88.1 98.1 98.4 64.7 0.0 0.0 0.0 0.0 0.1 0.0 0.3 1.3 1.6 1.7 3.4 2.3 0.6 6.6 11.9 15.7 65.1 100.0 -20 -232 -459 -734 -3,662 -783 -3.3 -9.8 -7.4 -6.0 -8.4 -7.8 0.1 -0.1 0.1 0.4 -0.4 0.0 1.6 5.1 12.6 20.9 59.6 100.0 -0.2 -1.2 -1.3 -1.3 -2.4 -1.8 7.1 10.7 16.9 20.8 26.2 21.2 98.3 98.6 98.7 96.8 83.8 0.0 0.0 0.0 2.5 15.5 2.7 3.4 4.6 3.0 1.5 15.7 13.0 22.6 13.8 2.8 -1,677 -2,955 -6,791 -20,617 -48,319 -7.9 -9.3 -12.0 -5.6 -2.4 0.0 -0.2 -0.7 0.4 0.5 15.5 10.7 14.0 19.5 9.6 -2.0 -2.5 -3.3 -1.9 -0.9 23.3 24.3 24.4 32.6 37.2 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total Number (thousands) Percent of Total 16,972 15,474 14,005 11,543 9,596 68,932 24.6 22.5 20.3 16.8 13.9 100.0 8,380 19,970 34,261 55,833 151,979 43,878 613 2,364 6,243 12,343 43,522 10,087 7,768 17,606 28,019 43,490 108,457 33,791 7.3 11.8 18.2 22.1 28.6 23.0 4.7 10.2 15.9 21.3 48.2 100.0 5.7 11.7 16.9 21.6 44.7 100.0 1.5 5.3 12.6 20.5 60.1 100.0 5,066 2,373 1,795 361 32 7.4 3.4 2.6 0.5 0.1 84,037 119,032 204,548 1,060,631 5,243,107 21,287 31,904 56,631 366,744 2,000,114 62,750 87,128 147,916 693,887 3,242,992 25.3 26.8 27.7 34.6 38.2 14.1 9.3 12.1 12.7 5.5 13.7 8.9 11.4 10.8 4.4 15.5 10.9 14.6 19.0 9.1 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Married Tax Units Filing Jointly Percent of Tax Units 4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 28.1 70.4 83.7 98.4 99.1 83.2 0.0 0.0 0.0 0.0 0.2 0.1 2.2 3.4 3.0 3.4 2.8 3.0 1.2 5.2 9.9 22.2 61.4 100.0 -313 -998 -1,495 -2,551 -5,690 -2,811 -73.2 -27.6 -15.6 -13.1 -7.3 -9.1 -0.1 -0.4 -0.4 -0.7 1.5 0.0 0.0 1.4 5.4 14.8 78.3 100.0 -2.2 -3.0 -2.5 -2.7 -2.0 -2.2 0.8 7.8 13.5 17.8 25.8 22.3 99.3 99.5 99.2 94.9 84.1 0.0 0.0 0.1 4.0 15.2 3.5 3.5 3.3 1.4 1.2 18.8 14.2 18.3 10.1 3.6 -3,654 -5,071 -8,100 -17,174 -60,312 -11.0 -10.4 -8.8 -3.1 -2.2 -0.3 -0.2 0.1 2.0 1.1 15.2 12.3 19.1 31.8 15.9 -2.6 -2.6 -2.4 -1.0 -0.8 21.3 22.8 25.0 30.9 34.0 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total Number (thousands) Percent of Total 6,622 8,956 11,470 15,032 18,609 61,357 10.8 14.6 18.7 24.5 30.3 100.0 14,526 33,405 59,671 95,023 281,842 126,020 428 3,613 9,569 19,486 78,271 30,917 14,098 29,791 50,102 75,537 203,571 95,103 2.9 10.8 16.0 20.5 27.8 24.5 1.2 3.9 8.9 18.5 67.8 100.0 1.6 4.6 9.9 19.5 64.9 100.0 0.2 1.7 5.8 15.4 76.8 100.0 8,860 4,843 3,890 1,015 102 14.4 7.9 6.3 1.7 0.2 138,312 192,091 337,723 1,748,464 7,890,377 33,151 48,821 92,607 557,591 2,743,674 105,160 143,270 245,116 1,190,874 5,146,703 24.0 25.4 27.4 31.9 34.8 15.9 12.0 17.0 23.0 10.5 16.0 11.9 16.3 20.7 9.0 15.5 12.5 19.0 29.8 14.8 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Head of Household Tax Units Percent of Tax Units 4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 29.3 89.3 96.2 99.3 98.9 72.9 0.0 0.0 0.0 0.0 0.1 0.1 1.2 3.7 3.2 2.8 2.2 2.8 5.8 31.8 27.8 19.4 15.2 100.0 -177 -1,015 -1,309 -1,676 -2,930 -976 22.4 -35.7 -14.6 -10.0 -6.2 -14.4 -1.6 -3.2 -0.1 1.4 3.4 0.0 -5.3 9.6 27.5 29.4 38.7 100.0 -1.3 -3.3 -2.6 -2.2 -1.6 -2.3 -7.2 6.0 15.3 19.7 24.9 13.9 99.0 98.5 99.4 95.8 79.3 0.0 0.0 0.2 3.5 20.4 2.5 2.8 2.3 1.2 0.7 7.0 3.1 3.5 1.6 0.4 -2,091 -3,224 -4,819 -11,423 -30,529 -7.5 -8.2 -6.9 -2.5 -1.3 1.1 0.4 0.6 1.3 0.7 14.5 5.8 7.9 10.4 5.0 -1.9 -2.1 -1.7 -0.8 -0.4 22.8 23.2 23.6 31.6 34.8 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total Number (thousands) Percent of Total 7,840 7,497 5,095 2,777 1,242 24,547 31.9 30.5 20.8 11.3 5.1 100.0 13,490 30,617 50,275 76,881 178,521 41,760 -789 2,845 8,985 16,783 47,356 6,781 14,279 27,772 41,290 60,099 131,165 34,979 -5.9 9.3 17.9 21.8 26.5 16.2 10.3 22.4 25.0 20.8 21.6 100.0 13.0 24.3 24.5 19.4 19.0 100.0 -3.7 12.8 27.5 28.0 35.3 100.0 805 232 173 33 3 3.3 0.9 0.7 0.1 0.0 112,763 154,893 278,418 1,423,600 6,950,503 27,789 39,119 70,393 461,226 2,450,721 84,974 115,775 208,025 962,374 4,499,782 24.6 25.3 25.3 32.4 35.3 8.9 3.5 4.7 4.6 2.0 8.0 3.1 4.2 3.7 1.5 13.4 5.5 7.3 9.2 4.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Tax Units with Children Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal 6 Average Federal Tax Rate Change (% Points) Under the Proposal 37.2 94.4 98.2 99.6 99.6 84.9 0.0 0.0 0.0 0.0 0.3 0.1 2.1 4.6 3.9 4.2 2.8 3.4 2.8 12.1 16.5 27.0 41.5 100.0 -336 -1,433 -1,967 -3,372 -6,114 -2,490 34.7 -40.5 -17.0 -14.4 -6.9 -11.0 -0.5 -1.1 -0.7 -0.8 3.1 0.0 -1.3 2.2 9.9 19.8 69.3 100.0 -2.3 -4.1 -3.2 -3.3 -2.0 -2.6 -8.9 6.1 15.4 19.4 27.0 21.1 99.9 99.8 99.4 94.8 81.0 0.0 0.0 0.3 4.7 18.8 3.7 3.8 2.9 1.2 0.8 15.8 10.2 10.7 5.0 1.6 -4,382 -6,298 -8,337 -16,208 -53,265 -11.0 -10.5 -7.3 -2.3 -1.5 0.0 0.1 0.7 2.3 1.2 15.8 10.7 16.8 26.1 12.6 -2.8 -2.8 -2.1 -0.8 -0.5 22.6 23.9 26.6 33.1 35.2 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 2,3 Cash Income Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Average Federal Tax 6 Rate 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total Number (thousands) Percent of Total 10,133 10,359 10,251 9,800 8,315 49,155 20.6 21.1 20.9 19.9 16.9 100.0 14,723 34,672 62,298 103,142 306,063 95,419 -967 3,535 11,567 23,356 88,803 22,663 15,690 31,137 50,731 79,785 217,260 72,756 -6.6 10.2 18.6 22.6 29.0 23.8 3.2 7.7 13.6 21.6 54.3 100.0 4.5 9.0 14.5 21.9 50.5 100.0 -0.9 3.3 10.6 20.6 66.3 100.0 4,398 1,976 1,567 374 36 9.0 4.0 3.2 0.8 0.1 157,496 224,546 400,356 2,088,455 9,839,694 40,023 59,858 114,689 706,818 3,520,731 117,473 164,688 285,667 1,381,637 6,318,963 25.4 26.7 28.7 33.8 35.8 14.8 9.5 13.4 16.7 7.6 14.5 9.1 12.5 14.5 6.4 15.8 10.6 16.1 23.7 11.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 6-Aug-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0204 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Elderly Tax Units Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal 6 Average Federal Tax Rate Change (% Points) Under the Proposal 4.6 29.6 56.6 95.2 97.6 54.9 0.0 0.0 0.0 0.0 0.3 0.1 0.2 0.7 1.3 2.1 3.9 2.8 0.2 2.3 5.5 13.4 78.5 100.0 -21 -146 -486 -1,282 -7,319 -1,716 -7.3 -14.7 -17.1 -14.2 -10.6 -11.3 0.0 -0.1 -0.2 -0.4 0.7 0.0 0.3 1.7 3.4 10.3 84.2 100.0 -0.2 -0.7 -1.2 -1.8 -2.9 -2.3 2.4 3.8 5.7 11.0 24.0 17.8 97.1 98.3 98.9 94.0 83.8 0.0 0.0 0.0 4.2 15.9 3.8 4.3 5.3 2.8 1.9 15.2 13.5 28.2 21.6 6.4 -3,286 -5,181 -10,591 -26,089 -79,212 -16.7 -15.6 -15.2 -5.7 -3.4 -0.6 -0.5 -0.9 2.7 1.9 9.7 9.3 20.0 45.3 23.3 -3.1 -3.4 -4.0 -1.9 -1.2 15.6 18.3 22.0 30.8 34.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 Tax Units4 2,3 Cash Income Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Average Federal Tax 6 Rate 1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total Number (thousands) Percent of Total 5,016 8,213 5,981 5,495 5,617 30,543 16.4 26.9 19.6 18.0 18.4 100.0 10,899 22,528 41,094 70,238 257,048 75,737 283 992 2,840 9,009 69,078 15,205 10,616 21,536 38,254 61,229 187,970 60,532 2.6 4.4 6.9 12.8 26.9 20.1 2.4 8.0 10.6 16.7 62.4 100.0 2.9 9.6 12.4 18.2 57.1 100.0 0.3 1.8 3.7 10.7 83.6 100.0 2,427 1,362 1,394 434 42 8.0 4.5 4.6 1.4 0.1 105,444 153,103 267,882 1,396,961 6,520,091 19,712 33,255 69,630 456,038 2,339,269 85,732 119,848 198,252 940,923 4,180,822 18.7 21.7 26.0 32.7 35.9 11.1 9.0 16.1 26.2 12.0 11.3 8.8 15.0 22.1 9.6 10.3 9.8 20.9 42.6 21.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law, Proposal extends 2009 estate tax law and all the individual income tax provisions in the 2001 and 2003 tax cuts other than the high-income provisions. The proposal: retains a 20 percent rate on qualified dividends and capital gains for taxpayers in the top 2 tax brackets (because the proposal repeals the lower rates for gains on assets held for 5 years or more, some high-income taxpayers experience a tax increase); retains the limitation on itemized deductions (Pease) and the personal exemption phaseout (PEP) for taxpayers with income greater than $250,000 for married couples ($200,000 for unmarried individuals), indexed for inflation after 2009; retains a top statutory tax rate of 39.6 percent; retains the 36 percent tax rate and adjusts the threshold for the 36-percent bracket to equal $250,000 less the standard deduction and two personal exemptions for married couples, $200,000 less the standard deduction and one personal exemption for singles, and an amount equal to the midpoint of the married and single thresholds for heads of household, with the dollar values indexed for inflation after 2009. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.