10‐Jun‐11 PRELIMINARY RESULTS Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups.

advertisement

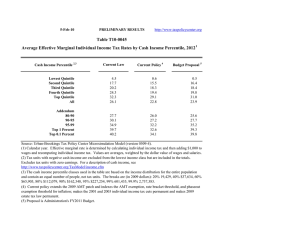

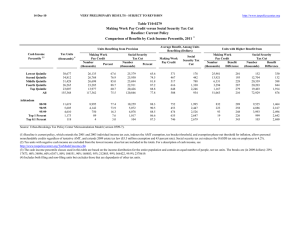

10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy 1 Distribution of Federal Tax Change by Cash Income Percentile, 2013 Summary Table Percent of Tax Units 4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After‐Tax Income 5 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate6 Change (% Points) Under the Proposal 14.1 54.1 86.1 98.0 99.7 63.6 0.1 0.5 0.7 0.3 0.1 0.3 0.2 0.8 2.2 3.6 11.6 7.1 0.2 1.1 4.6 10.3 83.6 100.0 ‐23 ‐205 ‐955 ‐2,572 ‐23,557 ‐4,078 ‐0.2 ‐0.7 ‐1.9 ‐3.0 ‐8.6 ‐5.6 1.6 7.4 13.3 15.9 17.2 15.1 99.6 99.9 99.8 99.9 100.0 0.1 0.1 0.1 * * 5.3 6.5 10.2 21.6 27.9 10.2 8.4 18.3 46.8 26.1 ‐5,672 ‐9,654 ‐25,796 ‐261,433 ‐1,424,842 ‐4.2 ‐5.0 ‐7.6 ‐14.8 ‐18.1 17.3 17.9 17.3 16.6 17.0 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). Number of AMT Taxpayers (millions). Baseline: 4.5 Proposal: 0.0 * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2011 dollars): 20% $17,910; 40% $37,091; 60% $64,533; 80% $111,349; 90% $160,384; 95% $227,324; 99% $593,011; 99.9% $2,682,257. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. TPC estimates are based on Governor Pawlenty's description of his tax proposal and subsequent remarks to the New York Times by his spokesperson Alex Conant. Because Governor Pawlenty did not specify which corporate tax expenditures he would eliminate, we provide an illustrative option that broadens the corporate tax base by eliminating the tax expenditures included in the Bipartisan Policy Center's Rivlin‐Domenici plan. Based on remarks by the Governor and Alex Conant, we did not eliminate any individual income tax expenditures. If Governor Pawlenty or his campaign staff provide the Tax Policy Center with additional details on his proposal we will re‐estimate his plan. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy 1 Distribution of Federal Tax Change by Cash Income Percentile, 2013 Detail Table Percent of Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut 4 With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 14.1 54.1 86.1 98.0 99.7 63.6 0.1 0.5 0.7 0.3 0.1 0.3 0.2 0.8 2.2 3.6 11.6 7.1 0.2 1.1 4.6 10.3 83.6 100.0 ‐23 ‐205 ‐955 ‐2,572 ‐23,557 ‐4,078 ‐12.3 ‐9.1 ‐12.4 ‐15.7 ‐33.4 ‐27.2 0.1 0.9 2.1 2.8 ‐5.8 0.0 0.4 4.3 12.2 20.8 62.2 100.0 ‐0.2 ‐0.7 ‐1.9 ‐3.0 ‐8.6 ‐5.6 1.6 7.4 13.3 15.9 17.2 15.1 99.6 99.9 99.8 99.9 100.0 0.1 0.1 0.1 * * 5.3 6.5 10.2 21.6 27.9 10.2 8.4 18.3 46.8 26.1 ‐5,672 ‐9,654 ‐25,796 ‐261,433 ‐1,424,842 ‐19.4 ‐21.8 ‐30.5 ‐47.1 ‐51.5 1.5 0.8 ‐0.7 ‐7.4 ‐4.6 15.7 11.3 15.6 19.6 9.2 ‐4.2 ‐5.0 ‐7.6 ‐14.8 ‐18.1 17.3 17.9 17.3 16.6 17.0 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 43,362 37,681 32,699 27,208 24,067 166,272 26.1 22.7 19.7 16.4 14.5 100.0 10,122 27,586 50,739 87,197 272,779 72,381 3.7 8.6 13.8 19.7 54.6 100.0 186 2,257 7,722 16,406 70,446 14,984 0.3 3.4 10.1 17.9 68.1 100.0 9,936 25,330 43,016 70,791 202,333 57,397 4.5 10.0 14.7 20.2 51.0 100.0 1.8 8.2 15.2 18.8 25.8 20.7 12,130 5,919 4,805 1,213 124 7.3 3.6 2.9 0.7 0.1 136,031 193,370 338,609 1,767,267 7,871,135 13.7 9.5 13.5 17.8 8.1 29,193 44,300 84,475 555,087 2,765,076 14.2 10.5 16.3 27.0 13.8 106,837 149,071 254,134 1,212,179 5,106,059 13.6 9.2 12.8 15.4 6.7 21.5 22.9 25.0 31.4 35.1 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). Number of AMT Taxpayers (millions). Baseline: 4.5 Proposal: 0.0 * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2011 dollars): 20% $17,910; 40% $37,091; 60% $64,533; 80% $111,349; 90% $160,384; 95% $227,324; 99% $593,011; 99.9% $2,682,257. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 12.1 35.7 85.1 98.1 99.5 63.6 0.1 0.4 0.7 0.3 0.1 0.3 0.2 0.3 1.4 3.3 11.3 7.1 0.1 0.4 2.7 9.1 87.6 100.0 ‐19 ‐75 ‐549 ‐2,020 ‐19,362 ‐4,078 8.0 ‐4.8 ‐9.0 ‐14.5 ‐32.7 ‐27.2 ‐0.2 0.7 2.0 3.0 ‐5.5 0.0 ‐0.5 2.9 10.2 20.1 67.3 100.0 ‐0.2 ‐0.3 ‐1.2 ‐2.7 ‐8.4 ‐5.6 ‐2.7 6.1 12.4 15.7 17.2 15.1 99.3 99.6 99.7 99.9 100.0 0.1 0.1 0.1 * * 5.3 6.5 9.5 21.3 27.9 11.0 9.4 18.6 48.6 27.4 ‐4,836 ‐8,289 ‐20,704 ‐224,635 ‐1,253,902 ‐19.4 ‐21.8 ‐28.9 ‐47.1 ‐51.7 1.7 0.9 ‐0.4 ‐7.7 ‐4.9 17.1 12.7 17.1 20.4 9.6 ‐4.2 ‐5.0 ‐7.1 ‐14.7 ‐18.1 17.3 18.0 17.6 16.4 17.0 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 36,065 34,713 33,034 30,538 30,666 166,272 21.7 20.9 19.9 18.4 18.4 100.0 9,430 24,668 44,764 76,122 230,715 72,381 2.8 7.1 12.3 19.3 58.8 100.0 ‐237 1,572 6,118 13,946 59,133 14,984 ‐0.3 2.2 8.1 17.1 72.8 100.0 9,667 23,095 38,646 62,176 171,582 57,397 3.7 8.4 13.4 19.9 55.1 100.0 ‐2.5 6.4 13.7 18.3 25.6 20.7 15,414 7,701 6,085 1,466 148 9.3 4.6 3.7 0.9 0.1 115,967 165,716 289,779 1,533,122 6,917,786 14.9 10.6 14.7 18.7 8.5 24,950 38,099 71,727 476,633 2,427,135 15.4 11.8 17.5 28.1 14.4 91,017 127,617 218,051 1,056,489 4,490,651 14.7 10.3 13.9 16.2 7.0 21.5 23.0 24.8 31.1 35.1 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). Number of AMT Taxpayers (millions). Baseline: 4.5 Proposal: 0.0 * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table ‐ Single Tax Units Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 12.4 40.0 86.5 98.4 99.0 56.6 0.1 0.3 0.6 0.2 0.1 0.3 0.2 0.4 1.9 4.4 11.6 6.2 0.2 1.0 5.4 14.3 78.9 100.0 ‐15 ‐77 ‐536 ‐1,912 ‐12,843 ‐1,940 ‐4.8 ‐5.1 ‐10.9 ‐17.4 ‐32.6 ‐25.1 0.3 1.3 2.4 2.1 ‐6.1 0.0 1.5 6.1 14.8 22.8 54.6 100.0 ‐0.2 ‐0.4 ‐1.6 ‐3.5 ‐8.6 ‐5.0 4.1 7.6 12.9 16.6 17.7 14.8 98.6 99.1 99.6 99.8 100.0 0.1 0.2 0.1 * 0.0 6.4 6.9 9.1 25.0 34.7 13.3 9.2 15.8 40.6 22.7 ‐4,074 ‐6,145 ‐13,830 ‐173,743 ‐1,065,323 ‐21.3 ‐21.3 ‐27.8 ‐51.3 ‐56.0 0.8 0.6 ‐0.5 ‐7.0 ‐4.2 16.5 11.4 13.8 12.9 6.0 ‐4.9 ‐5.2 ‐6.8 ‐16.8 ‐21.4 18.1 19.2 17.8 15.9 16.8 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 23,198 19,587 15,802 11,719 9,604 80,622 28.8 24.3 19.6 14.5 11.9 100.0 7,467 19,069 33,699 54,610 150,063 39,043 5.5 11.9 16.9 20.3 45.8 100.0 324 1,529 4,897 10,981 39,366 7,723 1.2 4.8 12.4 20.7 60.7 100.0 7,144 17,539 28,801 43,629 110,697 31,320 6.6 13.6 18.0 20.3 42.1 100.0 4.3 8.0 14.5 20.1 26.2 19.8 5,116 2,332 1,790 365 33 6.4 2.9 2.2 0.5 0.0 83,160 118,552 202,277 1,033,246 4,968,941 13.5 8.8 11.5 12.0 5.3 19,149 28,905 49,811 338,423 1,901,322 15.7 10.8 14.3 19.8 10.2 64,011 89,647 152,467 694,823 3,067,618 13.0 8.3 10.8 10.0 4.1 23.0 24.4 24.6 32.8 38.3 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table ‐ Married Tax Units Filing Jointly Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 19.7 35.0 82.1 98.0 99.8 81.9 0.3 1.1 1.2 0.4 0.1 0.5 0.4 0.3 1.1 2.8 11.2 8.1 0.1 0.2 1.3 6.9 91.4 100.0 ‐59 ‐107 ‐554 ‐2,164 ‐22,922 ‐8,371 7.1 ‐5.0 ‐7.6 ‐13.4 ‐32.9 ‐28.6 ‐0.1 0.3 1.5 3.2 ‐4.8 0.0 ‐0.3 1.1 6.5 17.9 74.6 100.0 ‐0.4 ‐0.3 ‐1.0 ‐2.3 ‐8.4 ‐6.3 ‐6.3 5.8 11.6 15.0 17.0 15.7 99.7 99.8 99.8 99.9 100.0 0.1 0.1 0.1 * * 5.1 6.5 9.7 20.3 26.5 10.4 9.9 20.0 51.2 28.4 ‐5,461 ‐9,456 ‐24,048 ‐237,787 ‐1,293,290 ‐19.3 ‐22.2 ‐29.3 ‐46.1 ‐50.6 2.0 1.1 ‐0.2 ‐7.8 ‐4.9 17.4 13.9 19.3 24.0 11.1 ‐4.0 ‐5.0 ‐7.3 ‐14.1 ‐17.4 16.9 17.6 17.5 16.5 17.0 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 4,398 6,664 11,624 15,415 19,298 57,802 7.6 11.5 20.1 26.7 33.4 100.0 14,027 35,110 58,324 93,246 274,004 132,789 0.8 3.1 8.8 18.7 68.9 100.0 ‐823 2,149 7,315 16,189 69,607 29,259 ‐0.2 0.9 5.0 14.8 79.4 100.0 14,850 32,960 51,008 77,057 204,397 103,530 1.1 3.7 9.9 19.9 65.9 100.0 ‐5.9 6.1 12.5 17.4 25.4 22.0 9,190 5,048 4,018 1,042 106 15.9 8.7 7.0 1.8 0.2 135,542 188,768 331,401 1,686,659 7,429,691 16.2 12.4 17.4 22.9 10.3 28,296 42,591 82,170 516,339 2,554,014 15.4 12.7 19.5 31.8 16.0 107,246 146,177 249,230 1,170,320 4,875,677 16.5 12.3 16.7 20.4 8.6 20.9 22.6 24.8 30.6 34.4 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table ‐ Head of Household Tax Units Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 7.4 24.7 86.4 97.4 99.2 42.7 * 0.2 0.2 0.4 * 0.2 0.1 0.2 1.3 2.7 7.8 2.3 0.3 1.7 13.1 22.4 62.5 100.0 ‐7 ‐43 ‐556 ‐1,677 ‐10,262 ‐821 0.5 ‐3.8 ‐7.9 ‐11.7 ‐23.5 ‐16.5 ‐2.1 1.1 2.8 1.8 ‐3.7 0.0 ‐12.1 8.2 30.3 33.4 40.2 100.0 ‐0.1 ‐0.1 ‐1.1 ‐2.2 ‐5.9 ‐2.1 ‐12.3 3.6 13.3 16.8 19.1 10.4 99.3 98.5 99.7 100.0 99.8 0.1 0.0 0.0 0.0 0.0 3.4 4.4 7.5 21.0 28.0 11.6 5.8 13.6 31.6 16.7 ‐2,946 ‐5,192 ‐15,224 ‐195,702 ‐1,167,769 ‐11.6 ‐14.4 ‐24.1 ‐45.4 ‐50.8 1.0 0.2 ‐0.9 ‐4.0 ‐2.2 17.4 6.8 8.5 7.5 3.2 ‐2.6 ‐3.4 ‐5.7 ‐14.4 ‐18.0 20.1 20.1 18.0 17.3 17.5 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 8,232 8,034 4,869 2,769 1,263 25,256 32.6 31.8 19.3 11.0 5.0 100.0 12,526 29,745 49,199 75,439 175,207 39,986 10.2 23.7 23.7 20.7 21.9 100.0 ‐1,538 1,110 7,075 14,327 43,685 4,975 ‐10.1 7.1 27.4 31.6 43.9 100.0 14,065 28,635 42,124 61,112 131,521 35,011 13.1 26.0 23.2 19.1 18.8 100.0 ‐12.3 3.7 14.4 19.0 24.9 12.4 814 230 186 33 3 3.2 0.9 0.7 0.1 0.0 111,657 154,037 266,330 1,361,869 6,471,563 9.0 3.5 4.9 4.5 1.9 25,425 36,163 63,267 431,248 2,299,317 16.5 6.6 9.4 11.5 5.4 86,232 117,874 203,063 930,621 4,172,246 7.9 3.1 4.3 3.5 1.4 22.8 23.5 23.8 31.7 35.5 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). * Less than 0.05 (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table ‐ Tax Units with Children Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 7.9 29.4 89.5 98.9 99.8 63.1 0.1 0.7 0.6 0.2 0.1 0.3 0.1 0.2 1.3 2.9 11.0 6.4 0.1 0.3 2.9 10.1 86.5 100.0 ‐15 ‐62 ‐674 ‐2,356 ‐24,181 ‐4,721 0.7 ‐5.2 ‐7.6 ‐12.3 ‐30.5 ‐25.0 ‐0.8 0.4 2.2 3.5 ‐5.2 0.0 ‐3.1 1.8 11.8 23.9 65.6 100.0 ‐0.1 ‐0.2 ‐1.1 ‐2.3 ‐8.1 ‐5.1 ‐15.9 3.3 13.6 16.6 18.4 15.2 99.8 99.9 99.8 100.0 100.0 0.1 0.1 * 0.0 * 5.1 6.1 10.4 21.0 27.1 11.5 8.8 20.4 45.9 24.2 ‐6,102 ‐10,331 ‐29,963 ‐279,815 ‐1,605,709 ‐17.7 ‐19.7 ‐29.1 ‐44.2 ‐49.4 1.6 0.8 ‐1.0 ‐6.6 ‐4.0 17.9 11.9 16.5 19.3 8.3 ‐3.9 ‐4.7 ‐7.6 ‐14.2 ‐17.5 18.4 19.0 18.6 18.0 17.9 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 10,088 10,789 10,009 9,950 8,349 49,418 20.4 21.8 20.3 20.1 16.9 100.0 13,356 33,957 60,740 101,182 298,935 93,026 2.9 8.0 13.2 21.9 54.3 100.0 ‐2,114 1,196 8,903 19,148 79,224 18,899 ‐2.3 1.4 9.5 20.4 70.8 100.0 15,469 32,761 51,837 82,034 219,711 74,127 4.3 9.7 14.2 22.3 50.1 100.0 ‐15.8 3.5 14.7 18.9 26.5 20.3 4,396 1,981 1,589 382 35 8.9 4.0 3.2 0.8 0.1 154,877 221,864 392,402 1,966,324 9,174,185 14.8 9.6 13.6 16.4 7.0 34,568 52,483 102,861 633,051 3,251,762 16.3 11.1 17.5 25.9 12.2 120,309 169,381 289,541 1,333,273 5,922,424 14.4 9.2 12.6 13.9 5.7 22.3 23.7 26.2 32.2 35.4 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). * Less than 0.05 Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 10‐Jun‐11 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T11‐0171 TPC Interpretation of Governor Tim Pawlenty's Tax Proposal Outline Baseline: Current Policy Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2013 1 Detail Table ‐ Elderly Tax Units Percent of Tax Units4 Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Cut With Tax Increase Percent Change in After‐Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Average Federal Tax Rate 6 Under the Proposal Change (% Points) Under the Proposal 16.2 38.7 74.0 97.0 99.6 64.4 0.0 0.1 1.4 0.9 0.1 0.5 0.2 0.4 1.1 3.5 14.3 8.9 0.1 0.4 1.9 7.2 90.5 100.0 ‐15 ‐84 ‐429 ‐2,170 ‐25,326 ‐5,222 ‐23.3 ‐26.5 ‐21.7 ‐28.2 ‐45.9 ‐43.0 0.0 0.2 1.4 2.8 ‐4.4 0.0 0.1 0.9 5.0 13.8 80.1 100.0 ‐0.2 ‐0.4 ‐1.1 ‐3.1 ‐10.9 ‐7.4 0.5 1.2 3.9 7.9 12.8 9.8 99.4 99.6 99.9 99.9 100.0 * * 0.1 * * 6.2 8.5 11.5 25.2 32.3 9.1 9.6 19.3 52.5 29.3 ‐5,563 ‐10,575 ‐23,935 ‐237,689 ‐1,292,589 ‐33.6 ‐37.0 ‐40.7 ‐54.3 ‐56.9 1.9 1.2 0.8 ‐8.3 ‐5.4 13.6 12.3 21.1 33.2 16.7 ‐5.3 ‐6.9 ‐9.0 ‐17.2 ‐20.6 10.4 11.8 13.1 14.5 15.6 Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes 1 by Cash Income Percentile Adjusted for Family Size, 2013 Tax Units Cash Income Percentile 2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All 4 Pre‐Tax Income Federal Tax Burden After‐Tax Income 5 Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total Average (dollars) Percent of Total 5,988 9,396 8,334 6,402 6,913 37,068 16.2 25.4 22.5 17.3 18.7 100.0 9,531 20,198 40,053 69,759 232,751 71,055 2.2 7.2 12.7 17.0 61.1 100.0 66 316 1,981 7,707 55,130 12,158 0.1 0.7 3.7 11.0 84.6 100.0 9,464 19,882 38,072 62,051 177,621 58,897 2.6 8.6 14.5 18.2 56.2 100.0 0.7 1.6 5.0 11.1 23.7 17.1 3,175 1,753 1,557 427 44 8.6 4.7 4.2 1.2 0.1 105,683 152,604 266,474 1,382,440 6,274,992 12.7 10.2 15.8 22.4 10.4 16,542 28,583 58,752 437,431 2,272,830 11.7 11.1 20.3 41.5 22.1 89,141 124,021 207,722 945,009 4,002,162 13.0 10.0 14.8 18.5 8.0 15.7 18.7 22.1 31.6 36.2 Number (thousands) Addendum 80‐90 90‐95 95‐99 Top 1 Percent Top 0.1 Percent Source: Urban‐Brookings Tax Policy Center Microsimulation Model (version 0411‐2). * Less than 0.05 Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Baseline is current policy, which assumes extension of all temporary provisions in place for 2011 with the exception of the payroll tax cut and indexes the AMT exemption level after 2011. Proposal would: (a) repeal individual alternative minimum tax; (b) impose rate of 10 percent on first $50,000 of taxable income ($100,000 for married couples filing a joint return) and 25 percent on amounts above that threshold, indexed for inflation after 2011; (c) exclude interest income, dividends, and gains from sales of capital assets from gross income; (d) repeal deduction for investment interest; (e) repeal 3.8 percent additional Medicare tax on investment income; (f) impose an alternative tax rate of 15 percent on sole proprietor, farm, partnership, S corporation, and rental income; (g) repeal the estate tax; and (h) reduce the corporate tax rate to 15 percent. Governor Pawlenty has not specified which corporate tax expenditures he would eliminate; our estimates assume the same base broadeners as in the Bipartisan Policy Center's tax reform proposal (Rivlin/Domenici). Effective date: 01/01/13. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2011 dollars): 20% $12,691; 40% $24,715; 60% $41,205; 80% $67,703; 90% $97,820; 95% $138,778; 99% $358,616; 99.9% $1,621,247. (4) Includes both filing and non‐filing units but excludes those that are dependents of other tax units. (5) After‐tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.