Time-Series Analysis

advertisement

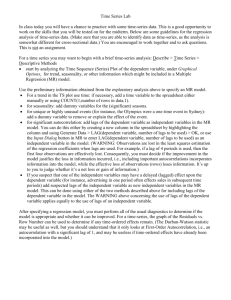

http://www.ifi.uio.no/it/latex-links/STORE/opt/rsi/idl/help/online_help/TimeSeries_Analysis.html Time-Series Analysis A time-series is a sequential collection of data observations indexed over time. In most cases, the observed data is continuous and is recorded at a discrete and finite set of equally-spaced points. An n-element time-series is denoted as x = (x0, x1, x2, ... , xn-1), where the time-indexed distance between any two successive observations is referred to as the sampling interval. A widely held theory assumes that a time-series is comprised of four components: A trend or long term movement. A cyclical fluctuation about the trend. A pronounced seasonal effect. A residual, irregular, or random effect. Collectively, these components make the analysis of a time-series a far more challenging task than just fitting a linear or nonlinear regression model. Adjacent observations are unlikely to be independent of one another. Clusters of observations are frequently correlated with increasing strength as the time intervals between them become shorter. Often the analysis is a multi-step process involving graphical and numerical methods. The first step in the analysis of a time-series is the transformation to stationary series. A stationary series exhibits statistical properties that are unchanged as the period of observation is moved forward or backward in time. Specifically, the mean and variance of a stationary time-series remain fixed in time. The sample autocorrelation function is a commonly used tool in determining the stationarity of a time-series. The autocorrelation of a timeseries measures the dependence between observations as a function of their time differences or lag. A plot of the sample autocorrelation coefficients against corresponding lags can be very helpful in determining the stationarity of a time-series. For example, suppose the IDL variable X contains time-series data: X = [5.44, 5.21, 6.16, 5.36, 5.29, 6.38, 5.23, 6.07, 5.17, 5.58, 5.43, 4.33, 6.56, 5.35, 4.77, 5.22, 5.58, 5.93, 5.61, 5.17, 5.28, 6.18, 5.70, 5.83, 5.33] $ $ $ $ The following IDL commands plot both the time-series data and the sample autocorrelation versus the lags. ; Set the plotting window to hold two plots and plot the data: IPLOT, X, VIEW_GRID=[1,2] Compute the sample autocorrelation function for time lagged values 0 - 20 and plot. lag = INDGEN(21) result = A_CORRELATE(X, lag) IPLOT, lag, result, /VIEW_NEXT ; Add a reference line at zero: IPLOT, [0,20], [0,0], /OVERPLOT The following figure shows the resulting graphs. Figure 11-3: Time-series data (Top) and Autocorrelation of that Data Versus the Lag (Bottom) Figure 11-3: Time-series data (Top) and Autocorrelation of that Data Versus the Lag (Bottom) The top graph plots time-series data. The bottom graph plots the autocorrelation of that data versus the lag. Because the time-series has a significant autocorrelation up to a lag of seven, it must be considered nonstationary. Nonstationary components of a time-series may be eliminated in a variety of ways. Two frequently used methods are known as moving averages and forward differencing. The method of moving averages dampens fluctuations in a time-series by taking successive averages of groups of observations. Each successive overlapping sequence of k observations in the series is replaced by the mean of that sequence. The method of forward differencing replaces each time-series observation with the difference of the current observation and its adjacent observation one step forward in time. Differencing may be computed recursively to eliminate more complex nonstationary components. Once a time-series has been transformed to stationarity, it may be modeled using an autoregressive process. An autoregressive process expresses the current observation, xt, as a combination of past time-series values and residual white noise. The simplest case is known as a first order autoregressive model and is expressed as xt = xt-1 + t The coefficient is estimated using the time-series data. The general autoregressive model of order p is expressed as xt = 1xt-1 +2xt-2 + ... + pxt-p + t Modeling a stationary time-series as a p-th order autoregressive process allows the extrapolation of data for future values of time. This process is know as forecasting.