Option 2: Reduce the Maximum Amount of Debt Eligible for... Baseline: Current Law

advertisement

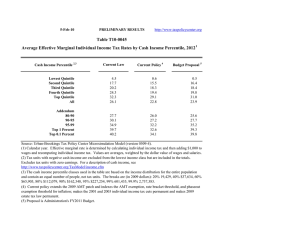

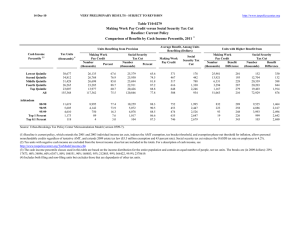

14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2016 ¹ Summary Table Tax Units with Tax Increase or Cut 4 Expanded Cash Income Percentile2,3 With Tax Cut Pct of Tax Units Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Avg Tax Cut With Tax Increase Avg Tax Pct of Tax Units Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0 0 0 0 0 0 0.0 0.0 0.1 0.9 6.2 1.0 0 0 571 1,330 3,657 3,255 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.1 0.4 5.9 93.6 100.0 0 0 1 12 225 33 0.0 0.0 0.0 0.0 0.1 0.0 4.3 8.3 13.7 17.4 26.4 20.4 0.0 0.0 0.0 0.0 0.0 0 0 0 0 0 2.6 5.0 13.0 24.4 26.0 1,671 2,852 4,048 5,960 6,135 0.0 -0.1 -0.2 -0.1 0.0 9.2 14.8 40.9 28.8 3.2 43 142 525 1,455 1,596 0.0 0.1 0.1 0.1 0.0 20.4 22.3 25.9 34.2 35.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). Number of AMT Taxpayers (millions). Baseline: 4.3 Proposal: 4.3 * Less than 0.05 ** Insufficient data (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2015 dollars): 20% $22,823; 40% $44,550; 60% $79,661; 80% $141,303; 90% $207,758; 95% $294,348; 99% $720,886; 99.9% $3,672,221. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2016 ¹ Detail Table Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.9 6.2 1.0 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.1 0.4 5.9 93.6 100.0 0 0 1 12 225 33 0.0 0.0 0.0 0.1 0.3 0.2 0.0 0.0 0.0 0.0 0.1 0.0 0.9 3.4 9.4 17.4 68.7 100.0 0.0 0.0 0.0 0.0 0.1 0.0 4.3 8.3 13.7 17.4 26.4 20.4 0.0 0.0 0.0 0.0 0.0 2.6 5.0 13.0 24.4 26.0 0.0 -0.1 -0.2 -0.1 0.0 9.2 14.8 40.9 28.8 3.2 43 142 525 1,455 1,596 0.1 0.3 0.5 0.2 0.0 0.0 0.0 0.1 0.0 0.0 14.1 10.7 15.8 28.1 13.5 0.0 0.1 0.1 0.1 0.0 20.4 22.3 25.9 34.2 35.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Percent of Total Federal Tax Burden Average (dollars) Percent of Total After-Tax Income 5 Average (dollars) Percent of Total Average Federal Tax Rate 6 47,691 37,422 33,984 28,418 23,750 172,532 27.6 21.7 19.7 16.5 13.8 100.0 13,336 33,359 61,542 107,903 336,456 86,987 4.2 8.3 13.9 20.4 53.2 100.0 568 2,782 8,456 18,784 88,524 17,747 0.9 3.4 9.4 17.4 68.7 100.0 12,768 30,577 53,086 89,120 247,931 69,241 5.1 9.6 15.1 21.2 49.3 100.0 4.3 8.3 13.7 17.4 26.3 20.4 12,233 5,942 4,447 1,129 115 7.1 3.4 2.6 0.7 0.1 173,085 248,145 420,979 2,239,143 10,045,915 14.1 9.8 12.5 16.8 7.7 35,184 55,136 108,599 763,369 3,579,846 14.1 10.7 15.8 28.1 13.5 137,901 193,009 312,380 1,475,774 6,466,069 14.1 9.6 11.6 13.9 6.3 20.3 22.2 25.8 34.1 35.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent 6 Under the Proposal Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). Number of AMT Taxpayers (millions). Baseline: 4.3 Proposal: 4.3 * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2015 dollars): 20% $22,823; 40% $44,550; 60% $79,661; 80% $141,303; 90% $207,758; 95% $294,348; 99% $720,886; 99.9% $3,672,221. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.8 4.8 1.0 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.0 0.9 6.1 93.0 100.0 0 0 1 11 176 33 0.0 0.0 0.0 0.1 0.2 0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.1 2.4 7.6 16.7 73.1 100.0 0.0 0.0 0.0 0.0 0.1 0.0 0.5 6.8 12.5 16.9 26.0 20.4 0.0 0.0 0.0 0.0 0.0 2.1 3.4 9.7 22.3 23.7 0.0 -0.1 -0.1 -0.1 0.0 11.2 14.0 37.8 30.1 3.6 41 106 375 1,299 1,504 0.1 0.2 0.4 0.2 0.1 0.0 0.0 0.0 0.0 0.0 15.1 11.7 17.3 29.1 14.1 0.0 0.1 0.1 0.1 0.0 20.2 22.2 25.5 34.0 35.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Number (thousands) Pre-Tax Income Percent of Total Average (dollars) Percent of Total Federal Tax Burden Average (dollars) Percent of Total After-Tax Income 5 Average (dollars) Percent of Total Average Federal Tax Rate 6 38,232 36,211 34,505 32,174 30,143 172,532 22.2 21.0 20.0 18.7 17.5 100.0 12,438 29,245 53,941 94,039 285,692 86,987 3.2 7.1 12.4 20.2 57.4 100.0 57 2,000 6,723 15,900 74,202 17,747 0.1 2.4 7.6 16.7 73.1 100.0 12,381 27,245 47,219 78,139 211,490 69,241 4.0 8.3 13.6 21.0 53.4 100.0 0.5 6.8 12.5 16.9 26.0 20.4 15,518 7,548 5,756 1,321 136 9.0 4.4 3.3 0.8 0.1 147,812 214,051 361,215 1,985,313 8,905,644 15.3 10.8 13.9 17.5 8.1 29,773 47,345 91,720 673,125 3,173,218 15.1 11.7 17.2 29.1 14.1 118,039 166,706 269,496 1,312,188 5,732,427 15.3 10.5 13.0 14.5 6.5 20.1 22.1 25.4 33.9 35.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). Number of AMT Taxpayers (millions). Baseline: 4.3 Proposal: 4.3 * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table - Single Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.2 1.8 0.2 0.0 0.0 0.0 0.0 -0.1 0.0 0.0 0.0 0.8 1.0 98.2 100.0 0 0 0 0 60 6 0.0 0.0 0.0 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 2.1 6.0 13.8 22.2 55.6 100.0 0.0 0.0 0.0 0.0 0.0 0.0 6.2 8.6 13.8 18.3 26.1 18.6 0.0 0.0 0.0 0.0 0.0 0.8 0.9 4.5 16.3 19.0 0.0 0.0 -0.1 -0.1 0.0 13.6 7.4 38.2 39.0 6.9 14 20 148 879 1,253 0.1 0.1 0.2 0.2 0.1 0.0 0.0 0.0 0.0 0.0 16.1 9.3 12.0 18.2 9.7 0.0 0.0 0.1 0.1 0.0 21.3 22.6 25.9 36.4 37.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Pre-Tax Income 29.5 24.8 20.2 14.7 10.1 100.0 9,700 23,067 41,046 68,044 175,035 44,584 6.4 12.8 18.6 22.5 39.6 100.0 598 1,993 5,642 12,461 45,615 8,266 2.1 6.0 13.8 22.2 55.6 100.0 9,102 21,074 35,404 55,583 129,420 36,317 7.4 14.4 19.7 22.6 35.9 100.0 6.2 8.6 13.8 18.3 26.1 18.5 5,172 2,001 1,374 237 29 5.9 2.3 1.6 0.3 0.0 105,179 148,758 244,058 1,524,021 6,406,099 14.0 7.7 8.6 9.3 4.8 22,416 33,635 62,976 553,461 2,391,340 16.1 9.3 12.0 18.2 9.7 82,763 115,123 181,081 970,560 4,014,758 13.5 7.3 7.9 7.3 3.7 21.3 22.6 25.8 36.3 37.3 Average (dollars) Percent of Total Average Federal Tax Rate 6 25,683 21,585 17,636 12,851 8,784 87,180 Average (dollars) Percent of Total After-Tax Income 5 Percent of Total Average (dollars) Percent of Total Federal Tax Burden Number (thousands) Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table - Married Tax Units Filing Jointly Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 * 0.3 1.3 6.2 2.5 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.0 0.7 6.1 93.1 100.0 0 0 3 19 234 85 0.0 0.0 0.0 0.1 0.3 0.2 0.0 0.0 0.0 0.0 0.0 0.0 -0.1 0.8 4.2 13.8 81.1 100.0 0.0 0.0 0.0 0.0 0.1 0.1 -1.3 6.3 11.5 16.1 26.0 22.2 0.0 0.0 0.0 0.0 0.0 2.8 4.4 11.6 23.8 25.8 0.0 -0.1 -0.2 -0.1 0.0 10.8 14.7 38.3 29.3 3.2 57 141 454 1,411 1,619 0.2 0.3 0.5 0.2 0.1 0.0 0.0 0.0 0.0 0.0 14.9 12.8 20.0 33.3 15.4 0.0 0.1 0.1 0.1 0.0 19.7 22.0 25.4 33.5 35.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Pre-Tax Income 8.4 11.4 18.7 27.0 33.7 100.0 18,801 41,196 71,227 115,487 338,411 164,217 1.0 2.9 8.1 19.0 69.4 100.0 -235 2,578 8,194 18,618 87,643 36,401 -0.1 0.8 4.2 13.8 81.0 100.0 19,035 38,618 63,033 96,869 250,768 127,815 1.2 3.5 9.2 20.4 66.0 100.0 -1.3 6.3 11.5 16.1 25.9 22.2 9,309 5,126 4,159 1,023 97 16.0 8.8 7.1 1.8 0.2 172,936 241,837 403,001 2,065,598 9,569,483 16.8 13.0 17.5 22.1 9.7 33,980 53,138 101,902 690,920 3,373,039 14.9 12.8 20.0 33.3 15.5 138,956 188,699 301,099 1,374,678 6,196,444 17.4 13.0 16.8 18.9 8.1 19.7 22.0 25.3 33.5 35.3 Average (dollars) Percent of Total Average Federal Tax Rate 6 4,872 6,661 10,912 15,713 19,617 58,288 Average (dollars) Percent of Total After-Tax Income 5 Percent of Total Average (dollars) Percent of Total Federal Tax Burden Number (thousands) Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table - Head of Household Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.4 1.2 4.2 0.4 0.0 0.0 0.0 0.0 -0.1 0.0 0.0 0.0 5.6 20.7 73.7 100.0 0 0 2 13 117 8 0.0 0.0 0.0 0.1 0.2 0.1 0.0 0.0 0.0 0.0 0.0 0.0 -8.2 6.7 24.4 32.4 44.7 100.0 0.0 0.0 0.0 0.0 0.1 0.0 -9.6 3.7 11.4 17.2 25.2 11.9 0.0 0.0 0.0 0.0 0.0 3.0 3.5 7.7 25.8 24.7 0.0 -0.1 -0.1 -0.1 0.0 12.9 14.6 24.9 21.4 2.5 32 99 355 1,361 1,471 0.1 0.2 0.4 0.2 0.0 0.0 0.0 0.0 0.0 0.0 14.7 8.1 7.4 14.5 8.4 0.0 0.1 0.1 0.1 0.0 21.0 22.6 25.8 34.2 35.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Pre-Tax Income Federal Tax Burden 7,312 7,436 5,226 2,957 1,165 24,145 30.3 30.8 21.6 12.3 4.8 100.0 17,857 36,660 62,412 97,505 231,777 53,332 10.1 21.2 25.3 22.4 21.0 100.0 -1,713 1,365 7,117 16,727 58,374 6,313 -8.2 6.7 24.4 32.5 44.6 100.0 19,570 35,295 55,295 80,778 173,403 47,020 12.6 23.1 25.5 21.0 17.8 100.0 -9.6 3.7 11.4 17.2 25.2 11.8 734 273 129 29 3 3.0 1.1 0.5 0.1 0.0 145,231 201,115 337,575 2,238,359 11,305,434 8.3 4.3 3.4 5.0 2.8 30,410 45,291 86,585 763,247 4,060,765 14.7 8.1 7.4 14.5 8.4 114,821 155,824 250,990 1,475,112 7,244,669 7.4 3.7 2.9 3.8 2.0 20.9 22.5 25.7 34.1 35.9 Average (dollars) Percent of Total Average (dollars) Percent of Total Average Federal Tax Rate 6 Percent of Total Average (dollars) Percent of Total After-Tax Income 5 Number (thousands) Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table - Tax Units with Children Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.5 2.0 9.1 2.2 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.0 1.2 8.5 90.3 100.0 0 0 4 31 351 73 0.0 0.0 0.1 0.1 0.3 0.3 0.0 0.0 0.0 0.0 0.0 0.0 -1.3 1.4 7.2 16.8 75.7 100.0 0.0 0.0 0.0 0.0 0.1 0.1 -8.8 4.3 12.4 17.3 26.8 20.7 0.0 0.0 0.0 0.0 0.0 4.7 7.2 17.0 30.7 32.8 -0.1 -0.1 -0.2 -0.1 0.0 12.8 16.2 37.0 24.3 2.7 99 260 717 1,839 2,092 0.3 0.4 0.6 0.2 0.1 0.0 0.0 0.1 0.0 0.0 14.8 11.3 18.4 31.3 14.3 0.1 0.1 0.2 0.1 0.0 20.5 22.8 26.5 34.1 35.2 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Pre-Tax Income 20.4 20.7 20.0 19.7 18.6 100.0 18,852 40,647 74,066 126,678 388,066 123,886 3.1 6.8 12.0 20.1 58.4 100.0 -1,667 1,733 9,191 21,860 103,661 25,527 -1.3 1.4 7.2 16.9 75.7 100.0 20,519 38,914 64,875 104,819 284,405 98,359 4.3 8.2 13.2 21.0 53.9 100.0 -8.8 4.3 12.4 17.3 26.7 20.6 4,730 2,275 1,882 482 47 9.4 4.5 3.7 1.0 0.1 195,763 280,240 473,252 2,453,236 11,186,185 14.9 10.2 14.3 19.0 8.4 40,041 63,617 124,816 834,989 3,940,058 14.8 11.3 18.3 31.3 14.3 155,722 216,623 348,436 1,618,247 7,246,127 14.9 10.0 13.3 15.8 6.8 20.5 22.7 26.4 34.0 35.2 Average (dollars) Percent of Total Average Federal Tax Rate 6 10,234 10,415 10,074 9,897 9,368 50,272 Average (dollars) Percent of Total After-Tax Income 5 Percent of Total Average (dollars) Percent of Total Federal Tax Burden Number (thousands) Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0224 Option 2: Reduce the Maximum Amount of Debt Eligible for the Mortgage Interest Deduction to $500,000 Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Detail Table - Elderly Tax Units Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units With Tax Cut 4 With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 * 0.2 2.4 0.4 0.0 0.0 0.0 0.0 -0.1 0.0 0.0 0.0 1.5 2.8 95.7 100.0 0 0 1 2 97 15 0.0 0.0 0.0 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.2 1.3 4.9 13.2 80.0 100.0 0.0 0.0 0.0 0.0 0.0 0.0 1.7 2.6 6.0 11.9 25.9 17.8 0.0 0.0 0.0 0.0 0.0 0.7 1.1 5.2 16.5 18.9 0.0 0.0 -0.1 -0.1 0.0 6.9 7.1 29.5 52.2 8.0 13 29 172 1,019 1,193 0.1 0.1 0.2 0.2 0.0 0.0 0.0 0.0 0.0 0.0 13.2 10.6 15.3 40.9 22.6 0.0 0.0 0.1 0.1 0.0 17.2 20.3 24.4 34.9 36.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Percentile Adjusted for Family Size, 2016 ¹ Expanded Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Tax Units Pre-Tax Income 16.4 26.5 22.9 18.0 15.1 100.0 11,850 24,835 47,748 83,981 277,400 76,347 2.6 8.6 14.3 19.8 55.0 100.0 197 642 2,885 9,948 71,666 13,565 0.2 1.3 4.9 13.2 80.0 100.0 11,652 24,194 44,863 74,033 205,734 62,782 3.1 10.2 16.3 21.2 49.6 100.0 1.7 2.6 6.0 11.9 25.8 17.8 3,290 1,531 1,087 325 43 8.0 3.7 2.6 0.8 0.1 130,820 191,752 321,464 2,015,265 8,080,211 13.7 9.3 11.1 20.9 11.0 22,416 38,813 78,335 701,931 2,947,959 13.2 10.6 15.2 40.9 22.6 108,404 152,939 243,130 1,313,334 5,132,252 13.8 9.1 10.2 16.5 8.5 17.1 20.2 24.4 34.8 36.5 Average (dollars) Percent of Total Average Federal Tax Rate 6 6,761 10,923 9,410 7,396 6,233 41,164 Average (dollars) Percent of Total After-Tax Income 5 Percent of Total Average (dollars) Percent of Total Federal Tax Burden Number (thousands) Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law. Proposal would reduce the maximum amount of debt eligible for the mortgage interest deduction to $500,000 of debt on a primary residence, second home, and/or a home equity loan. Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2015 dollars): 20% $15,856; 40% $29,550; 60% $51,312; 80% $85,800; 90% $124,732; 95% $174,098; 99% $413,202; 99.9% $2,095,408. (4) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (5) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income.