Table T10-0153

advertisement

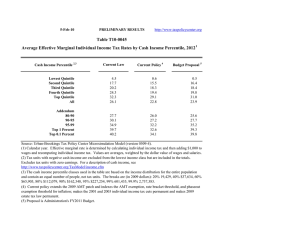

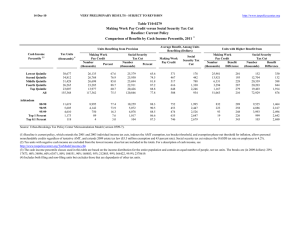

21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile, 2012 1 Summary Table Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.2 0.3 0.2 0.6 1.7 10.4 17.9 69.1 100.0 -3 -9 -58 -119 -525 -112 0.0 0.0 -0.1 -0.1 -0.2 -0.2 4.6 10.3 16.4 19.3 25.0 20.8 0.1 0.1 0.2 0.4 0.6 0.0 0.0 0.0 0.0 0.0 0.2 0.2 0.4 0.2 0.1 15.7 11.0 25.7 16.7 2.6 -237 -340 -977 -2,480 -3,887 -0.2 -0.2 -0.3 -0.1 -0.1 21.8 23.0 24.9 28.7 31.1 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 5.0 Proposal: 5.0 ** This table is part of a series of tables showing the distributional effects of moving incrementally from current law to current policy. For definitions and further information, see “Related Tables: Moving Incrementally from Current Law to Current Policy” at http://taxpolicycenter.org/numbers/displayatab.cfm?template=simulation&SimID=366 (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 percent tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,356, 40% $37,493, 60% $65,656, 80% $111,659, 90% $161,739, 95% $226,402, 99% $599,181, 99.9% $2,727,123. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile, 2012 1 Detail Table Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.2 0.3 0.2 0.6 1.7 10.4 17.9 69.1 100.0 -3 -9 -58 -119 -525 -112 -0.5 -0.3 -0.7 -0.7 -0.7 -0.7 0.0 0.0 0.0 0.0 0.0 0.0 0.8 4.2 10.9 18.4 65.6 100.0 0.0 0.0 -0.1 -0.1 -0.2 -0.2 4.6 10.3 16.4 19.3 25.0 20.8 0.1 0.1 0.2 0.4 0.6 0.0 0.0 0.0 0.0 0.0 0.2 0.2 0.4 0.2 0.1 15.7 11.0 25.7 16.7 2.6 -237 -340 -977 -2,480 -3,887 -0.8 -0.8 -1.1 -0.5 -0.2 0.0 0.0 -0.1 0.1 0.1 14.2 10.4 16.1 25.0 12.5 -0.2 -0.2 -0.3 -0.1 -0.1 21.8 23.0 24.9 28.7 31.1 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile, 2012 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 38,450 34,947 31,868 26,646 23,298 157,348 24.4 22.2 20.3 16.9 14.8 100.0 11,600 28,852 52,224 88,978 280,229 76,169 536 2,970 8,617 17,314 70,664 15,954 11,064 25,882 43,606 71,663 209,565 60,215 4.6 10.3 16.5 19.5 25.2 21.0 3.7 8.4 13.9 19.8 54.5 100.0 4.5 9.6 14.7 20.2 51.5 100.0 0.8 4.1 10.9 18.4 65.6 100.0 11,720 5,734 4,655 1,190 120 7.5 3.6 3.0 0.8 0.1 138,385 196,549 345,574 1,825,188 8,367,274 30,374 45,448 86,906 525,547 2,608,788 108,011 151,101 258,669 1,299,641 5,758,486 22.0 23.1 25.2 28.8 31.2 13.5 9.4 13.4 18.1 8.4 13.4 9.1 12.7 16.3 7.3 14.2 10.4 16.1 24.9 12.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 5.0 Proposal: 5.0 (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 percent tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,356, 40% $37,493, 60% $65,656, 80% $111,659, 90% $161,739, 95% $226,402, 99% $599,181, 99.9% $2,727,123. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table 4 Percent of Tax Units Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1 0.3 0.2 0.3 0.8 5.2 8.6 84.7 100.0 -2 -5 -30 -50 -501 -112 -1.6 -0.2 -0.4 -0.3 -0.9 -0.7 0.0 0.0 0.0 0.1 -0.1 0.0 0.1 2.9 8.7 17.6 70.5 100.0 0.0 0.0 -0.1 -0.1 -0.2 -0.2 1.0 8.5 15.1 18.9 24.9 20.8 0.1 0.1 0.3 0.6 0.8 0.0 0.0 0.0 0.0 0.0 0.2 0.2 0.4 0.3 0.1 13.1 11.8 32.5 27.2 4.1 -155 -278 -968 -3,356 -5,052 -0.6 -0.7 -1.3 -0.7 -0.2 0.0 0.0 -0.1 0.0 0.1 15.5 11.7 17.3 26.0 13.0 -0.1 -0.2 -0.3 -0.2 -0.1 21.9 23.2 24.6 28.5 30.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Average Federal Tax 6 Rate Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 31,706 32,349 31,237 29,980 29,936 157,348 20.2 20.6 19.9 19.1 19.0 100.0 10,935 26,208 46,322 77,565 235,547 76,169 114 2,221 7,000 14,691 59,198 15,954 10,821 23,987 39,322 62,875 176,349 60,215 1.0 8.5 15.1 18.9 25.1 21.0 2.9 7.1 12.1 19.4 58.8 100.0 3.6 8.2 13.0 19.9 55.7 100.0 0.1 2.9 8.7 17.6 70.6 100.0 15,019 7,540 5,940 1,436 142 9.6 4.8 3.8 0.9 0.1 117,658 167,170 294,212 1,584,726 7,360,192 25,937 38,973 73,449 454,265 2,279,204 91,720 128,197 220,763 1,130,461 5,080,988 22.0 23.3 25.0 28.7 31.0 14.7 10.5 14.6 19.0 8.7 14.5 10.2 13.8 17.1 7.6 15.5 11.7 17.4 26.0 12.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 5.0 Proposal: 5.0 (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 perc tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 20121 Detail Table - Single Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.1 0.3 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.3 1.2 0.6 0.3 0.4 5.8 8.8 84.5 100.0 -2 -4 -62 -114 -1,314 -217 -0.4 -0.2 -1.1 -1.0 -3.3 -2.3 0.0 0.1 0.2 0.3 -0.6 0.0 1.6 5.2 12.8 21.2 59.1 100.0 0.0 0.0 -0.2 -0.2 -0.9 -0.5 7.1 10.7 16.9 20.8 25.6 20.9 0.2 0.3 0.7 1.4 1.5 0.0 0.0 0.0 0.0 0.0 0.7 0.9 1.8 1.4 0.3 14.8 12.8 32.4 24.5 2.5 -437 -803 -2,692 -10,112 -11,890 -2.2 -2.7 -5.1 -3.1 -0.7 0.0 0.0 -0.4 -0.1 0.2 15.7 10.9 14.1 18.3 8.8 -0.5 -0.7 -1.3 -1.0 -0.2 23.3 24.3 24.3 30.3 33.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 16,972 15,474 14,005 11,543 9,596 68,932 24.6 22.5 20.3 16.8 13.9 100.0 8,380 19,970 34,261 55,833 151,979 43,878 595 2,136 5,846 11,723 40,206 9,386 7,786 17,834 28,416 44,110 111,773 34,492 5,066 2,373 1,795 361 32 7.4 3.4 2.6 0.5 0.1 84,037 119,032 204,548 1,060,631 5,243,107 20,048 29,751 52,417 331,108 1,777,081 63,990 89,280 152,131 729,523 3,466,025 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 7.1 10.7 17.1 21.0 26.5 21.4 4.7 10.2 15.9 21.3 48.2 100.0 5.6 11.6 16.7 21.4 45.1 100.0 1.6 5.1 12.7 20.9 59.6 100.0 23.9 25.0 25.6 31.2 33.9 14.1 9.3 12.1 12.7 5.5 13.6 8.9 11.5 11.1 4.6 15.7 10.9 14.5 18.5 8.7 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 percent tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 20121 Detail Table - Married Tax Units Filing Jointly Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.0 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.0 0.8 3.2 1.7 6.0 87.4 100.0 -3 -9 -4 -10 -115 -40 -2.4 -0.3 0.0 -0.1 -0.2 -0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.1 1.4 5.6 15.3 77.6 100.0 0.0 0.0 0.0 0.0 0.0 0.0 0.8 7.8 13.5 17.8 24.7 21.6 0.0 0.0 0.1 0.3 0.6 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1 0.1 3.3 5.9 33.8 44.4 13.0 -9 -30 -213 -1,074 -3,123 0.0 -0.1 -0.3 -0.2 -0.1 0.0 0.0 0.0 0.0 0.0 15.7 12.7 19.5 29.8 14.7 0.0 0.0 -0.1 -0.1 0.0 21.3 22.8 24.8 28.0 30.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 6,622 8,956 11,470 15,032 18,609 61,357 10.8 14.6 18.7 24.5 30.3 100.0 14,526 33,405 59,671 95,023 281,842 126,020 118 2,624 8,078 16,945 69,733 27,246 14,408 30,780 51,593 78,078 212,109 98,773 8,860 4,843 3,890 1,015 102 14.4 7.9 6.3 1.7 0.2 138,312 192,091 337,723 1,748,464 7,890,377 29,506 43,779 83,813 490,657 2,396,246 108,806 148,311 253,909 1,257,807 5,494,131 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 0.8 7.9 13.5 17.8 24.7 21.6 1.2 3.9 8.9 18.5 67.8 100.0 1.6 4.6 9.8 19.4 65.1 100.0 0.1 1.4 5.5 15.2 77.6 100.0 21.3 22.8 24.8 28.1 30.4 15.9 12.0 17.0 23.0 10.5 15.9 11.9 16.3 21.1 9.3 15.6 12.7 19.5 29.8 14.7 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 percent tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 20121 Detail Table - Head of Household Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.0 0.2 2.0 6.6 18.4 72.4 100.0 0 -1 -4 -18 -162 -11 0.0 0.0 -0.1 -0.1 -0.4 -0.2 0.0 0.0 0.0 0.0 -0.1 0.0 -5.4 9.7 27.7 29.7 38.1 100.0 0.0 0.0 0.0 0.0 -0.1 0.0 -7.2 6.0 15.3 19.7 24.2 13.8 0.0 0.1 0.1 0.2 0.4 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.2 0.2 0.1 10.4 15.9 25.9 20.3 3.8 -36 -190 -416 -1,701 -3,599 -0.1 -0.5 -0.6 -0.4 -0.2 0.0 0.0 0.0 0.0 0.0 14.7 5.9 8.0 9.6 4.5 0.0 -0.1 -0.2 -0.1 -0.1 22.8 23.2 23.4 28.7 31.0 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 7,840 7,497 5,095 2,777 1,242 24,547 31.9 30.5 20.8 11.3 5.1 100.0 13,490 30,617 50,275 76,881 178,521 41,760 -966 1,831 7,680 15,125 43,432 5,757 14,455 28,786 42,595 61,756 135,089 36,003 805 232 173 33 3 3.3 0.9 0.7 0.1 0.0 112,763 154,893 278,418 1,423,600 6,950,503 25,734 36,085 65,508 410,578 2,157,929 87,028 118,809 212,910 1,013,022 4,792,574 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total -7.2 6.0 15.3 19.7 24.3 13.8 10.3 22.4 25.0 20.8 21.6 100.0 12.8 24.4 24.6 19.4 19.0 100.0 -5.4 9.7 27.7 29.7 38.2 100.0 22.8 23.3 23.5 28.8 31.1 8.9 3.5 4.7 4.6 2.0 7.9 3.1 4.2 3.8 1.6 14.7 5.9 8.0 9.6 4.5 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 percent tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Tax Units with Children 4 Percent of Tax Units Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 1.2 3.4 17.5 77.0 100.0 0 -1 -2 -11 -57 -12 0.0 0.0 0.0 -0.1 -0.1 -0.1 0.0 0.0 0.0 0.0 0.0 0.0 -1.4 2.3 10.2 20.4 68.4 100.0 0.0 0.0 0.0 0.0 0.0 0.0 -8.9 6.1 15.4 19.4 25.9 20.5 0.0 0.0 0.0 0.1 0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 5.9 6.8 33.4 31.0 7.2 -8 -21 -131 -508 -1,218 0.0 0.0 -0.1 -0.1 0.0 0.0 0.0 0.0 0.0 0.0 16.3 11.0 17.0 24.1 11.5 0.0 0.0 0.0 0.0 0.0 22.6 23.9 26.1 29.7 31.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Number (thousands) Percent of Total 10,133 10,359 10,251 9,800 8,315 49,155 20.6 21.1 20.9 19.9 16.9 100.0 14,723 34,672 62,298 103,142 306,063 95,419 -1,303 2,103 9,603 19,996 79,198 19,586 16,026 32,569 52,695 83,146 226,865 75,833 4,398 1,976 1,567 374 36 9.0 4.0 3.2 0.8 0.1 157,496 224,546 400,356 2,088,455 9,839,694 35,649 53,579 104,707 619,706 3,079,014 121,846 170,967 295,648 1,468,749 6,760,680 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -8.9 6.1 15.4 19.4 25.9 20.5 3.2 7.7 13.6 21.6 54.3 100.0 4.4 9.1 14.5 21.9 50.6 100.0 -1.4 2.3 10.2 20.4 68.4 100.0 22.6 23.9 26.2 29.7 31.3 14.8 9.5 13.4 16.7 7.6 14.4 9.1 12.4 14.7 6.5 16.3 11.0 17.1 24.1 11.5 Average Federal Tax 6 Rate Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 perc tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0153 Incremental Effects of Extending the 2001 and 2003 Tax Cuts Impose Estate Tax with 45 Percent Tax Rate and $3.5 Million Exemption, Not Indexed Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Elderly Tax Units 4 Percent of Tax Units Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Share of Federal Taxes Change (% Points) Percent Under the Proposal Average Federal Tax Rate Change (% Points) 6 Under the Proposal 0.0 0.0 0.0 0.1 0.7 0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1 0.4 0.4 1.2 0.8 0.3 0.7 5.4 8.6 84.7 100.0 -9 -14 -138 -238 -2,293 -498 -3.3 -1.6 -5.6 -3.0 -3.7 -3.7 0.0 0.0 -0.1 0.1 0.0 0.0 0.3 1.8 3.5 10.7 83.6 100.0 -0.1 -0.1 -0.3 -0.3 -0.9 -0.7 2.4 3.8 5.7 11.0 23.0 17.2 0.4 0.5 1.0 1.6 2.0 0.0 0.0 0.0 0.0 0.0 1.0 1.1 1.7 0.9 0.3 14.3 12.1 32.5 25.9 3.4 -896 -1,345 -3,543 -9,071 -12,215 -5.2 -4.6 -5.7 -2.2 -0.6 -0.2 -0.1 -0.4 0.7 0.7 10.0 9.6 20.6 43.4 21.9 -0.9 -0.9 -1.3 -0.7 -0.2 15.6 18.3 21.9 28.5 31.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Number (thousands) Percent of Total 5,016 8,213 5,981 5,495 5,617 30,543 16.4 26.9 19.6 18.0 18.4 100.0 10,899 22,528 41,094 70,238 257,048 75,737 271 860 2,493 7,965 61,481 13,515 10,628 21,668 38,601 62,273 195,567 62,223 2,427 1,362 1,394 434 42 8.0 4.5 4.6 1.4 0.1 105,444 153,103 267,882 1,396,961 6,520,091 17,322 29,419 62,221 406,889 2,062,172 88,122 123,684 205,661 990,072 4,457,919 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 2.5 3.8 6.1 11.3 23.9 17.8 2.4 8.0 10.6 16.7 62.4 100.0 2.8 9.4 12.2 18.0 57.8 100.0 0.3 1.7 3.6 10.6 83.7 100.0 16.4 19.2 23.2 29.1 31.6 11.1 9.0 16.1 26.2 12.0 11.3 8.9 15.1 22.6 9.9 10.2 9.7 21.0 42.8 21.2 Average Federal Tax 6 Rate Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law plus a permanent AMT patch at 2009 levels, indexed for inflation; extension of low- and middle-income tax cuts (extend the 10, 25, and 28 percent rates; set the standard deduction and and 15 percent tax brackets for couples filing jointly to double those for singles; raise the EITC phaseout threshold for couples filing jointly; and extend expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC); taxation of qualified dividends the same as long-term capital gains; reduced tax rates on long-term capital gains (0 percent for tax units in 15 percent bracket or lower, 15 percent for tax units in tax brackets above 15 percent); repeal of the personal exemption phaseout (PEP) and limitation on itemized deductions (Pease); extension of the 33 and 35 perc tax brackets. Policy is an estate tax set at the 2009 level, not indexed for inflation ($3.5 million exemption, 45 percent tax rate). (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,219, 40% $24,782, 60% $41,864, 80% $68,188, 90% $97,830, 95% $138,709, 99% $361,983, 99.9% $1,670,467. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.