Option 3: Replace the Mortgage Interest Deduction with a 15... Baseline: Current Law

advertisement

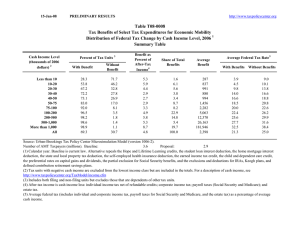

14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Summary Table Expanded Cash Income Level (thousands of 2015 dollars) 2 Tax Units with Tax Increase or Cut 3 With Tax Cut Pct of Tax Units Avg Tax Cut With Tax Increase Avg Tax Pct of Tax Units Increase Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All * 1.1 3.0 9.1 16.2 24.7 35.0 31.5 7.9 3.4 6.2 14.8 ** -189 -257 -272 -303 -326 -432 -512 -554 -729 -1,624 -414 0.0 0.0 0.2 0.7 1.2 5.4 13.0 30.3 69.2 74.0 57.5 11.9 0 0 312 330 388 432 619 841 1,884 3,805 5,568 1,385 0.0 0.0 0.0 0.1 0.1 0.1 0.1 -0.1 -0.6 -0.6 -0.2 -0.2 0.0 -0.3 -0.9 -2.0 -3.3 -7.6 -6.3 14.4 73.1 20.6 12.3 100.0 0 -2 -7 -22 -44 -57 -71 94 1,260 2,792 3,103 103 0.0 0.0 0.0 -0.1 -0.1 -0.1 -0.1 0.1 0.4 0.4 0.1 0.1 7.6 3.5 5.5 8.8 11.4 13.7 16.3 19.2 23.9 29.0 34.9 20.5 Addendum 100-125 125-150 150-175 175-200 38.6 32.7 24.3 18.5 -516 -512 -489 -522 15.7 29.1 44.4 55.2 736 732 869 1,009 0.1 0.0 -0.2 -0.3 -5.1 1.9 7.8 9.8 -84 46 266 460 -0.1 0.0 0.2 0.2 17.6 18.8 20.1 21.3 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). Number of AMT Taxpayers (millions). Baseline: 4.3 Proposal: 4.9 * Less than 0.05 ** Insufficient data (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate taxes; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table Expanded Cash Income Level (thousands of 2015 dollars) 2 Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All * 1.1 3.0 9.1 16.2 24.7 35.0 31.5 7.9 3.4 6.2 14.8 0.0 0.0 0.2 0.7 1.2 5.4 13.0 30.3 69.2 74.0 57.5 11.9 0.0 0.0 0.0 0.1 0.1 0.1 0.1 -0.1 -0.6 -0.6 -0.2 -0.2 0.0 -0.3 -0.9 -2.0 -3.3 -7.6 -6.3 14.4 73.1 20.6 12.3 100.0 0 -2 -7 -22 -44 -57 -71 94 1,260 2,792 3,103 103 0.0 -0.4 -0.5 -0.7 -0.8 -0.7 -0.5 0.4 1.9 1.4 0.3 0.6 0.0 0.0 0.0 0.0 0.0 -0.1 -0.1 -0.1 0.3 0.1 -0.1 0.0 0.2 0.5 1.0 1.6 2.2 6.6 7.5 24.0 23.2 8.5 24.5 100.0 0.0 0.0 0.0 -0.1 -0.1 -0.1 -0.1 0.1 0.4 0.4 0.1 0.1 7.6 3.5 5.5 8.8 11.4 13.7 16.3 19.2 23.9 29.0 34.9 20.5 Addendum 100-125 125-150 150-175 175-200 38.6 32.7 24.3 18.5 15.7 29.1 44.4 55.2 0.1 0.0 -0.2 -0.3 -5.1 1.9 7.8 9.8 -84 46 266 460 -0.4 0.2 0.8 1.2 -0.1 0.0 0.0 0.0 7.1 6.4 5.6 5.0 -0.1 0.0 0.2 0.2 17.6 18.8 20.1 21.3 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Addendum 100-125 125-150 150-175 175-200 Tax Units Number (thousands) Percent of Total 14,724 26,039 21,906 16,072 13,205 23,789 15,880 27,265 10,362 1,317 705 ########### 8.5 15.1 12.7 9.3 7.7 13.8 9.2 15.8 6.0 0.8 0.4 ########## 10,817 7,442 5,221 3,785 6.3 4.3 3.0 2.2 Pre-Tax Income Federal Tax Burden Average (dollars) Percent of Total Average (dollars) 5,753 15,359 25,245 35,565 45,784 62,910 88,631 141,622 288,418 686,585 3,064,525 86,987 0.6 2.7 3.7 3.8 4.0 10.0 9.4 25.7 19.9 6.0 14.4 100.0 439 539 1,382 3,153 5,244 8,655 14,527 27,050 67,569 195,971 1,066,076 17,747 114,131 139,840 165,502 190,750 8.2 6.9 5.8 4.8 20,177 26,253 32,982 40,076 Percent of Total After-Tax Income 4 Average Federal Tax Rate 5 Average (dollars) Percent of Total 0.2 0.5 1.0 1.7 2.3 6.7 7.5 24.1 22.9 8.4 24.6 100.0 5,313 14,820 23,863 32,412 40,540 54,255 74,103 114,572 220,849 490,614 1,998,449 69,241 0.7 3.2 4.4 4.4 4.5 10.8 9.9 26.2 19.2 5.4 11.8 100.0 7.6 3.5 5.5 8.9 11.5 13.8 16.4 19.1 23.4 28.5 34.8 20.4 7.1 6.4 5.6 5.0 93,954 113,586 132,520 150,674 8.5 7.1 5.8 4.8 17.7 18.8 19.9 21.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). Number of AMT Taxpayers (millions). Baseline: 4.3 Proposal: 4.9 * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Non-refundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table - Single Tax Units Expanded Cash Income Level (thousands of 2015 2 dollars) Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax 4 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All * 1.2 3.6 11.1 19.6 24.0 18.9 8.2 1.7 2.2 6.0 8.4 0.0 0.0 * * 0.1 7.5 26.9 40.0 53.4 55.2 40.3 5.8 0.0 0.0 0.0 0.1 0.1 0.1 -0.2 -0.3 -0.6 -0.4 -0.1 -0.1 0.0 -1.6 -4.4 -9.7 -13.9 -10.3 24.8 62.5 39.3 7.8 5.5 100.0 0 -2 -9 -30 -55 -27 131 346 1,144 2,011 1,904 33 0.0 -0.2 -0.4 -0.7 -0.8 -0.3 0.7 1.2 1.6 0.9 0.2 0.4 0.0 0.0 0.0 -0.1 -0.1 -0.1 0.1 0.2 0.1 0.0 0.0 0.0 1.0 2.7 4.5 5.5 6.7 16.3 13.6 21.9 10.3 3.5 13.8 100.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.2 0.3 0.4 0.3 0.1 0.1 9.5 6.4 9.1 12.2 14.4 17.2 20.5 22.6 27.1 32.5 37.7 18.6 Addendum 100-125 125-150 150-175 175-200 10.9 7.2 3.7 1.9 36.7 42.3 44.3 47.1 -0.3 -0.3 -0.4 -0.5 24.5 17.1 10.8 10.1 260 366 447 640 1.1 1.2 1.2 1.4 0.1 0.1 0.0 0.0 9.3 5.9 3.7 3.0 0.2 0.3 0.3 0.3 21.6 22.6 23.2 25.1 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 2 dollars) Tax Units Pre-Tax Income Number (thousands) Percent of Total Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 12,809 20,058 14,163 9,258 7,373 10,972 5,479 5,238 994 112 83 87,180 14.7 23.0 16.3 10.6 8.5 12.6 6.3 6.0 1.1 0.1 0.1 ########## Addendum 100-125 125-150 150-175 175-200 2,728 1,353 700 457 3.1 1.6 0.8 0.5 Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax 5 Rate 5,712 15,217 25,106 35,513 45,789 62,354 87,830 133,711 276,795 694,692 3,180,472 44,584 1.9 7.9 9.2 8.5 8.7 17.6 12.4 18.0 7.1 2.0 6.8 100.0 540 971 2,305 4,363 6,653 10,769 17,880 29,832 73,900 223,500 1,197,912 8,266 1.0 2.7 4.5 5.6 6.8 16.4 13.6 21.7 10.2 3.5 13.8 100.0 5,171 14,246 22,801 31,150 39,137 51,585 69,951 103,878 202,896 471,193 1,982,560 36,317 2.1 9.0 10.2 9.1 9.1 17.9 12.1 17.2 6.4 1.7 5.2 100.0 9.5 6.4 9.2 12.3 14.5 17.3 20.4 22.3 26.7 32.2 37.7 18.5 113,538 139,393 164,372 190,329 8.0 4.9 3.0 2.2 24,278 31,137 37,722 47,032 9.2 5.9 3.7 3.0 89,259 108,256 126,650 143,297 7.7 4.6 2.8 2.1 21.4 22.3 23.0 24.7 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table - Married Tax Units Filing Jointly Expanded Cash Income Level (thousands of 2015 2 dollars) Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax 4 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 0.0 0.0 1.1 3.9 9.1 26.6 46.5 39.5 8.7 3.5 6.1 25.4 0.0 0.0 * 1.0 2.4 3.0 2.3 26.2 71.0 76.4 60.6 22.9 0.0 0.0 0.0 0.0 0.1 0.2 0.3 0.0 -0.6 -0.6 -0.2 -0.2 0.0 0.0 -0.1 -0.1 -0.4 -5.2 -12.4 -0.6 81.0 23.9 13.9 100.0 0 0 -3 -7 -21 -93 -221 -4 1,264 2,890 3,306 242 0.0 0.0 -1.2 -0.5 -0.7 -1.5 -1.8 0.0 1.9 1.5 0.3 0.7 0.0 0.0 0.0 0.0 0.0 -0.1 -0.1 -0.2 0.4 0.1 -0.1 0.0 0.0 0.0 0.0 0.2 0.4 2.3 4.5 24.3 28.8 10.7 28.5 100.0 0.0 0.0 0.0 0.0 -0.1 -0.2 -0.3 0.0 0.4 0.4 0.1 0.2 2.3 1.0 0.9 3.8 6.8 9.9 13.6 18.2 23.5 28.6 34.4 22.3 Addendum 100-125 125-150 150-175 175-200 53.1 40.7 29.2 21.7 3.6 24.3 43.5 56.0 0.3 0.1 -0.2 -0.3 -13.4 -2.6 6.1 9.4 -275 -68 204 419 -1.5 -0.3 0.6 1.1 -0.1 -0.1 0.0 0.0 5.8 6.4 6.3 5.8 -0.2 -0.1 0.1 0.2 15.8 17.7 19.4 20.6 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 2 dollars) Tax Units Number (thousands) Percent of Total Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 825 1,902 2,948 2,940 2,904 7,878 7,909 19,667 9,043 1,165 594 58,288 1.4 3.3 5.1 5.0 5.0 13.5 13.6 33.7 15.5 2.0 1.0 ########## Addendum 100-125 125-150 150-175 175-200 6,866 5,469 4,179 3,153 11.8 9.4 7.2 5.4 Pre-Tax Income Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax 5 Rate 4,990 15,969 25,619 35,768 45,927 63,892 89,407 144,686 290,037 685,362 2,981,946 164,217 0.0 0.3 0.8 1.1 1.4 5.3 7.4 29.7 27.4 8.3 18.5 100.0 114 165 243 1,355 3,124 6,395 12,363 26,354 66,806 192,911 1,023,566 36,401 0.0 0.0 0.0 0.2 0.4 2.4 4.6 24.4 28.5 10.6 28.6 100.0 4,876 15,804 25,376 34,412 42,803 57,497 77,045 118,332 223,232 492,451 1,958,379 127,815 0.1 0.4 1.0 1.4 1.7 6.1 8.2 31.2 27.1 7.7 15.6 100.0 2.3 1.0 1.0 3.8 6.8 10.0 13.8 18.2 23.0 28.2 34.3 22.2 114,485 140,013 165,610 190,822 8.2 8.0 7.2 6.3 18,380 24,883 31,928 38,878 6.0 6.4 6.3 5.8 96,105 115,131 133,681 151,944 8.9 8.5 7.5 6.4 16.1 17.8 19.3 20.4 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table - Head of Household Tax Units Expanded Cash Income Level (thousands of 2015 2 dollars) Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax 4 Income Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 0.0 0.1 1.3 5.5 12.2 21.7 33.7 18.1 4.5 4.8 7.3 10.8 0.0 0.0 0.7 2.3 2.8 3.1 13.2 41.5 68.6 64.3 55.0 6.7 0.0 0.0 0.0 0.0 0.1 0.1 0.1 -0.3 -0.7 -0.5 -0.1 -0.1 0.0 -0.1 -1.7 -5.4 -17.3 -59.9 -25.0 118.4 71.3 11.1 8.6 100.0 0 0 -2 -8 -34 -71 -59 314 1,429 2,403 3,162 21 0.0 0.0 0.2 -0.7 -1.0 -1.0 -0.4 1.2 2.2 1.2 0.2 0.3 0.0 0.0 0.0 0.0 -0.1 -0.3 -0.2 0.3 0.2 0.0 0.0 0.0 -0.4 -4.1 -2.9 2.7 5.6 19.8 19.0 33.2 11.4 3.3 12.4 100.0 0.0 0.0 0.0 0.0 -0.1 -0.1 -0.1 0.2 0.5 0.4 0.1 0.0 -10.2 -10.6 -3.9 3.3 7.2 11.1 15.2 19.6 24.7 30.1 34.8 11.9 Addendum 100-125 125-150 150-175 175-200 21.2 20.2 7.8 5.5 34.4 41.5 58.8 62.8 -0.2 -0.3 -0.5 -0.5 37.1 29.0 34.1 18.2 186 286 663 735 0.9 1.0 1.9 1.8 0.1 0.1 0.1 0.1 13.9 9.5 6.3 3.5 0.2 0.2 0.4 0.4 18.1 19.9 21.7 22.2 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 2 dollars) Tax Units Pre-Tax Income Number (thousands) Percent of Total Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 944 3,778 4,451 3,522 2,630 4,350 2,175 1,950 258 24 14 24,145 3.9 15.7 18.4 14.6 10.9 18.0 9.0 8.1 1.1 0.1 0.1 ########## Addendum 100-125 125-150 150-175 175-200 1,033 523 266 128 4.3 2.2 1.1 0.5 Average (dollars) Federal Tax Burden Percent of Total Average (dollars) Percent of Total After-Tax Income 4 Average (dollars) Percent of Total Average Federal Tax 5 Rate 6,963 15,795 25,430 35,527 45,596 62,486 87,734 132,812 274,070 693,999 3,840,137 53,332 0.5 4.6 8.8 9.7 9.3 21.1 14.8 20.1 5.5 1.3 4.2 100.0 -711 -1,677 -986 1,194 3,301 7,017 13,431 25,725 66,328 206,308 1,333,715 6,313 -0.4 -4.2 -2.9 2.8 5.7 20.0 19.2 32.9 11.2 3.2 12.4 100.0 7,674 17,473 26,416 34,333 42,295 55,469 74,303 107,087 207,742 487,692 2,506,422 47,020 0.6 5.8 10.4 10.7 9.8 21.3 14.2 18.4 4.7 1.0 3.1 100.0 -10.2 -10.6 -3.9 3.4 7.2 11.2 15.3 19.4 24.2 29.7 34.7 11.8 113,608 139,299 167,150 189,759 9.1 5.7 3.5 1.9 20,363 27,481 35,543 41,375 13.8 9.4 6.2 3.5 93,245 111,818 131,607 148,384 8.5 5.2 3.1 1.7 17.9 19.7 21.3 21.8 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table - Tax Units with Children Expanded Cash Income Level (thousands of 2015 dollars) 2 Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 0.0 0.0 0.4 3.1 9.3 19.1 38.7 37.0 7.5 3.6 6.4 17.2 0.0 0.0 0.7 2.6 4.2 5.7 9.0 32.7 79.8 83.3 67.7 20.0 0.0 0.0 0.0 0.0 0.0 0.1 0.2 -0.1 -0.7 -0.7 -0.2 -0.2 0.0 0.0 0.0 0.0 -0.6 -3.3 -6.7 7.4 70.9 20.4 11.8 100.0 0 0 0 1 -18 -54 -151 74 1,568 3,358 3,873 233 0.0 0.0 0.0 0.1 -0.6 -0.8 -1.2 0.3 2.3 1.7 0.4 0.9 0.0 0.0 0.0 0.0 0.0 -0.1 -0.1 -0.2 0.4 0.1 -0.2 0.0 -0.1 -0.7 -0.5 0.2 0.8 3.6 5.1 23.6 28.3 10.8 28.6 100.0 0.0 0.0 0.0 0.0 0.0 -0.1 -0.2 0.1 0.5 0.5 0.1 0.2 -11.8 -11.5 -4.8 2.0 6.3 10.6 14.2 18.2 23.6 28.9 34.6 20.8 Addendum 100-125 125-150 150-175 175-200 47.9 41.0 26.9 18.7 11.3 27.6 52.0 63.9 0.2 0.0 -0.2 -0.4 -7.0 -1.4 6.8 9.0 -200 -51 326 576 -1.1 -0.2 1.0 1.5 -0.1 -0.1 0.0 0.0 5.9 6.2 6.1 5.5 -0.2 0.0 0.2 0.3 16.1 17.5 19.4 20.4 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 dollars) 2 Tax Units Number (thousands) Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 1,246 4,675 5,672 4,492 3,628 7,050 5,198 11,657 5,301 712 357 50,272 Addendum 100-125 125-150 150-175 175-200 4,112 3,266 2,443 1,835 Percent of Total 2.5 9.3 11.3 8.9 7.2 14.0 10.3 23.2 10.5 1.4 0.7 ########## 8.2 6.5 4.9 3.7 Pre-Tax Income Federal Tax Burden Average (dollars) Percent of Total Average (dollars) 6,635 15,763 25,471 35,564 45,644 63,024 89,122 144,292 293,122 683,288 2,994,529 123,886 0.1 1.2 2.3 2.6 2.7 7.1 7.4 27.0 25.0 7.8 17.2 100.0 -782 -1,818 -1,218 705 2,881 6,717 12,820 26,147 67,624 193,863 1,031,349 25,527 114,421 139,695 165,757 190,832 7.6 7.3 6.5 5.6 18,656 24,519 31,758 38,360 Percent of Total After-Tax Income 4 Average Federal Tax Rate 5 Average (dollars) Percent of Total -0.1 -0.7 -0.5 0.3 0.8 3.7 5.2 23.8 27.9 10.8 28.7 100.0 7,417 17,580 26,689 34,858 42,763 56,307 76,302 118,145 225,498 489,425 1,963,181 98,359 0.2 1.7 3.1 3.2 3.1 8.0 8.0 27.9 24.2 7.0 14.2 100.0 -11.8 -11.5 -4.8 2.0 6.3 10.7 14.4 18.1 23.1 28.4 34.4 20.6 6.0 6.2 6.1 5.5 95,765 115,176 133,999 152,471 8.0 7.6 6.6 5.7 16.3 17.6 19.2 20.1 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income. 14-Dec-15 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T15-0225 Option 3: Replace the Mortgage Interest Deduction with a 15 Percent Nonrefundable Credit Baseline: Current Law Distribution of Federal Tax Change by Expanded Cash Income Level, 2016 ¹ Detail Table - Elderly Tax Units Expanded Cash Income Level (thousands of 2015 dollars) 2 Percent of Tax Units 3 With Tax cut With Tax Increase Percent Change in After-Tax Income 4 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate5 Change (% Points) Under the Proposal Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 0.2 0.8 3.0 8.8 19.0 31.3 41.4 32.1 10.3 3.2 5.9 15.9 0.0 0.0 0.0 * 0.1 2.0 5.5 17.0 46.0 61.3 45.7 5.2 0.0 0.0 0.0 0.1 0.1 0.1 0.2 0.0 -0.3 -0.4 -0.1 0.0 -0.1 -3.3 -11.4 -23.7 -38.0 -108.3 -107.5 -31.1 241.5 101.2 80.8 100.0 0 -2 -7 -24 -48 -79 -119 -26 672 1,969 2,176 10 -0.1 -0.7 -1.0 -1.5 -1.7 -1.5 -1.1 -0.1 1.0 1.0 0.2 0.1 0.0 0.0 0.0 0.0 0.0 -0.1 -0.1 0.0 0.2 0.1 0.0 0.0 0.0 0.4 0.8 1.2 1.7 5.6 7.5 21.6 18.5 8.2 34.1 100.0 0.0 0.0 0.0 -0.1 -0.1 -0.1 -0.1 0.0 0.2 0.3 0.1 0.0 2.4 1.7 2.8 4.4 6.0 8.5 12.3 17.0 23.6 29.3 35.9 17.8 Addendum 100-125 125-150 150-175 175-200 39.7 30.0 22.9 21.6 8.0 18.8 26.3 33.9 0.1 0.0 -0.1 -0.1 -60.7 -6.5 16.5 19.6 -114 -20 79 144 -0.7 -0.1 0.3 0.4 -0.1 0.0 0.0 0.0 6.8 6.0 4.8 4.0 -0.1 0.0 0.1 0.1 14.6 17.2 18.3 20.3 Baseline Distribution of Income and Federal Taxes by Expanded Cash Income Level, 2016 ¹ Expanded Cash Income Level (thousands of 2015 dollars) 2 Tax Units Number (thousands) Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All 1,889 7,909 6,516 4,256 3,361 5,868 3,871 5,135 1,539 220 159 41,164 Addendum 100-125 125-150 150-175 175-200 2,270 1,390 893 582 Percent of Total 4.6 19.2 15.8 10.3 8.2 14.3 9.4 12.5 3.7 0.5 0.4 ########## 5.5 3.4 2.2 1.4 Pre-Tax Income Federal Tax Burden Average (dollars) Percent of Total Average (dollars) 5,514 15,610 25,150 35,561 45,754 62,781 88,361 138,547 285,155 710,712 3,339,288 76,347 0.3 3.9 5.2 4.8 4.9 11.7 10.9 22.6 14.0 5.0 16.9 100.0 131 265 721 1,580 2,786 5,408 10,948 23,509 66,530 206,407 1,195,134 13,565 114,026 139,736 164,995 190,799 8.2 6.2 4.7 3.5 16,786 24,020 30,040 38,497 Percent of Total After-Tax Income 4 Average Federal Tax Rate 5 Average (dollars) Percent of Total 0.0 0.4 0.8 1.2 1.7 5.7 7.6 21.6 18.3 8.1 34.0 100.0 5,383 15,344 24,429 33,981 42,968 57,373 77,413 115,038 218,625 504,305 2,144,154 62,782 0.4 4.7 6.2 5.6 5.6 13.0 11.6 22.9 13.0 4.3 13.2 100.0 2.4 1.7 2.9 4.4 6.1 8.6 12.4 17.0 23.3 29.0 35.8 17.8 6.8 6.0 4.8 4.0 97,240 115,716 134,956 152,301 8.5 6.2 4.7 3.4 14.7 17.2 18.2 20.2 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0515-3). * Less than 0.05 Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law. Proposal would replace the deduction for mortgage interest with a 15 percent non-refundable credit subject to current law limits ($1,000,000 of debt on a primary residence or second home, and $100,000 in home equity loans). Estimates are static and do not assume that taxpayers would adjust their investment portfolio and pay down their mortgage balance if their tax benefit from mortgage interest was reduced. For a description of TPC’s current law baseline, see http://www.taxpolicycenter.org/taxtopics/Baseline-Definitions.cfm (2) Includes both filing and non-filing units but excludes those that are dependents of other tax units. Tax units with negative adjusted gross income are excluded from their respective income class but are included in the totals. For a description of expanded cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes tax units with a change in federal tax burden of $10 or more in absolute value. (4) After-tax income is expanded cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); estate tax; and excise taxes. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, the estate tax, and excise taxes) as a percentage of average expanded cash income.