Chapter 4 Completing the Accounting Cycle

advertisement

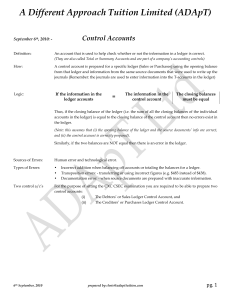

Chapter 4 Completing the Accounting Cycle • The accounting cycle is repeated each accounting period. The goal of the cycle is the financial statements. • The accounting cycle includes work performed at two different times: • During the period journalizing transactions Posting to the ledger • End of the period adjusting the accounts Closing the accounts Preparing financial statements The work sheet is an optional tool that accountants use in the adjusting and closing process. 1. Start with ledger balances 2. Analyze & journalize transactions 7. Post-closing Trial Balance 6. Journalize & post adjusting & closing entries 3. Post to the ledger 4. Unadjusted trial balance 5. Work sheet (optional) Financial Statements ILLUSTRATION WORK SHEET Account Titles Trial Balance Debit Credit 1. Prepare trial balance on the worksheet. Adjustments Debit Credit 2. Enter adjustment data. Adjusted Trial Balance Debit Credit 3. Enter adjusted balances Income Statement Debit Credit Balance Sheet Debit Credit 4. Extend adjusted balance to appropriate columns. 5. Calculate income/loss and complete the worksheet. Closing the Accounts At the end of the fiscal period, we must prepare the accounts for recording the transactions for the next period. Nominal (temporary) accounts are closed each fiscal period. These include Revenue, Expenses, Drawings. Real (permanent) accounts are NOT closed. These include Assets, Liabilities and Capital. 3 Steps to Closing Accounts 1. Transfer the sum of the Revenues to Capital. DR. Revenue CR. Capital 2. Transfer the sum of the Expenses to Capital. DR. Capital CR. Amortization Expense CR. Salary Expense 3. Transfer the Drawings to Capital. DR. Capital CR. Drawings