Schroders Portfolio Solutions Monthly

advertisement

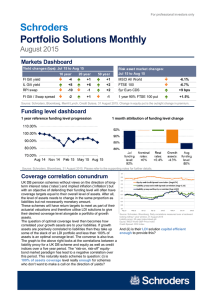

Portfolio Solutions Monthly July 2015 For professional investors only Schroders Portfolio Solutions Monthly July 2015 Markets dashboard Yield changes (bps): Jun 15 to Jul 15 10 year 20 year 50 year Risk asset market changes: Jun 15 to Jul 15 FI Gilt yield -15 -16 -18 MSCI All World +1.7% IL Gilt yield -5 -12 -15 FTSE 100 +2.7% RPI swap -8 -5 -3 5yr Euro CDS -13 bps FI Gilt / Swap spread -1 +1 -2 1 year 90% FTSE 100 put -0.4% Source: Schroders, Bloomberg, Merrill Lynch, Credit Suisse, 31 July 2015. Change in equity put is the outright change in premium. Funding level dashboard 1 year reference funding level progression 1 month attribution of funding level change Source: Schroders, Bloomberg, 31 July 2015. Please refer to the supporting notes for further details. Infrastructure UK (iUK) HM Treasury has made £40bn of funding available for certain projects via the Infrastructure UK (iUK) guarantee. It has provided guarantees to approximately £1.7bn of commitments, and has roughly 40 further projects in the pipeline. These include the Mersey Gateway Bridge (£257m), the Northern Line Extension (£750m), and the largest project, the Hinkley Point C nuclear reactor (£17bn) coming later this year. Bonds have so far been issued around gilts + 35-39bps, tightening to their current level of gilts + 32-35bps (1012bps wider than Network Rail bonds), with liquidity more robust at issuance than in the secondary market. These bonds may suit pension funds that seek higher yield and are comfortable with the potential illiquidity. Schroders is happy to work with clients to incorporate these bonds in our LDI portfolios where appropriate, and happy to discuss specific client situations. Contact us Please contact us at PortfolioSolutions@schroders.com if you would like further information on how Schroders can help manage your Scheme’s exposure to risk. Portfolio Solutions Monthly July 2015 For professional investors only Market data: LDI markets One year range •L H• Month end 31 Jul 2015 One Month 30 Jun 2015 Three Months 30 Apr 2015 One Year 31 Jul 2014 Month end curve (LHS): Nominal rates - Gilt markets 5 Year 1.45% 1.52% 1.34% 2.04% 10 Year 2.04% 2.19% 1.97% 2.82% 20 Year 2.63% 2.80% 2.58% 3.39% 30 Year 2.68% 2.86% 2.69% 3.48% 50 Year 2.45% 2.63% 2.53% 3.33% 1 Month change (RHS, Bps): 5.0% 60 2.5% 0 0 10 20 30 40 50 0.0% -60 Real rates - Index-linked gilt markets 2.0% 30 0.0% 0 5 Year -1.16% -1.22% -1.25% -0.94% 10 Year -0.85% -0.80% -0.91% -0.32% 20 Year -0.84% -0.72% -0.83% -0.11% 30 Year -0.84% -0.69% -0.83% -0.10% 50 Year -0.99% -0.84% -0.90% -0.14% 5 Year 2.89% 3.01% 2.89% 3.11% 10 Year 3.14% 3.22% 3.11% 3.25% 20 Year 3.45% 3.50% 3.46% 3.53% 30 Year 3.49% 3.52% 3.52% 3.57% 50 Year 3.50% 3.53% 3.55% 3.57% 5 Year -0.23% -0.21% -0.20% -0.18% 10 Year -0.02% -0.01% 0.02% 0.02% 20 Year 0.36% 0.35% 0.35% 0.19% 30 Year 0.45% 0.46% 0.42% 0.27% 50 Year 0.37% 0.39% 0.32% 0.18% 10 Year Bund 0.64% 0.76% 0.37% 1.16% 10 Yr Gilt / Bund Spread 1.23% 1.25% 1.46% 1.43% 10 Year US Treasury 2.18% 2.35% 2.03% 2.56% 10 Yr Gilt / US Spread -0.29% -0.32% -0.19% 0.04% 1.0% 5 year IG CDS - Euro 62 75 61 65 0.0% 5 year IG CDS - US 70 70 63 64 -2.0% -30 0 10 20 30 40 50 Inflation rates - RPI swap market 5.0% 40 2.5% 0 0.0% -40 0 10 20 30 40 50 Nominal gilt curve vs swap curve Global bond markets 0.5% 10 0.0% 0 -0.5% -10 0 10 20 30 40 50 Forward gilt curves 3.0% 2.0% Gilt curve 3 yrs fwd 0 Currency rates Money markets 10 1 yr fwd 5 yrs fwd 20 30 40 50 31 Jul 2015 30 Jun 2015 30 Apr 2015 31 Jul 2014 1.69 Bank of England base 0.50% 0.50% 0.50% 0.50% GBP / USD 1.56 1.57 1.53 SONIA 0.47% 0.46% 0.45% 0.45% GBP / EUR 1.42 1.41 1.37 1.26 3m Libor 0.58% 0.58% 0.57% 0.56% GBP / JPY 193.6 192.0 183.5 173.7 Interest rate swaptions as at month end: 1y20y 3y20y 5y20y 3y30y 5y30y ATM* Forward Par swap rate 2.31% 2.39% 2.39% 2.29% 2.29% ATM* Implied volatility 81.6 83.4 73.5 77.3 69.8 Source: Schroders, Bloomberg, 31 July 2015. *At the money. All data as at month end allowing for UK trading days. 2 Portfolio Solutions Monthly July 2015 For professional investors only Market data: Risk management strategies Month end 31 Jul 2015 One Month 30 Jun 2015 Three Months 30 Apr 2015 MSCI World 1,766 1,736 1,778 1,714 FTSE 100 6,696 6,521 6,961 6,730 One year range •L H• One Year 31 Jul 2014 Equity indices S&P 500 2,104 2,063 2,086 1,931 Euro Stoxx 50 3,601 3,424 3,616 3,116 Nikkei 225 20,585 20,236 19,520 15,621 15.6% 15.9% 13.6% 4.8% 4.7% 4.5% MSCI All World Total Return (re-based to 100) 120 100 80 Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Equity option market indicators (FTSE 100, 1 year) ATM* Implied volatility Skew (90 - 110) 13.7% 4.6% ATM implied 1 year volatility Skew (90 vol - 110 vol) 20.0% 6.0% 5.0% 15.0% 4.0% 10.0% Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 3.0% Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Equity risk management strategy indicators (FTSE 100 total return, spot prices) Zero cost put spread collar call strike (70% / 90%) 108.9% 90% Put Zero cost collar call strike (90% Put) 1 yr 2.9% 106.9% 3 yr 5.6% 113.6% 123.6% 95% Put Zero cost collar call strike (95% Put) Zero cost put spread collar call strike (70% / 95%) 1 yr 4.0% 104.4% 105.9% 3 yr 8.8% 110.2% 117.9% NB - one year range indicators for equity risk management strategies are based on month end values. Source: Schroders, Bloomberg, Merrill Lynch, Credit Suisse, 31 July 2015. *At the money. All data as at month end allowing for UK trading days. About us The Schroders Portfolio Solutions Team partners with investors to provide risk management strategies across all major financial markets. The team structures and executes physical and derivative based strategies to manage the exposure to global equity and fixed income markets. These solutions draw on the full opportunity set of exchange traded and Over-The-Counter derivatives. To help manage interest and inflation rate risk, Schroders Portfolio Solutions offers a comprehensive and fully flexible solution utilising segregated solutions (encompassing physical bonds, swaps, swaption and synthetic gilt based strategies), as well as the Schroder Matching Plus pooled fund solution. We also provide funding level and market based trigger monitoring and execution for both pooled and segregated solutions. Clients can access these solutions under directed or discretionary mandates. 3 Portfolio Solutions Monthly July 2015 For professional investors only Notes The funding level dashboard shows the funding level progression and attribution of funding level change of a Reference Pension Scheme. This Reference Pension Scheme has a liability duration of around 20 years and assumes the liability is linked 50% to real interest rates and 50% to nominal rates. The assets are assumed to have a beta of 0.75 to global equity markets. This enables the reader to observe the scale of component changes. No allowance for the impact of the progression of time on liabilities is included in the funding level dashboard. Funding level progression is presented on a rolling 12 month basis, indexed to an initial funding level of 100%. Important Information For professional investors only. The views and opinions contained herein are those of the Portfolio Solutions Team at Schroders, and do not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This newsletter is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Limited (SIM) does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. The forecasts stated in the newsletter are the result of statistical modelling, based on a number of assumptions. Forecasts are subject to a high level of uncertainty regarding future economic and market factors that may affect actual future performance. The forecasts are provided to you for information purposes as at today's date. Our assumptions may change materially with changes in underlying assumptions that may occur, among other things, as economic and market conditions change. We assume no obligation to provide you with updates or changes to this data as assumptions, economic and market conditions, models or other matters change. For your security, communications may be taped or monitored. Issued in August 2015 by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority. 4