& Venue Event Management

advertisement

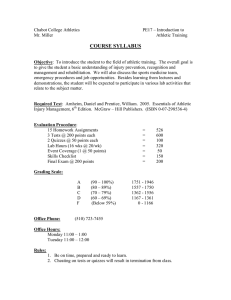

OF Editor: Mark S. Nagel University of South Carolina Associate Editor: John M. Grady University of South Carolina Venue Event Management JOURNAL Editorial Board and Staff: & Consulting Editor: Peter J. Graham University of South Carolina Editorial Review Board Members: Rob Ammon—University of South Dakota John Benett—Venue Management Association, Asia Pacific Limited Chris Bigelow—The Bigelow Companies, Inc. Matt Brown—University of South Carolina Brad Gessner—San Diego Convention Center Peter Gruber —Wiener Stadthalle, Austria Todd Hall—Georgia Southern University Kim Mahoney—Industry Consultant Michael Mahoney—California State University at Fresno Larry Perkins—RBC Center Carolina Hurricanes Jim Riordan—Florida Atlantic University Frank Roach—University of South Carolina Philip Rothschild—Missouri State University Frank Russo—Global Spectrum Rodney J. Smith—University of Denver Kenneth C. Teed—The George Washington University Scott Wysong—University of Dallas Who is in charge? An analysis of NCAA Division I Arena Management Models Mauro Palmero—East Tennessee State University Ming Li—Ohio University Heather Lawrence—Ohio University Valerie Martin Conley—Ohio University Abstract Financial accountability pressures in higher education force athletic departments to closely examine their expenditures to ensure that cost-efficient managerial approaches are used in all facets of operations, including facility management. Five distinct management models are currently used by intercollegiate athletic departments to manage arenas hosting National Collegiate Athletic Association (NCAA) Division I men’s basketball competitions (Palmero, Li & Lawrence, 2010). Little research is available to help athletic administrators understand each of the models and determine which model would provide them with the most benefits when contemplating whether or not they should change the management model utilized in operating their arenas. The purpose of this study was to fill this gap in the public assembly facility management literature and to assist athletic directors in choosing the most cost-effective arena operations model possible. The results indicated that the following factors should be taken into consideration when making the decision to adopt a certain arena management model: overall satisfaction, venue management and control, revenue and costs, venue characteristics, university policy, transfer of risks, and enrollment. Who is in charge? An analysis of NCAA Division I Arena Management Models Introduction Higher education budgets have decreased noticeably in the last decade (Ehrenberg, 2006; Lee & Clery, 2004; Zumeta, 2009). The trickle-down effects of these budget cuts are impacting many areas of institutional operations, including athletics. Intercollegiate athletics operations are especially vulnerable since they are sometimes not seen as a core function of the institution. This scrutiny often demands athletic departments to closely examine expenditures to ensure cost-efficient managerial approaches are used in all facets of operations. Athletic facility management is no exception. The most common strategies athletic departments utilize to try to ensure financial accountability associated with facility management are: 1) turn the facilities into auxiliary enterprises, 2) outsource the entire facilities’ operations, and 3) outsource selected facility services (i.e. concessions, security, and venue booking) (Burden & Li, 2005). The athletic director is commonly the final decision maker responsible for choosing the appropriate management model for all aspects of athletics’ operations. As leaders of the department most directly benefitting from the usage of arenas, athletic directors are influential in the decision regarding the facility management model that best fits their needs (Seidler, Gerdy Journal of Venue and Entertainment Management, Vol. 3, Issue 2 & Cardinal, 1998). Their knowledge of the different management models and their perception of the models’ advantages and disadvantages are crucial factors in the decision to utilize (or not utilize) a certain management model (Li & Burden, 2002). A study conducted by Palmero et al. (2010) found that five distinct management models (i.e., operated by athletic department, operated by other university departments, operated as an auxiliary enterprise, operated by private management, operated by government) are currently used in NCAA Division I arena operations. Operated by the athletic department and operated by other university departments are arena management models in which the respective department responsible for the venue has complete control and decision making power over the venue. Operated as an auxiliary enterprise is a model in which the venue is an independent, financially self-sufficient unit of the institution. Operated by private management is the model in which a private management company specializing in one or more area of facility operations allows the institution/ athletic department to retain all rights while the management company provides a vast array of specialized services in exchange for a fee or shared revenue. Operated by government is a model in which local (city and county) or state government operates the venue and negotiates use by a college athletic department as a tenant (Palmero et al, 2010). 18 Even with existing management models identified, the literature lacks specific guidance for venue managers and academics alike regarding how to select a management model that is a good fit for their venue. This study sought to fill this void in the literature by using a two-part approach to the investigation. First, an empirical approach was used to address three specific research questions that determined the factors related to choice of arena management model by facility managers. Then, the authors conceptualized a decisionmaking framework grounded in the empirical results. As an outcome, the study adds to the academic body of knowledge in the area as well as provides practical guidance to professionals in higher education and sport facility management about how a facility manager can select an arena management model in intercollegiate athletics. Specifically, the three empirical research questions were: 1. What are the reasons perceived by NCAA Division I athletic directors for adopting different arena management models? 2. What are the common constructs that can be extracted from the reasons perceived by the surveyed NCAA Division I athletic directors and their levels of satisfaction towards the adopted arena management model? 3. Are there any components that differentiate the perceptions between the athletic directors from institutions that adopted the traditional arena management models and the athletic directors from institutions that adopted the emerging management models, at the NCAA Division I level? Results are valuable to those in leadership positions associated with NCAA Division I university administration, university venue management and intercollegiate athletics. Athletic directors armed with this information will be able to make informed decisions that allow them to (a) adapt to reduced financial resources, (b) contain costs, (c) acquire expertise, (d) free resources to be utilized in core functions, (e) show accountability to various stakeholders (internal and external), and (f) achieve self-sufficiency. Other benefits to institutional leaders include the ability to demonstrate accountability to stakeholders and to provide justification for decisions regarding the selected facility management model. Journal of Venue and Entertainment Management, Vol. 3, Issue 2 Review of Literature There are only a few studies that examine issues related to intercollegiate athletics venue management in the sport management literature. To form a theoretical foundation for the current study, literature in the areas of escalating costs in intercollegiate athletics, fiscal accountability in higher education, cost containment in intercollegiate athletics, and the management of intercollegiate athletic arenas was examined. Escalating Costs in Intercollegiate Athletics In NCAA Division I athletics, very few athletic departments are profitable and financially independent from institutional resources (Brown, Rascher, Nagel, & McEvoy, 2010; Fulks, 2011; Sperber, 1990; 2000). A large number of athletic departments depend heavily on institutional subsidies to cover departmental expenses and pay for the operational costs of athletic facilities (Brown et al.; Penry, 2008; Sperber, 1990; 2000). The most recent NCAA Division I Revenues and Expenses Report (Fulks, 2011) provided evidence of a growing financial crisis in Division I intercollegiate athletics. The report (Fulks, 2011) indicated that 22 out of 330 athletics programs reported positive net revenues for the 2010 fiscal year, which represents an increase from 14 reported in 2009, and a decrease from 25 reported in 2008 and 2007. In 2010, athletic departments playing in the Football Bowl Subdivision (i.e., institutions sponsoring football in a division considered highly competitive, commonly requiring substantial financial investments, and featuring the Bowl Championship Series to determine the champion) received an average of 20% of their revenues from their institution (Fulks, 2011). During the same period, revenues received from the institution accounted for 71% of the revenues received by athletic departments competing in the Football Championship Subdivision (i.e., institutions sponsoring football in a division featuring less financial investment and a playoff to determine the champion). The rest of the Division I athletic departments (i.e., those institutions that do not sponsor football) received 76% of their revenues from their institutions (Fulks, 2011). In 2007, this lack of self-sufficiency translated into $8.2 million dollars (on average) in annual financial burden to NCAA Division I institutions (Zimbalist, 2007). Four years later, the NCAA Division I Revenues and Expenses Report data does not show any significant reduction in the institutions’ financial contribution to their athletic departments (Fulks, 2011). 19 Fiscal Accountability in Intercollegiate Athletics Intercollegiate Athletics Arenas As a microcosm of its institution, an athletic department is exposed to the same accountability and financial pressures as the institution (Burden & Li, 2005; Li & Burden, 2002; Penry, 2008). As a result, many athletic departments have their own budget and pay their share of administrative and direct operating expenses (including debt service and provisions for renewal or replacement of venues). They are also expected to be self-sufficient by becoming auxiliary enterprises and outsourcing functions that are not core activities (Burden & Li, 2005; Li & Burden, 2002; Penry, 2008). These organizational pressures co-exist with the expectation of producing winning athletic teams. Many athletic departments in the Football Bowl Subdivision spend a considerable amount of funds each year hoping to produce winning teams. According to Fulks (2011), the median budget of athletic departments in the Football Bowl Subdivision exceeds $45 million. Such large operating expenses often prevent athletic departments from meeting the institution’s financial expectations (Brown et al., 2010; Sperber, 1990; 2000; Zimbalist, 2007). Athletic venues are one way in which the institution is publically identified because they are often large, prominent, and imposing physical structures. Plus, the community often attends events and identifies collegiate basketball arenas as their “home court”. Arenas are utilized not only as spaces to host intercollegiate athletic competitions, but also to attract quality prospective student-athletes, expose sponsors’ brand/ products, inspire donors to contribute and, consequently, provide athletics with vital financial resources (Jewell, 1992; 1998; Russo et al., 2009). Arenas are also typically unaffected by weather conditions. This allows arenas not only to host core events (e.g., basketball, volleyball, and hockey), but also a wide range of other events (e.g., indoor track, wrestling, volleyball, gymnastics, concerts, trade shows, and graduations) (Jewell, 1992; 1998; Russo et al., 2009). In addition to ticket sales, other events offer tremendous opportunities to generate revenues from space rentals, advertisements, concessions, premium seating, novelties, and food/beverage sales (Jewell, 1992; 1998; Russo et al. 2009). In an effort to appease stakeholders, athletic directors are often expected to stretch existing dollars, contain and cut costs, produce additional revenues, and generate competitive programs (Penry, 2008). To comply with institutional demands, athletic directors must go beyond department-wide cost containment measures and manage all athletic department units and all sources of revenue the athletic department has access to more efficiently. Along with revenue generation and intangible benefits for the athletic department, arenas also have expenses related to their operations. As such, both sides of the budget must be managed properly for the venue to achieve profitability and self-sufficiency (Ammon, Southall, & Nagel, 2010; Brown et al., 2010; Jewell, 1992; 1998; Russo et al., 2009; Steinbach, 2004). Expenditures incurred from the use of arenas include: salaries, employee benefits, debt service, sponsor activation, and facilities operation and maintenance (Ammon et al., 2010; Brown et al., 2010; Jewell, 1992; 1998; Russo et al., 2009; Steinbach, 2004). When an arena achieves a positive financial income statement, it has the potential to support other programs and services within the athletic department, fund scholarships, and reduce the athletic department’s dependence on institutional subsidies (Ammon et al., 2010; Brown et al., 2010; Russo et al., 2009; Shindell, 1993). At many institutions, a large part of the athletic department’s revenue comes from ticket sales (Denhart, Villwock, & Vedder, 2009; Fulks, 2011). Together with cash/alumni contributions, those two sources of revenue account for more than 50% of the total revenue generated from the athletic departments’ operations (Denhart et al., 2009; Fulks, 2011). Often, a desire to increase generated revenues is the main reason why schools build large stadiums (Denhart et al., 2009; Fulks, 2011). Based on such circumstances, it is logical to simultaneously focus on maximizing revenues and reducing operational costs of intercollegiate athletic facilities. These large amounts of revenue and expenses related to the management of intercollegiate athletic venues make the leadership role of athletic directors essential to the financial success of both the facilities and the athletic departments. Journal of Venue and Entertainment Management, Vol. 3, Issue 2 Arena Management Models As mentioned previously, a limited amount of research has been done on arena management models. The most well-known study by Bankhead (1975) which focused on large multi-purpose intercollegiate athletic arenas and their administrative policies and procedures is now 36 years old. The study described administrative policies and procedures for 52 large multi-purpose university arenas. Bankhead (1975) found that a ma20 jority of the arenas were operated either by the athletic department or the university business office. Since that time, many aspects of facility management have changed and different management options have been implemented (i.e., auxiliary enterprises and private management). Since the Bankhead (1975) investigation, new arena management models, such as arenas becoming university auxiliary enterprises or being managed by private companies, have emerged. A study conducted by Palmero et al. (2010) sought to identify the current management models used in NCAA Division I intercollegiate athletics arena management and, as a result, five distinct management models were identified. They are: management by the athletic department, management by other university department, management as an auxiliary enterprise, management by an outside enterprise (private management), and management by government (Palmero et al.). Other scholars have also provided categories by which to identify management models such as being operated by their owners, by the primary tenant, by not-for-profit entities, or by private management companies (Ammon et al., 2010; Fried, 2010; Jewell, 1992; 1998; Mulrooney & Styles, 2004; Russo et al., 2009; Steinbach, 2004). The emergence of private venue management companies (i.e. Comcast Spectator, Global Spectrum, SMG, etc.) has changed the facility management industry in professional sport (Lawrence & Moberg, 2009). Specifically, private management companies allow the ownership (team, venue, or municipality) to retain all rights while the management company provides specific services (e.g., administration and finance, booking and scheduling, security, concessions, budget analysis, marketing and sales, operations and engineering, sponsorships, ticketing, or ancillary services) or the management of the entire venue (Fried, 2010; Global Spectrum, 2009; Graham & Ward, 2004; Lawrence & Moberg, 2009). Although private management is extremely common in professional sport, it has not gained the same market share in intercollegiate athletics (Ammon et al., 2010; Jewell, 1992; 1998; Palmero et al., 2010; Steinbach, 2004). A possible reason for such lack of presence of private management in intercollegiate athletics is that private management companies appear to prefer to operate arenas with larger seating capacities (Ammon et al., 2010; Jewell, 1992; 1998; Palmero et al., 2010; Steinbach, 2004). According to Palmero et al., a majority of the NCAA Division I arenas have seating capacities of 9,000 or less. By managing venues with Journal of Venue and Entertainment Management, Vol. 3, Issue 2 a high revenue generation potential, private management companies may obtain a reasonable profit margin (Ammon et al., 2010; Jewell, 1992; 1998; Palmero et al., 2010; Steinbach, 2004). Other possible reasons may be the athletic departments’ preference to retain full control over their arena’s operations or that the current model has not been evaluated or challenged to date. Effective management of arenas can help intercollegiate athletics become less of a financial burden to their institutions. Consequently, the management model used to operate its arena is an important item in an athletic department’s self-sufficiency equation. Regardless of the management type, the financial success of an arena depends on the ability of the management team to control each of the arena’s functions (e.g., operations, marketing, tickets, etc.) and to balance conflicting variables (e.g., time, space, monetary resources, staffing, stakeholders demands and expectations of the general public) (Ammon et al., 2010; Brown et al., 2010; Russo et al., 2009). The decision regarding which venue management model best fits facilities’ and athletic departments’ characteristics (and needs) depend on a variety of factors. Previously identified factors include the facility’s revenue potential, in-house expertise, institutional demand, common practices (the way it has always been done), timing and circumstances, and contractor availability (Jewell, 1992; 1998; Mulrooney & Styles, 2004; Russo et al., 2009). The combination of these factors can lead decision makers to choose varying management models to operate their facilities (Jewell, 1992; 1998; Mulrooney & Styles, 2004; Russo et al., 2009; Seidler et al., 1998). The literature review helped to frame and support the current study. More specifically, the literature justifies this research by exposing institutional and athletic department’s contemporary needs to explore alternative models of arena operation. Examining management models, and potentially making a change, can allow an athletic department to (a) adapt to reduced financial resources, (b) contain costs, (c) acquire expertise, (d) free resources to be utilized in other functions, (e) show accountability to various stakeholders (internal and external), and (f) achieve self-sufficiency. The results of the current study provide the empirical evidence needed to generate a decision-making framework containing the factors that should be considered by athletic administrators and university presidents before choosing to adopt, maintain, or replace a certain management model. 21 Methods Subjects Three hundred-thirty athletic directors working for NCAA Division I institutions that support men’s basketball were the subjects of this study. The current study did not include NCAA Division II and III arenas due to the fact that the basketball programs of Division II and III institutions usually do not draw significant attendance figures. Additionally, their operating budgets at these institutions are typically much smaller. The pressure to use the arena to generate additional revenue at the Division II or III level is much lower than that of Division I institutions (Fulks, 2011; NCAA, 2010). Because of these differences, it is difficult to compare them to their Division I counterparts. As leaders of the department benefitting from the usage of arenas, athletic directors have a strong influence on the decision regarding the facility management model that best fits their needs (Seidler et al., 1998). Their perception towards various management models is a crucial factor in the decision to utilize (or not) a certain management model (Li & Burden, 2002). Instrumentation A survey instrument was used in this cross-sectional, non-experimental investigation. Based on the literature review and feedback from experts in the field of sport and facilities management, a survey instrument was designed to address the research questions. The instrument was verified and improved through a panel of experts’ review and a pilot study. The panel of six experts in the field of sport and facility management was conveniently selected and was composed of one senior athletic administrator, two intercollegiate athletic facilities managers and three scholars in the field of sport management/arena management. The panel reviewed and rated the instrument’s face and content validity. Via email, they provided their feedback, by rating and commenting on the appropriateness of each question and the overall questionnaire. The reliability of the instrument was also tested. Because the study collected responses to different items on the same instrument at the same time, Cronbach’s Alpha coefficient was utilized. The reliability test yielded a Cronbach’s Alpha coefficient of .710, ensuring that the instrument was reliable for the measurement in this study. The survey was divided into four parts. Part one Journal of Venue and Entertainment Management, Vol. 3, Issue 2 asked the respondents to select the definition that best defines the type of arena management model they currently utilize. Part two asked respondents to rate their perceptions of a list of reasons for using their current arena management model. Part three asked respondents to rate their satisfaction with specific aspects of the adopted model and their overall satisfaction with their model. The ratings utilized a five-point Likert scale (ranging from 1- strongly disagree to 5- strongly agree; 1- highly dissatisfied to 5- highly satisfied). Finally, part four asked the respondents to provide demographic information about themselves and their institutions. Data Collection A letter explaining the purpose of the study and inviting respondents to participate in an online survey was mailed to 330 athletic directors working at NCAA Division I institutions that support men’s basketball (NCAA, 2010). Endorsements from the International Association of Assembly Managers (IAAM) (currently the International Association of Venue Managers, IAVM), the Ohio University Center for Sport Administration, and the Ohio University Center for Higher Education were also enclosed. A week later, an email was sent to the respondents with a link that directed them to the survey. Two weeks after the survey was made available, a second email was sent to nonrespondents to encourage them to participate. Due to the inadequate number of initial survey responses, the Center for Sport Administration at Ohio University then directly sent the same email to 46 alumni who are athletic directors. The final total number of survey responses was 114 (34.5%), with 105 complete and usable surveys. The total number of completed responses accounted for 31.8% of the total population of NCAA Division I athletic directors (N=330). To ensure that the responses of the final 46 athletic directors (who responded to the invitation from the Center for Sport Administration at Ohio University) did not unduly influence the results, a t-test was conducted to compare their responses to the other 59 respondents’. The results of the t-test presented no significant difference for all survey items, suggesting that the data from both groups were consistent. Data Analysis Procedures Descriptive statistics were used to quantify the distribution of the different management models among the population (Table 1). The same statistical method 22 was utilized to analyze perceived reasons for adopting and the level of satisfaction with a certain management model. Factor analysis was then conducted to identify common components or constructs that can be extracted from the items that represent the reasons and perceived level of satisfaction. Lastly, a discriminant analysis was conducted to differentiate the perceptions of those athletic programs using traditional arena management models from that of those using emerging management models in terms of a number of institutional variables. I arena management models, conducted in the mid1970’s (Bankhead, 1975) with a focus mainly on large multi-purpose intercollegiate athletic arenas and their administrative policies and procedures, found that the arenas investigated were operated either by the athletic department or other university departments. The second reason is that, since the 1970’s, some aspects of facility management have changed and new management options have emerged (i.e., auxiliary enterprises and private management) (Russo et al.; Steinbach). Another reason for the consolidation of the models was that The five management models previously mentioned (i.e., operated by athletic department, operated by other university departments, operated as an auxiliary enterprise, operated by private management, and operated by government) were then consolidated into traditional management (athletic department and other university department) and emergent management (auxiliary enterprises, private management, and government) categories. Such consolidation was done due to a number of reasons. The first reason is the fact that athletic departments and other university departments are the models traditionally used in intercollegiate athletics (Russo, Esckilsen & Stewart, 2009; Steinbach, 2004). The most well-known study on NCAA Division the distribution of the respondents among the different types of arena management models was not homogeneous in this study; the number of schools adopted the “Operated by a Private Management Company” model and “Operated by a Government Entity” model were relatively small. Journal of Venue and Entertainment Management, Vol. 3, Issue 2 23 Results Reasons for Adopting a Certain Arena Management Model The first research question asked for the reasons perceived by the NCAA Division I athletic directors for adopting different arena management models. The results of the descriptive analysis indicated that the 19 out of 21 reason items had a mean higher than three. The respondents showed disagreement to only two of Journal of Venue and Entertainment Management, Vol. 3, Issue 2 the reason items (other schools’ success motivated our choice of arena management model, M= 2.62; and the institution does not have an on-campus venue available, M=2.08) (Table 2). Common Constructs Extracted To answer the second research question, factor analysis was used to explore the common components or constructs that can be extracted from the items that 24 represent the reasons, advantages and disadvantages, and level of satisfaction perceived by the surveyed athletic directors. The analysis yielded six meaningful constructs: revenue and costs, venue management and control, venue characteristics, university policy, overall Journal of Venue and Entertainment Management, Vol. 3, Issue 2 satisfaction, and transference of risks (Table 3). Table 4 illustrates each of these six constructs’ distribution among the population, and how these constructs were labeled to accurately reflect the variables that loaded under each one of them. 25 Components Differentiating Traditional and Emergent Arena Management Models The third research question asked whether there were any components that differentiate the perceptions between the athletic directors from institutions that adopted the traditional arena management models and the athletic directors from institutions that adopted the emerging management models. Discriminant analysis Journal of Venue and Entertainment Management, Vol. 3, Issue 2 was conducted including the six constructs identified through the factor analysis and demographic information (i.e., years of experience as administrator, seating capacity, average attendance, community size, and enrollment) which can potentially influence the decision to adopt a certain arena management model. 26 A stepwise protocol was used to remove any variable that did not statistically contribute in describing the groups. The results of discriminant analysis were initially analyzed by examining the Wilks’ lambda (.789) for each function. One discriminant function was generated with x2 (2) = 24.203, p < 0.05. Two main variables had significant association between the groups and the descriptor variables. The results of the discriminant Discussion and Implications analysis showed that venue management and control (.799) and that institution enrollment (-.607) were the constructs with the most significance in distinguishing the traditional models group from the emergent models group (Table 5). ment models, the findings indicated that respondents tend to desire full operational and financial control over their venue, as they believed they had the expertise to manage it. The results further suggested that most of the respondents concur that their departments need to reduce costs, maximize revenue, and transfer risks. It is interesting that the respondents acknowledge the need for improvement in these areas, but continue to manage their venues in traditional ways. This mindset could prevent athletic administrators from exploring alternative arena management models that may make their venues more cost efficient and profitable. The weak financial results of most NCAA Division I athletic de- Journal of Venue and Entertainment Management, Vol. 3, Issue 2 This empirical research explored athletic directors’ perceptions towards various arena management models and the factors that differentiate perceptions of athletic directors adopting the traditional-versus-emerging arena management models. When examining the perceived reasons for adopting different arena manage- 27 partments (Fulks, 2011) indicate that perhaps the way the departments are currently managed should change, including the management of their arenas. Supporting this idea is the fact that respondents reported having venues on-campus (only 16 respondents indicated they do not have a venue available on-campus) with the size and ability to successfully host profitable events to increase their net revenues. Such conditions make these arenas strong candidates for either being outsourced or becoming auxiliary enterprises. When exploring athletic directors’ perceptions towards various arena management models, six common constructs (overall satisfaction, venue management and control, revenue and costs, venue characteristics, university policy, and transference of risks) emerged from the list of reasons and satisfaction items originally included in the survey. The emergence of these six constructs from the factor analysis was expected. The literature on restructuring, outsourcing, and athletic venues describes those same constructs as part of the main factors for adopting a certain management model (Ammon et al., 2010; Fried, 2010; Jewell, 1992; 1998; Mulrooney & Styles, 2004; Russo et al., 2009; Steinbach, 2004). These constructs are important for they provide the essential factors that should be taken into consideration when considering a change in arena management model. The administrators’ overall satisfaction is an obvious justification for the maintenance of the model they currently use. The type of involvement the athletic department either can or wants to have in their venues operations (venue management and control construct) may prevent the use of certain management models (e.g. auxiliary enterprise, and private management) (Jewell, 1992;1998; Mulrooney & Styles, 2004; Russo et al., 2009; Steinbach, 2004). The revenue and costs construct supports the idea of choosing an arena management model that efficiently aids athletic departments in reducing costs and increasing revenue to pursuing self-sufficiency (Denhart et al., 2009; Fulks, 2011). Lack of size and revenue generation potential (venue characteristics construct) may prevent athletic directors from turning their arenas into auxiliary enterprises or outsourcing them to a private management company (Jewell, 1992; 1998; Russo et al., 2009; Steinbach, 2004). The existence of an university policy determining the way arenas are to be managed directly affects the arena management options available to administrators when deciding to maintain or change the way arenas are controlled and operated (Jewell, 1992; 1998; Russo et al., 2009). The necessity and ability to transfer risks and Journal of Venue and Entertainment Management, Vol. 3, Issue 2 reduce loss (risk reduction construct) is influential when determining which arena management model best fits the athletic departments’ circumstances and needs (Corbett, 2004; Ender & Mooney, 1994; Russo et al., 2009). Finally, when identifying the perception components that differentiate administrators adopting traditional arena management models from those adopting emergent models, the results showed that venue management and control and institution enrollment are the two constructs with the most significance in differentiating the two groups. It was not surprising to find that venue management and control surfaced as one of the constructs that best differentiated traditional and emergent models given what is known from the literature. The decision regarding which venue management model best fits facilities’ and athletic departments’ characteristics (and needs) depends on factors including ownership’s desired level of control over the facility, the facility’s revenue potential, in-house expertise, institutional demand, common practices (the way it has always been done), timing and circumstances, and contractor availability (Ammon et al., 2010; Fried, 2010; Jewell, 1992; 1998; Mulrooney & Styles, 2004; Palmero et al., 2010; Russo et al., 2009; Steinbach, 2004). It was also not surprising to find that enrollment would help differentiate between traditional and emergent model groups. Schools with large enrollments tend to have optimum conditions (large venues and high potential for revenue generation) that facilitate the adoption of emergent arena management models (i.e., auxiliary enterprise and private management) (Ammon et al., 2010; Fried, 2010; Jewell, 1992; 1998; Mulrooney & Styles, 2004; Palmero et al., 2010; Russo et al., 2009; Steinbach, 2004). Based on these same principles, it still remains to be investigated in future research studies why venue size was not a significant factor differentiating the two groups. Arena Management Decision Framework The primary purpose of this study was to add to the body of knowledge in sport facility management as well as provide guidance on choosing an arena management model to executives in higher education. The empirical results, combined with logical inferences from other experiences, provided direction and foundation for the conceptualization and development of the Arena Management Decision Framework (Figure 1). Overall, the results implied that athletic departments and higher education institutions that seek more 28 Figure 1—Arena Management Model Decision Framework control over their venues may tend to adopt traditional arena management models; meanwhile, athletic departments that do not (or cannot) seek as much control over their arenas tend to lean toward the selection of an emergent model. It is also logical that athletic departments within larger institutions may be more prone to choose an emergent arena management model than those within smaller institutions. Larger schools tend to possess larger arenas, and larger venues tend to have greater revenue generation potential, which makes those venues capable to become auxiliary enterprises or be a good fit for private management (Ammon et al., 2010; Fried, 2010; Jewell, 1992; 1998; Mulrooney & Styles, 2004; Palmero et al., 2010; Russo et al., 2009; Steinbach, 2004). The Arena Management Model Decision Framework can be used as a guide for selecting an arena management model with the basic assumption for this framework being that the athletic department is curJournal of Venue and Entertainment Management, Vol. 3, Issue 2 rently managing the area internally and is expected to reduce costs and maximize revenues. The reason for the adoption of these assumptions is that 63% of the NCAA Division I athletic departments operate their arenas internally (Palmero et al., 2010). Plus, it is clear that there is widespread pressure to reduce costs in intercollegiate athletic operations. To illustrate the use of the Arena Management Model Decision Framework, the following steps are examples of how an athletic leader might navigate the decision to maintain or change arena management models. First, the athletic administrator should assess their level of satisfaction with the use of the current model. If they are satisfied, they should maintain its use. However, if they are unsatisfied, they should consider another model. The next step is to consider the amount of control administrators want to have over the venue, the availability of in-house expertise, and the university policies on arena management. Depending on institu29 tional policies, administrators may or may not have the ability to change the model. In situations where the administrators have power to decide how to operate the venue, they should also consider the need (or desire) to transfer risk. Lack of in-house expertise and opportunity to transfer risk may lead decision makers to contract a private management company to operate their venues. Finally, administrators should consider the size of the institution, the venue’s ability to host outside events, and the venue’s revenue generation potential. Larger venues within larger institutions and with good revenue generation potential have great chances to succeed either as auxiliary enterprises, or to be operated by private management companies. Recommendations for Future Research In contemporary venue management, private management is a model that is commonly utilized to operate professional-level sporting venues (Jewell, 1992; 1998; Steinbach, 2004). However, private management does not currently have the same presence at the college level (Palmero et al., 2010). It would be interesting to conduct a qualitative study involving all of the major private management companies to better understand the common criteria used to determine the feasibility of taking over the operation of a certain college venue. To complement the study, athletic directors could be surveyed to collect their perceptions regarding the identified services and advantages of outsourcing arenas’ operations to a private management company. Using the Arena Management Model Decision Framework, athletic directors could be asked to indicate their level of willingness to outsource their venue operations. This future study’s response rate could be enhanced by sending the surveys to senior athletic administrators responsible for facilities, in addition to the athletic directors. use. Six common constructs (overall satisfaction, venue management and control, revenue and costs, venue characteristics, university policy, and transference of risks) were identified as the essential factors that should be taken into account when considering a change in arena management model. Venue management and control and institution enrollment were the constructs which better distinguish the traditional-models group from the emergent-models group. Athletic departments seeking more control over their venues may tend to adopt traditional arena management models, and departments that do not (or cannot) seek as much control tend to select an emergent model. Because larger schools tend to possess optimum conditions for their arenas to either become auxiliary enterprises or be a good fit for private management, athletic departments within such schools may be more prone to choose an emergent arena management model than those within smaller institutions. These factors were the foundation for the development of the Arena Management Model Decision Framework that may provide guidance to higher education leaders who may be exploring the management model that best fits their needs. Conclusions The present study demonstrated that there are a variety of factors that should be part of any discussion in higher education related to intercollegiate athletic arena management. Although traditional arena management models remain the dominant approach in intercollegiate athletic arena management, emergent models (e.g., auxiliary enterprise and private management) should be considered as a viable option for institutions moving forward. A majority of the respondents seem to desire full operational and financial control over their venue, which may prevent them from exploring arena management models other than the one they currently Journal of Venue and Entertainment Management, Vol. 3, Issue 2 30 References Ammon, R., Jr., Southall, R. M. & Nagel, M. S. (2010). Sport facility management: Organizing events and mitigating risks (2nd ed.). Morgantown, WV: Fitness Information Technology. Bankhead, W. H. (1975). Administrative policies and procedures for large multi-purpose arenas on university campuses. Doctoral dissertation, Louisiana State University—Baton Rouge. Brown, M. T., Rascher, D. A., Nagel, M. S. & McEvoy, C. D. (2010). Financial management in the sport industry. Scottsdale, AZ: Holcomb Hathaway Publishers Inc. Burden, W., & Li, M. (2005). Circumstantial factors and institutions’ outsourcing decisions on marketing operations. Sport Marketing Quarterly, 14, 125–131. Corbett, M. F. (2004). The outsourcing revolution: Why it makes sense and how to do it right. Chicago, IL.: Dearbon Trade Publishing. Denhart, M., Villwock, R., & Vedder, R. (2009). The academics athletics trade-off: Universities and Intercollegiate athletics. Washington, DC: Center for College Affordability and Productivity. Ender, K. L., & Mooney, K. A. (1994). From outsourcing to alliances: Strategic strategies for sharing leadership and exploiting resources at metropolitan universities. Metropolitan Universities, 5(3), 51–60. Ehrenberg, R. G. (2006). The perfect storm and the privatization of public higher education. Change, 39(1), 46–53. Fried, G. (2010). Managing sport facilities, Champaign, IL: Human Kinetics. Fulks, D. (2011). 2004–2010 NCAA Division I revenues and expenses report. Indianapolis, IN: The National Collegiate Athletic Association. Global Spectrum (2009). Full/contract management. Retrieved on June 19, 2009 from http://www.globalspectrum.com/region/en/why-private-management. aspx. Graham, P. J. & Ward, R. (2004), Public assembly facility management: Principles and practices. Coppell, TX: International Association of Assembly Managers. Jewell, D. (1992). Public assembly facilities. Malabar, FL: Krieger Publishing Company. Journal of Venue and Entertainment Management, Vol. 3, Issue 2 Jewell, D. (1998). Privatization of public assembly facilities management. Malabar, FL: Krieger Publishing Company. Lawrence, H. J., & Moberg, C. R. (2009). Luxury suites and team selling in professional sport. Team Performance Management. 15(3/4). 185–201. Lee, J., & Clery, S. (2004). Key trends in higher education. American Academic, 1(1), 21–36. Li, M., & Burden, W. (2002). Outsourcing sport marketing operations by NCAA Division I athletic programs: An exploratory study. Sport Marketing Quarterly, 11(4), 226–232. Mulrooney, A., & Styles, A. (2004). Managing the facility. In B.L. Parkhouse (Ed.), The management of sport: Its foundation and application (pp. 45–52). New York: McGraw-Hill. National Collegiate Athletic Association. (2010). 2009 National college men’s basketball attendance report. Retrieved on May 20, 2010, from http:// web1.ncaa.org/web_files/stats/m_basketball_RB/ Reports/2009mbbattend.pdf. Palmero, M., Li, M. & Lawrence, H. (2010). Is private management of NCAA Division I basketball arenas a trend? Presentation at the 2010 NASSM Conference. Penry, J. C. (2008). Forecasting the financial trends facing intercollegiate athletic programs of public institutions as identified by athletic directors of the ACC, Big 12 and SEC conferences. Doctoral dissertation, Texas A&M University – College Station. Russo, F. E., Esckilsen, L. A. & Stewart, R. J. (2009). Public assembly facility management: Principles and practices, (2nd ed.). Coppell, TX: International Association of Assembly Managers, Inc. Seidler, T. L., Gerdy, J. R., & Cardinal, B. J. (1998). Athletic director authority in Division I intercollegiate athletics: Perceptions of athletic directors and college presidents. International Sports Journal, 2(2), 36–46. Shindell, W. G. (1993). Facilities management issues. In M.J. Barr (Ed.), The handbook of student affairs administration (pp. 12–22). San Francisco: Jossey-Bass Publishers. Sperber, M. (1990). College sports Inc.: The athletic department vs. the university. New York: Henry Holt and Company. 31 Sperber, M. (2000). Beer and circus: How big-time sports is crippling undergraduate education. New York: Owl Books. Steinbach, P. (2004). Special operations: Arena management firms help schools boost revenue from behind the scenes. Athletic Business, 28, 24–28. Zimbalist, A. (2007). College athletic budgets are bulging but their profits are slim to none. Sports Business Journal, 10(9), 26. Zumeta, W. (2009). State support of higher education: The roller coaster plunges downward yet again. The NEA 2009 Almanac of Higher Education, 1, 29–43. Journal of Venue and Entertainment Management, Vol. 3, Issue 2 32