Financial Policy and Decision- Making in Low Income Households Sendhil Mullainathan

advertisement

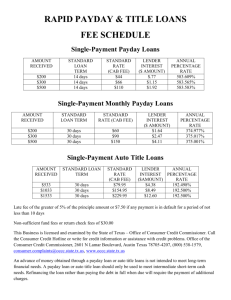

Financial Policy and DecisionMaking in Low Income Households Sendhil Mullainathan Eldar Shafir Two Dominant Views of Poverty Rational Choice view – Consistency, Willpower, Well-defined preferences,.. – Behavior: calculated adaptation to prevailing circumstances Pathology view – Psychological pathologies specific to the poor – Impatient, no planning, confused – Behaviors endemic to “culture of poverty” An alternative: Neither rational nor pathological; just plain human… A Psychological Perspective • Large body of decision research (among the “comfortable”): – – – – Biases in decision making Limited willpower Malleable preferences Channel factors • Operating assumption: – Rich and poor have similar psychological make-ups – Expression is different in different contexts – Consequences can be different Psychology: Power of Context • Darley and Batson • Recruited seminary students to deliver practice sermon on the parable of Good Samaritan • After completing surveys, told to go to another building for the sermon • Half (“Rushed”) were led to believe they were running late Psychology: Power of Context • On the way to give talk, all participants passed an ostensibly injured man slumped in a doorway, coughing and groaning. • Key DV: Would individual stop? Psychology: Power of Context • Outcome: – No hurry 63% helped, – Medium hurry 45% – High hurry 10% • Notice: – These are priests…ironically giving a lecture on the good samaritan • Key insight: – Channel factors. Facilitate good behaviors The failure to act… (Lack of attention; indecision; decision avoidance; procrastination; status quo..) Elective surgery: 10% of older adults who were willing to consider total joint arthroplasty, and were perfect candidates, chose to have it. Interviews with others: Hadn’t decided “no”; just deferred… (Hudak et al.) Medical self-exams: Among teaching physicians!..: “… low rates of self-examination for both TSE and BSE. Barriers… included embarrassment, perceived unpleasantness and difficulty, concern about reliability, and worries about what tests might reveal...” “Where standard intuition would hold the primary cause of a problem to be human frailty, or the particular weakness of a group of individuals, the social psychologist would often look to situational barriers and to ways to overcome them.” Ross and Nisbett, 1991 Theme Common to Both Traditional Views: Major problem => Major Cause => Major intervention Large subsidies Costly education A change in values and “culture” Instead: Social psych / BDT may provide different insights, which can be used to explain (and intervene with) behavior of the poor… minor situational details can have a large impact context, construal, etc. Channel Factors (Lewin) • Contrary to major interventions that prove ineffectual, apparently minor situational details can have a large impact… • Leventhal, Singer and Jones: – Students receive persuasive messages about tetanus inoculation. Offered tetanus shot – Only 3% showed up later at shot – If given map and urged to decide particular time, 28% showed up. • Did students “want” tetanus shot? Revealed preference Two implications of this insight • Revealed preference: – Outcomes do not reflect “deep” preferences • Design of institutions Poor versus Rich • Why might common failings such as these lead the poor to be more affected than the rich? – Different institutions – Different problems/circumstances • Will use this perspective to understand three phenomena about financial services: – Banking services – Payday borrowing Role of Institutions • Shape defaults • Provide implicit planning Defaults Institutions Shape default • Power of direct deposit – Default translates from cash in hand to cash in account – Must take active step to withdraw certain amount of money • Gives simple perspective on how direct deposit could have very large consequences for behavior • Suggests simple policy intervention Institutions Provide Implicit Planning • Problem of planning: – Attention • How much time have you spent deciding how much to save for retirement? – Time inconsistency • Hard to stick to plans • Hard to continue implementing plans Problem of Planning • Intentions don’t always match behavior. Examples from US data • Consumers report a preference for flat or rising consumption paths – But consumption drops by 1/3 after midlife • 76% of households believe they should be saving more for retirement – Baby boomers report desired savings rate of 15%. Actual savings: 5% • One quarter of employees say they’ll increase 401(k) savings in the next quarter. – Only 3% do. Institutions Provide Planning • Even credit card companies send reminders – Solve attention problems • Automatic bill payment – Solve attention problem in the best way • 401(k) – Make savings automatic. Best planning possible Lack of Planning Institutions • Poor risk late fees, missed payments disconnected utilities, etc. • Key policy insight: – How do we facilitate more automatic planning amongst poor? Contexts • So far, have talked about institutions • Now we discuss three non-institutional context differences Lack of Financial Slack • Financial slack – Different from economic model – Assumes there is always “frivolous” consumption • Consumption that is not really valued by future or past selves • Lots of slack means – Easy to deal with planning mistakes Rich and Financial Slack • Suppose a rich individual makes a mistake and forgets about his credit card bill which then comes due • Can cut back on expenses to pay it – Eating out less – An IPod purchase Poor and Financial Slack • Suppose a poor individual makes a mistake and forgets about his credit card bill which then comes due • Can cut back on expenses to pay it – Eating! – Rent payment • In other words, if the poor are at the margin of fewer frivolous expenses they are more exposed Poor face difficulty in cutting back • Cost of cutting back high – Late fees are high • 5% late fee for a monthly bill is equivalent to 100% APR • Bigger problems – Loss of home – Loss of telephone • Reconnect fees – Loss of car • Late to job - > Loss of job – Each of which has consequences Poor on the edge • Suggests that mis-planning can lead to two phenomena: – Large desire for credit funds even at very high rates • Extremely important point we return to later – Falling over the edge • Domino effect of phones being cut off, etc. Difficulty of Small to Big Transformation • Many of the purchases needed by the poor are big – Durables • Yet much of their income is small • Produces central tension: – How to transform small amounts of cash into big amounts? – Key role of savings and other institutions Difficulty of Savings • “Voluntary” mechanism – Raises problem of Self-control • Alternative mechanisms – Lotteries • Relation to ROSCAs – Layaways • Notice inflexibility • Suggests class of savings mechanisms should focus specifically on this problem – Very different from buffer stock No buffer stock • Another key feature of lives of the poor: – Extremely high volatility of incomes • Yet key puzzle: Why the lack of a buffer stock – Again, self control problem: leaky bucket – Note: due to lack of financial slack, poor would need a bigger buffer stock. • Design challenge: – Create buffer stock institution that cannot be tapped into for temptations Summary • Lack of Financial Slack – Poor can find themselves at the “edge” of deep poverty • Difficulty of small to big transformation • Lack of buffer stock to deal with shocks Three Institutions • Banking • Payday Loans • Check Cashing Unbanked • Why remain unbanked? • Channel factors? – The Federal Reserve Bank conducted a study in 2000 that asked un-banked families why they didn’t have a checking account. Among top reasons: Do not like dealing with banks. • What if…Unbanked due to: – Nuisances (sneers from teller, no babysitter…), – unfamiliarity, conscious violation of social norms • How do we reduce channel factors? Providing low-fee bank accounts to the poor (Bertrand, Mullainathan, & Shafir) QuickTime™ and a TIFF (Uncompressed) decompressor are needed to see this picture. QuickTime™ and a TIFF (Uncompressed) decompressor are needed to see this picture. – Prior program proved of limited effectiveness (<50% take-up.) – Follow-up surveys: 90% intended to, but forgot, misplaced the relevant forms, etc… – 2-hour long workshop; If workshop participant interested in FA: • Referral letter to take to the bank, OR • Sign up on site if bank representative present at the workshop Presence of a bank representative: significantly increased opening and keeping an account, and decreased check cashing, and borrowing from family. Take-up: ~8 percentage points higher among those who voluntarily attended workshop. Take up: ~10 percentage points higher among those who attended workshop where a Shorebank representative was present. (Can compare accounts opened at financial educ. workshop vs. tax prep. sites: No significant differences in closure rates, or in monthly usage patterns) Cf., Retirement Savings; “Save More Tomorrow” (Benartzi & Thaler) Deeper Issue • How do we encourage private sector to remove channel factors? • Key policy observation: – Channel factors are largely unobservable by regulator – Suggests outcome regulation rather than input regulation Benefits of Banking • Perspective also suggests something else: – Why being unbanked can have big consequences • Cash on hand vs. in account • Help with planning • Access to other financial services that provide implicit planning and other automatic behavior Payday Loans • Often cited puzzle: – Poor take out payday loans at rates upward of 7000+% • Two observations: – Mental accounting – Where is the error? The Calculator Problem Imagine that you are about to purchase a calculator for $50. The calculator salesperson informs you that the calculator that you wish to buy is on sale at the store’s other branch, located a 20-minute drive away. What is the highest price that the calculator could cost at the other store such that you would be willing to travel there for the discount? The Computer Problem Imagine that you are about to purchase a computer for $2000. The computer salesperson informs you that the computer that you wish to buy is on sale at the store’s other branch, located a 20-minute drive away. What is the highest price that the computer could cost at the other store such that you would be willing to travel there for the discount? The Purchase Computer ($2,000) Calculator ($50) Mean response = $1849.50 Mean response =$26.74 Implied savings: $150 Implied savings: $24 Implications for Payday Loan Pricing • People do not evaluate prices in a vacuum – But relative to other prices or levels – So is the price of a payday loan 7000%? – Or is it $10? Are Payday Loans Bad? • Recall discussion of lack of financial slack • From that perspective payday loans are essential for the poor – Key problem is not taking out the loan – Key problem is mis-planning in the past that brought them to the point where they need a payday loan – From this perspective reduction in supply of payday loans would be bad • Unless it induces poor to plan more—hardly a stronger incentive than what is already there Payday Loans • Suggests that payday loans should instead focus on: – Other risk mitigation mechanisms (buffer stock mechanisms) – Late fee regulations amongst utilities, etc. Summary • Psychological perspective on financial lives of the poor • Enriches and complicates our view of role of: – Institutions – Regulation