Problem Set #2: Overlapping Generations Models Question 1 Jorge F. Chavez

advertisement

University of Warwick

EC9A2 Advanced Macroeconomic Analysis

Problem Set #2: Overlapping Generations Models

Suggested Solutions - Q2 revised

Jorge F. Chavez∗

December 6, 2012

Question 1

Consider the following production function

2

6Kt − Kt /Lt if

Yt = F (Kt , Lt ) =

2K + 4L

if

t

t

Kt /Lt ≤ 2

Kt /Lt > 2

(a) Show that this function is characterized by constant returns to scale (CRS) and that output

per worker is given by:

2

6kt − kt if kt ≤ 2

yt = f (kt ) =

2k + 4 if k > 2

t

t

Solution. This implies showing that F : R2 → R is homogeneous of degree 1. That’s it, we need to

show that for λ > 0, F (λKt , λLt ) = λF (Kt , Lt ). Then:

• For kt ≤ 2:

2

F (λKt , λLt )

(λKt )

6 (λKt ) −

λLt

(

)

= λ 6Kt − Kt2 /Lt = λF (Kt , Lt )

=

• for kt > 2:

F (λKt , λLt )

=

2λKt + 4λLt

= λ (2Kt + 4L) = λF (Kt , Lt )T hen

∗

e-mail:j.chavez-cotrado@warwick.ac.uk

1

EC9A2 (Fall 2012)

Problem Set # 2

Finally, to show the formula for f (kt ):

{

F (Kt , Lt )

Lt

=

t

6K

Lt −

t

2K

Lt

{

=

Kt2

L2t t

+4

6kt − k 2t

2kt + 4

Kt /Lt ≤ 2

Kt /Lt > 2

kt ≤ 2

kt > 2

For the following parts assume that population and technology are constant and that capital

fully depreciates at the end of each period.

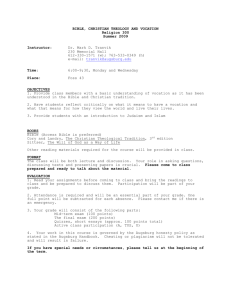

(b) Calculate the share of labor income as a function of kt . Show your results in a figure.

Solution. Recall that wt = f (kt ) − kt f ′ (kt ), then:

{

′

wt = f (kt ) − kt f (kt )

=

{

=

6kt − kt2 − 6t kt + 2kt2

2kt + 4 − 2kt

kt2

4

if kt ≤ 2

if kt > 2

if kt ≤ 2

if kt > 2

Finally, the share of labor income is:

sL =

wt

=

f (kt )

{

kt / (6 − kt )

2/ (2 + k)

if kt ≤ 2

if kt > 2

Figure 1 plots the share of labor income as a function of kt .

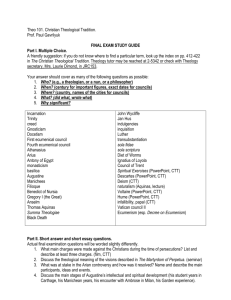

(c) Find the dynamical system for the Solow model under the assumption that the saving rate

s = 1/3. Show that there exists a unique, globally stable, non-trivial steady state.

Solution. Because δ = 0:

{

kt+1

=

sf (kt ) =

≡

ϕ (kt )

(

)

6kt − kt2

(2kt + 4)

1

3

1

3

kt ≤ 2

kt > 2

The steady-states for this dynamical system are:

(a) For k ≤ 2:

k

=

k2

=

6k − k 2

3

3k ⇒

k(k − 3) = 0

⇒

k1 = 0, k2 = 3

Because this function is defined for k ≤ 2, we rule out k = 3. Then the only steady-state here

is k = 0

Jorge F. Chávez

2

EC9A2 (Fall 2012)

Problem Set # 2

1

0.5

sL =

sL =

k

6−k

2

k+2

0

1

2

3

4

Figure 1: Share of labor income

(b) For k > 2:

k

2k + 4

3

3 ⇒

=

2k + 4 =

k=4

Stability of the steady-state k ss requires |ϕ′ (kss )| < 1. The derivative of the policy rule φ(kt ) is:

′

ϕ (kt ) =

{

1

3

(6 − 2kt )

2

3

if kt ≤ 2

if kt > 2

Then |ϕ′ (0)| = 2 > 1 which implies that this steady-state is unstable. Finally, |ϕ′ (4)| = 23 < 1

which implies that this steady state is globally stable. Therefore, there exists a unique non-trivial

steady-state.

Remark 1. If you would like to be more formal, you can always try to show uniqueness by contradiction. Start assuming that there is another feasible non-trivial steady-state, and then look for a

clear contradiction.

(d) Find the dynamical system of the OLG model (where individuals work in their first life period

and retire in the second). Assume utility is a function of only second period consumption

(that is, individuals save their entire first period income). Is the non-trivial steady state

unique and globally stable?

Solution. Because individuals only consume in their second year of life (when old):

st = wt = kt+1

Jorge F. Chávez

3

EC9A2 (Fall 2012)

Problem Set # 2

45o

6

5

1

3 (2kt

+ 4)

4

3

8

3

2

1

3 (6kt

1

0

1

2

− kt2 )

3

4

5

6

7

8

Figure 2: Law of motion for kt+1 in the Solow model

Because δ = 1:

st = syt + sot = kt+1 − (1 − δ)kt = kt+1

Then:

{

kt+1 = wt

kt2

4

if kt ≤ 2

if kt > 2

In steady-state:

{

k=

k2

4

kt ≤ 2

kt > 2

Then, k1 = 4 if k > 2, k2 = 0 and k3 = 1 if k ≤ 2

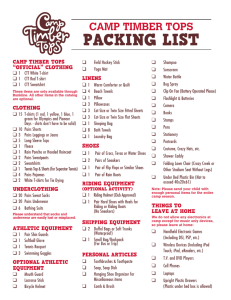

(e) Why do the two models generate results that are qualitatively different?

Solution. In the Solow model savings per capita (st ) are a fraction of yt = f (kt ), which is concave.

In contrast, in the OLG setting, savings are a constant fraction of wages.

Jorge F. Chávez

4

EC9A2 (Fall 2012)

Problem Set # 2

45o

6

5

1

3 (2kt

4

+ 4)

kt2

3

8

3

2

1

3 (6kt

1

0

1

2

− kt2 )

3

4

5

6

7

8

Figure 3: Law of motion for kt+1 : Solow model vs. OLG model

Question 2

Consider the following overlapping generations model (OLG). Technology and population are

constant. Output per worker is

yt = Aktα kt = Kt /Lt

Utility of individuals who are born in t is

1

U (ct , ct+1 ) = ct + ct+1

ρ

Capital fully depreciates at the end of each period: δ = 1.

(a) Find the dynamical system. (hint: the system is characterized by two qualitatively different

regimes, separated by a threshold level of kt+1 , where, for low levels of kt+1 there is no

consumption in the first period).

Solution. A household born in time t solves:1

{

}

ctt + ρ1 ctt+1

max

(ctt ,ctt+1 )∈R2+

s.t.

ctt + stt ≤ wt

ctt+1 ≤ Rt+1 stt

1

The budget constraints can give way to a life-time budget constraint: ctt +

Jorge F. Chávez

ctt+1

Rt+1

≤ wt

5

EC9A2 (Fall 2012)

Problem Set # 2

Note that this is a particular case as the utility is linear, implying that goods a perfect substitutes.

Appendix 1 shows how to analyze this kind of settings using the Karush-Kuhn-Tucker generalization

of the so-called method of Lagrangean multipliers for a problem with non-negativity constraints, like

the one stated above.

However this problem can be tacked directly. In principle, there will be three cases regarding the

relationships between Rt+1 and ρ. First, if the slope of the budget constraint is higher than the slope

of the indifference curve (Rt+1 < ρ) then the problem will have a corner solution (ctt > 0, ctt+1 = 0)

as can be seen in figure 4a. Likewise, if Rt+1 > ρ then we will have a second potential corner solution

(ctt = 0, ctt+1 > 0) as is shown in figure 4b. The third case is the case in which the slope of the

indifference curve is exactly equal to the slope of the budget constraint Rt+1 = ρ, in which case we

will have a continuum of interior solutions.

U3

ctt+1

ctt+1

U2

0, ctt+1 )

U1

0, ctt+1 )

U3

U2

U1

0

(ctt , 0))

{ ctt , ctt+1 ∈ R2+ s.th. ctt +

ctt+1

Rt+1

ctt

0

(ctt , 0))

{ ctt , ctt+1 ∈ R2+ s.th. ctt +

= wt }

(a) If Rt+1 < ρ

ctt+1

Rt+1

ctt

= wt }

(b) If Rt+1 > ρ

Figure 4: Linear utilities

We can summarize the results in terms of savings st :

wt

if Rt+1 > ρ (because ctt = 0 & ctt+1 > 0)

st =

∈ [0, wt ] if Rt+1 = ρ (because ctt > 0 & ctt+1 > 0)

0

if Rt+1 < ρ (because ctt > 0 & ctt+1 = 0)

α

Recall that Rt+1 = αAkt+1

. Then, if Rt+1 = ρ:

α−1

Rt+1 = αAkt+1

=

ρ

|{z}

constant

which implies a particular and constant level of kt+1 :

(

k̄ =

Jorge F. Chávez

αA

ρ

)1/(1−α)

>0

6

EC9A2 (Fall 2012)

Problem Set # 2

Then we can define the following if and only if statements:

Rt+1 > ρ

α−1

⇔ αAkt+1

>ρ

⇔ kt+1 < k̄

Rt+1 = ρ

(1)

α−1

⇔ αAkt+1

=ρ

⇔ kt+1 = k̄

Rt+1 < ρ

(2)

α−1

⇔ αAkt+1

<ρ

⇔ kt+1 > k̄

(3)

Clearly k̄ is an important landmark to understand the law of motion that governs the evolution of

kt .

Two important things to note are:

i. The individual born in t’s saving/investment decision (stt = st = kt+1 ) affects the return to this

α−1

we can see that this

investment. Since the return to capital tomorrow will be Rt+1 = αAkt+1

return is a function of kt+1 .

ii. Because the individuals budget constraint in the first period is ctt + stt ≤ wt , then it is clear that

the wage at time t (which by the way depends on the stock of capital in the economy when the

individual from the t generation was young, wt = (1 − α)Aktα will be an upper bound for the

stock of capital: stt = st = kt+1 ≤ wt : the individual cannot save more than your income in the

first period of your life.

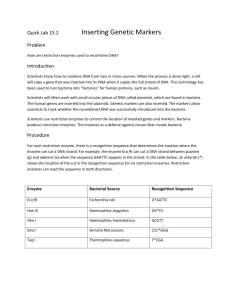

45o

wt = (1 − α)Aktα

C

B

A

k̄

ϕ(kt )

k1

k0 k̂

k1 k̄

kt

Figure 5: Dynamic system

At first sight, the iff statements (1), (2) and (3) stated above seem to sketch the dynamical system for

kt+1 . However, a closer examination of the last condition reveals that it implies a huge contradiction:

Jorge F. Chávez

7

EC9A2 (Fall 2012)

Problem Set # 2

if st = kt+1 > k̄ then Rt+1 < ρ and the economy will consume everything in the first period and

therefore savings in the first period will be zero st = 0. So, the second corner ctt = wt > 0, ctt+1 = 0

is not feasible in an equilibrium.2

Then as figure 5 shows, there is a critical value for kt (in the first period) defined by:

wt = (1 − α) Ak̂ α = kt+1 = k̄

which yields:

[

k̄

k̂ =

(1 − α) A

]1/α

If the individual is born in an economy with starting capital k0 < k̂, then she will save all her wage

wt = (1 − α)Ak0α = k1 < k̂. Clearly k1 > k0 . If k1 < k̂ then we repeat the whole decision process.

However, if k0 is high enough so that k1 > k̂, as depicted in figure ??, now the upper bound wt will

be above k̄: w1 = (1 − α)Ak1α > k̄. Then the individual will have three alternatives for her saving

decision, and here is where the fact that the individual’s saving decision determines the return to

her savings (capital) will play a crucial role:

(a) If s1 = w1 > k̄ (save all, consumer nothing at t = 1), then s1 = k1 > k̄ and therefore the return

to the savings R2 will be less than ρ. This implies that s1 = 0 was the optimal strategy.

(b) If s1 < k̄ (save less than k̄), then the return will be R1 > ρ which implies that saving the whole

wage w1 was the optimal strategy.

(c) Finally the individual could choose to save s1 = k̄. In this case, R1 = ρ which implies that

k1 = k̄.

One can think of this decision-making process as a trial and error process. First the individual

considers saving everything. Then, realizing that it is not optimal, it could consider saving less than

the whole w1 and will do this until it reaches k̄, in which there is not contradictions. Likewise, if the

individual starts by considering saving less than k̄, later will realize that it reaches an equilibrium if

and only if k1 = k̄.

Finally, we can defined the dynamical system kt+1 ≡ φ(kt ) as:

{

(1 − α) Aktα if kt < k̂

kt+1 =

k̄

if kt ≥ k̂

Figure 5 plots φ(kt ).

(b) Find sufficient conditions on the parameters that assure that the steady state is characterized

by consumption in the first period.

Solution. In order to ensure that the steady state has positive consumption for agents when young

(ctt > 0) we need k̂ < k̄. That is, that point B in 5 is to the left of point C. Otherwise the steady-state

will be characterizing as having ctt = 0 all the time.

2

Indeed the case in which st is suspicious as the fact that the economy accumulates no capital (given the

assumption full depreciation) implies that the economy will be stuck in the trivial steady-state: no capital, no

production, no consumption. That is, the economy will virtually disappear.

Jorge F. Chávez

8

EC9A2 (Fall 2012)

Problem Set # 2

Then, k̂ < k̄ requires:

(

αA

[(1 − α) A]

> k̄ =

ρ

(

)

αA

(1 − α) A >

ρ

)1/(1−α)

1/(1−α)

Which yields the condition:

ρ>

Jorge F. Chávez

α

1−α

9

EC9A2 (Fall 2012)

Problem Set # 2

Appendix 1

A1 KKT conditions for the case of linear utlity

A household born in time t solves the following problem with non-negativity constraints:

max

ctt + ρ1 ctt+1

2

)∈R+

ctt ,ctt+1

(

s.t.

ct

ctt + Rt+1

≤ wt

t+1

t

t

ct ≥ 0, ct+1 ≥ 0

The lagrangean is:

L=

ctt

(

)

ctt+1

1 t

t

+ ct+1 + λ wt − ct −

ρ

Rt+1

The Karush-Kuhn-Tucker (KKT) FONCs are:

Lctt

Lctt+1

Lλ

ctt

= 1−λ≤0

(4)

λ

1

−

≤0

ρ Rt+1

ct

= wt − ctt − t+1 ≤ 0

Rt+1

≥ 0

=

(5)

(6)

(7)

≥ 0

(8)

λ ≥ 0

(9)

ctt+1

Complementary slackness conditions are ctt Lctt = 0, ctt+1 Lctt+1 = 0, λLλ = 0 and must be satisfied

simultaneously with the KKT conditions.

i. For interior solutions: ctt > 0, ctt+1 > 0, λ > 0

Now (4), (5) and (6) bind so that λ = 1 and then (5) implies that Rt+1 = ρ. That is, if and

only if when this last condition is satisfied we can achieve an interior solution.3

ii. Corner solution 1: ctt > 0, ctt+1 = 0, λ > 0

Now (4) binds which implies that λ = 1 > 0 while (5) does not bind. Therefore

1

λ

−

<0

ρ Rt+1

⇒

Rt+1 < ρ

That is, for corner solution 1 to be a solution we need Rt+1 < ρ

iii. Corner solution 2: ctt = 0, ctt+1 > 0, λ > 0

3

Note that whenever ctt > 0 (4) binds and so it must be the case that λ > 0

Jorge F. Chávez

10

EC9A2 (Fall 2012)

Problem Set # 2

Now (4) does not bind, which implies that λ > 1.4 Then:

1

λ

−

=0

ρ Rt+1

⇒

Rt+1 = ρλ

⇒

Rt+1 > ρ

That is, for corner solution 2 to be a solution we need Rt+1 > ρ

A2: An alternative method to solve the UMP

There is a third alternative to analytically solve the optimization problem which entails reducing

the budget constraint and the non-negativity constraints into a single restriction on the domain

of the objective function. This is by far the most efficient method in the cases in which the

objective is a non-linear function, as you may have already seen in other problems.

Here, the standard non-linear programming problem, with non-negativity constraints, in A1

reduces to a single-variable problem in which the objective has a domain bounded from above

and from below. This means that we need to check for both type corners.

The agent solves:

{(

)

}

ct

1

wt − t+1 + ctt+1

max

Rt+1

ρ

0≤ctt+1 ≤Rt+1 wt

FONCs now reduce to a condition on parameters:

1

i. Corner 1: − Rt+1

+

1

ii. Interior: − Rt+1

+

1

ρ

1

iii. Corner 2: − Rt+1

+

4

1

ρ

< 0 for ct+1 = 0

= 0 for ct+1 ∈ (0, Rt+1 wt )

1

ρ

< 0 for ct+1 = Rt+1 wt

Therefore we can rule out the case for λ = 0.

Jorge F. Chávez

11