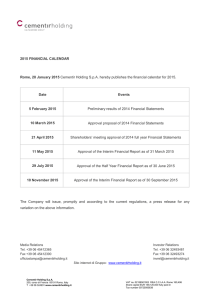

Financial Stability Measures Miguel Segoviano* and Raphael Espinoza RE

advertisement

Financial Stability Measures

Miguel Segoviano* and Raphael Espinoza

msegoviano@cnbv.gob.mx

RE i

REspinoza@imf.org

@i f

Financial Markets Group - Bank of England Conference

London-January 25, 2011

*O temporall leave

*On

l

f

from

the

h IMF.

IMF The

Th views

i

expressed

d iin this

hi presentation

i are those

h

off the

h author

h and

dd

do

not necessarily represent those of the IMF, CNBV or IMF,CNBV policy. Any errors remain attributable to the

authors.

Outline

I. Objective.

II. Main points of Modelling Framework.

III. Financial Stability and Systemic Risk Assessment:

Distress Dependence Amongst FIs.

Financial Stability Indicators

Financial Stability Indicators.

Systemic Macro‐Financial ST.

Second‐round effects

IV. Financial Stability and Sovereign Risk.

Spillover Coefficient.

Index of Global Risk Aversion.

Fundamentals.

V. Conclusions.

2

Modeling Framework

We assume that the financial system is a portfolio of FIs.

Macroeconomic

Risk Factors

Financial Risk Factors

Commercial Banking

PoD

Pension Funds

PoD

Mutual Funds

POD

Develpmt Bking Insurance Cos

PoD

POD

Brokers

PoD

Others

Financial System´s

Multivariate Density

EAD

LGD

0 . 2

0 . 1 5

0 . 1

0 . 0 5

0

4

2

4

2

0

Systemic

Loss Simulation

0

-2

-2

-4

-4

Systemic Stress

Indicators

Contagion

Indicators

Systemic Loss

Indicators

Sovereign Risk

Assessment

3

Objective

Framework to estimate consistently:

•

Complementary financial stability indicators.

•

Q

Quantification of expected and extreme losses at the systemic level.

ifi i

f

d d

l

h

i l l

•

Quantification of the marginal contribution to systemic risk of Quantification

of the marginal contribution to systemic risk of

individual institutions.

•

Assessment of the underlying factors causing sovereign risk to spread.

•

Stress Testing

Stress Testing.

4

Main Points

• It is a comprehensive coverage: The methodology allows for the inclusion of banking and non‐banking financial institutions (FIs)/sectors.

• It captures contagion effects: It takes into account interlinkages (direct and indirect) amongst Fis.

• It captures changes across the economic cycle of distress dependence amongst FIs and sovereigns.

dependence amongst FIs and sovereigns.

• It integrates complementary information: It uses micro‐

f

founded supervisory data and market‐based information.

d d

i

d t

d

k t b di f

ti

• It

It incorporates a wide set of factors: It accounts for a wide incorporates a wide set of factors: It accounts for a wide

set of macroeconomic and financial risk factors.

5

Main Points

• It

It provides robust estimations: It benefits from robust provides robust estimations: It benefits from robust

estimation with restricted data (under the PIT criterion).

• It can be extended to capture second round effects: It allows to take into account second‐round effects and macro‐

financial linkages.

financial linkages.

• It is being extended to different applications with national authorities around the world.

h ii

d h

ld

6

Implementation Map

IMF

ECB

USA , Canada / FSAP

Egypt FSAP

South Africa

FSAP

Denmark FSAP

Bank of Lithuania /

FSAP

Banque de France

Norges Bank

Banca d’Italia

CNBV México

Bank of Japan

Bank of Jordan

Deutshe Bundesbank

Sveriges Riksbank

Central Bank of UAE

Bank of Malaysia

7

Distress Dependence

Segoviano and Goodhart (2009)

Distress dependence between institutions is incorporated via joint Distress

dependence between institutions is incorporated via joint

movements of their PoDs, which in turn move in tandem due to

Systemic shocks

h k

Indirect Links

Lending to common sectors

Proprietary Trades

Direct Links

InterI t -Bank

Inter

B kD

Deposit

it M

Markets

k t

Syndicated Loans

The recent crisis underlined that proper estimation of distress dependence amongst FIs in a financial system is essential for financial stability FI i fi

i l

i

i l f fi

i l bili

assessment.

Contagion through

Idi

Idiosyncratic

i Shocks

Sh k

G dh

Goodhart, Sunirand, Tsomocos (2004).

S i d T

(2004)

8

The CIMDO Methodology

•

•

•

Problem: ‘how to estimate P(A,B) if we have P(A) and P(B)?’

( )

( )

( )

We can assume a known parametric distribution (e.g. multivariate normal), and estimate/calibrate parameters using data on A and B, but it seldom fits the data…

…or, we can try to “match” the data with a non‐parametric distribution ‐‐> CIMDO.

Advantages:

•

Robust: Without imposing unrealistic parametric assumptions.

•

It can be estimated from partial information: From PoDs on marginals, without the need to explicitly

to

explicitly set correlation structures.

set correlation structures

•

It characterizes the full “distributional dependence”: Rather than just linear dependence (correlations) or relations in the first few moments.

•

It embeds effects of changing macroeconomic conditions/shocks (via PoDs): It allows measurement of changes in dependence after shocks.

Source: Segoviano (2006)

9

CIMDO‐Density

Empirical

I f

Information

ti

10

CIMDO‐Copula

Lett X and

L

d Y be

b two

t

random

d

variables

i bl with

ith continuous

ti

di t ib ti functions

distribution

f

ti

F and

d H respecitvely,

it l

then the Spearman Correlation of X and Y is defined and denoted by the following:

S ( X , Y ) ( F ( X ), H (Y )) 12 [C (u , v) uv]dudv 12 C (u, v) 3

2

I2

I

Where I [0,1]x[0,1] and ρ(F(X),H(Y)) is the Pearson Correlation of the transformed uniform

random variables F(X) and G(Y).

2

11

Complementary Indicators

SYSTEMIC INDICATORS

MICRO-BASED INDICATORS

Market-based

Information

Supervisory

Information

Supervisory

Information

Market-based

Information

M to M Assets

PD Credit

Card

PD

ConsCre

PD

Housing

Ho

sing

PD

Commercial

Systemic Stress Indicators

PoD

Banks

SI

PoD

Banks

MI

Joint

Probability

of Distress

Financial

Stability

Index

PD

Governmental

C t i Indicators

Contagion

I di t

PD

Financial

PoD

Developt

B k

Banks

PoD

Pension

Funds

PoD

Mutual

Funds

PoD

Insurance

C

Co

PoD

Brokers

Distress

Dependence

Matrix

Contagion

Index

Spillover

Coefficient

Systemic Loss Indicators

Extreme

Systemic

Loss

Marginal

Contribution

to Systemic

Risk

Sovereign

Risk

A

Assessment

t

Cascade

Effects

Probability

PoD from Supervisory Information

PLD Baseline Scenario

PLD Stressed Scenario

St

Stressed

dV

VaR

R

Expected Loss

Unexpected Loss

PLD Baseline Scenario

PLD Stressed Scenario

Stressed PoD

PoD

Benchmark

13

Systemic Stress Indicators: U.S. Financial Stability Index: Expected number of FIs in distress given that p

g

at least one became distressed (left scale).

Joint Probability of Distress (JPoD):

Likelihood of common distress of all the FIs in the system (right scale).

3.5

3.0

0.025

1.

2.

3.

4.

Bear Stearns episode (3/11/08)

Lehman Bankruptcy

p y and AIG bailout (9/15-16/08)

(

)

TARP I bill failure (9/30/08)

Global central bank intervention (10/8/08)

1

2 34

0.020

2.5

2.0

Bank Stability Index

(Number of banks, left scale)

0.015

1.5

0 010

0.010

1.0

JPoD

(Probability of default %, right scale)

0.005

0.5

0.0

Jan 07

Jan-07

0.000

May 07

May-07

Sep 07

Sep-07

Jan 08

Jan-08

May 08

May-08

Sep 08

Sep-08

14

Systemic Stress Indicators: Mexico

Financial Stability Index: Expected number of FIs in distress given that

Expected number of FIs in distress given that at least one became distressed (left scale).

Joint Probability of Distress (JPoD):

Likelihood of common distress of all the FIs in the system (right scale).

JPOD-FSI: México

FSI

BSI

4

35

3.5

3

2.5

2

1.5

1

0.5

0

1. Lehman spillover, derivatives’ market

crisis and mutual funds

funds’ crisis (Oct2008).

2. H1N1 crisis (March-April-2009).

JPOD

JPOD

0.002

1

2

0.0018

0.0016

0.0014

0.0012

0.001

0.0008

0.0006

0.0004

0.0002

0

15

Systemic Stress Indicators

They incorporate changes in distress‐dependence that are consistent with They

incorporate changes in distress dependence that are consistent with

the economic cycle.

30

3.0

Joint probability of distress

2.5

Average probability of distress

20

2.0

1.5

1.0

0.5

0.0

-0.5

-1.0

J

Jan-07

07

M

May-07

07

S

Sep-07

07

J

Jan-08

08

M

May-08

08

S

Sep-08

08

16

Contagion Indicators: DiDe U.S.

Distress Dependence Matrix: Probability that FI (row) falls in distress given that FI (column) falls in distress.

July 1 2007 September 12, 2008

July 1, 2007‐

September 12 2008

July 1, 2007

Citi

BAC

JPM

Wacho

WAMU

GS

LEH

MER

MS

AIG

Citigroup

Bank of America

JPMorgan

Wachovia

Washington Mutual

Goldman Sachs

Lehman

Merrill Lynch

y

Morgan Stanley

AIG

Column average

1.00

0.12

0 15

0.15

0.12

0.16

0.17

0.22

0.19

0.19

0.07

0.24

0.14

1.00

0 42

0.42

0.33

0.28

0.25

0.32

0.32

0.31

0.14

0.35

0.11

0.27

1 00

1.00

0.24

0.21

0.28

0.32

0.33

0.28

0.10

0.31

0.11

0.27

0 31

0.31

1.00

0.23

0.21

0.26

0.25

0.24

0.10

0.30

0.08

0.11

0 13

0.13

0.11

1.00

0.11

0.15

0.17

0.14

0.05

0.21

0.09

0.11

0 19

0.19

0.12

0.12

1.00

0.43

0.33

0.35

0.07

0.28

0.08

0.10

0 16

0.16

0.10

0.12

0.31

1.00

0.31

0.28

0.06

0.25

0.09

0.12

0 19

0.19

0.12

0.16

0.28

0.35

1.00

0.30

0.07

0.27

0.09

0.12

0 18

0.18

0.12

0.13

0.31

0.33

0.31

1.00

0.06

0.26

0.08

0.15

0 17

0.17

0.14

0.15

0.17

0.20

0.20

0.16

1.00

0.24

September 12, 2008

Citi

BAC

JPM

Wacho

WAMU

GS

LEH

MER

MS

AIG

Citigroup

Bank of America

JPMorgan

W h i

Wachovia

Washington Mutual

Goldman Sachs

Lehman

Merrill Lynch

Morgan Stanley

AIG

Column average

1.00

0.14

0.13

0 34

0.34

0.93

0.15

0.47

0.32

0 21

0.21

0.50

0.42

0.20

1.00

0.29

0 60

0.60

0.97

0.19

0.53

0.41

0 28

0.28

0.66

0.51

0.19

0.31

1.00

0 55

0.55

0.95

0.24

0.58

0.47

0 29

0.29

0.59

0.52

0.14

0.18

0.16

1 00

1.00

0.94

0.13

0.43

0.30

0 19

0.19

0.53

0.40

0.07

0.05

0.05

0 17

0.17

1.00

0.06

0.25

0.16

0 09

0.09

0.29

0.22

0.17

0.16

0.19

0 36

0.36

0.91

1.00

0.75

0.53

0 40

0.40

0.54

0.50

0.13

0.10

0.11

0 27

0.27

0.88

0.18

1.00

0.37

0 22

0.22

0.43

0.37

0.14

0.13

0.14

0 31

0.31

0.92

0.20

0.59

1.00

0 27

0.27

0.49

0.42

0.16

0.15

0.16

0 34

0.34

0.91

0.27

0.62

0.48

1 00

1.00

0.47

0.46

0.11

0.11

0.09

0 29

0.29

0.89

0.11

0.37

0.26

0 14

0.14

1.00

0.34

Row

average

0.19

0.24

0 29

0.29

0.24

0.26

0.31

0.36

0.34

0.33

0.17

0.27

Row

average

0.23

0.23

0.23

0 42

0.42

0.93

0.25

0.56

0.43

0 31

0.31

0.55

0.41

17

Contagion Indicators: DiDe Mexico

Distress Dependence Matrix: Probability that FI (row) falls in distress given that FI (column) falls in distress.

July 1, 2007‐ October 22, 2008

01/01/07

Banamex

BBVA

Santander

Banorte

HSBC

Inbursa

Scotiabank

ING

Bajío

Interacciones

IXE

Azteca

Prom

Columna

22/10/08

Banamex

BBVA

Bancomer

Santander

Banorte

HSBC

Inbursa

Scotiabank

Inverlat

ING

Bajío

Interacciones

IXE

Azteca

Prom

Columna

Banamex

BBVA

Santander

Banorte

HSBC

Inbursa

Scotiabank

ING

Bajío

Interacciones

IXE

Azteca

Prom

Renglón

1.00

0.25

0.25

0.24

0 27

0.27

0.18

0.31

0.25

0.31

0.11

0.11

0.19

0.26

1.00

0.72

0.29

0 42

0.42

0.15

0.25

0.47

0.42

0.11

0.12

0.19

0.25

0.69

1.00

0.29

0 41

0.41

0.16

0.25

0.44

0.41

0.11

0.11

0.19

0.24

0.28

0.29

1.00

0 27

0.27

0.18

0.23

0.28

0.31

0.11

0.11

0.18

0.27

0.40

0.41

0.26

1 00

1.00

0.15

0.25

0.37

0.61

0.11

0.11

0.18

0.18

0.14

0.16

0.17

0 15

0.15

1.00

0.16

0.15

0.22

0.11

0.10

0.22

0.32

0.24

0.25

0.22

0 26

0.26

0.17

1.00

0.23

0.29

0.11

0.12

0.17

0.25

0.45

0.44

0.27

0 36

0.36

0.15

0.23

1.00

0.36

0.11

0.11

0.18

0.30

0.39

0.40

0.30

0 60

0.60

0.22

0.28

0.36

1.00

0.10

0.11

0.43

0.11

0.11

0.11

0.10

0 11

0.11

0.12

0.11

0.11

0.11

1.00

0.11

0.10

0.11

0.11

0.11

0.11

0 11

0.11

0.11

0.12

0.11

0.11

0.11

1.00

0.11

0.19

0.18

0.19

0.18

0 18

0.18

0.23

0.17

0.18

0.43

0.10

0.11

1.00

0.29

0.35

0.36

0.29

0 35

0.35

0.23

0.28

0.33

0.38

0.18

0.18

0.26

0.29

0.37

0.36

0.29

0.34

0.23

0.28

0.33

0.38

0.18

0.18

0.26

0.29

Banamex

BBVA

Bancomer

Santander

Banorte

HSBC

Inbursa

Scotiabank

Inverlat

ING

Bajío

Interacciones

IXE

Azteca

Prom

Renglón

1.00

0.49

0.48

0.46

0.49

0.39

0.54

0.47

0.53

0.29

0.29

0.40

0.49

0.46

0.47

0.47

0.50

0.38

1.00

0.83

0.52

0.63

0.35

0.79

1.00

0.52

0.62

0.35

0.48

0.50

1.00

0.49

0.37

0.58

0.60

0.49

1.00

0.34

0.34

0.36

0.39

0.36

1.00

0.46

0.48

0.46

0.49

0.37

0.62

0.62

0.50

0.58

0.35

0.59

0.61

0.53

0.75

0.42

0.27

0.29

0.28

0.29

0.28

0.28

0.29

0.30

0.29

0.27

0.37

0.39

0.40

0.39

0.42

0.52

0.54

0.49

0.53

0.41

0.50

0.48

0.52

0.29

0.25

0.41

0.45

0.67

0.61

0.30

0.26

0.40

0.45

0.64

0.60

0.30

0.26

0.40

0.42

0.50

0.51

0.28

0.25

0.39

0.45

0.57

0.72

0.29

0.25

0.39

0.35

0.36

0.43

0.29

0.24

0.44

1.00

0.46

0.51

0.29

0.26

0.39

0.42

1.00

0.56

0.29

0.25

0.39

0.48

0.58

1.00

0.29

0.26

0.61

0.27

0.29

0.28

1.00

0.24

0.26

0.28

0.29

0.29

0.28

1.00

0.29

0.36

0.39

0.59

0.26

0.25

1.00

0.45

0.52

0.55

0.35

0.31

0.45

0.48

0.54

0.53

0.47

0.52

0.41

0.48

0.50

0.55

0.34

0.35

0.44

0.47

18

DiDe: Mexico

DiDe: México- IFs Españolas

MEXICO-BBVA

MEXICO-SANTANDER

Probabilida

ad

1

0.8

0.6

0.4

0.2

0

Jun-2007

Oct-2007

Feb-2008

Jun-2008

Oct-2008

Feb-2009

Jun-2009

Oct-2009

Feb-2010

Jun-201

DiDe: IF´s Españolas-México

Probabilidad

d

BBVA-MEXICO

SANTANDER-MEXICO

0.9

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

Jun-2007

Oct-2007

Feb-2008

Jun-2008

Oct-2008

Feb-2009

Jun-2009

Oct-2009

Feb-2010

Jun-201

Contagion Indicators: Spillover Coefficient

Spillover Coefficient (SC): Vulnerability of a country/FI given distress in other countries/Fis.

P(A)

P(B)

P(C)

CIMDO

Methodolog

y

P( A / A) P( A / B ) P( A / C )

P( B / A) P( B / B ) P( B / C )

P(C / A) P(C / B) P(C / C )

P(A,B,C) JPoD

P(A B); P(A,C);

P(A,B);

P(A C); P(B,C)

P(B C)

Bayes’

Bayes

Law

For e.g. country (A)/FI(A):

SC(A)=P(A/B)*P(B) + P(A/C)*P(C)

20

Contagion Indicators: SC Europe

Spillover Coefficient: European

p

p

Region

g

0.35

0.3

0.25

0.2

GER

GRE

0.15

IRE

SWE

0.1

0.05

0

03/01/05

03/01/06

03/01/07

03/01/08

03/01/09

03/01/10

21

Contagion Indicators: Contagion Index

Contagion Index (CI): Toxicity of the distress of a country/FI on other countries/FIs.

P(A)

P(B)

P(C)

CIMDO

Methodolog

y

P( A / A) P( A / B ) P( A / C )

P( B / A) P( B / B ) P( B / C )

P(C / A) P(C / B) P(C / C )

P(A,B,C) JPoD

P(A B); P(A,C);

P(A,B);

P(A C); P(B,C)

P(B C)

Bayes’

Bayes

Law

For e.g. country (A)/FI(A):

CI(A)=P(A)+P(B/A)*P(A) + P(C/A)*P(A)

22

Contagion Indicators: Probability of Cascade Effects

Probability of Cascade Effects (PCE): Probability that at least one FI becomes distressed given that a given FI becomes distressed.

PCE Lehman/AIG (September 12).

100

90

Lehman

AIG

80

70

60

50

40

30

20

10

9/1/2008

8

8/1/2008

8

7/1/2008

8

6/1/2008

8

5/1/2008

8

4/1/2008

8

3/1/2008

8

2/1/2008

8

1/1/2008

8

12/1/2007

7

11/1/2007

7

10/1/2007

7

9/1/2007

7

8/1/2007

7

7/1/2007

7

6/1/2007

7

5/1/2007

7

4/1/2007

7

3/1/2007

7

2/1/2007

7

1/1/2007

7

0

23

Output: Cross-region Spillovers

1.00

0.90

0.80

0.70

0.60

0.50

0 40

0.40

0.30

0.20

0.10

0.00

C it i-M exico

C it i-Lat

C it i-EE

i EE

5/

20

09

09

7/

9/

2/

2/

20

09

09

20

20

2/

2/

20

3/

11

1/

/2

2/

/2

00

8

09

08

08

20

20

2/

9/

7/

3/

2/

08

08

20

2/

2/

20

20

2/

1/

11

5/

7

08

07

00

/2

/2

07

20

2/

20

2/

7/

5/

9/

07

20

2/

20

20

2/

2/

3/

1/

07

C it i-A sia

07

Prob ab ility

Probability of dis tre s s of C itigrou p con dition al on dis tre s s of an oth e r e n tity

Probability of dis tre s s of an e n tity con dition al on dis tre s s of C itigrou p

0.60

Prob ab ility

0.50

0 40

0.40

B A C -C it i

0.30

U B S-C it i

0.20

D B -C it i

0.10

09

20

09

3/

9/

5/

7/

3/

3/

20

09

20

09

09

20

3/

1/

3/

3/

20

00

8

08

/2

11

9/

/3

3/

20

08

20

08

5/

7/

3/

3/

20

08

20

3/

20

3/

3/

11

1/

/3

/2

00

7

08

07

07

20

9/

7/

5/

3/

3/

20

07

07

20

3/

20

3/

1/

3/

3/

20

07

0.00

1.00

0.90

0.80

0.70

0.60

0.50

0.40

0.30

0.20

0.10

0 00

0.00

C it igroup

U BS

DB

09

3/

20

3/

20

09

9/

09

20

3/

5/

7/

09

09

20

3/

3/

20

8

00

/2

3/

1/

/3

11

9/

3/

20

08

08

08

20

3/

7/

5/

3/

20

08

3/

3/

20

08

00

1/

3/

20

7

07

11

/3

/2

07

20

3/

9/

20

3/

7/

20

3/

5/

20

3/

3/

07

07

BA C

07

20

3/

1/

Prob ab ility

C as cade Effe cts

24

Systemic Loss Indicators

Commercial Banking

PoD

Pension Funds

PoD

Mutual Funds

POD

Develpmt Bking Insurance Cos

PoD

POD

Brokers

PoD

Others

Financial System´s

Multivariate Density

EAD

LGD

Systemic

L

Loss

Si

Simulation

l ti

0 . 2

0 . 1 5

0 . 1

0 . 0 5

0

4

2

4

2

0

0

-2

-2

-4

Systemic Loss

Indicators

MCSR

-4

Systemic Stress

Indicators

Contagion

Indicators

Sovereign Risk

Indicators

25

Systemic Loss Indicators

E

Extreme Systemic Loss

S

i L

PLD

Independent IFs

PLD

Stressed PoDs

Independent IFs

PLD

Stressed PoDs

Stressed Distress Dependence

Expected Loss

Unexpected Loss

25-45%

26

14.0%

10.0%

1999Q2

2000Q1

2000Q4

2001Q3

2002Q2

2003Q1

2003Q4

2004Q3

2005Q2

2006Q1

2006Q4

2007Q3

2008Q2

2009Q1

2009Q4

2010Q3

2011Q2

2012Q1

2012Q4

2013Q3

2014Q2

2015Q1

2015Q4

Forecasted PoD Under Assumed

Macroeconomic Scenarios

Baseline

12.0%

Min

Mean

Max

8.0%

6.0%

4.0%

2.0%

0.0%

Risk-Neutral and Subjective PoD

0.045

0.040

0.035

Comparing Risk‐Neutral Default Probability and Adjusted Real‐world Probability

0.030

0.025

0.020

RN‐Median

0.015

Real‐Median

0.010

0.005

0.000

•

For loss estimation purposes, we convert risk neutral CDS-PoDs to subjective PoDs.

((Espinoza

p

and Segoviano,

g

, 2011).

)

Systemic Expected Losses

B li

Baseline

•

•

2007

2008

2009

2010

2011

2012

2013

$000

% Assets

27,144,218

0.22

123,251,952

0.96

58,981,703

0.45

109,916,227

0.84

77 632 877

77,632,877

0 59

0.59

33,721,172

0.26

22,758,454

0.17

T t l

Total

453 406 602

453,406,602

3 50

3.50

Ad

Adverse

% GDP

0.19

0.85

0.42

0.77

0 53

0.53

0.22

0.15

3 14

3.14

$000

% Assets

27,144,218

0.22

123,251,952

0.96

60,233,379

0.46

127,844,040

0.98

83 131 248

83,131,248

0 64

0.64

77,552,119

0.59

59,380,397

0.45

558 537 354

558,537,354

4 31

4.31

% GDP

0.19

0.85

0.43

0.90

0 57

0.57

0.52

0.39

3 84

3.84

Potential Losses the system

y

could incur.

Through-time pattern of losses is highly consistent with assumed

macroeconomic scenarios.

Systemic Unexpected Losses

2007

2008

2009

2010

2011

2012

2013

Bas eline

Advers e

VaR 99%

VaR 99%

$000

% As s ets

162 523 198

162,523,198

1.33

1

33

356,360,895

2.78

238,209,910

1.82

334,112,073

2.56

270 050 643

270,050,643

2 07

2.07

180,355,988

1.38

148,846,513

1.14

% GDP

1 15

1.15

2.47

1.70

2.34

1 84

1.84

1.20

0.97

$000

% As s ets

162 523 198

162,523,198

1.33

1

33

356,360,895

2.78

245,110,532

1.87

368,703,692

2.82

295 548 717

295,548,717

2 26

2.26

278,878,012

2.13

242,699,313

1.86

% GDP

1 15

1.15

2.47

1.74

2.59

2 02

2.02

1.85

1.57

1,690,459,220

13.07

11.67

1,949,824,359

15.06

13.40

Memo item

2009 total equity 1,022,994,436

7.82

7.28

1,022,994,436

7.82

7.28

Total

•

Extreme Losses that the system could incur with 1 percent probability.

•

Cumulative extreme losses could be significant in both scenarios, especially

compared to 2009 capital levels.

Marginal Contribution to Systemic Risk

Marginal Contribution to Systemic Risk (MCSR): It takes into account of size and interconnectedness.

Commercial Banking

PoD

Pension Funds

PoD

Mutual Funds

POD

Develpmt Bking Insurance Cos

PoD

POD

Brokers

PoD

Others

Financial System´s

Multivariate Density

EAD

LGD

Systemic

L

Loss

Si

Simulation

l ti

0 . 2

0 . 1 5

0 . 1

0 . 0 5

0

4

2

4

2

0

0

-2

-2

-4

Syste c Loss

Systemic

oss

Indicators

Expected Shortfall

Shapley Value

-4

Systemic Stress

Indicators

Contagion

Indicators

Sovereign Risk

Indicators

MCSR

31

Shapley Value

•

Let F be a sub-group of members of the financial system containing the financial institution I, we define the “contribution of institution I to F” as

V(F)-V(F-{I}).

The Shapley Value of institution I could be viewed as the weighted average of the contributions of I over all the sub-groups of the

financial system containing institution I.

Let´s assume three financial institutions A, B , C

Sub‐Group

Loss

Contribution A to Sub‐group

Contribution B to Sub‐group

Contribution C to Sub‐group

A

B

C

A,B

A,C

B,C

A,B, C

Shapley Value

MCSR

1

3

5

3.5

5.5

7

8.5

1

None

None

0.5

0.5

None

1.5

1

0.12

None

3

None

2.5

None

2

3

2.75

0.32

None

None

5

None

4.5

4

5

4.75

0.56

Permutation

Sub‐Group of all instituions before A including A

Sub‐Group of all instituions before A including A

Calculation of Contribution of A

Calculation of Contribution of A

Contribution of A

Contribution of A ABC

ACB

BAC

CAB

BCA

CBA

A

A

B,A

C,A

B,C,A

C,B,A

Shapley Value of A

V(A) ‐ V(0) = 1‐0 = 1 V(A) ‐ V(0) = 1‐0 = 1 V(B,A) ‐V(B) = 3.5 ‐ 3 = 0.5

V(C,A) ‐ V( C) = 5.5 ‐5=0.5 V(C,B,A) ‐ V(C,B) = 8.5 ‐ 7 = 1.5

V(C,B,A) ‐ V(C,B) = 8.5 ‐ 7 = 1.5

Weighted Average

1

1

0.5

0.5

1.5

1.5

1

MCSR

0.12

•

Additivity. The sum of the shapley values of all the members of our financial system gives us the systemic risk of all the financial system.

•

Intuitive Indicator. The Shapley Value of a financial institution captures the systemic importance of it in only one number.

•

Flexibility. Can be applied to any measure of system-wide risk.

Marginal Contribution to Systemic Risk

Marginal Contribution to Systemic Risk:

g

y

It takes into account of size and interconnectedness.

0.4

0.016

0.35

0.014

0.3

0.012

0.25

0.01

0.2

0.008

0.15

0.006

0.1

0.004

0.05

0.002

MCSR

POD AIG

Spearman Corr AIG

Mar-09

Feb-09

Jan-09

Dec-08

Nov-08

Oct-08

Sep-08

Aug-08

Jul-08

Jun-08

May-08

Apr-08

Mar-08

Feb-08

Jan-08

0

Dec-07

0

Contagion Index AIG

Right Axis for CI

AIG Factors

Second-Round Effects

Macroeconomic

Factors

Comm Banks

PoD

Dvlpmt Banks

PoD

GSEs

PoD

Financial System’s

Returns

Pension Funds

PoD

Insurance

PoD

Mutual Funds

PoD

Financial System´s

Tail Risk (JPoD)

Macroeconomic

Factor

Comm Banks

PoD

Exposures

Financial

Factors

Dvlpmt Banks

PoD

LGDs

Systemic

Loss Simulation

Marginal Contribution

to Systemic Risk

GSEs

PoD

Financial

Factors

Pension Funds

PoD

Insurance

PoD

Mutual Funds

PoD

Financial System´s

y

Multivariate Density

Financial System’s

Loss Distribution

Financial Stability

Measures

34

Financial Stability Measures: Additional Applications

Additional Applications:

1.

Macro‐Financial stages over time.

2.

Spillovers between the banking and corporate sectors.

3.

Sovereign Risk Assessment (Caceres Guzzo Segoviano IMF WP 10/120)

(Caceres, Guzzo, Segoviano, IMF WP 10/120).

35

Financial Stability Over Time

•

Markov Switching VAR

Definition of alternative risk zones given specific values of JPoD

and

d other

th variables

i bl

0.002

MSIAH(2)-VAR(1), 1999 (7) - 2009 (3)

Jpodrev

dlhouse

0.000

-0.002

1.0

2000

2001

2002

Probabilities of Regime 1

filtered

predicted

2003

2004

2005

2006

2007

2008

2009

2003

2004

2005

2006

2007

2008

2009

2003

2004

2005

2006

2007

2008

2009

smoothed

0.5

1.0

2000

2001

2002

Probabilities of Regime 2

filtered

predicted

di d

smoothed

0.5

2000

•

•

2001

2002

Probability of being in different economic

actual/assumed ((in ST)) economic shocks.

Analysis of IRFs in different enconomic regimes

regimes

due

to

36

10/1/2009

7/1/2009

4/1/2009

1/1/2009

10/1/2008

7/1/2008

4/1/2008

1/1/2008

10/1/2007

7/1/2007

4/1/2007

1/1/2007

10/1/2006

7/1/2006

0.7

4/1/2006

1/1/2006

10/1/2005

7/1/2005

4/1/2005

1/1/2005

10/1//2009

7/1//2009

4/1//2009

1/1//2009

10/1//2008

7/1//2008

4/1//2008

1/1//2008

10/1//2007

7/1//2007

4/1//2007

1/1//2007

10/1//2006

7/1//2006

4/1//2006

1/1//2006

10/1//2005

7/1//2005

4/1//2005

1/1//2005

Spillovers Between Financial

and Corporate Sectors

0.08

PoD: Banks & Corporates

0.07

0.06

0.05

0.04

0.03

Average Bank

0.02

Average Corp

0.01

0.00

Distress Dependence: Banks & Corporates

0.6

0.5

0.4

0.3

Bank-Bank

02

0.2

Bank-Corp

Corp-Bank

Corp

Bank

0.1

Corp-Corp

0

37

Sovereign Risk Assessment: Four Phases

EUR Sovereign 10Y Swap Spreads

1,000

800

600

400

200

GER

FRA

ITA

SPA

NET

BEL

AUT

GRE

IRE

POR

Sovereign

Risk

Systemic

Response

p

Systemic

Outbreak

Financial Crisis Build‐Up

0

Jul‐22010

May‐22010

Mar‐22010

Jan‐22010

Nov‐22009

Sep‐22009

Jul‐22009

May‐22009

Mar‐22009

Jan‐22009

Nov‐22008

Sep‐22008

Jul‐22008

May‐22008

Mar‐22008

Jan‐22008

Nov‐22007

Sep‐22007

Jul‐22007

‐200

38

Some Existing Literature on Sovereign Spreads

• Models with Risk Aversion based on observable measures ( corporate –

(e.g

t Treasury spread):

T

d)

– Fiscal situation has temporary and limited impact on sovereign spreads (Afonso and Strauch, 2004).

spreads (Afonso

and Strauch, 2004).

– Short‐term interest rates are the main driver (Manganelli and Wolswijk, 2007) but international risk factors and liquidity premia

also matter (Bernoth et al., 2004).

– Sovereign spreads widen when the prospects of a domestic financial sector worsen (Mody 2009)

sector worsen (Mody, 2009).

Risk Aversion as a common factor:

Aversion as a common factor:

• Risk

– common factor using a Kalman filter (Geyer et al, 2004). y g

y

g

– Time‐varying common factor estimated with Bayesian filtering technique (Sgherri and Zoli, 2009).

39

Data and Construction of the Variables:

3 Types of ‘Measures’

• Measure of “contagion”: the Spillover Coefficient (SC). Segoviano and Goodhart, IMF WP 09/4.

g

• Measure of “risk aversion”: the Index of Risk Aversion (IRA).

f

( )

(Espinoza and Segoviano, IMF WP, forthcoming 2011).

• Country‐specific fiscal fundamentals:

– Overall Budget Balance (% of GDP).

Overall Budget Balance (% of GDP).

– Public Debt (% of GDP).

40

The Index of Risk Aversion (IRA)

Espinoza and Segoviano, IMF WP forthcoming, 2011.

• Global risk aversion proxies tend to be ‘over simplistic’ (e.g. US corporate bond spreads to Treasuries).

• Statistically sophisticated methods depend on the sample: global risk aversion is assigned to a common trend

g

or common factor

f

((i.e. ‘filtering’).

– common factors might be capturing ‘distress dependence’ as well as ‘risk aversion’

• O

Our IRA is the ‘factor’ linking risk‐neutral probabilities (extracted IRA i th ‘f t ’ li ki

ik

t l

b biliti ( t t d

e.g. from CDS spreads) to the actual probabilities of nature . This

factor is the market price of risk in situations of distress

p

– It does not depend on the sample used

41

The Index of Risk Aversion (IRA)

• The price of an asset reflects

– Market expectations of the asset´s returns – The price of risk: what investors are willing to pay for receiving income in distress states of nature. The linear (one factor) pricing and the risk‐neutral pricing formulae

1

Pt Et [mt 1 xt 1 ] t 1 ( s )mt 1 ( s ) xt 1 ( s )

t 1 ( s ) xt 1 ( s )

F

1 rt s

s

t1(s)mt1(s)

where is the price of a security paying $1 in state s

and

t 1 ( s ) (1 rt F ) t 1 ( s )mt 1 ( s )

is the risk‐neutral probability that is given by CDS spreads

42

The Index of Risk Aversion (IRA)

• Market price of risk under distress:

Et mt 1 | distress Et mt 1 | mt 1

( t )

Et mt 1 vart (mt 1 )

1 1[ t ]

where t

t Et (mt 1 )

vart (mt 1 )

(1)

(2)

• The threshold τ can be exogenous, or such that the probability that the market‐price of risk exceeds the threshold p

τ is equal to q

the actual probability of distress:

t Et (mt 1 ) 1[1 t ] * var(mt 1 )

(3)

43

The Index of Risk Aversion (IRA)

• Market price of risk under distress:

mt

Et ( mt 1 | mt 1 )

Et (mt 1 )

t 1

(1 rt F ) t 1

1[1 t ] * var(mt 1 )

44

The Index of Risk Aversion (IRA)

Et[mt+1 | mt+1 > τ]

3.2

3.0

2.6

2.8

2.4

2.2

2.0

1.8

45

Estimation: Methodology

• Simple GARCH(1,1) model to estimate sovereign swap (Yt) spreads as a function of: – its lag Yt‐1

– The Spillover Coefficient p

– Index of Risk aversion

Xt

– debt/GDP and fiscal balance

debt/GDP and fiscal balance

Yt Yt 1 ' X t t

t2 t21 t21

• Estimated by Maximum Likelihood

46

Estimation: Main Results

GER

Mean equation:

Constant

Lag dep.variable

IRA

SC

Overall balance

Debt ratio

-0.122***

(0 025)

(0.025)

0.933***

(0.006)

-0.217***

(0 034)

(0.034)

0.083***

(0.026)

-0.002***

(0 001)

(0.001)

0.000

(0.000)

Variance

V

i

equation:

i

Constant

0.000***

(0.000)

ARCH term

0.381***

(0 034)

(0.034)

GARCH term

0.702***

(0.017)

R-squared

d

No. of observations

0.981

0

981

1,194

FRA

ITA

SPA

NET

-0.042**

(0 019)

(0.019)

0.971***

(0.005)

-0.202***

(0 032)

(0.032)

0.176***

(0.034)

-0.002***

(0 001)

(0.001)

0.001**

(0.000)

0.039

(0 030)

(0.030)

0.981***

(0.005)

-0.046

(0 038)

(0.038)

0.137***

(0.035)

-0.002***

(0 001)

(0.001)

0.001*

(0.000)

-0.140***

(0 013)

(0.013)

0.943***

(0.008)

-0.074***

(0 027)

(0.027)

0.268***

(0.037)

-0.000

(0 000)

(0.000)

0.002***

(0.000)

-0.077***

(0 015)

(0.015)

0.966***

(0.005)

-0.118***

(0 033)

(0.033)

0.154***

(0.030)

-0.000

(0 000)

(0.000)

0.000**

(0.000)

0.000***

(0.000)

0.095***

(0 007)

(0.007)

0.918***

(0.005)

0.000***

(0.000)

0.074***

(0 007)

(0.007)

0.933***

(0.005)

0.000*** 0.000***

(0.000)

(0.000)

0.283*** 0.089***

(0 023)

(0.023)

(0 009)

(0.009)

0.789*** 0.926***

(0.014)

(0.006)

0.984

0

984

1,194

0.993

0

993

1,194

0.992

0

992

1,194

0.986

0

986

1,194

47

Estimation: Main Results (2)

BEL

Mean equation:

Constant

GRE

IRE

POR

-0.028

(0 034)

(0.034)

0.962***

(0.006)

-0.098***

(0 032)

(0.032)

0.177***

(0.025)

-0.002***

(0.000)

0.000

(0.000)

-0.258***

(0 035)

(0.035)

0.956***

(0.006)

-0.052

(0 035)

(0.035)

0.579***

(0.073)

-0.001*

(0.000)

0.002***

(0.000)

-0.059*

(0 030)

(0.030)

1.008***

(0.004)

-0.053**

(0 024)

(0.024)

0.183***

(0.037)

0.002***

(0.000)

0.000

(0.000)

Variance equation:

Constant

0.000*** 0.000***

(0.000)

(0.000)

ARCH term

0 113*** 0.076

0.113

0 076***

(0.011)

(0.007)

GARCH term

0.913*** 0.935***

(0.008)

(0.005)

0.000***

(0.000)

0 066***

0.066

(0.005)

0.945***

(0.004)

0.000*** 0.000***

(0.000)

(0.000)

0 289*** 0.150

0.289

0 150***

(0.023)

(0.010)

0.800*** 0.885***

(0.011)

(0.005)

Lag dep. variable

IRA

SC

Overall balance

Debt ratio

-0.090***

(0 016)

(0.016)

0.953***

(0.007)

-0.097***

(0 032)

(0.032)

0.278***

(0.024)

-0.000

(0.001)

0.000*

(0.000)

AUT

R-squared

0.991

No. of observations 1,194

0.993

1,194

0.996

1,194

0.998

1,194

-0.018

(0 020)

(0.020)

0.950***

(0.007)

-0.316***

(0 035)

(0.035)

0.631***

(0.059)

0.000

(0.000)

-0.002***

(0.000)

0.993

1,194

48

Global Risk Aversion, Contagion or Fundamentals?

Contributions to 10-year Swap Spread

3.0

2.5

2.0

15

1.5

1.0

0.5

0.0

-0.5

-1.0

-1.5

20

-2.0

-2.5

Germany

Jul 07 Sep 08 Oct 08 Mar

09

Fundamentals

Contagion

Apr 09 Sep Oct 09 Feb 10

09

Global Risk Aversion

49

Global Risk Aversion, Contagion or Fundamentals?

Contributions to 10-year Swap Spread

8.0

Italy

6.0

4.0

2.0

0.0

-2.0

-4.0

-6.0

-8.0

Jul 07 Sep 08 Oct 08 Mar Apr 09 Sep Oct 09 Feb 10

09

09

Fundamentals

Contagion

g

Global Risk Aversion

50

Global Risk Aversion, Contagion or Fundamentals?

Contributions to 10-year Swap Spread

250.0

200.0

150.0

100.0

50.0

0.0

-50.0

50.0

-100.0

-150.0

-200.0

-250.0

250 0

-300.0

Greece

Jul 07 Sep 08 Oct 08 Mar

09

Fundamentals

Contagion

Apr 09 Sep Oct 09 Feb 10

09

Global Risk Aversion

51

Global Risk Aversion, Contagion or Fundamentals?

Contributions to 10-year Swap Spread

20.0

Ireland

15.0

10.0

5.0

0.0

-5.0

-10.0

Jul 07 Sep 08 Oct 08 Mar

09

Fundamentals

Contagion

Apr 09 Sep Oct 09 Feb 10

09

Global Risk Aversion

52

Estimation: Index of Risk Aversion

• When Risk Aversion rises, swap spreads widen, as sovereign yields fall further below swap yields (flight‐to‐quality leads to i ld f ll f th b l

i ld (fli ht t

lit l d t

capital flowing away from risky assets).

• Not the case for some high‐debt, lower‐rated issuers (notably Greece and Italy) that do not benefit from flight‐to‐quality. • Outside the euro area, the US and the UK benefit from rising Risk Aversion. For Sweden (and to some extent Japan), risk aversion is (

)

not significant.

• The impact of the IRA on US swap spreads is larger than the impact on the spreads for the other three countries (US is a “safe p

p

haven”).

53

Estimation: Contagion and Fundamentals

• Contagion: sovereign bond yields rise when the probability

of a credit event rises (because of contagion from another sovereign issuer). • High‐debt, lower‐rated sovereigns exhibit larger sensitivities as these countries are vulnerable to even remote probabilities of distress among higher‐rated issuers.

• Fundamentals : significant relationship with sovereign spreads. Wh b d t d fi it i

When budget deficits increase, sovereign bond yields rise i b d i ld i

(versus swap yields).

54

But Contagion from Where?

• Contagion can further broken down across sources of g

distress.

• For a given probability of distress in a specific sovereign, we find the most significant sources of contagion.

• Our measure of distress dependence (contributions to the changes in each country’s SC) taken from the Contagion Matrices.

55

Contagion from Where? Systemic outbreak (1)

– October 2008‐March 2009: countries weighing adversely on other sovereigns were those whose financial institutions were hit hard by the

sovereigns were those whose financial institutions were hit hard by the financial crisis (Austria, Ireland, and Italy).

USA

JPN

UK

GER

FRA

ITA

SPA

NET

BEL

AUT

GRE

IRE

O

POR

SWE

AVG

USA JPN

5.2

3.7

3.7

5.3

55

5.5

48

4.8

4.1

5.1

3.5

5.3

34

3.4

51

5.1

4.1

5.0

3.6

5.5

39

3.9

58

5.8

3.4

5.9

3.8

5.9

3.2

5.6

4.1

5.1

3.5

5.0

UK

8.3

8.4

8.8

8

8

8.8

9.2

89

8.9

9.4

8.9

91

9.1

8.6

9.1

8.5

9.4

8.3

GER FRA ITA

7.2

5.6

8.1

4.5

5.0

8.9

5.1

5.4

9.7

65

6.5

88

8.8

6.2

8.7

4.9

5.1

52

5.2

57

5.7

92

9.2

5.4

6.2

9.7

5.1

5.5

8.9

46

4.6

4 8 10

4.8

10.4

4

4.4

4.7

9.7

4.5

4.5 10.2

4.9

5.4

8.6

5.2

5.7

9.7

4.6

4.9

8.7

SPA NET BEL AUT GRE IRE POR SWE

6.4

8.4

6.7 11.4 7.6 11.0 5.2

9.0

6.8

7.3

7.1 12.2 9.4 12.2 6.5

7.9

7.4

8.6

7.2 11.9 8.6 11.8 6.1

9.2

74

7.4

84

8.4

7 2 10.3

7.2

10 3 7.5

7 5 10.0

10 0 6.1

61

87

8.7

7.8

9.2

7.3 10.2 7.6

9.4

6.4

9.1

7.3

8.4

6.9 12.9 9.2 12.5 5.9

9.0

85

8.5

6 7 12.4

6.7

12 4 8.7

8 7 11.5

11 5 5.8

58

92

9.2

7.8

7.9 10.7 8.0 10.6 6.4

8.9

6.8

8.8

12.0 8.5 11.5 5.9

9.0

79

7.9

75

7.5

75

7.5

9 8 13.5

9.8

13 5 7.0

70

83

8.3

7.3

7.3

7.0 12.8

14.3 6.5

8.1

7.4

7.5

7.2 13.8 11.0

6.5

8.5

6.8

8.1

6.7 12.7 9.0 11.6

8.7

7.9

8.3

7.5 11.2 8.3 11.3 6.4

6.8

7.5

6.6 11.1 8.2 10.9 5.8

8.0 56

Conclusions

• Readily implementable in terms of data needs.

• Reliable in the sense of being robust under data‐restricted environments.

• Interpretable, so that the approach itself and its output can be used as an input to policy development. • Incorporates distress dependence among FIs and its changes across the economic cycle.

• Includes all the relevant IFs and Sectors.

• Framework

Framework that produces complementary measures in a consistent that produces complementary measures in a consistent

manner.

• Integrates

Integrates complementary information (micro‐founded supervisory data complementary information (micro‐founded supervisory data

and market‐based).

57

Conclusions (ctd.)

• Debt sustainability and appropriate management of sovereign balance sheets are necessary conditions for preventing sovereign risk from feeding back into broader financial stability concerns.

• Rising sovereign risk requires credible medium‐term fiscal consolidation plans as well as a solid public debt management framework.

• Emphasis should be given to the presence of significant contingent risk on sovereign balance sheets and the need for sovereigns to gradually disengage

sovereign balance sheets and the need for sovereigns to gradually disengage from a number of measures supporting the financial sector.

• Immediate steps should be taken to reduce the possibility of projecting longer‐

term sovereign credit risks into short‐term financing concerns.

58

References

•

•

•

•

•

•

•

•

•

Afonso A. and Strauch, R. (2004). “Fiscal Policy Events and Interest Rate Swap Spreads: Evidence from the EU”, ECB Working Paper, No.303.

Athanosopoulou, M., Segoviano, M., and Tieman A., (2011), “Banks’ Probability of Default: Which Methodology, When, and Why?”, IMF Working Paper (forthcoming).

Bernoth K., von Hagen, J. and Schuknecht, L. (2004), “Sovereign Risk Premia in the European Government Bond Market”, ECB Working Paper, No. 369.

Cáceres, C., Guzzo, V., Segoviano, M., (2010), “Sovereign Spreads: Global Risk Aversion, Contagion or Fundamentals?”, IMF Working Paper WP/10/120.

Cochrane, J. (2001). Asset Pricing, Princeton: NJ, Princeton University Press

Codogno, L., Favero, C. and Missale, A. (2003). “Yield

Codogno, L., Favero, C. and Missale, A. (2003). Yield spreads on EMU spreads on EMU

governments bonds”, Economic Policy, October, 505‐32.

Afonso A. and Strauch, R. (2004). “Fiscal Policy Events and Interest Rate Swap Spreads: Evidence from the EU”, ECB Working Paper, No.303.

Spreads: Evidence from the EU

ECB Working Paper No 303

Bernoth K., von Hagen, J. and Schuknecht, L. (2004), “Sovereign Risk Premia in the European Government Bond Market”, ECB Working Paper, No. 369.

Espinoza R and Segoviano M (2011) “Probabilities of Default and the Market

Espinoza, R. and Segoviano, M. (2011). “Probabilities of Default and the Market Price of Risk in a Distressed Economy”, IMF Working Paper, (forthcoming).

59

References

•

•

•

•

•

•

•

•

Geyer, A., Kossmeier, S., and Pichler, S. (2004). “Measuring systematic risk in EMU government yield spreads”, Review of Finance, 8, 171‐97.

Goodhart, C., Hofmann, B. and Segoviano, M. (2004), “Bank

Goodhart, C., Hofmann, B. and Segoviano, M. (2004), Bank Regulation and Regulation and

Macroeconomic Fluctuations,” Oxford Review of Economic Policy, Vol. 20, No. 4, pp. 591–615.

Goodhart, C., Hofmann B., and Segoviano M., (2006), “Default, Credit Growth, and Asset Prices”, IMF Working Paper 06/223.

and Asset Prices

IMF Working Paper 06/223

Manganelli S. and Wolswijk, G. (2007). “Market Discipline, Financial Integration and Fiscal Rules: What Drives Spreads in the Euro Area Government Bond M k t?” ECB W ki P

Market?”, ECB Working Paper, No. 745.

N 745

Mody A. (2009). “From Bear Stearns to Anglo Irish: How Eurozone Sovereign Spreads Related to Financial Sector Vulnerability”, IMF Working Paper, 09/108

Schuknecht, L., von Hagen, J., and Wolswijk, G. (2010). “Government bond risk premiums in the EU revisited. The impact of the financial crisis”, ECB Working Paper, No. 1152. Segoviano, M. (2006). “Consistent Information Multivariate Density Optimizing Methodology”. Financial Markets Group, Discussion Paper No. 557.

Segoviano, M. and Goodhart, C. (2009). “Banking Stability Measures”, IMF Working Paper, 09/4.

60

References

•

•

•

•

Segoviano, M., (2006), “The Conditional Probability of Default Methodology,” Financial Markets Group, London School of Economics, Discussion Paper 558.

Financial Markets Group, London School of Economics, Discussion Paper 558.

Segoviano, M., (2011), “The CIMDO‐Copula. Robust Estimation of Default Dependence under Data Restrictions”, IMF Working Paper (forthcoming).

Segoviano, M. and Padilla, P., (2006), “Portfolio Credit risk and Macroeconomic Sh k A li i

Shocks: Applications to Stress Testing under Data Restricted Environments,” IMF S

T i

d D

R

i dE i

” IMF

Working Paper 06/283.

Sgherri, S. and Zoli, E. (2009). “Euro Area Sovereign Risk During the Crisis”, IMF Working Paper, 09/222.

g p , /

61