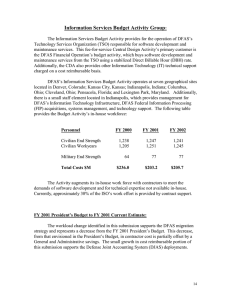

Defense Working Capital Fund Pricing in the Defense Finance and Accounting Service

advertisement