Transparent, Activity-Based Budget System Session 5: TABBS Operating Budget Model www.usask.ca/tabbs www.usask.ca

advertisement

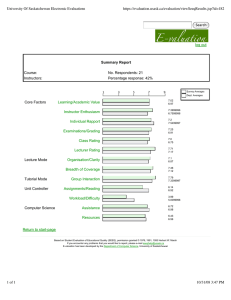

Transparent, Activity-Based Budget System www.usask.ca/tabbs Session 5: TABBS Operating Budget Model April 19, 2012 www.usask.ca Overview: Review of Critical Design Features’ Recommendations Example of College of Pharmacy and Nutrition Format of TABBS Operating Budget Model Scenario Analysis example Phase Three Next Steps Question/Answer Breakout Session Closing www.usask.ca 2 Within TABBS model: Operating Budget 2010/11 www.usask.ca 3 Strategic Envelope Academic Priorities Fund Including Strategic Research Fund (1.5% of operating budget revenue) Strategic Envelope (3.5% of operating budget revenue) RenewUS (1% of operating budget revenue) Balancing Fund Strategic Initiatives (1% of operating budget revenue) Other Strategic Initiatives www.usask.ca 4 Within TABBS model: All expenses allocated out Indirect Costs: 42% Direct Costs: 57% Operating Budget 2010/11, $387M www.usask.ca 5 Review of Critical Design Features Responsibility Centres Provincial Operating Grant Allocation Integration of Research Tuition Revenue Allocation Expenses Strategic Envelope Governance Transition/Implementation www.usask.ca 6 TABBS Operating Budget Model Responsibility Centres (RCs): Overview TABBS is a “responsibility centre management” model a) b) c) Places unit-level control within the budgeting structure and management structure Aligns authority over revenues and costs with the responsibility for revenues and costs (i.e. to Responsibility Centres) The establishment of Responsibility Centres is a key component of responsibility centre management, planning, and budgeting www.usask.ca 7 TABBS Operating Budget Model RC Recommendation A Revenue Centre is an RC whereby the majority of activities result in the generation of external revenues. A Support Centre is an RC that generates little or no external revenue but which provide critical services to support the activities of the Revenue Centres and other Support Centres. www.usask.ca 8 TABBS Operating Budget Model Current RC Classification (condensed) Revenue Centres Colleges/schools Some research centres (e.g. Toxicology Centre, VIDO) Support Centres Administrative units (e.g. FSD, FMD, ITS, HR, IPA) College of Graduate Studies & Research Consumer Services Division University Library/University Archives CCDE (Community Programming/ Language Centre) President’s Office (and other VP offices) Etc… CCDE (credit programming) Etc… www.usask.ca 9 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION REVENUE CENTRE www.usask.ca 10 TABBS Operating Budget Model Provincial Operating Grant Recommendation Allocate the core provincial operating grant, less a portion for strategic initiatives, to revenue centers based on their teaching and research activity as compared to other revenue centres. Allocate the directed funding, less a portion for strategic initiatives, to the revenue centres as indicated in the provincial grant. Allocate the targeted funding as instructed in the provincial grant. www.usask.ca 11 TABBS Operating Budget Model Provincial Operating Grant Allocation Infrastructure Instruction 70% 25% Instruction 45% 10% Research 30% Research 20% www.usask.ca 12 TABBS Operating Budget Model Allocation of Instruction: Steps 1.) Determine Cost Support for faculty & staff support resources (based on # of FLEs and ratios per discipline) Calculate as percentage of all revenue centres 2.) % of Cost support x Operating Grant amount (including tuition expectation) 3.) Minus Tuition Expectation (per discipline factors) = Instruction allocation of Operating Grant www.usask.ca 13 TABBS Operating Budget Model Allocation of Instruction Step 1: Support for Faculty Resources College of Pharmacy & Nutrition FLEs Faculty FTE Entitlement Instructional Support Cost Total Instruction (FLEs x student : faculty ratio) (FTEs x salary x discipline multiplier*) (total faculty + instructional support) UG 460.9 17.94 Masters 26.3 2.02 Doctoral 17.3 2.10 • • • • $2,101,670 + $1,032,215 $1,032,215 = $3,133,885 Teaching activity will be measured by student full-load equivalency Weights and multipliers employed by SUFM will be used Social Sciences is the baseline: 1 faculty resource for every 40 FLEs * faculty ratio and discipline multiplier differ based on discipline www.usask.ca 14 TABBS Operating Budget Model Allocation of Instruction Total Tuition Expectation: $76,321,441 Step 2: Tuition Expectation College of Pharmacy & Nutrition FLEs UG 460.9 Masters 26.3 Doctoral 17.3 Tuition Weightings Tuition Expectation (FLEs x tuition fee unit factorper discipline) (tuition weighting x avg tuiton fee) Tuition adj for Grant amount (% tuition exp x grant’s total tuition expectation) 662.2 $3,007,938 29.4 $2,849,722 Or 3.7% 19.4 • Tuition Expectation employed by SUFM will be used • Highlighted weighting represents the base tuition fee • *Tuition fee unit factor varies per discipline www.usask.ca 15 TABBS Operating Budget Model Allocation of Instruction Instruction portion of Grant (incl tuition): $220,905,830 Step 3: Instruction Portion College Pharmacy Cost Total Instruction (step 1) $3,133,885 % of Cost Total 3.77 Tuition Expectation adj for Grant amount (step 2) $2,849,722 Instruction Portion of Grant (% x Total Instruction portion of Actual Grant – Tuition adj) $5,468,748 % of allocation 3.78 • Total Instruction portion of actual grant includes the instructional support and tuition expectation www.usask.ca 16 TABBS Operating Budget Model Allocation of Research Portion Tri-Agency & Non-Tri-Agency Activity 33% Tri-Agency Activity 67% www.usask.ca 17 TABBS Operating Budget Model Allocation of Research • 67% ($41M) allocated on research dollar of total Tri-Agency • 33% ($21M) allocated on research dollar of total Tri-Agency plus non-Tri-Agency Step 1 Pharmacy Step 2 Pharmacy Tri Non-Tri Total Tri & Non-Tri Total % $450,173 $971,793 $1,421,966 1.8% 67% 33% Total Distribution Total % $975,443 $363,948 $1,339,391 2.2% www.usask.ca 18 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION PROVINCIAL OPERATING GRANT: INSTRUCTION $5,468,748 RESEARCH $1,339,391 DIRECTED FUNDING $0 TARGETED FUNDING $0 TOTAL AMOUNT ALLOCATED: $ 6,808,139 www.usask.ca 19 TABBS Operating Budget Model Tuition Recommendation To allocate tuition revenue to RCs based on enrolment and instructional activity for undergraduate students, and enrolment, instruction, and supervisory activity for graduate students as follows: www.usask.ca 20 TABBS Operating Budget Model Tuition Allocation Methodology PHARMACY Undergraduate/ Non-Degree Enrolment 25% Instruction 75% Student’s College of Enrolment Home College/Unit of Instructor of Course $721,194 $2,130,115 $2,851,309 Tuition Enrolment 40% Graduate Instruction 20% Supervision 40% Student’s College of Enrolment $63,782 Home College/Unit of Instructor of Course2 $28,654 Supervisor’s College/Unit1 $72,279 $164,715 1. If no supervisor is assigned, or the supervisor’s home college/unit cannot be determined, then 40% will default to the student’s college of enrolment. 2. If no instructional activity exists (i.e. no active courses enrolled), then 20% will default to the student’s college of enrolment. www.usask.ca 21 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION TOTAL REVENUE ALLOCATED IN TABBS: PROVINCIAL OPERATING GRANT $ 6,808,139 TUITION REVENUE $ 3,016,024 TOTAL REVENUE ALLOCATED $ 9,824,163 www.usask.ca 22 TABBS Operating Budget Model Revenue Centre within TABBS: www.usask.ca 23 TABBS Operating Budget Model Expenses Recommendation Direct and indirect expenses will be allocated to the revenue centers whose activities generate those expenditures. Direct expenditures will continue to be directly funded by revenue centres. Indirect expenditures will be allocated using activity measures (cost drivers) that recognizes the revenue centre’s proportionate share of indirect expenditures. www.usask.ca 24 Cost Bins: TABBS Operating Budget Model Indirect costs are placed into common cost groupings (cost bins) based upon activity supported by those costs (e.g. support of students, support of faculty and staff, etc.) Expense Source Cost Bins Student Support Bin Budgeted Direct Expenses of Support Centres and Central Expense Funds Faculty/Staff Support Bin Research Support Bin Occupancy Costs Bin General Support Bin www.usask.ca 25 TABBS Operating Budget Model Indirect Cost Allocation www.usask.ca 26 TABBS Operating Budget Model Indirect Cost Allocation Continued… www.usask.ca 27 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION INDIRECT COSTS Research Support Cost Bin Activity Allocation Driver 1,303,474 $ 0.2032 264,901 515 $ 2,315 1,192,472 61 $ 727 44,340 6,267,087 $ 0.0639 400,622 General Occupancy Costs Sub-bin- based on total NASM 3,578 $ 107 381,592 Utilities Sub-bin- based on NASM per building for RC Electrical NASM Steam NASM Chilled Water NASM Water NASM Gas NASM Heating-other NASM 3,578 3,578 3,578 3,578 3,578 3,578 Based on Research Expenditures ($) Student Support Cost Bin (incl Classroom Costs) $ Based on Student Headcount Enrolled -ALL Based on Student Headcount Enrolled -Graduate Faculty/Staff Support Cost Bin Based on Salary Expenditures ($) Occupancy Cost Bin $ Caretaking Sub-bin- based on NASM per building for RC Leases Sub-bin- based on NASM per building for RC Health Sciences Holding Bin 214,234 3,578 - $ - 32 115,391 - Based on Operating Expenditures ($) General Support Cost Bin $ 8,570,158 $ 0.0060 51,268 Based on Operating Expenditures ($) Total Indirect Costs $ 8,570,158 $ 0.0749 641,907 3,306,728 www.usask.ca 28 TABBS Operating Budget Model TABBS Model Reference Level (TMRL) Implied funding level through the allocation of operating budget revenue and allocation of indirect expenses in TABBS. Provincial Operating Grant Allocation + Tuition Revenue Allocation – Indirect cost allocation = TMRL www.usask.ca 29 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION TABBS MODEL REFERENCE LEVEL (TMRL) TOTAL REVENUE ALLOCATION $ 9,824,163 - TOTAL INDIRECT COSTS $3,306,728 = TABBS MODEL REFERENCE LEVEL: $ 6,517,435 www.usask.ca 30 TABBS Operating Budget Model Current Operating Budget Allocation Historically adjust annually for a) b) c) Salary/benefit incremental increases Economic changes Strategic priority funding For Pharmacy and Nutrition: $4,822,710 www.usask.ca 31 Example: College of Pharmacy & Nutrition COLLEGE OF PHARMACY & NUTRITION DIFFERENCE BETWEEN TMRL & CURRENT BUDGET ALLOCATION TABBS MODEL REFERENCE LEVEL $ 6,517,435 - CURRENT OPERATING BUDGET ALLOCATION (DIRECT COSTS) $4,822,710 = DIFFERENCE BETWEEN TMRL & CURRENT BUDGET ALLOCATION $ 1,694,725 www.usask.ca 32 What the Model is and is not Represents actual activity levels in the past a) b) How revenue actually is received by the university Actual operating budgets of support centres and revenue centres Does not represent planned activity levels Is not representative of the revenue centre’s consolidated budget Is not to be viewed on its own, but in conjunction with other tools and judgment www.usask.ca 33 What does this mean to units? Better ability to plan for change with greater certainty as to the potential impacts on revenue Greater correlation between their teaching and research activity and their budgets Additional changes are expected, from consultation with other universities…see next slide www.usask.ca 34 From Other Universities--Changes We Anticipate: improved clarity around the cost of specific activity has enhanced interdivisional collaboration; units tend to pay more attention to details, such as increasing revenue or leveraging opportunities; conversations with funders such as the governments are enhanced by the open, transparent process including the data created by the model; www.usask.ca 35 From Other Universities--Changes We Anticipate continued… increased transparency and understanding within units of the overall resources available to the university and to the units; there are opportunities for divisions to collaborate to utilize capital and infrastructure more effectively; increase in energy conservation and sustainability practices; promotion of collaborative research; and, interdisciplinary growth. www.usask.ca 36 Scenario Analysis Case reviewed: new undergraduate program in Pharmacy & Nutrition a) b) 25 new students 1 new faculty member • c) Tri-Agency and non-Tri-Agency research plus instructs Half-time staff member Review the effect of the new revenue and expenses in the model, holding all else constant. www.usask.ca 37 Scenario Analysis: Statistics 25 FLEs Tuition rate of $8,207 for 35 credits a) b) 10 credits are instructed by College of Medicine 25 credits are instructed by College of Pharmacy & Nutrition 1.0 FTE new faculty member with $35,000 Tri-Agency research and $30,000 non-Tri-Agency research 0.5 FTE staff member – CUPE phase 4 Non-salary costs $2,500 per FTE No additional space cost www.usask.ca 38 Scenario Analysis: New Program in Pharmacy Increased Revenue Provincial Operating Grant Allocation- Instruction $250,606 Provincial Operating Grant Allocation- Research $90,243 Total Provincial Operating Grant Allocation $340,849 Tuition Revenue – Undergraduate: Enrolment $51,294 Tuition Revenue – Undergraduate: Instruction $109,913 Total Tuition Revenue – Undergraduate Total Revenue Allocation Based on 2010/2011 Operating Budget; rates $161,206 $502,055 www.usask.ca 39 Scenario Analysis: New Program in Pharmacy Increased Cost Indirect Costs Research Support Bin $13,208 Student Support Bin $57,875 Faculty/Staff Bin $11,146 Occupancy Bin Health Sciences Holding Bin General Support Bin Total – Indirect Costs Based on 2010/2011 Operating Budget; rates $0 $1,069 $13,346 $96,644 www.usask.ca 40 Scenario Analysis: New Program in Pharmacy Result: Total Revenue Allocation Total Indirect Costs $502,055 $96,644 TABBS Model Reference Level $405,411 Additional Direct Costs $178,183 Difference b/w TMRL & Current Budget Allocation $227,228 Based on 2010/2011 Operating Budget; rates www.usask.ca 41 Phase Three Refinement of Model a) Adherence to principles: fall 2012 b) Data validation (sources, definitions): summerwinter 2012/13 c) Error corrections: 2012-13 * Consultation points with focus groups: summer 2012; winter 2012/13 www.usask.ca 42 Phase Three Implementation of Model a) Training of Model • • • b) Develop prototype of model: winter 2012/13 Documentation: 2012/13 Training sessions: spring 2013 Establishment of Support Unit Budget Review Committee • Determine membership: Fall 2012 • Develop terms of reference: Fall 2012 • c) Consultation Fall 2012 Consultation Fall 2012 Start meeting: winter/spring 2013 Developing Reports: 2012/13 www.usask.ca 43 Next Steps Online Review Period: April 20 to April 30 www.usask.ca/tabbs Questions/answers facilitated by email with response during the Online Review Period. Website’s “online review” page tabbs@usask.ca www.usask.ca 44 Questions/Comments? www.usask.ca 45 Breakout Session 9 flip chart stations 3 questions being asked (3 stations per question) Please take 10 mins on each question Team member will gather feedback www.usask.ca 46 Questions: 1. 2. 3. With the knowledge of each critical design feature’s recommendation and presentation of the TABBS Operating Budget Model today, does the model adhere to the principles of the model? [please see a handout of the principles in your packet] How do you see TABBS linking budgets to cycles of integrated planning and ensuring resources are allocated to strategic priorities? Collaboration and interdisciplinary teaching/learning are a priority at the University of Saskatchewan. How do you see this model assisting in the further progression of this priority moving forward? www.usask.ca 47 Closing Comments www.usask.ca 48