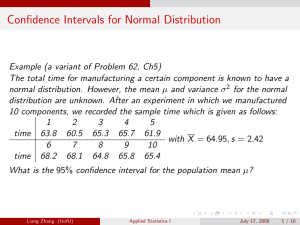

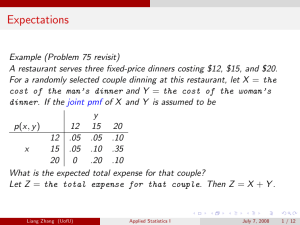

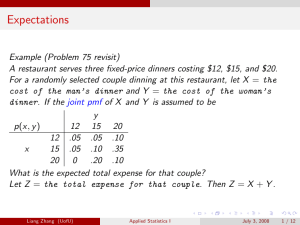

Exponential, Gamma, & Chi-Squared Distributions

advertisement

Exponential Distribution

Definition

X is said to have an exponential distribution with parameter λ(λ > 0) if

the pdf of X is

(

λe −λx x ≥ 0

f (x; λ) =

0

otherwise

Remark:

1. Usually we use X ∼ EXP(λ) to denote that the random variable X has

an exponential distribution with parameter λ.

2. In some sources, the pdf of exponential distribution is given by

(

1 − θx

e

x ≥0

f (x; θ) = θ

0

otherwise

The difference is that λ → 1θ .

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

1 / 20

Exponential Distribution

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

2 / 20

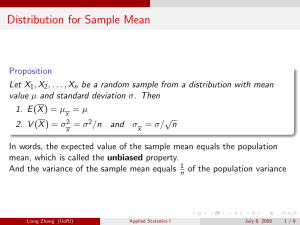

Exponential Distribution

Proposition

If X ∼ EXP(λ), then

E (X ) =

1

λ

and

V (X ) =

1

λ2

And the cdf for X is

(

1 − e −λx

F (x; λ) =

0

Liang Zhang (UofU)

Applied Statistics I

x ≥0

x <0

June 30, 2008

3 / 20

Exponential Distribution

Proof:

Z

E (X ) =

=

=

=

=

=

∞

xλe −λx dx

0

Z

1 ∞

(λx)e −λx d(λx)

λ 0

Z

1 ∞ −y

ye dy

y = λx

λ 0

Z ∞

1

[−ye −y |∞

e −y dy ] integration by parts:u = y , v = −e −y

0 +

λ

0

1

−y ∞

[0 + (−e |0 )]

λ

1

λ

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

4 / 20

Exponential Distribution

Proof (continued):

Z ∞

2

E (X ) =

x 2 λe −λx dx

0

Z ∞

1

= 2

(λx)2 e −λx d(λx)

λ 0

Z ∞

1

= 2

y 2 e −y dy

λ 0

Z ∞

1

= 2 [−y 2 e −y |∞

+

2ye −y dy ]

0

λ

0

Z ∞

1

−y ∞

= 2 [0 + 2(−ye |0 +

e −y dy )]

λ

0

1

= 2 2[0 + (−ye −y |∞

0 )]

λ

2

= 2

λ

Liang Zhang (UofU)

Applied Statistics I

y = λx

integration by parts

integration by parts

June 30, 2008

5 / 20

Exponential Distribution

Proof (continued):

2

1

1

V (X ) = E (X 2 ) − [E (X )]2 = 2 − ( )2 = 2

λ

λ

λ

Z x

−λy

F (x) =

λe

dy

0

Z x

=

e −λy d(λy )

0

Z x

=

e −z dz

z = λy

0

= −e −z |x0

= 1 − e −x

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

6 / 20

Exponential Distribution

Example (Problem 108)

The article “Determination of the MTF of Positive Photoresists Using the

Monte Carlo method” (Photographic Sci. and Engr., 1983:

254-260) proposes the exponential distribution with parameter λ = 0.93

as a model for the distribution of a photon’s free path length (µm) under

certain circumstances. Suppose this is the correct model.

a. What is the expected path length, and what is the standard deviation

of path length?

b. What is the probability that path length exceeds 3.0?

c. What value is exceeded by only 10% of all path lengths?

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

7 / 20

Exponential Distribution

Proposition

Suppose that the number of events occurring in any time interval of length

t has a Poisson distribution with parameter αt (where α, the rate of the

event process, is the expected number of events occurring in 1 unit of

time) and that numbers of occurrences in nonoverlappong intervals are

independent of one another. Then the distribution of elapsed time

between the occurrence of two successive events is exponential with

parameter λ = α.

e.g.

the number of customers visiting Costco in each hour =⇒ Poisson

distribution;

the time between every two successive customers visiting Costco =⇒

Exponential distribution.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

8 / 20

Exponential Distribution

Example (Example 4.22)

Suppose that calls are received at a 24-hour hotline according to a Poisson

process with rate α = 0.5 call per day.

Then the number of days X between successive calls has an exponential

distribution with parameter value 0.5.

The probability that more than 3 days elapse between calls is

P(X > 3) = 1 − P(X ≤ 3) = 1 − F (3; 0.5) = e −0.5·3 = 0.223.

The expected time between successive calls is 1/0.5 = 2 days.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

9 / 20

Exponential Distribution

“Memoryless” Property

Let X = the time certain component lasts (in hours) and we

assume the component lifetime is exponentially distributed with parameter

λ. Then what is the probability that the component can last at least an

additional t hours after working for t0 hours, i.e. what is

P(X ≥ t + t0 | X ≥ t0 )?

P({X ≥ t + t0 } ∩ {X ≥ t0 })

P(X ≥ t0 )

P(X ≥ t + t0 )

=

P(X ≥ t0 )

1 − F (t + t0 ; λ)

=

F (t0 ; λ)

P(X ≥ t + t0 | X ≥ t0 ) =

= e −λt

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

10 / 20

Exponential Distribution

“Memoryless” Property

However, we have

P(X ≥ t) = 1 − F (t; λ) = e −λt

Therefore, we have

P(X ≥ t) = P(X ≥ t + t0 | X ≥ t0 )

for any positive t and t0 .

In words, the distribution of additional lifetime is exactly the same as the

original distribution of lifetime, so at each point in time the component

shows no effect of wear. In other words, the distribution of remaining

lifetime is independent of current age.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

11 / 20

Gamma Distribution

Definition

For α > 0, the gamma function Γ(α) is defined by

Z ∞

x α−1 e −x dx

Γ(α) =

0

Properties for gamma function:

1. For any α > 1, Γ(α) = (α − 1) · Γ(α − 1) [via integration by parts];

2. For any positive integer, n, Γ(n) = (n − 1)!;

√

3. Γ( 21 ) = π.

√

e.g. Γ(4) = (4 − 1)! = 6 and Γ( 52 ) = 23 · Γ( 32 ) = 23 [ 12 · Γ( 12 )] = 34 π

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

12 / 20

Gamma Distribution

Definition

A continuous random variable X is said to have a gamma distribution if

the pdf of X is

(

1

x α−1 e −x/β x ≥ 0

α

f (x; α, β) = β Γ(α)

0

otherwise

where the parameters α and β satisfy α > 0, β > 0. The standard

gamma distribution has β = 1, so the pdf of a standard gamma rv is

(

1

x α−1 e −x x ≥ 0

f (x; α) = Γ(α)

0

otherwise

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

13 / 20

Gamma Distribution

Remark:

1. We use X ∼ GAM(α, β) to denote that the rv X has a gamma

distribution with parameter α and β.

2. If we let α = 1 and β = 1/λ, then we get the exponential distribution:

1

f (x; 1, ) =

λ

(

1

1

Γ(1)

λ

1

x 1−1 e −x/ λ = λe −λx

0

x ≥0

otherwise

3. When X is a standard gamma rv (β = 1), the cdf of X ,

Z

F (x; α) =

0

x

y α−1 e −y

dy

Γ(α)

is called the incomplete gamma function.

There are extensive tables of F (x; α) available (Appendix Table A.4).

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

14 / 20

Gamma Distribution

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

15 / 20

Gamma Distribution

Proposition

If X ∼ GAM(α, β), then

E (X ) = αβ

and

V (X ) = αβ 2

Furthermore, for any x > 0, the cdf of X is given by

x

;α

P(X ≤ x) = F (x; α, β) = F

β

where F (•; α) is the incomplete gamma function.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

16 / 20

Gamma Distribution

Example:

The survival time (in days) of a white rat that was subjected to a certain

level of X-ray radiation is a random variable X ∼ GAM(5, 4). Then what is

a. the probability that the survival time is at most 16 days;

b. the probability that the survival time is between 16 days and 20 days

(not inclusive);

c. the expected survival time.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

17 / 20

Chi-Squared Distribution

Definition

Let ν be a positive integer. Then a random variable X is said to have a

chi-squared distribution with parameter ν if the pdf of X is the gamma

density with α = ν/2 and β = 2. The pdf of a chi-squared rv is thus

(

1

x (ν/2)−1 e −x/2 x ≥ 0

ν/2

f (x; ν) = 2 Γ(ν/2)

0

x <0

The parameter ν is called the number of degrees of freedom (df) of X .

The symbol χ2 is often used in place of “chi-squared”.

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

18 / 20

Chi-Squared Distribution

Remark:

1. Usually, we use X ∼ χ2 (ν) to denote that X is a chi-squared rv with

parameter ν;

2. If X1 , X2 , . . . , Xn is n independent standard normal rv’s, then

X12 + X22 + · · · + Xn2 has the same distribution as χ2 (n).

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

19 / 20

Chi-Squared Distribution

Liang Zhang (UofU)

Applied Statistics I

June 30, 2008

20 / 20