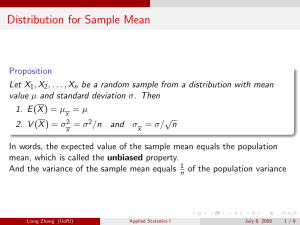

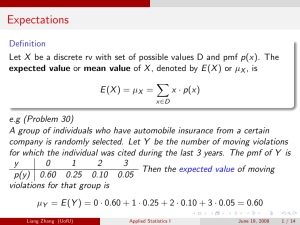

Expectations

advertisement

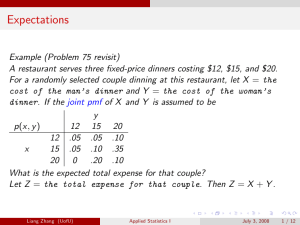

Expectations Example (Problem 75 revisit) A restaurant serves three fixed-price dinners costing $12, $15, and $20. For a randomly selected couple dinning at this restaurant, let X = the cost of the man’s dinner and Y = the cost of the woman’s dinner. If the joint pmf of X and Y is assumed to be y p(x, y ) 12 15 20 12 .05 .05 .10 x 15 .05 .10 .35 20 0 .20 .10 What is the expected total expense for that couple? Let Z = the total expense for that couple. Then Z = X + Y . Liang Zhang (UofU) Applied Statistics I July 7, 2008 1 / 12 Expectations p(x, y ) x 12 15 20 12 .05 .05 0 y 15 .05 .10 .20 20 .10 .35 .10 Z =X +Y E (Z ) = .05(12 + 12) + .05(12 + 15) + .10(12 + 20) + .05(15 + 12) + .10(15 + 15) + .35(15 + 20) + 0(20 + 12) + .20(20 + 15) + .10(20 + 20) = 33.35 Liang Zhang (UofU) Applied Statistics I July 7, 2008 2 / 12 Expectations Definition Let X and Y be jointly distributed rv’s with pmf p(x, y ) or pdf f (x, y ) according to whether the variables are discrete or continuous. Then the expected value of a function h(X , Y ), denoted by E [h(X , Y )] or µh(X ,Y ) , is given by (P P h(x, y ) · p(x, y ) if X and Y are discrete E [h(X , Y )] = R ∞x R y∞ if X and Y are continuous −∞ −∞ h(x, y ) · f (x, y )dxdy Liang Zhang (UofU) Applied Statistics I July 7, 2008 3 / 12 Expectations Example (Problem 12) Two components of a minicomputer have the following joint pdf for their useful lifetimes X and Y : ( xe −x(1+y ) x ≥ 0 and y ≥ 0 f (x, y ) = 0 otherwise If the lifetime of the minicomputer is the sum of the lifetimes of the two components, then what is the expected lifetime of the minicomputer? Liang Zhang (UofU) Applied Statistics I July 7, 2008 4 / 12 Covariance Liang Zhang (UofU) Applied Statistics I July 7, 2008 5 / 12 Covariance Liang Zhang (UofU) Applied Statistics I July 7, 2008 6 / 12 Covariance Liang Zhang (UofU) Applied Statistics I July 7, 2008 7 / 12 Covariance Definition The covariance between two rv’s X and Y is Cov (X , Y ) = E [(X − µX )(Y − µY )] (P P y (x − µX )(y − µY )p(x, y ) = R ∞x R ∞ −∞ −∞ (x − µX )(y − µY )f (x, y )dxdy X , Y discrete X , Y continuous Remark: The covariance depends on both the set of possible pairs and the probabilities. Proposition Cov (X , Y ) = E (XY ) − µX · µY Liang Zhang (UofU) Applied Statistics I July 7, 2008 8 / 12 Covariance Example (Problem 75 revisit) A restaurant serves three fixed-price dinners costing $12, $15, and $20. For a randomly selected couple dinning at this restaurant, let X = the cost of the man’s dinner and Y = the cost of the woman’s dinner. If the joint pmf of X and Y is assumed to be y 12 15 20 p(x, y ) 12 .05 .05 .10 x 15 .05 .10 .35 20 0 .20 .10 Cov (X , Y ) = E (XY ) − µX · µY = 276.7 − 15.9 · 17.45 = −0.755 Liang Zhang (UofU) Applied Statistics I July 7, 2008 9 / 12 Covariance If we change the unit for the previous example from dollar to cent, then the joint pmf would be y p(x, y ) 1200 1500 2000 1200 .05 .05 .10 x 1500 .05 .10 .35 0 .20 .10 2000 And correspondingly, Cov (X , Y ) = E (XY ) − µX · µY = 7550 Liang Zhang (UofU) Applied Statistics I July 7, 2008 10 / 12 Covariance Definition The correlation coefficient of X and Y , denoted by Corr (X , Y ), ρX ,Y or just ρ is defined by Cov (X , Y ) ρX ,Y = σX · σY e.g. for the previous example, the correlation coefficient of X and Y is ρ= Liang Zhang (UofU) −0.755 = −0.09 2.91 · 2.94 Applied Statistics I July 7, 2008 11 / 12 Covariance Proposition 1. Corr (aX + b, cY + d) = Corr (X , Y ) if a · c > 0. 2. −1 ≤ Corr (X , Y ) ≤ 1. 3. ρ = 1 or −1 iff Y = aX + b for some a and b with a 6= 0. 4. If X and Y are independent, then ρ = 0. However, ρ = 0 does not imply that X and Y are independent Liang Zhang (UofU) Applied Statistics I July 7, 2008 12 / 12