Document 10808218

advertisement

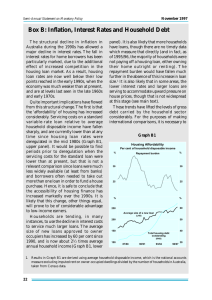

1 EMEAP SENIOR OFFICIALS MEETING, KUALA LUMPUR, 18 JANUARY 2011 THE AUSTRALIAN FINANCIAL SYSTEM Graph 2 Banks’ Non-performing Assets Domestic books, per cent of loans by type % % Business* 3 3 2 2 Personal 1 1 Total 0 2004 Housing 2006 2008 2010 0 * Includes bill acceptances and debt securities, and other non-household loans Source: APRA For the housing portfolio – which accounts for over half of banks’ on-balance sheet loans – the aggregate NPA ratio has steadied, to be 0.7 per cent in September 2010. This remains very low by international standards (Graph 3). Graph 3 Non-performing Housing Loans Per cent of loans* % % 8 8 US** 6 6 Spain 4 4 + UK 2 2 Australia** Canada**+ 0 1990 1994 1998 2002 2006 0 2010 * Per cent of loans by value. Includes ‘impaired’ loans unless otherwise stated. For Australia, only includes loans 90+ days in arrears prior to September 2003. ** Banks only. + Per cent of loans by number that are 90+ days in arrears. Sources: APRA; Bank of Spain; Canadian Bankers’ Association; Council of Mortgage Lenders; FDIC; RBA 3 Household sector net worth has retraced much of the deterioration experienced over 2008 and 2009 despite the recent moderation in house price appreciation. Australian dwelling prices increased by 3 per cent in the first eleven months of 2010, compared to the 12 per cent increase over 2009 (Graph 9). Graph 9 Australian Dwelling Prices* 2005 = 100 Index Index RP Data-Rismark 140 140 130 130 120 120 APM 110 110 100 100 90 2005 2006 2007 2008 2009 * Weighted average of houses and apartments in capital cities Sources: APM; RBA; RP Data-Rismark Reserve Bank of Australia 11 January 2011 2010 90 2 DEVELOPMENTS IN AUSTRALIAN HOUSEHOLDS’ BORROWING CAPACITY Households’ potential borrowing capacity declined by around 13 per cent between March 2009 and December 2010, according to lenders’ online loan calculators. While higher interest rates are the main source of the reduction in potential borrowing capacity, there also appears to have been some tightening in serviceability standards by a number of lenders. Maximum Borrowing Capacity Graph 1 A survey of lenders’ online loan calculators suggests that the potential borrowing capacity of Australian households declined by around 13 per cent between March 2009 and December 2010 (Graph 1). Furthermore, the decline in the maximum loan amount was apparent across all lenders, albeit to different degrees (Table 1). The range of maximum loan sizes offered by lenders declined somewhat. Maximum Loan Size Per cent of gross income; single individual, loan of 20 years % % March 2009 550 550 December 2007 500 500 June 2004 450 450 May 2008 400 400 December 2010 350 300 350 40 60 80 100 120 Gross household income ($’000) 140 300 * Median of 12 lenders. Sources: company websites; RBA Table 1: Change in Maximum Loan Size since March 2009 Single individual; gross income of $90 000; loan of 20 years Total RAMS Mortgage Choice WBC CBA STG Suncorp ANZ CUA HSBC BOQ AMP Bank Median Due to interest rates* -18.4 -16.3 -15.4 -14.6 -13.5 -13.0 -12.7 -12.9 -12.1 -12.1 -5.8 -13.0 -11.9 -13.3 -13.3 -13.3 -13.3 -13.3 -13.3 -14.1 -13.3 -13.3 -13.3 -13.3 Due to tax rates 1.0 1.4 1.4 1.4 1.5 1.4 1.4 1.4 1.4 1.4 1.4 1.4 Residual (includes serviceability/ interest-rate buffers) -7.5 -4.4 -3.5 -2.7 -1.7 -1.1 -0.8 -0.2 -0.2 -0.2 6.1 -1.1 * Six lenders allow changes in the maximum loan size arising from changes in interest rates to be identified. The median effect for these lenders is used as a proxy for the other lenders. Sources: ATO; company websites; RBA. Most of the decline in households’ borrowing capacity reflects the increase in mortgage interest rates over this period. Movements in interest rates influence borrowing capacity as lenders generally set borrowing limits based on rules regarding the maximum size of repayments relative to either gross or net income. Repayments are, in turn, often calculated using a percentage point buffer above the current variable interest rate. While the increase in interest rates has been the main factor behind the reduction in borrowing capacity, there also appears to have been some tightening in lending standards since March 2009. In particular, most of the surveyed lenders have reduced their maximum loan-to-income ratios by a greater amount than can be explained by the actual movement in interest rates and changes in income tax.2 However, this ‘residual’ accounts for only a small change in households’ borrowing capacity and it is possible that some of this may reflect an increase in interest rate buffers . Indeed, any tightening in serviceability policies is roughly equivalent to an increase in interest rates of only 17 basis points. In contrast to the other surveyed lenders, appears to have loosened its serviceability policies. This is consistent with the fact that market share of housing loan approvals has doubled since March 2009. However, increased market share has also been assisted by its competitive pricing. Likewise, market share moved in line with changes in its serviceability policies during this period Debt-servicing ratio The above analysis of maximum borrowing capacity can be recast to examine the maximum debt-servicing ratios offered by lenders. While most lenders now use net income surplus models – which require a borrower to have a minimum surplus of net income after taking into account debt repayments and living expenses – the ratio of loan repayments to gross income is often used as a simple metric of potential mortgage stress. 2 There are a number of ways financial institutions can tighten their lending standards that may not be reflected in the output of online calculators; for example, tighter income checks, lower maximum Loan-to-Valuation-Ratios (LVRs), tighter criteria on property type, or lower property valuations. For a gross income of over $80 000, the maximum debt servicing ratio implied by banks’ online calculators is currently around 50 per cent of gross income, somewhat higher than in March 2009 (Graph 3). This is partly because higher interest rates have resulted in higher maximum repayments (the higher level of interest rates more than offsets the fall in maximum loan size). It also reflects the lower tax paid on incomes of over $35 000 p.a. for the current fiscal year. That is, for the same level of gross income, an individual’s net income, and therefore debt servicing capacity, will be higher this year compared to last year. Abstracting from tax effects, the maximum net debt servicing ratio (loan repayments as a share of net income) is slightly higher than in March 2009 for net household incomes above $60 000 (Graph 4). Given that we would have expected a considerable rise in the net debt servicing ratio, as a result of the rise in interest rates, these results are consistent with a general tightening in lending standards. Graph 3 Graph 4 Maximum Debt-servicing Ratio* Maximum Debt-servicing Ratio* Loan repayments as a share of gross income; single individual, 20 years % % December 2007 Loan repayments as a share of net income; single individual, 20 years % % 75 May 2008 50 December 2007 50 70 45 45 June 2004 March 2009 40 40 December 2010 35 35 30 30 30 50 70 90 110 130 Gross household income ($’000) * Assuming constant repayments Sources: ATO; company websites; RBA Cameron Deans and Lisa Zhou Institutional Markets Section Domestic Markets Department 20 January 2011 150 May 2008 75 December 2010 70 June 2004 65 65 March 2009 60 60 55 55 50 50 45 45 30 40 50 60 70 80 90 Net household income ($’000) * Assuming constant repayments Sources: ATO; company websites; RBA 100 110 4 From: To: Cc: Subject: Date: CHAN, Iris STEWART, Chris BROADBENT, John; GORAJEK, Adam RE: Note FS: APRA Credit Conditions Survey - December Quarter 2010 [SEC=UNCLASSIFIED] Tuesday, 1 February 2011 09:53:36 Hi Chris, I think you’re right about conditions for residential property development not having changed much over the past two quarters. Obviously we don’t have any concrete information about how tight conditions are in an absolute sense, but at least no bank has explicitly said that they eased conditions for the segment in the December quarter. Cheers, Iris From: STEWART, Chris Sent: Monday, 31 January 2011 22:30 To: CHAN, Iris Cc: BROADBENT, John Subject: FW: Note FS: APRA Credit Conditions Survey - December Quarter 2010 [SEC=UNCLASSIFIED] Hi Iris, My reading of the September Quarter results – this afternoon as background for the SMP – was that there really wasn’t much evidence suggesting that conditions were changing in any material way from being relatively restrictive. Regards Chris From: CHAN, Iris Sent: Monday, 31 January 2011 7:20 PM To: Notes policy groups Subject: Note FS: APRA Credit Conditions Survey - December Quarter 2010 [SEC=UNCLASSIFIED] In the December credit conditions survey, banks appeared to be looking for market share in housing loans in an environment of muted credit demand. Nonetheless, no significant relaxation of lending standards appeared to have occurred thus far. Banks reported that margins decreased for housing loans following a two-year period of reported margin compression. Iris Chan Australian Financial System Financial Stability Department Reserve Bank of Australia P: +61 2 9551 8542 F: +61 2 9551 8052 CONFIDENTIAL APRA CREDIT CONDITIONS SURVEY – DECEMBER QUARTER 2010 In the December credit conditions survey, banks appeared to be looking for market share in housing loans in an environment of muted credit demand. Nonetheless, no significant relaxation of lending standards appeared to have occurred thus far. Banks reported that margins increased for housing loans following a two-year period of reported margin compression. CONFIDENTIAL Residential housing lending there appeared to be some tightening in non-price lending standards, Half of the sample also reported a reduction in non-standard loans as a share of new mortgage lending Some of these changes may have been done to prepare for the responsible lending requirements of the new National Consumer Credit Protection regime, which took effect for all credit providers on 1 January 2011. Media reports have suggested that banks are now requiring both their branch and broker channels to ask additional questions of potential borrowers to determine the suitability of a credit product, and borrowers to provide more verification when applying for low-doc loans.6 The number of policy overrides was reported to be little changed. 6 For example, see Searle (2010), ‘Credit Checks Stiffened’, Australian Financial Review, 10 January 2011, p.39. CONFIDENTIAL All banks reported that they expect higher delinquencies over the coming quarter for both owner-occupier and investor housing, a trend that some respondents attributed to seasonal impact from the Christmas/new year period. Banks also expect the demand for housing credit to decline, partly because of the floods and partly because borrowers expect interest rates to rise further. Iris Chan Australian Financial System, Financial Stability 31 January 2011 5 DOMESTIC MARKETS REVIEW: JANUARY 2011 21 Domestic Markets Department The major banks have been active in directing mortgage brokers to undertake a more rigorous approach to assessing the suitability of the borrower as, while this obligation has been imposed on brokers since mid 2010, there have been reports of poor compliance. Low doc housing lending continues under the new credit regulations Several lenders have also reportedly overhauled their low-doc lending practices following the aforementioned regulatory changes. Reaction to the new rules has varied. While some lenders have cited uncertainty (regarding the standard of borrower assessment that is required under the new regulations) as a reason for not reentering the low-doc market, other lenders do not see any need to overhaul their existing practices. 6 LOMAS, Phil From: Sent: To: Cc: Subject: Attachments: CHAN, Iris Wednesday, 9 February 2011 16:36 DONOVAN, Bernadette GORAJEK, Adam NPA sneak peek [SEC=UNCLASSIFIED] image001.png; image002.png; image003.png; image004.png 1 Banks' Asset Quality $b Non- performing housing assets Domestic books Non-performing business assets* Specific provisions $b 20 20 15 15 Impaired 10 10 Business Past- due 5 5 Housing 0 0 2007 2009 2011 2008 2010 2007 2009 2011 * Includes bill acceptances and securities, and other non -household loans Sources: APRA Banks' Non- performing Assets % Domestic books Per cent of on-balance sheet Per cent of all on-balance loans by type sheet loans 4 % 4 Business* 3 3 2 Personal 2 Total 1 1 Housing 0 0 2007 2009 2011 2008 2010 * Includes lending to non-ADI financial businesses, bill acceptances and debt * securities, and other non -household loans Source: APRA 2 7 HILDA analysis of flood areas A higher proportion of flood affected households in Queensland qualify as vulnerable under our usual definition (DSR>50, LVR>80 or 90%) compared to Australia as a whole. Flood affected areas All Australia Households With Low Equity and High Repayments Households With Low Equity and High Repayments Per cent of households with owner-occupier debt* Per cent of households with owner-occupier debt* % 8 % % 8 8 DSR>30, LVR>80 % 8 DSR>30, LVR>80 6 6 DSR>30, LVR>90 4 4 4 4 DSR>50, LVR>80 2 DSR>50, LVR>90 0 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 * Includes the first and second mortgages secured against the property Source: HILDA Release 9.0 6 DSR>30, LVR>90 DSR>50, LVR>80 2 6 2 2 DSR>50, LVR>90 0 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 * Includes the first and second mortgages secured against the property Source: HILDA Release 9.0 This is caused predominantly by higher LVRs in the flood affected regions compared to Australian as a whole. DSRs across the two regions were similar. % DSRs and LVRs DSRs and LVRs Indebted owner-occupier households Indebted owner-occupier households LVR DSR % % 60 30 75th percentile 30 75th percentile 60 75th percentile 75th percentile Median Median 20 40 20 40 Median Median 25th percentile 10 20 10 0 0 25th percentile 0 2001 2004 2007 2001 2004 2007 25th percentile 0 2004 40 0<DSR<30 2004 2007 % % 40 40 30 30 20 20 10 10 0 % 40 0<DSR<30 30<DSR<50 30 60-80 80-100 DSR>50 20 10 0 40-60 Indebted owner-occupier households, 2009 DSR>50 30<DSR<50 20-40 2001 DSR Distribution by LVR Indebted owner-occupier households, 2009 0-20 2007 Source: HILDA Release 9.0 DSR Distribution by LVR 30 20 25th percentile 2001 Source: HILDA Release 9.0 % % LVR DSR 10 0 100+ 0 0-20 Source: HILDA Release 9.0 20 20-40 40-60 60-80 80-100 100+ Source: HILDA Release 9.0 Loan-to-valuation Ratios Loan-to-valuation Ratios Indebted owner-occupier households by income quintile Indebted owner-occupier households by income quintile % 2001 2008 70 60 75th percentile 75th percentile 50 Median 40 Median 30 20 25th percentile 25th percentile 10 0 % % 70 70 60 60 50 50 40 40 30 30 20 20 10 10 0 2 3 4 5 Total 2 3 4 5 Household disposable income quintile Source: HILDA Release 9.0 Total 2001 % 2008 70 75th percentile 75th percentile 60 50 Median 40 Median 30 25th percentile 20 25th percentile 10 0 0 2 3 4 5 Total 2 3 4 5 Total Household disposable income quintile Source: HILDA Release 9.0 Shows thatin flood affected areas in 2009 more HHs increased their LVR because of negative house price movements than in previous years, with debt being less important. Also, more HHs experienced an increase in LVRs in flood affected areas than in previous years. These trends are not evident at the aggregate level. % LVR Movements LVR Movements By reason, per cent of indebted owner-occupiers* By reason, per cent of indebted owner-occupiers* LVR down/equity up LVR up/equity down House price movements 60 Debt & price movements 40 Debt movements 20 0 % % 60 60 40 40 20 20 0 0 2002 2004 2006 2008 2002 2004 2006 2008 Renters and other 20 % % 40 40 30 Home bought without a mortgage Debt & price movements Debt movements 40 20 0 Per cent of all households Owner-occupiers with original mortgage Indebted owner-occupiers* 30 60 Households' Debt Repayment Status Per cent of all households 40 House price movements % * Movements in LVRs between two adjoining survey years. Source: HILDA Release 9.0 Households' Debt Repayment Status All households LVR up/equity down 2002 2004 2006 2008 2002 2004 2006 2008 * Movements in LVRs between two adjoining survey years. Source: HILDA Release 9.0 % LVR down/equity up All households Owner-occupiers with original mortgage 40 Indebted owner-occupiers* 30 % 30 Renters and other Ahead of schedule 20 Home bought without a mortgage 20 Mortgage paid off 10 About on schedule 10 Ahead of schedule Mortgage paid off 10 About on schedule 20 10 Behind schedule 0 2001 0 2004 2007 2001 2004 * Owner-occupiers with any mortgage debt Source: HILDA Release 9.0 2007 Behind schedule 0 2001 0 2004 2007 2001 2004 2007 * Owner-occupiers with any mortgage debt Source: HILDA Release 9.0 Surprisingly, a greater proportion flood affected households are ahead if schedule, although this mainly reflects the fact that a greater proportion of flood affected households are indebted owneroccupiers. Measures of Housing Arrears Measures of Housing Arrears Per cent by number* Per cent by number; not seasonally adjusted % % 5 5 4 4 4 4 3 3 3 3 2 2 2 2 1 1 1 1 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 0 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 0 % 5 Behind schedule* * Per cent of owner-occupier households, indebted with their 1st mortgage. ** Prime & non-conforming loans securitised by all lenders; excludes selfsecuritisations. Sources: HILDA Release 8.0; Perpetual % * Per cent of owner-occupier households, indebted with their 1st mortgage. Sources: HILDA Release 8.0; Owner-occupier Housing Debt Owner-occupier Housing Debt 2009, average $000 300 2009, average Original mortgage Loans from friends, family, solicitors or community organisations Other mortgage debt* Per cent of total debt in income quintile (RHS) 200 100 0 % $000 60 300 40 200 20 100 0 1 2 3 4 5 5 Behind schedule Total Income quintile * Second mortgage, home equity and refinanced loans Source: HILDA Release 9.0 % Original mortgage Loans from friends, family, solicitors or community organisations Other mortgage debt* 60 Per cent of total debt in income quintile (RHS) 40 20 0 0 1 2 3 4 5 Total Income quintile * Second mortgage, home equity and refinanced loans Source: HILDA Release 9.0 Owner-occupier Housing Debt 2008 Owner-occupier Housing Debt 2008 As a per cent of disposable income As a per cent of disposable income % % Original mortgage Loans from friends, family, solicitors or community organisations Other mortgage debt* 800 800 % % Original mortgage Loans from friends, family, solicitors or community organisations Other mortgage debt* 600 600 600 600 400 400 400 400 200 200 200 200 0 0 1 2 3 4 5 Total 0 0 1 2 Income quintile * Second mortgage, home equity and refinanced loans Source: HILDA Release 8.0 Rank 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 4 5 Total Income quintile * Second mortgage, home equity and refinanced loans Source: HILDA Release 8.0 Queensland Housing Loan Arrears by Region As at December 2010 Per cent of population Region in flood affected postcodes Gold Coast East 100.00 Gold Coast Bal 100.00 Far North - North West Mackay - Central West Ipswich City 100.00 Sunshine Coast 5.05 Caboolture Shire 23.33 Wide Bay-Burnett 99.84 Logan City 87.44 Redcliffe City 100.00 West Moreton 99.43 Fitzroy Inner Brisbane 100.00 Darling Downs - South West 89.60 Southeast Inner Brisbane 100.00 Northern QLD Redland Shire 100.00 Southeast Outer Brisbane 100.00 Pine Rivers Shire 97.92 Northwest Outer Brisbane 100.00 Northwest Inner Brisbane 98.99 Australia Sources: Perpetual; RBA 3 90+ days arrears rate 0.85 0.72 0.71 0.66 0.59 0.58 0.56 0.54 0.54 0.51 0.50 0.44 0.43 0.41 0.36 0.33 0.24 0.23 0.22 0.22 0.17 0.44 8 ASIC SUMMER SCHOOL TALK : SPECULATIVE BOOMS , BUBBLES AND BUSTS – HOW MUCH CAN WE KNOW ? I would start by mentioning that nothing I have to say is relevant to near-term policy decisions. Credit growth is slow; housing prices have levelled off; commercial property prices are at a trough; and other markets are well off their peaks. The household saving ratio has returned to levels last seen in the late 1980s. None of that sounds like a speculative boom to me. History shows that asset price busts cost the most when they occur together with a banking crisis. The recent bust in the United States was centred on households and housing markets. It is actually quite unusual for households to be the instigators of the crisis in this way. Housing price busts are more often a symptom or knock-on effect of financial instability, not the thing that started it off. But property in general is usually implicated in banking crises. Commercial real estate – offices, shopping centres, as well as loans for property development – are often the source of problems for the financial system. They have certainly dominated the loan losses of Irish, British and the smaller US banks lately. The decline in commercial property prices has in fact been larger than for housing in almost every industrialised country (Graph 1). Graph 1 Property Price Indicators 31 December 2000 = 100 Index Commercial real estate Residential real estate Index Spain 200 200 Australia US 150 150 UK Ireland 100 100 Sweden 50 2002 2006 2010 2002 2006 2010 50 Sources: APM; Bloomberg; BIS; Jones Lang LaSalle; Thomson Reuters Why are property markets so often implicated in financial instability in this way? The answer lies in the combination of their use as collateral for lending, and the dynamics of the physical property markets. Lenders would rather lend against collateral than unsecured. And borrowers like to magnify their capital gains on property through leverage. But if prices fall, leverage magnifies the capital losses. Some borrowers become distressed and a fire sale ensues, causing further distress. Equity markets can also boom and bust. But they are less likely to spark off a vicious circle of distress sales, because buyers in that market are generally less leveraged. The inherent dynamics of the physical market for property also contribute to the boom-bust cycles. It takes time to build a building, more so for large, complex commercial developments than detached housing. And new construction is always going to be a small fraction of the existing stock. So the supply of both commercial real estate and housing is always going to be sluggish. And if it is sluggish, the market can end up oscillating in repeated boom-bust cycles. These are the inherent dynamics of the system. In this sense, and unlike equity markets, property markets can boom and bust even without a credit-fuelled speculative bubble. 1 What are the fundamentals? It should be obvious that we would want to know if an expansion in property markets is sustainable, or a boom that will inevitably bust, whether it is truly a bubble or not. The question is how we could tell. Of course, hindsight is a beautiful thing and now many people think that of course you can tell if there is a bubble! I think we need to be more modest about our understanding of the economy than that. My first point is that it is not sensible just to look at some historical average for prices, or some other simple ratio, and assume that they will revert to that level. The fundamentals do not stay constant over long periods. For example, Australia has had a much lower inflation rate over the past twenty years than it did over the previous twenty. So, nominal interest rates are lower. That means borrowers can service a bigger mortgage with the same repayment and on the same income (Graph 2). Graph 2 Maximum Loan-to-income Ratio* Assuming 3% real interest rate on 25-year loan Ratio Ratio 8 8 Repayment = 50% income 6 6 Repayment = 40% income 4 4 Repayment = 30% income 2 0 2 0 1 2 3 4 5 6 7 Inflation (%) 8 9 10 11 0 12 Source: RBA Another example is that credit supply is no longer artificially restricted the way it was in the 1970s and early 1980s, before the financial sector was deregulated. Some good credit risks amongst households were not able to get mortgages back then; now they can. So it is not correct to assume that prices will revert to mean, either in real terms or relative to income. There are other fundamentals than income. Another reason why you shouldn’t assume that prices revert exactly to historical averages is that most models of fundamentals are really models of a single person or household. If you use them, you are implicitly assuming that the so-called ‘representative agent’ assumption is true. But in reality, people are different; their circumstances – their fundamentals – can and do change. Distributional issues will therefore matter a great deal. For example, household debtincome ratios and the leverage on the housing stock in Australia have risen over the past decade. But survey data show that much of that occurred because more households in older age groups still have a small mortgage (Graph 3). Fewer of them have completely paid their mortgage off. This seems a less risky outcome than if it had been that younger, recent homebuyers had even bigger mortgages than they currently do. 2 Graph 3 Indebted Owner-occupiers by Age Group % % Share of households 60 60 2001 30 % 30 % Median LVR 60 60 30 30 2009 0 0 15-24 25-34 35-44 45-54 55-64 65+ Source: HILDA Release 9.0 Fundamentals also differ across countries. Housing supply can be more or less flexible; the tax treatment of housing can differ. And housing is more expensive in bigger cities, even relative to city-level income (Gabaix 1999). National averages are therefore higher if everyone lives in big cities (Ellis and Andrews 2001). So you should not expect either rental returns or price-income ratios to be the same across countries. It is as mistaken to think that prices will revert to some cross-country average as it is to think they will necessarily revert to an historical average. You would end up concluding that movements in housing prices during the pre-crisis boom phase implied that the US had less of a bubble than Canada (Graph 4)! Graph 4 House Prices and Household Debt Percentage point change in ratios to household income* (2000 to 2006) % pts % pts House prices Household debt 200 200 150 150 100 100 50 50 0 US Australia Canada Spain NZ UK 0 * Household income is after tax, before interest payments Sources: BIS; national sources I would also argue that it is not as simple as just estimating a model of fundamentals, and attributing the deviation between the model and actual data as the ‘bubble’ component. As I mentioned, the models are usually of a single household. And we need to take variations in credit constraints into account; most models of fundamentals don’t do that. I have another, more philosophical, objection to this approach. It assumes that the model is exactly right. But we know that ‘all models are wrong’; there are always simplifications. How do you know that the difference between data and model is really a bubble? It could just be that your model isn’t very good, or that your data don’t measure exactly what your theory requires. The required fundamentals are things like expected future interest rates or expected future incomes growth. The estimate of fundamental levels for prices will only be as good as the estimates of these inputs. 3 In my view, just asking whether prices are in line with fundamentals misses the point. It is a wholly static question. Of course if there were a bubble, that would be a concern. Speculative booms and bubbles can collapse in on themselves from their own dynamics. But we don’t face a simple decision of: bubble – worry; no bubble – don’t worry. Even if asset prices are in line with estimated fundamentals, there are times when we should not be complacent. As I mentioned in my speech last May,1 every speculative boom starts with something real, something fundamental. Behind the dot-com bubble, there really was new technology and strong productivity. And before the Asian crisis, Asia really was developing fast.2 So if you see unusually strong fundamentals, and price rises to match, you don’t need to be alarmed. But you should definitely be alert! That asset market need not go from that fundamentals-based phase to a more speculative one, but its conditions are such that it could. Likewise you should be alert to the fundamentals’ dynamics, and the risk that they might reverse. That doesn’t mean that policymakers should try to undo the effects of strong fundamentals on asset markets or the real economy. But it does suggest that they should take steps to ensure that the financial system would be resilient if those fundamentals did reverse. That explains our interest in the lending standards that apply to the financing of property and other assets. You should be even more alert if you detect increasing speculative activity. Remember, bubbles are speculative booms; the motivations of the asset buyers matter. We might not be able to see the speculation directly, but we can dust for its fingerprints. For example, prudential supervisors notice changes in lenders’ behaviour, such as when their business models and product offerings have become more aggressive. Policymakers can and do share those observations and concerns, even if they can’t make them public. We can also look for signs of borrowers using loan products that enable speculative purchases, like investor housing loans or deposit bonds. For example, it turns out that it was interest-only loans – not subprime loans – that predicted which US cities would have boom-bust cycles in housing prices (Barlevy and Fisher 2010). And in ASIC’s realm, we can see if there are signs of speculative fervour in the growth of the ‘property seminar’ industry. This was a big deal during the 2002–03 boom, and we said so at the time in the Bank’s Submission to the Productivity Commission. We can also use household surveys and other disaggregated data, to check for concentrations of risk. For both housing and commercial property, it is the marginal borrower, not the median borrower, where the risks lie. And the median household is not the median borrower. As I mentioned before, much of the recent increase in housing debt in Australia was driven by lowrisk older households with small mortgages. It would be different if households with low and variable incomes and little equity in the home had contributed the most. That is what happened in the United States during the boom in the subprime market. 1 http://www.rba.gov.au/speeches/2010/sp-so-180510.html I struggle to name the fundamental behind the US subprime mortgage boom, but long-term interest rates and thus US mortgage rates did fall to low levels, and the GSEs that dominated the US prime mortgage market were facing new constraints on their activities. 2 4 What policy responses are possible? Whether it’s a speculative boom or a shift in fundamentals that only might become one, the question is how to respond. If the fundamentals are strong, then conventional macroeconomic policies will be pushing in the right direction anyway. You don’t have to target asset prices. You just have to recognise that they tell you something about what is happening in the real economy. A good example of this connection was, again, the boom in housing prices in 2002– 2003. The real economy was also very strong at the time, especially consumption growth. Even if you had thought that the growth in housing prices was based on fundamentals, it was clear what macro policies should be doing. But it might not make sense to tighten macroeconomic policies more than the real economy requires. So if you are concerned that the boom might be partly speculative, you might want to look for other ways to respond. Many people in the international policy community are looking at ‘macroprudential’ policy. I don’t have time to discuss these today. But broadly speaking, it means using prudential tools to lean against credit-fuelled asset speculation. There are some policies that can help limit how far a speculative boom can go, even though they weren’t designed with that purpose in mind. A good example of this is consumer protection regulation around the provision of credit. Australia’s National Consumer Credit Code requires that the lender must be able to verify and show that the consumer can be reasonably expected to repay the loan from their own resources, without having to sell the collateral. If not, the loan can be modified or even set aside by the courts. This provides a powerful incentive for lenders to extend credit responsibly. They should be less prone to do the assetbased and ‘no-doc’ lending that caused so many problems in the United States in the lead-up to the crisis. By limiting lending in this way, the NCCC helps limit the finance available for risky and speculative purposes, at least if a household is doing the borrowing. Tax policy is another example of a type of policy that isn’t obviously about financial stability, but can be designed to limit speculative behaviour. Of course, tax systems are designed with many other goals in mind, not just their effects on asset markets and financial stability. But it is useful to have open eyes about the incentives tax systems create or don’t create for speculative behaviour. If different countries have different tax systems, the same developments in asset markets might have different implications for their financial stability. Policymakers with a range of mandates have to pay attention to asset prices and the financing of those markets. But there is no single indicator or smoking gun that tells you it’s a bubble. Nor can you find an easy rule of thumb to know if it’s a boom that might not be speculative now, but could become so. In the end, there is no substitute for careful analysis from a range of perspectives, focussed on distributions and risks, not just macro-level data and simple ratios. There is also no substitute for policymakers who can use that analysis judiciously, neither dismissing every boom as based on fundamentals, nor seeing bubbles in every wobble of a price index. And if they do see something that concerns them, those policymakers need to have the mandate and the willingness to respond. Sometimes that might mean responding to a boom when it occurs, perhaps with a prudential instrument. But perhaps just as often, it might require ensuring that the broader institutional environment does not overly reward leveraged speculation. 5 References Barlevy G and JDM Fisher (2010), ‘Mortgage Choices and Housing Speculation’, Federal Reserve Bank of Chicago Working Paper 2010-13. Ellis L and D Andrews (2001), ‘City Sizes, Housing Costs, and Wealth’, Reserve Bank of Australia Research Discussion Paper 2001-08. Gabaix X (1999), ‘Zipf’s Law and the Growth of Cities’, American Economic Review, 89(2), pp 129–132. 6 Speculative booms, bubbles and busts – how much can we know? Luci Ellis Head of Financial Stability Department Reserve Bank of Australia Presentation to ASIC Summer School 22 February 2011 Property Price Indicators 31 December 2000 = 100 Index Commercial real estate Residential real estate Index Spain 200 200 Australia US 150 150 UK Ireland 100 100 Sweden 50 2002 2006 2010 2002 2006 2010 Sources: APM; Bloomberg; BIS; Jones Lang LaSalle; Thomson Reuters 50 Maximum Loan-to-income Ratio* Assuming 3% real interest rate on 25-year loan Ratio Ratio 8 8 Repayment = 50% income 6 6 Repayment = 40% income 4 4 Repayment = 30% income 2 2 0 0 12 0 1 2 Source: RBA 3 4 5 6 7 Inflation (%) 8 9 10 11 Indebted Owner-occupiers by Age Group % % Share of households 60 60 2001 30 % 30 % Median LVR 60 60 30 30 2009 0 0 15-24 25-34 Source: HILDA Release 9.0 35-44 45-54 55-64 65+ House Prices and Household Debt Percentage point change in ratios to household income* (2000 to 2006) % pts % pts House prices Household debt 200 200 150 150 100 100 50 50 0 0 US Australia Canada Spain NZ * Household income is after tax, before interest payments Sources: BIS; national sources UK