Module 4 Stationary Time Series Models Part 1

advertisement

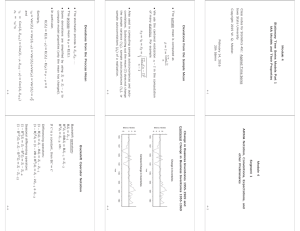

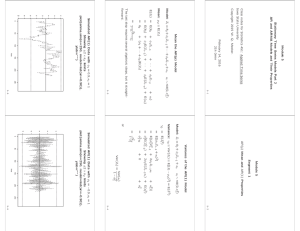

Module 4 Stationary Time Series Models Part 1 MA Models and Their Properties Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W. Q. Meeker. February 14, 2016 20h 58min 4-1 Module 4 Segment 1 ARMA Notation, Conventions, Expectations, and other Preliminaries 4-2 Deviations from the Sample Mean • The sample mean is computed as Pn zt t=1 b µ = z̄ = n • We use the centered realization zt − z̄ in the computation of many statistics. For example v uP u n (z − z̄)2 t bZ = γ b0 = SZ = t t=1 σ n−1 • Also used in computing sample autocovariances and autocorrelations. Subtracting out the mean (z̄) does not change the sample variance (γb0), sample autocovariances (γbk ), or sample autocorrelations (ρbk ) of a realization. 4-3 Change in Business Inventories 1955-1969 and Centered Change in Business Inventories 1955-1969 10 5 0 -5 Billions of Dollars Change in Inventories 1955 1957 1959 1961 1963 1965 1967 1969 1967 1969 Year 10 5 0 -10 Billions of Dollars Centered Change in Inventories 1955 1957 1959 1961 1963 1965 Year 4-4 Deviations from the Process Mean • The stochastic process is Z1, Z2, . . . . • The process mean is µ = E(Zt). • Some derivations are simplified by using Żt = Zt − µ to compute model properties (only the mean has changed). • In particular, E(Żt) = E(Zt − µ) = E(Zt) − E(µ) = µ − µ = 0 Similarly, 2 γ0 = Var(Żt ) = Var(Zt −µ) = Var(Zt )+Var(µ) = Var(Zt) = σZ and γk = Cov(Żt , Żt+k ) = Cov(Zt − µ, Zt+k − µ) = Cov(Zt , Zt+k ) ρk = γk /γ0 4-5 Backshift Operator Notation Backshift operators: BZt = Zt−1 B2Zt = BBZt = BZt−1 = Zt−2 B3Zt = Zt−3, etc. If C is a constant, then BC = C Differencing operators: (1 − B)Zt = Zt − BZt = Zt − Zt−1 (1 − B)2Zt = (1 − 2B + B2)Zt = Zt − 2Zt−1 + Zt−2 Seasonal differencing operators: (1 − B4)Zt = Zt − B4Zt = Zt − Zt−4 (1 − B12)Zt = Zt − B12Zt = Zt − Zt−12 4-6 Polynomial Operator Notation φ(B) = φp(B) ≡ (1 − φ1B − φ2B2 − · · · − φpBp) is useful for expressing the AR(p) model. For example, with p = 2, an AR(2) model. φ2(B)Żt = at (1 − φ1B − φ2B2)Żt = at Żt − φ1Żt−1 − φ2Żt−2 = at or Żt = φ1Żt−1 + φ2Żt−2 + at Other polynomial operators: θ(B) = θq (B) ≡ (1−θ1B−θ2B2 −· · ·−θq Bq ) [as in Żt = θq (B)at ] ψ(B) = ψ∞(B) ≡ (1 + ψ1B + ψ2B2 + · · · ) [as in Żt = ψ(B)at ] π(B) = π∞(B) ≡ (1 − π1B − π2B2 − · · · ) [as in π(B)Żt = at] 4-7 General ARMA(p, q) Model in Terms of Żt Żt ≡ Zt − µ φp(B)Żt = θq (B)at (1 − φ1B − φ2B2 − · · · − φp Bp)Żt = (1 − θ1B − θ2B2 − · · · − θq Bq )at Żt − φ1Żt−1 − φ2Żt−2 − · · · − φpŻt−p = at − θ1at−1 − θ2at−2 − · · · − θq at−q or Żt = φ1Żt−1+φ2Żt−2+· · ·+φpŻt−p−θ1at−1−θ2at−2−· · ·−θq at−q +at 4-8 Mean (µ) and Constant Term (θ0) for an ARMA(2,2) Model Replace Żt with Żt = Zt − µ and solve for Zt = · · · . For example, using p = 2 and q = 2, giving an ARMA(2,2) model: Żt = φ1Żt−1 + φ2Żt−2 − θ1at−1 − θ2at−2 + at and Zt − µ = φ1(Zt−1 − µ) + φ2(Zt−2 − µ) − θ1at−1 − θ2at−2 + at Zt = µ − φ1µ − φ2µ + φ1Zt−1 + φ2Zt−2 − θ1at−1 − θ2at−2 + at Zt = θ0 + φ1Zt−1 + φ2Zt−2 − θ1at−1 − θ2at−2 + at where θ0 = µ − φ1µ − φ2µ = µ(1 − φ1 − φ2) is the ARMA model “constant term.” Also, E(Zt) = µ = θ0/(1 − φ1 − φ2). Note that E(Zt) = µ = θ0 for an MA(q) model. 4-9 Module 4 Segment 2 Properties of the MA(1) Model and the PACF 4 - 10 −4 −2 0 2 Simulated MA(1) Data with θ1 = 0.9, σa = 1 plot(arima.sim(n=250, model=list(ma=0.90)), ylab=””) 0 50 100 150 200 250 Time 4 - 11 −4 −2 0 2 4 Simulated MA(1) Data with θ1 = −0.9, σa = 1 plot(arima.sim(n=250, model=list(ma=-0.90)), ylab=””) 0 50 100 150 200 250 Time 4 - 12 Mean and Variance of the MA(1) Model Model: Zt = θ0 − θ1at−1 + at, at ∼ nid(0, σa2) Mean: µZ ≡ E(Zt) = E(θ0 − θ1at−1 + at ) = θ0 + 0 + 0 = θ0. 2 ≡ Var(Z ) ≡ E[(Z − µ )2 ] = E(Ż 2) Variance: γ0 ≡ σZ t t Z t t γ0 = E(Żt2) = E[(−θ1at−1 + at)2] = E[(θ12a2 t−1 = θ12E(a2 t−1 ) − 2θ1at−1 at + a2 t )] − 2θ1E(at−1at ) + E(a2 t) = θ12σa2 − 0 = (θ12 + 1)σa2 + σa2 4 - 13 Autocovariance and Autocorrelation Functions for the MA(1) Model Autocovariance: γk ≡ Cov(Zt, Zt+k ) = E[(Zt − µZ )(Zt+k − µZ )] = E(ŻtŻt+k ) γ1 ≡ E(ŻtŻt+1) = E[(−θ1at−1 + at)(−θ1at + at+1)] = E(θ12at−1 at − θ1at−1at+1 − θ1a2 t + at at+1) = 0 − 0 − θ1σa2 + 0 = −θ1σa2 Thus ρ1 = γγ1 = −θ12 . (1+θ1 ) 0 Using similar operations, it is easy to show that γ2 ≡ E(ŻtŻt+2) = 0 and thus ρ2 = γ2/γ0 = 0. In general, for MA(1), ρk = γk /γ0 = 0 for k > 1. 4 - 14 Partial Autocorrelation Function For any model, the process PACF φkk can be computed from the process ACF from ρ1, ρ2, . . . using the recursive formula from Durbin (1960): φ1,1 = ρ1 ρk − φkk = k−1 X φk−1 ,j ρk−j j=1 k−1 X 1− , k = 2, 3, ... φk−1,j ρj j=1 where φkj = φk−1,j − φkk φk−1,k−j (k = 3, 4, ...; j = 1, 2, ..., k − 1) This formula is based on the solution of the Yule-Walker equations (covered later). Also, the sample PACF can be computed from the sample ACF. That is, φbkk is a function of ρb1, ρb2, . . .. 4 - 15 Hints For Using Durbin’s formula φ11 = ρ1 ρ − φ11ρ1 φ22 = 2 1 − φ11ρ1 depends on ρ1 depends on ρ1, ρ2 and φ11 • φ33 depends on ρ1, ρ2, ρ3, φ21, and φ22 • φ44 depends on ρ1, ρ2, ρ3, ρ4, φ31, φ32, and φ33 • φ55 depends on ρ1, ρ2, ρ3, ρ4, ρ5, φ41, φ42, φ43, and φ44 • and so on. 4 - 16 True ACF and PACF for MA(1) Model with θ1 = 0.95 True ACF 0.0 -1.0 True ACF 1.0 ma: 0.95 0 5 10 15 20 15 20 Lag True PACF 0.0 -1.0 True PACF 1.0 ma: 0.95 0 5 10 Lag 4 - 17 True ACF and PACF for MA(1) Model with θ1 = −0.95 True ACF 0.0 -1.0 True ACF 1.0 ma: -0.95 0 5 10 15 20 15 20 Lag True PACF 0.0 -1.0 True PACF 1.0 ma: -0.95 0 5 10 Lag 4 - 18 Simulated Realization (MA(1), θ1 = 0.95, n = 75) Graphical Output from Function iden Simulated data -3 -2 -1 w 0 1 2 w= Data 0 10 20 30 40 50 60 70 time ACF 4.5 0.0 -1.0 ACF 0.5 5.0 1.0 Range-Mean Plot 0 5 10 15 20 15 20 Range Lag 0.5 0.0 -1.0 3.5 Partial ACF 1.0 4.0 PACF -0.8 -0.6 -0.4 -0.2 Mean 0.0 0.2 0 5 10 Lag 4 - 19 Simulated Realization (MA(1), θ1 = 0.95, n = 300) Graphical Output from Function iden Simulated data -2 0 w 2 w= Data 0 50 100 150 200 250 300 time ACF 0.0 5 -1.0 ACF 6 0.5 1.0 Range-Mean Plot 0 5 10 15 20 15 20 Range Lag 0.5 0.0 -1.0 3 Partial ACF 1.0 4 PACF -0.1 0.0 0.1 Mean 0.2 0 5 10 Lag 4 - 20 Simulated Realization (MA(1), θ1 = −0.95, n = 75) Graphical Output from Function iden Simulated data -2 0 w 2 4 w= Data 0 10 20 30 40 50 60 70 time ACF 0.0 -1.0 5 ACF 6 0.5 1.0 Range-Mean Plot 5 10 15 20 15 20 4 0 Range Lag 0.5 0.0 -1.0 1 2 Partial ACF 1.0 3 PACF -0.6 -0.4 -0.2 0.0 Mean 0.2 0.4 0.6 0 5 10 Lag 4 - 21 Simulated Realization (MA(1), θ1 = −0.95, n = 300) Graphical Output from Function iden Simulated data w -4 -2 0 2 4 w= Data 0 50 100 150 200 250 300 time ACF 5 0.0 -1.0 ACF 6 0.5 1.0 Range-Mean Plot 5 10 15 20 15 20 4 Lag 0.5 0.0 Partial ACF 3 1.0 PACF -1.0 2 Range 0 -0.5 0.0 0.5 Mean 1.0 0 5 10 Lag 4 - 22 Module 4 Segment 3 Inverting the MA(1) Model and MA(q) Properties 4 - 23 Geometric Power Series 1 = (1 − θ1B)−1 = (1 + θ1B + θ12B2 + · · · ) (1 − θ1B) This expansion provides a convenient method for re-expressing parts of some ARMA models. When |θ1| < 1 the series converges. Similarly, 1 2 =(1 − φ1B)−1 = (1 + φ1B + φ2 1B + · · · ) (1 − φ1B) Again, when |φ1| < 1 the series converges. 4 - 24 Using the Geometric Power Series to Re-express the MA(1) Model as an Infinite AR Żt = (1 − θ1B)at at = (1 − θ1B)−1 Żt at = (1 + θ1B + θ12B2 + · · · )Żt Żt = −θ1Żt−1 − θ12Żt−2 − · · · + at Thus the MA(1) can be expressed as an infinite AR model. If −1 < θ1 < 1, then the weight on the old observations is decreasing with age (having more practical meaning). This is the condition of “invertibility” for an MA(1) model. 4 - 25 Using the Back-substitution to Re-express the MA(1) Model as an Infinite AR Żt = −θ1at−1 + at at−1 = Żt−1 + θ1at−2 at−2 = Żt−2 + θ1at−3 at−3 = Żt−3 + θ1at−4 Substituting, successively, at−1, at−2, at−3 . . ., shows that Żt = −θ1Żt−1 − θ12Żt−2 − · · · + at This method works, more generally, for higher-order MA(q) models, but the algebra is tedious. 4 - 26 Notes on the MA(1) Model Given ρ1 = γγ1 = −θ12 we can see (1+θ1 ) 0 • −0.5 ≤ ρ1 ≤ 0.5 • Solving the ρ1 = · · · quadratic equation for θ1 gives r 1 −1 ± −1 2ρ1 (2ρ1 )2 θ1 = 0 ρ1 6= 0 ρ1 = 0 The two solutions are related by 1 θ1 = ′ θ1 For any −0.5 ≤ ρ1 ≤ 0.5, the solution with −1 < θ1 < 1 is the “invertible” parameter value. • Substituting ρb1 for ρ1 provides an estimator for θ1. 4 - 27 Mean, Variance, and Covariance of the MA(q) Model Model: Zt = θ0 + θq (B)at = θ0 − θ1at−1 − · · · − θq at−q + at Mean: µZ ≡ E(Zt) = E(θ0 − θ1at−1 − · · · − θq at−q + at) = θ0. Variance: γ0 ≡ Var(Zt) ≡ E[(Zt − µZ )2] = E(Ż 2) Centered MA(q): Żt = θq (B)at = −θ1at−1 − · · · − θq at−q + at Var(Zt ) ≡ γ0 = E(Żt2) = (1 + θ12 + · · · + θq2)σa2 Cov(Zt , Zt+k ) = γk = E(ŻtŻt+k ) = · · · ρk = γk γ0 4 - 28 Re-expressing the MA(q) Model as an Infinite AR More generally, any MA(q) model can be expressed as Żt = θq (B)at = (1 − θ1B − θ2B2 − · · · − θq B)at 1 Żt = π(B)Żt = (1 − π1B − π2B2 − . . . )Żt = at θq (B) Żt = π1Żt−1 + π2Żt−2 + · · · + at = ∞ X πk Żt−k + at k=1 Values of π1, π2, . . . depend on θ1, . . . , θq . For the model to have practical meaning, the πj values should not remain large as j gets large. Formally, the invertibility condition is met if ∞ X i=1 |πj | < ∞ Invertibility of an MA(q) model can be checked by finding the roots of the polynomial θq (B) ≡ (1−θ1B−θ2B2 −· · ·−θq Bq ) = 0. All q roots must lie outside of the “unit-circle.” 4 - 29 Module 4 Segment 4 Checking Invertibility and Polynomial Roots 4 - 30 Checking the Invertibility of an MA(2) Model Invertibility of an MA(2) model can be checked by finding the roots of the polynomial θ2(B) = (1 − θ1B − θ2B2) = 0. Both roots must lie outside of the “unit-circle.” B= −θ1 ± q θ12 + 4θ2 2θ2 Roots have the form z = x + iy where i = √ −1. A root is “outside of the unit circle” if |z| = q x2 + y 2 > 1 This method works for any q, but for q > 2 it is best to use numerical methods to find the q roots. 4 - 31 Roots of (1 − 1.5B − 0.4B2) = 0 arma.root(c(1.5, 0.4)) Coefficients= 1.5, 0.4 Roots and the Unit Circle • • -2 0 Imaginary Part -10 -15 -4 -20 Function -5 2 0 4 Polynomial Function versus B -8 -6 -4 B -2 0 -4 -2 0 2 4 Real Part 4 - 32 Roots of the Quadratic (1 − 0.5B + 0.9B2) = 0 and the Unit Circle Unit Circle 0.0 −0.5 −1.0 −1.5 Imaginary Part 0.5 1.0 1.5 Coefficients= 0.5, −0.9 −1.5 −1.0 −0.5 0.0 0.5 1.0 1.5 Real Part 4 - 33 Roots of (1 − 0.5B + 0.9B2) = 0 arma.root(c(0.5, −0.9)) Coefficients= 0.5, -0.9 Roots and the Unit Circle 1.02 1.5 Polynomial Function versus B 0.5 -0.5 Imaginary Part 0.98 0.96 • -1.5 0.94 Function 1.00 • 0.0 0.2 0.4 B 0.6 -1.5 -0.5 0.5 1.5 Real Part 4 - 34 Roots of (1 − 0.5B + 0.9B2 − 0.1B3 − 0.5B4) = 0 arma.root(c(0.5, −0.9, 0.1, 0.5)) Coefficients= 0.5, -0.9, 0.1, 0.5 Roots and the Unit Circle 1 • • • -1 0 Imaginary Part -40 -60 -80 • -100 Function -20 0 Polynomial Function versus B -4 -2 0 B 2 -1 0 1 Real Part 4 - 35 Checking the Invertibility of an MA(2) Model Simple Rule Both roots lying outside of the “unit-circle” implies θ2 + θ1 < 1 θ2 < 1 − θ 1 θ2 − θ 1 < 1 θ2 < 1 + θ1 −1 < θ2 < 1 −1 < θ2 < 1 and the inequalities define the MA(2) triangle. 4 - 36 Module 4 Segment 5 MA(2) Model Properties 4 - 37 Autocovariance and Autocorrelation Functions for the MA(2) Model γ1 ≡ Cov(Zt, Zt+1) = E[(Zt − µZ )(Zt+1 − µZ )] = E(ŻtŻt+1) = E[(−θ1at−1 − θ2at−2 + at)(−θ1at − θ2at−1 + at+1)] 2 = E(θ1θ2a2 t−1 − θ1at ) + 0 + 0 + 0 + 0 + 0 + 0 + 0 2 2 = θ1θ2E(a2 ) − θ E(a ) = (θ θ − θ )σ 1 1 2 1 t a t−1 Thus γ θ θ −θ ρ1 = 1 = 1 22 1 2 . γ0 1 + θ1 + θ2 Using similar operations, it is easy to show that −θ2 γ2 = ρ2 = γ0 1 + θ12 + θ22 and that, in general, for MA(2), ρk = γk /γ0 = 0 for k > 2. 4 - 38 True ACF and PACF for MA(2) Model with θ1 = 0.78, θ2 = 0.2 True ACF 0.0 -1.0 True ACF 1.0 ma: 0.78, 0.2 0 5 10 15 20 15 20 Lag True PACF 0.0 -1.0 True PACF 1.0 ma: 0.78, 0.2 0 5 10 Lag 4 - 39 True ACF and PACF for MA(2) Model with θ1 = 1, θ2 = −0.95 True ACF 0.0 -1.0 True ACF 1.0 ma: 1, -0.95 0 5 10 15 20 15 20 Lag True PACF 0.0 -1.0 True PACF 1.0 ma: 1, -0.95 0 5 10 Lag 4 - 40 Simulated Realization (MA(2), θ1 = 0.78, θ2 = 0.2, n = 75) Graphical Output from Function iden Simulated data -3 -2 -1 w 0 1 2 w= Data 0 10 20 30 40 50 60 70 time ACF 0.0 -1.0 4.6 ACF 4.8 0.5 1.0 Range-Mean Plot 4.4 5 10 15 20 15 20 Lag 0.5 -1.0 0.0 4.0 Partial ACF 1.0 4.2 PACF 3.8 Range 0 -0.04 -0.02 0.0 0.02 Mean 0.04 0.06 0.08 0 5 10 Lag 4 - 41 Simulated Realization (MA(2), θ1 = 0.78, θ2 = 0.2, n = 300) Graphical Output from Function iden Simulated data -2 0 w 2 4 w= Data 0 50 100 150 200 250 300 time ACF 0.0 6 -1.0 7 ACF 0.5 1.0 Range-Mean Plot 0 5 10 15 20 15 20 Range Lag 3 0.5 0.0 -1.0 4 Partial ACF 1.0 5 PACF -0.2 -0.1 0.0 0.1 Mean 0.2 0 5 10 Lag 4 - 42 Simulated Realization (MA(2), θ1 = 1, θ2 = −0.95, n = 75) Graphical Output from Function iden Simulated data -2 0 w 2 4 w= Data 0 10 20 30 40 50 60 70 time ACF 0.0 -1.0 6 ACF 0.5 7 1.0 Range-Mean Plot 5 10 15 20 15 20 5 Lag 0.5 -1.0 0.0 Partial ACF 1.0 PACF 4 Range 0 -0.2 0.0 0.2 Mean 0.4 0 5 10 Lag 4 - 43 Simulated Realization (MA(2), θ1 = 1, θ2 = −0.95, n = 300) Graphical Output from Function iden Simulated data -6 -4 -2 w 0 2 4 w= Data 0 50 100 150 200 250 300 time ACF 0.0 -1.0 8 ACF 0.5 10 1.0 Range-Mean Plot 0 5 10 15 20 15 20 Range Lag 0.5 0.0 -1.0 4 Partial ACF 1.0 6 PACF -0.6 -0.4 -0.2 0.0 Mean 0.2 0.4 0.6 0 5 10 Lag 4 - 44 MA(2) Triangle Relating ρ1 and ρ2 to θ1 and θ2 4 - 45 MA(2) Triangle Showing ACF and PACF Functions 4 - 46