Math 142 Business Mathematics II Minh Kha Section 1.2: Mathematical Modeling

advertisement

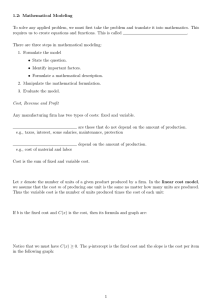

Math 142 Business Mathematics II Minh Kha Section 1.2: Mathematical Modeling Goals: to understand what a mathematical model is, and some of its examples in business. Definition 0.1. Mathematical Modeling is an attempt to describe some part of the real world in mathematical terms. More precisely, to solve any applied problem by a mathematical model, we must first take the problem and translate it into mathematics by creating equations and functions. There are three steps in mathematical modeling: 1. Formulate the model • State the question. • Identify important factors. • Formulate a mathematical description. 2. Manipulate the mathematical formulation. 3. Evaluate the model. 1 Mathematical Models of Cost, Revenue and Profit There are two types of costs in any manufacturing firm: fixed costs and variable costs. Fixed Costs are those that do not depend on the amount of production. e.g., taxes, interest, some salaries, maintenance, protection Variable Costs depend on the amount of production. e.g., cost of material and labor Cost is the sum of fixed and variable cost, i.e., Cost=Fixed cost + Variable Cost. In the linear cost model, we assume that the cost m of producing one unit is the same no matter how many units are produced. Thus the variable cost is the number of units produced times the cost of each unit: Variable Cost = Cost per unit(m) × Number of units produced(x)=mx. If b is the fixed cost and C(x) is the cost, then its formula and graph are: C(x) = Variable Cost + Fixed Cost = mx + b. (1) Notice that we must have C(x) ≥ 0. The y-intercept is the fixed cost and the slope is the cost per item. 1 In the linear revenue model, we assume that the price p of a unit sold by a firm is the same no matter how many units are sold. Thus, the revenue is the price per unit times the number of units sold. Let x be the number of units sold. (For convenience, we assume the number of units sold equals the number of units produced.) Then, if we denote the revenue by R(x), then its formula is R(x)=revenue=(price per unit) × (number sold)=px. Notice that we must have R(x) ≥ 0. The line goes through (0, 0) because nothing sold results in no revenue. The slope is the price per unit. Thus, the profit P is always revenue less cost, i.e., P =profit=(revenue)-(cost)=R − C. Recall that both C(x) and R(x) must be nonnegative functions. However, profit P (x) can be positive or negative. Negative profits are called losses. Example 1. (J.D.Kim) A manufacturer of garbage disposals, has a monthly fixed cost of 15, 000 dollars and a production cost of 30 dollars for each garbage disposal manufactured. The unit sell for 60 dollars each. 1. What is the cost function? 2. What is the revenue function? 3. What is the profit function? Definition 1.1. The value of x at which the profit is zero is called the break-even quantity. The break-even quantity is the value of x at which cost equals revenue. Example 2. Find the break-even quantity for the previous example. 2 2 Mathematical Models of Supply and Demand Definition 2.1. Assume that x is the number of units produced and sold by the entire industry during a given period of time and that p = −cx + d, c > 0, is the price of one unit if x units are sold; that is, p = −cx+d is the price of the xth unit sold. We call p = −cx+d the demand equation and the graph the demand curve. Estimating the demand curve is a fundamental problem for the management of any comany or business. Note that the demand curve is typically decreasing. Example 3. When the price for an item is set at $10, consumers are willing to buy 30 items. When the price is set at $20, no consumer is willing to buy the item. Find the linear demand equation, p = D(x). Definition 2.2. The supply equation p = p(x) gives the price p necessary for suppliers to make available x units to the market. The graph of this equation is called the supply curve. A reasonable supply curve increases because the suppliers of any product naturally want to sell more if the price is higher. Example 4. The producer is not willing to sell any items if the price is set at $5. However, the producer will supply 10 items when the price is $10. Find the linear supply equation, p = S(x). Definition 2.3. The best-known law of economics is the law of supply and demand. The point where the supply curve intersects the demand curve is called the equilibrium point. The x-coordinate of the equilibrium point is called the equilibrium quantity and the p-coordinate is called the equilibrium price. 3 1 Example 5. Suppose the price of an item is given by p = − x + 30 when x items are demanded. 2 1 Further, manufacturers are willing to sell x items at the price p = x + 9 5 a) What is the surplus or shortage if the price is set at $20? b) What is the equilibrium quantity? What is the equilibrium price? Example 6. (Tomastic, #27) Many assets, such as machines or buildings, have a finite useful life and further more depreciate in value from year to year. For purposes of determining profits and taxes, various methods of depreciation can be used. In straight-line depreciation we assume that the value V of the asset is given by a linear equation in time t, say, V = mt + b. The slope m must be negative, since the value of the asset decreases over time. Consider a new machine that costs $10,000 and has a useful life of nine years and a scrap value of $1000. Using straight-line depreciation, find the equation for the value V in terms of t, where t is in years. Find the value after one year and after five years. 4 3 Quadratic Mathematical Models Definition 3.1. A quadratic is a polynomial function of degree 2: q(x) = ax2 + bx + c, a 6= 0. Every quadratic function can be placed in standard form a(x − h)2 + k. The point (h, k) is called the vertex and can be found by using the formulas h = −b/2a, k = c − b2 /4a. We will now consider quadratic mathematical models of revenue and profit. If the number of units of a product sold by an industry is to increase significantly, then the price per unit will most likely need to decrease (by supply and demand). Therefore, if the demand equation for an entire industry is the linear demand equation p = −cx + d with c > 0, then the revenue is: R = px = (−cx + d)x = −cx2 + dx. This is a quadratic model. 1 Example 7. Suppose that price of an item is given by p = − x + 10 when x items are demanded. 2 a) Find the revenue function. b) When is the revenue maximized? 5