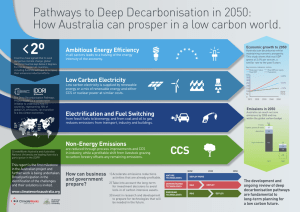

PATHWAYS TO DEEP DECARBONISATION IN 2050

advertisement