Chapter 23 – Perfect Competition What are the characteristics of

advertisement

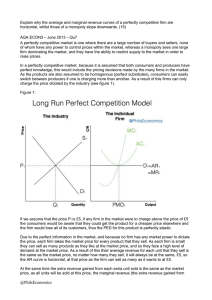

Chapter 23 – Perfect Competition Homework – Day 1 Read pages 413 – 423. Stop at "Marginal Cost and Short-Run Supply.” On your own paper in your notebook, answer the following: a. List and explain the characteristics of pure competition. b. List 4 examples of perfectly competitive industries or markets. c. Why is the demand curve of a perfectly competitive firm perfectly elastic? d. Why is a perfectly competitive firm called a "price taker?" e. What is the relationship between price and average revenue for a perfectly competitive firm? f. At what level of output should a perfectly competitive firm produce? State your answer using both methods for calculating profit-maximization. g. Take the quick quiz on p. 420 and check your answers. h. Why should a firm sometimes continue to produce even if it is incurring losses? i. At what point should a firm shut down? Chapter 23 – Perfect Competition • What are the characteristics of Perfect Competition • Very large number of firms • Product is standardized: each firm’s is exactly the same. • Each individual firm has no control over the market price. • New firms can enter the marketplace easily. • Firms compete only through price. • Agricultural products (wheat, corn, etc.), metals, stocks, foreign currency, etc. A firm in a perfectly competitive industry is a price taker. What does this mean? The firm has no control over price. It cannot raise price without losing all of its business, and it can sell all it wants at the market price, so it has no need to lower price below that. P D 0 Q The demand curve, for the individual firm is perfectly elastic. Revenue and Price • In pure competition, price, average revenue, and marginal revenue are all equal. • This might seem obvious, but it is not always true in other types of markets. For example, what is the price of cable TV? • What is the price of a 2 ton pick-up truck? • What is the price of a Toyota Tundra? Consumer Surplus: the difference between the amount consumers were willing to pay for a product and the amount they had to pay (the price). Consumer Surplus P Pe D 0 Q Profit Maximization • A perfectly competitive firm must produce where: • Total Revenue – Total Cost is greatest. • Or • Marginal Revenue = Marginal Cost • Remember, marginal costs are going up, so the firm needs to produce right up until the marginal cost of the last unit = the price for that unit. For the unit before that, cost is less than price, so they will make a profit on that unit. Once marginal cost gets above price, they start losing profit. Just replace MB with MR, after all the benefit to a company of producing a product is the revenue it receives for that product. Curve MR is horizontal because? What is P? At a price of $131 and 7 units of output, what should the firm do? Why? Why produce at 9 units? New Economic Profit What would happen if price fell to $100? How much would this firm produce? When to Shut Down? • Why would a firm continue to produce even if it’s losing money? • Because of fixed costs, it’s going to be losing money even if it produces nothing. It still has to pay its rent, property taxes, etc. In the short run, it cannot get out of these expenses. • If it can lose less money by producing, then it should go ahead and stay open. When to Shut Down? • If price is higher than average variable cost, then the firm can minimize its losses. Ask for explanation here if you need it. • If price is lower than average variable cost, then the firm should shut down, because then they will lose more money by producing than they will by producing nothing. Homework • Read Pages 423-426 – Take the quick quiz on 424 and check yourself (before you wreck yourself). – Do Study Questions 2, 3 (a, b, c only), 4, and 5. Q4 For each price (P1, P2, P3, & P4) determine: a. the profit-maximizing (or loss-minimizing) quantity (2 pts) b. whether the firm is making economic profit, normal profit, or incurring an economic loss. (2 pts.) c. whether the firm should continue to produce or shut down (2 pts.)