Managerial Accounting

McGraw-Hill/Irwin

Wild and Shaw

Third Edition

Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 1

Managerial Accounting

Concepts and Principles

Conceptual Learning Objectives

C1: Explain the purpose and nature of managerial

accounting and the role of ethics.

C2: Describe accounting concepts useful in classifying

costs.

C3: Define product and period costs and explain how

they impact financial statements.

C4: Explain how the balance sheets and income

statements for manufacturing and merchandising

companies differ.

C5: Explain manufacturing activities and the flow of

manufacturing costs.

C6: Identify trends in managerial accounting.

1-3

Analytical Learning Objectives

A1: Compute cycle time and cycle

efficiency, and explain their importance

to production management.

1-4

Managerial & Financial

Accounting

Managerial accounting

provides financial and

non-financial information

for managers of an

organization and other

decision makers

Financial accounting

provides general

purpose financial

information to those

who are outside

the organization.

1-5

Nature of Managerial

Accounting

Financial Accounting

Managerial Accounting

Investors, creditors and

other external users

Managers, employees and

other internal users

2. Purpose of

information

Making investment, credit

Planning and

and other decisions

control decisions

3. Flexibility

of practice

Structured and often

Relatively flexible

controlled by GAAP

(no GAAP constraints)

4. Timeliness of

information

Often available only

Available quickly without

after audit is complete

need to wait for audit

Historical information

with some predictions

Many projections

and estimates

Emphasis on

Projects, processes and

whole organization

segments of an organization

Monetary

Monetary and

information

nonmonetary information

1. Users and

decision makers

5. Time dimension

6. Focus of

information

7. Nature of

information

1-6

Managerial Cost Concepts

Behavior

Traceability

Controllability

Relevance

Function

1-7

Classification by Behavior

Cost behavior means how a cost will

react to changes in the level of

business activity.

A fixed cost does not change with

changes in the volume of activity

A variable cost changes in proportion

to changes in the volume of activity

A mixed cost refers to a combination of fixed

and variable

1-8

Classification by Traceability

Direct costs

Costs traceable to a

single cost object.

Examples: material

and labor cost for a

product.

Indirect costs

Costs that cannot be

traced to a single cost

object.

Example:

maintenance

expenditures

benefiting two or more

departments.

1-9

Classification by Controllability

The degree of control depends on the

level of management in the organization.

Very little control

1-10

Classification by Relevance:

Sunk Costs

All costs incurred in the past that cannot be

avoided or changed. Sunk costs should not be

considered in decisions.

Example: You bought an automobile that cost

$15,000 two years ago. The $15,000 cost is

sunk because whether you drive it, park it,

trade it, or sell it, you cannot change the

$15,000 cost.

1-11

Classification by Relevance:

Out-of-Pocket Costs

A cost that requires a future outlay of cash.

Out-of-pocket costs should be considered in

decisions.

Example: You plan on buying a new car for

$25,000 next month. The cost of the new car

is an out-of-pocket cost because you can

choose to spend the $25,000 or not in the

future

1-12

Classification by Relevance:

Opportunity Costs

The potential benefit lost by choosing a specific

action from two or more alternatives

Example: If you were not attending college,

you could be earning $20,000 per year. Your

opportunity cost of attending college for one

year is $20,000.

1-13

Classification by Function:

Product Costs

Direct

Material

Direct

Labor

Manufacturing

Overhead

The

Product

1-14

Period and Product Costs

in Financial Statements

Period Costs

(Expenses)

2011 Income

Statement

Operating

Expenses

2011 Costs

Incurred

Cost of

Goods Sold

Product

Costs

(Inventory)

Inventory

Sold in 2011

Inventory Not

Sold in 2011

2011 Balance

Sheet Inventory

Raw Materials

Goods in Process

Finished Goods

2012 Income

Statement

Cost of

Goods Sold

1-15

Balance Sheet of a

Manufacturer

Raw

Materials

Materials

waiting to be

processed.

Can be direct

or indirect.

Goods in

Process

Partially complete

products.

Material to which

some labor and/or

overhead have

been added.

Finished

Goods

Completed

products

for sale.

1-16

Income Statement of a

Manufacturer

Merchandiser

Manufacturer

Beginning

Merchandise

Inventory

Beginning

Finished Goods

Inventory

+

+

Cost of Goods

Purchased

_

The major

difference

Ending

Merchandise

Inventory

=

Cost of Goods

Manufactured

_

Ending

Finished Goods

Inventory

Cost of Goods

Sold

=

1-17

Income Statement of a

Manufacturer

Cost of goods sold for manufacturers differs only

slightly from cost of goods sold for merchandisers.

Merchandising Company

Cost of goods sold:

Beg. merchandise

inventory

+ Purchases

= Goods available

for sale

- Ending

merchandise

inventory

= Cost of goods

sold

$ 14,200

234,150

$ 248,350

(12,100)

$ 236,250

Manufacturing Company

Cost of goods sold:

Beg. finished

goods inv.

+ Cost of goods

manufactured

= Goods available

for sale

- Ending

finished goods

inventory

= Cost of goods

sold

$11,200

170,500

181,700

(10,300)

$

171,400

1-18

C5

Direct Materials Used

Direct Materials

Materials that are separately and readily

traced to a particular product.

Example:

Steel used to

manufacture

the automobile.

1-19

Income Statement of a

Manufacturer

Direct Labor

Labor costs that are separately and

readily traced to finished product.

Example:

Wages paid to an

automobile assembly

worker.

1-20

Income Statement of a

Manufacturer

Factory Overhead

All manufacturing costs except

direct material and direct labor

Factory costs that cannot be

separately or readily traced directly to

products.

Examples:

Indirect labor – maintenance

Indirect material – cleaning supplies

Factory utility costs

Supervisory costs

1-21

Income Statement of a

Manufacturer

Manufacturing costs are often

combined as follows:

Direct

Material

Direct

Labor

Prime

Cost

Manufacturing

Overhead

Conversion

Cost

1-22

Flow of Manufacturing

Activities

Materials

activity

Raw

Materials

Beginning

Inventory

Raw

Materials

Purchases

Production activity

Goods in Process

Beginning Inventory

Direct Labor

Factory

Overhead

Raw Materials

Used

Sales activity

Finished Goods

Beginning Inventory

Cost of Goods

Manufactured

Finished

Goods

Ending

Inventory

Raw Materials

Goods in Process

Ending Inventory

Ending Inventory

Cost

of

Goods

Sold

1-23

Manufacturing Statement

Summarizes the types and amounts of costs

Incurred in a company’s manufacturing process.

+

+

=

+

–

=

Direct Materials Used

Direct Labor

Factory Overhead

Total Manufacturing Costs

Beginning Work in Process

Ending Work in Process

Cost of Goods Manufactured

1-24

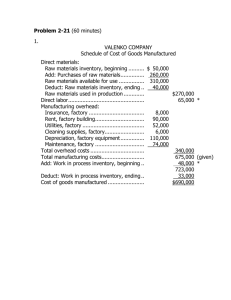

Manufacturing Statement

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2011

Direct materials used in production

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-25

Computation of Cost of Direct Material Used

Beginning raw materials inventory

Add: Purchases of raw materials

$

8,000

86,500

Cost of raw materials available for use

Deduct: Ending raw materials inventory

$ 94,500

9,000

ROCKY

MOUNTAIN

BIKES

Cost of direct materials

used

in production

$ 85,500

Manufacturing Statement

For Year Ended December 31, 2011

Direct materials used in production

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-26

Manufacturing Statement

Include all direct labor

costs

incurred

during

the

ROCKY

MOUNTAIN

BIKES

current period.

Manufacturing

Statement

For Year Ended December 31, 2011

Direct materials used in production

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-27

Computation of Total Manufacturing Overhead

Indirect labor

$

9,000

Manufacturing Statement

6,000

Factory supervision

Factory utilities

2,600

Property taxes, factory building

1,900

Factory supplies usedROCKY MOUNTAIN BIKES 600

Factory insurance expired

1,100

Manufacturing Statement

Depreciation, building and equipment

5,300

For Year Ended December 31, 2008

Other factory overhead

3,500

Total factory

overhead

Direct

materials

usedcosts

in production

$

30,000

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-28

Manufacturing Statement

Beginning work in

process inventory is

ROCKY MOUNTAIN

BIKESover from the

carried

Manufacturing Statement

prior period.

For Year Ended December 31, 2009

Direct materials used in production

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-29

Manufacturing Statement

Ending work in process inventory

contains

the cost ofBIKES

unfinished goods,

ROCKY MOUNTAIN

and

is reportedStatement

in the current assets

Manufacturing

of the balance

sheet.

For Yearsection

Ended December

31, 20009

Direct materials used in production

$

Direct labor

Total factory overhead costs

85,500

60,000

30,000

Total manufacturing costs for the period

Add: Beginning goods in process inventory

$

175,500

2,500

Total cost of goods in process

Deduct: Ending goods in process inventory

$

178,000

7,500

Cost of goods manufactured

$

170,500

1-30

Lean Practices

Customer

Orientation

in a Global

Economy

1-31

Total Quality Management

Quality improvement

applied to all aspects of

business activities.

Seek and uncover

waste.

on

Employees encouraged

to try new methods

to improve quality.

Company emphasizes

value of quality through

quality awards.

1-32

Just-In-Time (JIT)

Manufacturing

Receive

customer

orders.

Complete products

just in time to

ship to customers.

Schedule

production.

Receive materials

just in time for

production.

Complete parts

just in time for

assembly into products.

1-33

Just-In-Time (JIT)

Manufacturing

To accomplish just-in-time

manufacturing:

Processes must be

aligned to eliminate

delays and

inefficiencies

Companies must

establish good

relations with

suppliers

1-34

Cycle Time and Cycle Efficiency

Cycle Time =

Process Time +

Inspection Time +

Move Time +

Wait Time

Cycle Efficiency = Value-added time

Cycle Time

1-35

Fraud in Accounting

Fraud is the use of one’s job for personal

gain through the deliberate misuse of the

employer’s assets.

It is estimated that 7% of annual revenues

are lost to fraud.

All fraud is committed to provide direct or

indirect benefit to the perpetrator, violates

the employee’s duty to his/her employer,

costs the employer money, and is carried

out in secret.

1-36

Ethics in Accounting

Ethics are beliefs that distinguish right from wrong.

They are accepted standards of good and bad

behavior.

The IMA’s Statement of Ethical Professional Practice

requires management accountants to be competent,

maintain confidentiality, act with integrity, and

communicate information in a fair and credible

manner.

The Sarbanes-Oxley Act requires each issuer of

securities to disclose whether it has adopted a code of

ethics for its senior officers and the content of that

code.

1-37

End of Chapter 1

1-38