Biocon Ltd.: Building a

Biotech Powerhouse

Company Case Analysis

EMBA 240

Professor Sanjay Jain

ROBERT PAUL ELLENTUCK

EMBA 2011

5/10/2010

COPYRIGHT © 2010, 2011

ALL RIGHTS RESERVED

ROBERT PAUL ELLENTUCK

THE COPYRIGHT HOLDER EXPRESSLY PROHIBITS ANY AND ALL COPYING, FAXING, SCANNING,

XEROXING, REPRODUCING, TRANSMISSION, DISSEMINATION, FORWARDING, PRINTING,

SUBMISSION (EITHER ELECTRONICALLY OR OF A SCANNED OR OTHERWISE REPRODUCED COPY,

OR OF THE ORIGINAL COPYRIGHTED MATERIAL, A COPY OF THE COPYRIGHTED MATERIAL, OR

OF A PORTION OF THE ORIGINAL OR COPIED COPYRIGHTED MATERIAL), OR ANY AND ALL OTHER

ACTIONS: ELECTRONIC OR OTHERWISE, OF ANY PORTION OF THIS COPYRIGHTED MATERIAL OR

THE ENTIRE COPYRIGHTED MATERIAL, WHICH MAY IN ANY WAY VIOLATE THE RIGHTS OF THE

COPYRIGHT HOLDER. SUCH PROHIBITION INCLUDES THE ORIGINAL COPYRIGHTED MATERIAL, A

COPY OF THE ORIGINAL COPYRIGHTED MATERIAL, A PORTION OF THE ORIGINAL COPYRIGHTED

MATERIAL, A PORTION OF THE COPIED COPYRIGHTED MATERIAL, AN ELECTRONIC VERSION OF

THE COPYRIGHTED MATERIAL, OR ANY OTHER POTENTIAL VERSION OF THE COPYRIGHTED

MATERIAL (WHETHER THE TECHNOLOGY EXISTS AS OF THE COPYRIGHT DATE, OR IS YET TO BE

INVENTED). THIS PROHIBITION EXPLICITLY EXTENDS TO ALL OF THE ABOVE ACTIONS, BUT IS IN

NO WAY LIMITED TO THEM. ANY USE OF THE COPYRIGHTED MATERIAL, IN ANY MANNER, CAN

ONLY BE WITH THE PRIOR CONSENT AND AUTHORIZATION THAT IS BOTH WRITTEN AND

EXECUTED BY THE COPYRIGHT HOLDER AND THE OTHER PARTY, RELATING SPECIFICALLY TO

THIS COPYRIGHTED MATERIAL. THIS COPYRIGHT, AND ALL OF THE PROTECTIONS THAT IT

AFFORDS THE COPYRIGHT HOLDER EXPLICITLY EXTEND TO ANY COPYRIGHTED MATERIAL,

IMAGE, FILE, DATA, OR ANY OTHER ATTACHMENT IN ANY FORM, ELECTRONIC, PRINTED, OR IN

ANY OTHER FORMAT, THAT ARE ATTACHED TO THIS COPYRIGHTED MATERIAL IN ANY MANNER

OR FORM, AND TO WHICH THE COPYRIGHT HOLDER HOLDS OR IS ELIGIBLE, UNDER THE WIDEST

POSSIBLE INTERPRETATION, TO HOLD A COPYRIGHT TO. THE INTERPRETATION OF THE

COPYRIGHT HOLDER’S RIGHTS SHALL BE AS BROAD AS THE LAW ALLOWS, AND IN NO WAY

SHALL BE LIMITED BY THE RIGHT OR RESTRICTION NOT BEING STATED. THE COPYRIGHT SHALL

ALSO EXTEND TO ALL FUTURE PROTECTIONS UNDER THE LAW, AS THEY BECOME AVAILABLE.

THE FAILURE TO MENTION A PROTECTION OF ANY CURRENT OR FUTURE COPYRIGHT LAW

SHALL NOT IN ANY WAY INDICATE THAT THE LAW DOES NOT APPLY IN FULL TO THE

COPYRIGHTED MATERIAL. IF ANY PORTION OF THIS DOCUMENT OR COPYRIGHT IS NOT DEEMED

TO APPLY, AT ANY TIME, FOR ANY REASON, THAT SHALL IN NO WAY LIMIT ANY AND ALL OTHER

PROTECTIONS THAT THE COPYRIGHT GRANTS, NOR SHALL IT LIMIT FUTURE PROTECTIONS FROM

APPLYING AS THEY BECOME AVAILABLE. THIS COPYRIGHT IS IN NO WAY INTENDED TO

INFRINGE ON THE RIGHTS OF ANY OTHER PARTY.

2

Why Has Biocon been so successful?

Biocon is a fully integrated biopharmaceutical company located in Bangalore, India that

is focused on biopharmaceuticals, custom research and clinical research.i They have five

subsidiary companies that include Syngene, Clinigene, Biocon Biopharmaceuticals, AxiCorp,

and NeoBiocon.ii Biocon, Syngene and Clinigene together employee nearly 3600 biologists,

chemists, medical practitioners, engineers, and general administrators.iii Biocon delivers products

and solutions to partners and customers in over 50 countries. They are the largest biotechnology

company in India. As of 2008, Biocon was ranked as the 7th largest biotech company in the

world based on the number of employees.

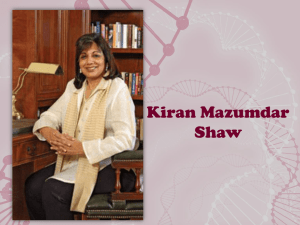

Biocon was founded in 1978 as a joint venture between Biocon Biochemicals Ltd. (BBL)

of Ireland and an Indian entrepreneur, Kiran Mazumdar-Shaw.iv When Mazumdar-Shaw saw

BBL being acquired by Unilever plc and ICI Ltd., she held onto her stock and formed Biocon

India. Since its inception, Biocon has evolved from an enzyme manufacturing company to a

fully integrated biopharmaceutical enterprise.v They have received numerous accolades through

the years for such achievements as the first biotechnology company to receive ISO 90001

certification in India, first Indian company to manufacture and export enzymes to the US and

Europe, first Indian company to receive US funding for proprietary technologies, and only the

second Indian company to cross a market capitalization of $1 billion on the first day of listing.

Mazumdar-Shaw, the co-founder of Biocon, remains the chairman and managing director

of Biocon. She and her husband John Shaw own over 60 percent of the company’s stock. Not

only has Mazumdar-Shaw accepted numerous awards through the years for the success of

Biocon, she has received numerous awards highlighting her own successes (to include receiving

one of India’s highest civilian honors, a lifetime achievement award, business leader of the year

in Biotechnology, and Best Entrepreneur).

Biocon’s success began at its inception with Mazumdar-Shaw’s sequential growth

strategy for the company. Each business she added to the company added to the mission of

Biocon by providing a stepping stone toward making Biocon a biotechnology powerhouse.

These “stepping stones” included consolidating Biocon’s core skills in enzymes, establishing a

footprint in biopharmaceuticals, and partnering with global firms. Biocon’s successes in these

areas, led Mazumdar-Shaw to pursue an even riskier adventure into the world of drug discovery.

The bulk of Biocon’s revenue in their early years came from their success in generic drug

manufacturing. Generic drugs typically cost 20 to 80 percent less to manufacture because the

products are not burdened with legacy expenses of research, development, clinical trials and

marketing (as the original pharmaceutical products would be). Biocon, like many other drug

companies, used a large portion of their generic revenue to finance their breakthrough into drug

discovery. However, increased competition in the biopharmaceutical market, led Biocon to the

realization that their success in generics alone, would not allow them to reach their global

3

aspirations. Additionally, changes in the regulatory environment prohibited them from

manufacturing and marketing generic versions of patented drugs (one of the main ways Indian

companies were prospering).

For nearly two decades, Biocon expanded and diversified into various fields beyond its

specialization in enzymes. These fields included biopharmaceuticals, custom research, and

clinical research. In 2004, their success led them to issue an initial public offering (IPO), valuing

the company at $1.1 billion. In 2005, they earned revenue of US $167 million.

The importance of Biocon’s manufacturing of enzymes was the basis for their

competitive advantage of fermentation. Biocon’s fermenting capacity gave it the ability to scale

up an industrial process and the platform to pursue discovery-led growth. Biocon was able to

differentiate itself from competitors in the making of Active Pharmaceutical Ingredients (APIs)

by deploying their core skills in fermentation while the global market for statins (a class of drug

used to lower plasma cholesterol level) was shrinking in value as statins lost patent protection,

though the market was growing in volume. Biocon was also successful because they went

beyond making APIs to supplying formulations to innovator companies.

Biocon’s ability to maintain molecular biology as their core competence has been one of

the most instrumental reasons for their success. Most companies come into the drug discovery

world only having skills in synthetic chemistry. Biocon is equally involved in synthetic

chemistry and molecular biology.

Biocon also demonstrated sophisticated business practices by allowing their clinical trials

to be handled by their subsidiary, Clinigene. This subsidiary leveraged India’s large population

and low cost medical and scientific professionals to provide clinical research services at low

prices and to facilitate rapid establishment of trial groups. By the year 2008, it was estimated that

30 percent of global clinical trials would take place outside of the US and that Europe and India

would be their preferred destination (due to speed of patient enrollments and shorter timelines).

Additionally, the clinical trial market was estimated to grow by 20 percent each year, which

would likely benefit Biocon even more.

As Mazumdar-Shaw began to envision her goal to generate a “six-fold increase” in

revenue within the next decade by building a strong discovery orientation biotechnology

enterprise, it was apparent that Biocon was already leading the way in several areas. In the

research stage of drug discovery Biocon had already launched a biodiversity program to collect,

catalogue and conserve rare and diverse species of indigenous bacteria, yeast, and fungi. This

was a valuable tool in discovering new biotech products. In the development phase of drug

discovery, Biocon relied on its partnerships with global biotech firms to share development

costs, which wasa powerful tool that helped to de-risk Biocon’s own investments.

Biocon appears to be achieving its success through many channels. Their intellectual

asset creation, state-of-the-art manufacturing capabilities, international benchmarks for the

4

quality of their regulatory systems and their disease-specific clinical research have all been

invaluable.vi They follow precise manufacturing, laboratory and documentation practices that

ensure consistent high quality results. With Mazumdar-Shaw as their leader they develop cross

functional teams to encourage empowerment, communicates clearly and truthfully to help shape

organizational values, and consistently pursues biotechnology commercialization opportunities

that are exciting but very risky.vii

Explore arguments in favor of success in the future.

Based on Biocon’s success record to date and the powerful leadership of MazumdarShaw, there are many areas we can examine in favor of success for the future of this company.

To begin, their sequential growth strategy since inception has proved to be priceless in their

aspirations to become a biotechnology powerhouse. Their consolidated core skills in enzymes,

established footprint in biopharmaceuticals and partnerships with global firms is leading to a far

more rewarding realm for them in drug discovery. By partnering with global companies they can

manage their risk better and lower costs in drug discovery. Drugs based on biology are also

estimated to replace 70 percent of conventional therapies by 2025,which is another one of

Biocon’s competitive advantages.

Biocon has a good source of revenue to move into drug discovery since they are a major

manufacturer of generics. They are one of 74 manufacturing facilities in India certified by the

US Food and Drug Administration (FDA) that sold generics in both the US and Europe. In

2006, there were $82 billion in global blockbuster drugs facing patent expiry,which would mean

the generic market would only grow. India’s share of global generic market was expected to

increase to about 33 percent in 2007, from 4 percent in 2004. Major drug companies were also

interested in driving down costs, so they were looking for partner specialist firms in India and

China as sources of input for research and clinical development.viii By focusing on unique

technology and patents in the US, Biocon has been given exclusive global rights for many

products.

Another argument for success revolves around Biocon’s focus on diversification in their

early years. Their manufacturing of enzymes was 15 percent of their revenue and was expected

to grow 6.5 percent a year. Enzymes were a springboard for fermentation, which was a core skill

in later stages of the value chain of biopharmaceuticals.

Biopharmaceuticals represented 80% of Biocon’s turnover and the global generics market

was set to grow even more as dozens of drugs came off patent. Governments, insurers and

health care organizations were turning to generics to reduce costs. Additionally, more of the

global drug companies were exporting parts of the value chain to low cost producers like India.

Biocon was also manufacturing via fermentation. This was important because molecular biology

produces a product that is less likely to fail in the end product. As a biologic process, molecular

5

biology is less intrusive when embedded in a biological system than a synthetic drug, and less

likely to fail in a clinical trial.

Biocon was successful in forming Syngene to capture the business of research process

outsourcing (RPO). This type of outsourcing was being done by many global drug companies

who wanted to reduce their R&D costs and shorten product valuation times. Biocon positioned

itself to provide synthetic chemistry in partnership with established pharmaceutical companies

and molecular biology in partnership with biotechnology companies while many of their

competitors had a specialty focus.

To be successful in the future in drug discovery, Biocon needed to excel in three areas of

drug discovery: research, development and commercialization. In research, Syngene and

Clinigene were leading the way for Biocon by providing a solid platform to move into drug

discovery. Biocon has had an in-house R & D team and a biodiversity program that was helping

in the discovery of new biotech products. Biocon’s partnerships with biotech startups were also

seen as a key element as they further helped Biocon to integrate backward into discovery

research.

Building on capabilities in clinical trials, Biocon had already taken tentative steps toward

involvement in the development state of drug discovery. They limited their activities to known

targets and known molecules and relied on partnerships with global biotech companies to share

development costs. Partnering with India was seen as a fast track way to climb the valuation

chain by many foreign companies. Through partnering, Biocon takes on molecules for

development that were built by partners who invested in the drug research and moves the drug

development process forward. They save on the costs on research while their foreign partners

save on drug development.

The last stage of drug discovery is commercialization, which is where Biocon has the

least expertise and they were making investments to create the manufacturing capacity for

industrial scale-up to meet commercial demand. Biocon would also need to comply with

manufacturing standards and deploy a sales force with expertise in marketing and promotions.

Through fine tuning of their commercialization skills and strengthening of some of their core

capabilities, Mazumdar-Shaw’s vision to turn Biocon into a top-10 biotechnology firm with sales

exceeding $1 billion by 2015 appears to be an achievable goal based on the success and

performance of this company to date.

Explore reasons for concern.

The primary reason of concern for Biocon’s success is the riskiness associated with drug

discovery. Only 1 in 5,000 molecules reach the clinical trial stage, only 1 in 500 undergoing

clinical trials reach the commercial stage. Biocon has 9 molecules at various stages of

6

development. The odds are against Mazumdar-Shaw’s expectations that all 9 molecules will

reach commercialization by the end of the decade. Additionally, the low availability of venture

capital in India requires Biocon to fund/take on a large portion of the risk. Drug discovery in the

words of Mazumdar-Shaw is managing “infinite risk”, that was not in the mindset at Biocon but

had to be learned. Drug discovery is different from Biocon’s traditional revenue source, of

generic drugs, which do not involve a unique discovery but differ only in price. Drug discovery

also doesn’t provide the instant cash gratification that generics provide.

The regulatory environment that had made generics so attractive, and was a critical part

of Biocon’s income was another reason for concern. India had introduced a full-fledged patent

regime in compliance with the World Trade Organization (WTO) agreement on Intellectual

Property. Previously Indian companies that had been able to manufacture generic versions of

drugs patented in other countries would no longer be able to do so. This would severely impact

these companies, including Biocon, as it would cut their income of manufacturing and marketing

of patented drugs and limit their funds for drug discovery. Generics would no longer be allowed

until the patent expired. This circumstance was creating an impetus to change their business

model and integrate it with their evolving strategy around drug discovery moving forward.

Another reason for concern was whether or not Biocon’s four broad areas of

specialization: enzymes, biopharmaceuticals, custom research and clinical research would

distract it from moving into drug discovery. Enzymes provided a springboard for Biocon’s

competitive advantage, offering leverage in stage three of the value chain of pharmaceuticals.

However, Biocon had less than a one percent share of world market in enzymes, and was up

against two large European players with 70 percent of the market share. Biocon competes

directly against niche players such as many Chinese firms are. The low cost Chinese firms could

potentially drive Biocon out of the sector on price. In addition, the European players may push

Biocon out of the market if they increased market share.

Biocon makes 45 percent of their revenue from ingredients (API’s) for statins. Although

Mazumdar-Shaw is confident that as the brand name statins lose patents the market for Biocon’s

ingredients will shrink in value but the volume of product sold will increase. However, there is

no guarantee that Biocon will gain any of this increased volume. In addition, if other

competitors move in with lower priced API’s and take away Biocon’s volume the resulting

reduction in cash flow will present a major problem for their plans to expand into drug

discovery.

There is also reason for concern with two of Biocon’s subsidiaries in relationship to drug

discovery research in the first stage of drug discovery. Clinigene makes up an extremely small

part of the rapidly growing clinical trial business, and has yet to build up its capabilities as a

clinical research organization. Syngene is operating in a competitive space against everyone

from full-service global drug development companies to teaching hospitals. While a growing

7

area, the extent of competition could prove formidable to Biocon as they change their focus to

drug development and away from their core businesses. Biocon is also outsourcing some of the

stages associated with drug discovery research because they don’t have the skills in this area.

This may prevent them from developing the skills that are crucial to drug discovery.

With regards to drug discovery development, Biocon is only taking “tentative steps” in

this stage by building on its capabilities in clinical trials, which are very limited based on

revenue. The company has limited its activities to known targets and known molecules and is

also relying on partnerships with global biotech companies to share development costs. Its

current activities utilized existing antibodies and molecules created by the firm’s partners,

instead of demonstrating the ability for Biocon to develop their own new drugs, which is its

stated goal.

Biocon has very little experience in commercialization, the final stage of drug discovery

and development. While the firm was investing in manufacturing capacity, the critical areas of

deployment of a sales force and development of expertise in promotions aimed at physicians and

end-customers are being neglected. This leads us to wonder if there is validity in discovering

and developing a drug if they’re not ready to sell it. This is especially true in a lucrative market

such as the US, which is heavily dependent on marketing.

Biocon may be spreading its resources too thin as it moves into drug discovery and faces

increased competition in generics, API’s for statins, and the substantially higher costs in drug

discovery. Moving away from their traditional area of commodities and business to drug

discovery and development also requires developing several new competencies such as building

a drug pipeline, project management, regulatory compliance, manufacturing and marketing.

These will all place great financial strain on the company’s resources. Mazumdar-Shaw needs to

determine if it’s worth it to take financial risk to expand her vision of achieving annual revenues

of $1 billion.

The final reason of concern for Biocon’s future success relates to the implementation of

the WTO patent law (combined with a repeal of restrictions on foreign investments under WTO).

This means that multinational corporations will begin invading the Indian market in force and

give Biocon more competition. Not only will they be competing in the local market against local

players, but they will also be competing in the local market against Merck and Bristol-Meyers

Squibb. In addition, multinational generic manufactures, such as Teva Pharmaceutical

Industries, will be competing against Biocon in its home market. The approximately 10,000

small companies in India’s domestic market currently producing copycat patents for local use

will all be competing for the generic market or attempting drug development to avoid going out

of business.ix Based on the prospective competition it may not be the proper time for Biocon to

expand their business to drug development.

8

Assume the role of Mazumdar-Shaw's top management team and develop an action plan

that will enable the company to meet its aggressive goals. Be as specific as possible in

developing your action plan.

In assuming the role of Mazumdar-Shaw’s top management team to develop an action

plan that will enable Biocon to meet its aggressive goal we first composed the goal into a single,

coherent and quantifiable statement, which is noted below. We then split the statement into

component parts that could be reasonably managed within the corporate skills of Biocon. The

intent of this approach was to break-up the effort so that risks could be more carefully managed

and rewards or consequences could be more closely measured. As identified by Michael Porter’s

framework in “The Competitive Advantage of Nations”,x Biocon’s corporate strategy provides

leverage internally and externally to establish a competitive advantage in achieving the goal.

Biocon Ltd goal for 2015:

Biocon Ltd’s goal is to become a top-10 biotechnology firm by reaching annual sales of

$1 billion by 2015.

As of March 2005, Biocon was positioned at number 14 in global rankings based on sales

according to exhibit one in the case.xi As of July 2008, they were positioned at number 20 in the

global rankings based on sales.xii Despite a slip in overall ranking, Biocon has successfully

grown their drug discovery revenue as planned. However, in comparison to other global

competitors, they have moved down in relative ranking. Biocon’s overall success was made

evident by a press release on September 24, 2009, when Biocon announced that they were

marked as one of only 20 Indian companies on Forbes ‘Best under a Billion List’ selected from

over 12,000 publicly-listed firms with sales of less than $1 billion in the Asia-Pacific region.

“Only 20 Indian companies have been featured in the list this year, which is dominated by

companies from China. All other companies have both increased sales and profits over the past

12 months or are forecasted to do so in upcoming quarters. ‘Apparel, media, technology and

health care led the way,’ said Forbes. This year's list is dominated by companies that have

withstood challenges that threatened their survival and those that have demonstrated exemplary

entrepreneurship.”xiii It is also worth noting a recent revenue statement made by MazumdarShaw herself that “All segments of our businesses have demonstrated robust growth.”

Mazumdar-Shaw said the company was confident of sustaining the growth momentum by using

its “differentiated profile” through its global partnerships. She said the partnerships would enable

the company to reach out to “lucrative opportunities in emerging and developed markets.”xiv

Observations of Biocon make it evident that the company is focused on accomplishing its

goal. In the book, The Indian Way, the author’s state that Mazumdar-Shaw “had built risktaking into her company’s culture through her own modeling—consistently pursuing

biotechnology commercialization opportunities that looked exciting but also very risky.”xv This

focus is also evident by comments from Mazumdar-Shaw in an interview of over 100 Indian

Executives where she states, "We have transformed ourselves into an integrated biopharmaceutical business. Our key areas of focus are diabetes and oncology. We are developing

9

oral insulin and antibodies for specific cancers."xvi The figure below is a graph of Biocon’s

Discovery Pipeline. It also offers a visual of the diverse segmentation balance between generics

and discovery drugs as well as the focus areas noted by Mazumdar-Shaw.xvii

The action plan below is proposed as a means to achieving the goal of reaching annual

sales of $1billion by 2015, and depending on the relative rankings of other firms in the sector

[NAICS 325412, SIC 2834,5] to become a top-10 global biotechnology firm. Acting as

Mazumdar-Shaw’s management team for Biocon, we identified two major steps to accomplish

the goal with sub-activities and two major barriers to overcome as part the action plan. These are

outlined below.

Steps to accomplish:

1) Build a highly effective project management team to accomplish step two below; comply with

regulations; control manufacturing; and create the marketing necessary for achieving the sales

goal.

2) Build a portfolio of strong candidate drugs to mature as efficiently as possible according to a

market driven schedule of at least one-per year for the next five years, 2010-2015.

a) Research: Under our research efforts, we will screen molecules and genes with the

highest probability of success and lowest consequence of failure by managing risks on

the most likely candidates that will increase revenue on pharmaceuticals in excess ($600

10

million by 2015) of the expected decrease in revenue on generics ($19 million starting in

2008).

b) Development: We will leverage the outputs from research by creating hybrid cells and

scaling them up with enzymes to establish a platform for commercialization.

c) Commercialization: Our success will depend on receiving regulatory approvals and

tactically marketing our products to reach our sales goal.

Barriers to overcome:

1) As we shift our business model from generics, to also include drug discovery, we must

determine how much to press the risk-reward continuum on all of our financial priorities by

seeking a balance between our capital obligations with venture capitalists, our subsidiaries, our

partners and our existing generics segment. We must also carefully monitor our new products for

potential post-market liability consequences and identify potential opportunities for product

growth events in the marketplace such as expanding into new markets or increasing our share of

existing markets.

2) In conjunction with overcoming the above barrier, we must design and build quality into all of

our new or expanding processes. By leveraging our recent capital expenditures of $135 million

($100 million in 2005-06 for enzyme fermenting and $35 million in 2008 to increase

biopharmaceutical capacity), we must also increase our existing productivity through continuous

improvement targets on our legacy processes so that they will approach our new process

capacities. This will enable us to more effectively integrate our total productive output by

supporting operations in all segments to exceed the expected decline in generic revenues with the

expected increase in biopharmaceutical revenues.

The action plan detailed above provides a strong internal framework to accomplish our

goal of $1 billion in annual sales by 2015. Exhibit 1 provides an excerpt of the framework in a

more detailed view that can be revised as needed based on quarterly reviews during execution of

the action planxviii. The global business climate will be a major determinant of whether or not we

will achieve the ranking of a top-10 biotechnology firm. As Mazumdar-Shaw’s top management

team, we will need to assist in controlling corporate matters on operational and tactical timeframes and advise on corporate matters from a strategic time-frame perspective. In reviewing the

framework offered by Porter, we learned that we need to integrate our action plan for Biocon

with a strategic plan that addresses factor conditions, demand conditions, related and supported

industries, firm strategies, structure and rivalry. In some aspects, Biocon has taken an approach

that addresses these areas by acquiring subsidiaries with Syngene in the research segment and

Clinigene in the development segment. Biocon has also taken this approach by setting up a

controlling interest in partnerships with CIMAB in development and AxiCorp in

commercialization (through distribution), among other minority stake interests. These

relationships are strategic business moves that seek to address the factor and demand conditions

as well as the related and supported industries. The remaining areas that Biocon should seek to

11

strengthen are the strategies that encompass their local and global approach to rivalries and

government policies.

Biocon’s strategy for establishing its global position could be compared with a

description offered by Pankaj Gemawat in a December 2005 Harvard Business Review article,

titled Regional Strategies for Global Leadership. In this article, Gemawat writes “Leading-edge

companies are starting to grapple with these definitional issues [on varying what defines a

region].” For example, firms in sectors as diverse as construction materials, forest products,

telecommunications equipment, and pharmaceuticals have invested significantly in modern

mapping technology, using such innovations as enhanced clustering techniques, better measures

for analyzing networks, and expanded data on bilateral, multilateral, and unilateral country

attributes to visualize new definitions of regions.xix

Biocon persists as India’s largest and most successful biotechnology firm by a healthy

margin over its other national competitors. From a local strategy perspective, they are

comfortably positioned to stay ahead of their in-country rivalries. For Biocon to reach its desired

position in global ranking within the top-10, they must baseline their goals on the performance

characteristics of at least the annual number 10 performer each year. As of 2005, Millenium

Pharmaceuticals (USA) was the number 10 ranked company. As of 2010, Actelion was the

number 10 ranked companyxx. Comparing financially reported sales for 2009 between Biocon

Ltd and Actelion in US dollars, the difference is roughly twice for Actelion at approximately

$1.7 billion than for Biocon at approximately $350 million (based on an exchange rate of 1 INR

= 0.0219539 USD retrieved on May 7, 2010). This difference shows that Biocon has a very

aggressive goal of reaching at least the number 10 global rank by year-end sales figures for 2009.

Holding all other variables constant, at this rate it would require Biocon to achieve an annual

average increase in sales on the order of $88 million per year for the next four years to reach $1

billion in sales by 2015. The action plan proposed is a strong plan that needs to be integrated

comprehensively with the strategic plan so that the goal is more achievable in the given time

frame and considers the relative factors of local, region, demand, support industry, competition,

risk and post-market consequences.

i

Biocon General Information, retrieved on May 8, 2010 on-line at Biocon’s website, http://www.biocon.com/biocon_aboutus_factsheet.asp

Biocon General Information, retrieved on May 8, 2010 on-line at Biocon’s website, http://www.biocon.com/biocon_aboutus_factsheet.asp

iii Biocon General Information, retrieved on May 8, 2010 on-line at Biocon’s website, http://www.biocon.com/biocon_aboutus_factsheet.asp

iv Anonymous. (2007, July 21). Biocon India. Retrieved May 8, 2010 from http://www.iloveindia.com/economy-of-india/top-50companies/biocon.html

v

Anonymous. (2007, July 21). Biocon India. Retrieved May 8, 2010 from http://www.iloveindia.com/economy-of-india/top-50companies/biocon.html

ii

vi

Anonymous. (2004). Naukri Hub. Retrieved May 8, 2010 from http://www.naukrihub.com/india/pharmaceutical/top-companies/biocon.html

Capelli, P., Singh, H., Singh, J., and Useem, M., The India Way. Harvard Business Press, 2010.

viii

Richard Balaban, “Beyond the Blockbuster,” a research report prepared by Mercer Management Consulting, www.

Amanet.org/PharmaFocus/food_company/mar_04.htm, referenced May 3, 2010.

ix Manjeet Kripalani, “India: Bigger Pharma,” BusinessWeek online, April 18, 2005,

www.businessweek.com/magazine/content/05_16/b3929068.htm, referenced May 3, 2010.

x

Enright, M., The Geography of Competition and Strategy, Harvard Business School 90793-135, Rev. December 1, 1994, page 4

xi

Chandrasekhar, R. (2006). BIOCON LTD: BUILDING A BIOTECH POWERHOUSE, Richard Ivey School of Business, University of Western Ontario

906M70, ver. (A) September 13, 2006, page 9.

vii

12

xii

Anonymous. (2008, July 18). Business Line: CORPORATE: Biocon gets global ranking of 20. Business Line (India) 1.pag. Retrieved May 7, 2010,

from NewsBank on-line database (Access World News)

xiiiAnonymous. (2009, September 24). Biocon among 20 Indian companies in Forbes 'Best Under A Billion' List. Accord Fintech (Mumbai, India)

1.pag. Retrieved May 7, 2010, from NewsBank on-line database (Access World News)

xiv Anonymous. (2010, April 29). Biocon profit zooms to Rs. 293 crore. The Hindu. 1.pag. Retrieved May 7, 2010, from www.Google.com on-line

news search

xv Cappelli, P., Singh H., Singh, J. Useem, M., The India Way, Harvard Business Press, 2010, page 126

xvi Anonymous. (2007, January 11). India Knowledge @ Wharton. 1.pag. Retrieved May 6, 2010, from link in Appendix B of The India Way, page

276

xvii Biocon Ltd, Discovery Pipeline Graph, retrieved on May 6, 2010 on-line at Biocon’s website under the R7D menu,

http://www.biocon.com/biocon_research_pipeline.asp

xviii

Van Houten, L. Miyasaka, J. Agullard, K. Zimmerman, J. (WestEd 2006). Adapted from excerpt in Developing and Effective School Plan: An

Activity-Based Guide to Understanding Your School and Improving Student Outcomes. Handout 4.7-2.

xix Ghemawat, P., Regional Strategies for Global Leadership, Harvard Business Review, December 2005, page 10

xx Research and Markets Offers Report: Top 10 Biotech Companies: Media Monitor. (2010, February). Wireless News, 1. Retrieved May 7, 2010,

from ABI/INFORM Complete. (Document ID: 1972670581).

13