Money and Real Economy

advertisement

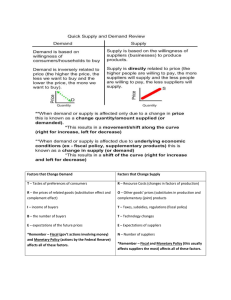

Money and Real Economy Money, Bonds, Monetary Policy, GDP 1 Money and Bonds There are many things in the economy Cash Chequing accounts Saving accounts Treasury bills Bonds Business shares (equity) etc Simplify Yields no interest = money Medium of exchange Cash Chequing accounts Yields interest = bond Medium of saving 2 Discounting A bond Coupon Maturity T Price Yield i Present value of a bond Stream of revenues in the future Discounted future payments Present value of a stream In equilibrium, bonds yield market interest rate The equilibrium market price of a bond = PV of the income stream 3 Demand for money Demand for money = amount of money that everyone in the economy wants to hold Greater demand for money = lower demand for bonds Reasons to hold money Transaction demand Simplest, M = aY Precautionary demand Speculative demand Adjusting portfolio of financial assets Lower interest rate expected = we expect bond prices will increase = we want more bonds now = we want to hold less money now 4 Demand for money, curve Interest rate is negatively related to the amount of money we want to hold Interest rate = cost of holding money MD = MD(i, Y, P) ∂MD/∂I < 0 Along the MD curve ∂MD/∂Y > 0 Shift in the MD curve ∂MD/∂P > 0 Shift in the MD curve 5 Monetary equilibrium Money supply MS is independent of interest rate Print more money = greater money supply Let banks create more money = greater money supply Any of these increase reserves Monetary equilibrium: MD = MS Because the bond prices change and so the interest rate changes This is the liquidity preference theory of interest 6 Monetary Transmission Mechanism Step 1: The liquidity preference theory of interest: Increase in MS Decrease in equilibrium interest rate Increase in equilibrium quantity of money Increase in MD Increase in equilibrium interest rate No change in equilibrium quantity of money 7 Monetary Transmission Mechanism Step 2: Decrease in equilibrium interest rate Increase in desired investments Demand for investments Increase in consumption Big ticket items Increase in net exports Capital outflow Depreciation of Canadian dollar Domestic goods cheaper than foreign goods The slope of the AD curve 8 Long Run vs Short Run Short run: Increase in money supply => Increase in AD => Positive AD shock Long run Y* = const Recall, factor prices will adjust Now can think: Positive AD shock => P increases => MD increases => interest rate increases 9 Long Run vs Short Run We say Money are neutral in long run Means money do not influence real GDP in long run Money are not neutral in short run Means money do influence real GDP in short run This is Classical Dichotomy 10 Effectiveness of monetary policy MD steep ID flat Monetary policy is effective Monetarists MD flat ID steep Monetary policy is ineffective Keynesians 11