Making Capital Investment Decisions

advertisement

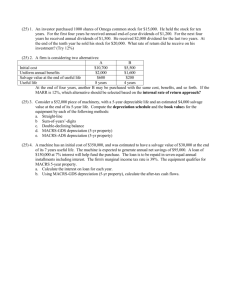

The depreciation expense used for capital budgeting should be the depreciation schedule required by the Revenue Canada for tax purposes Depreciation itself is a non-cash expense; consequently, it is only relevant because it affects taxes Depreciation tax shield = DT ◦ D = depreciation expense ◦ T = marginal tax rate 0 If the salvage value is different from the book value of the asset, then there is a tax effect Book value = initial cost – accumulated depreciation After-tax salvage = salvage – T(salvage – book value) Question: If a machine initially costs 120,00 and depreciated straight-line to zero, and sold after 6 years at 20,000, what is the after tax salvage value if tax rate is 40%? 1 Bottom-Up Approach ◦ Works only when there is no interest expense ◦ OCF = NI + depreciation Top-Down Approach ◦ OCF = Sales – Costs – Taxes ◦ Don’t subtract non-cash deductions Tax Shield Approach ◦ OCF = (Sales – Costs)(1 – T) + Depreciation*T 2 Assume we have the following background information for a project being considered by Gillis, Inc. See if we can calculate the project’s NPV and payback period. Assume: Required NWC investment = $40; project cost = $60; 3 year life. Annual sales = $100; annual costs = $50; straight line depreciation to $0. Tax rate = 34%, required return = 12% 3 Two golfing buddies are considering starting a new golf facility to there entertainment company. Because of the growing popularity of golf, they estimate the facility will generate rentals of 20,000 buckets of balls at $3 a bucket the first year, and that rentals will grow by 750 buckets a year thereafter. The price will remain $3 per bucket. Should they pursue this new venture? Capital spending requirements include: Ball dispensing machine Ball pick-up vehicle Tractor and accessories $ 2,000 8,000 8,000 $18,000 All the equipment is Class 10 CCA (30%), and is expected to have a salvage value of 10% of cost after 6 years. (Assume that there are many assets in this asset class apart from the golf business). Anticipated operating expenses are as follows: 4 Operating Costs (annual) Land lease Water Electricity Labor $ 12,000 1,500 3,000 30,000 Seed & fertilizer 2,000 Gasoline 1,500 Maintenance Insurance 1,000 1,000 Working Capital Initial requirement = $3,000 Working capital requirements are expected to grow at 5% per year for the life of the project. Company’s tax rate is 20%. Cost of capital is 10%. Misc. Expenses 1,000 $53,000 5 Year Revenues Fixed Costs Depreciation EBIT Taxes (20%) Net Income 1 2 3 4 5 6 $60,000 $62,500 $64,500 $66,750 $69,000 $71,250 53000 2,700 $4,300 $860.0 53000 4,590 $4,910 $982.0 53000 3213 $8,287 $1,657.4 53000 2249 $11,501 $2,300.2 53000 1574 $14,426 $2,885.2 53000 1102 $17,148 $3,429.6 $3,440.0 $3,928.0 $6,629.6 $9,200.8 $11,540.8 $13,718.4 6 Operating cash flows: Year EBIT 0 $0 1 4,300 2 4,910 3 8,287 4 11,501 5 14,426 6 17,148 + Depreciation – $ 0 2,700 4,590 3,213 2,249 1,574 1,102 Taxes -$ 0 - 860 - 982 -1657 - 2300 - 2885 - 3430 = = = = = = = = Operating cash flow $ 0 6140 8518 9843 11450 13115 14820 Total Cash flow from assets: Year 0 1 2 3 4 5 6 OCF $0 6140 8518 9843 11450 13115 14820 – Chg. in NWC -$ 3,000 -150 -158 -165 -174 -182 +3829 – Cap. Sp. -$18,000 0 0 0 0 0 +1,800 = Cash flow = – $21,000 = 5590 = 8360 = 9678 = 11276 = 12933 = 20089 7 Straight-line depreciation UCC ◦ D = (Initial cost – salvage) / number of years ◦ Very few assets are depreciated straight-line for tax purposes ◦ Need to know which asset class is appropriate ◦ Follow procedure is done in Chapter 2 8 The Canadian CCA calculation means that depreciation tends to change over time. Figuring out EBIT is rather involved, because it requires us to do an analysis for every year. The tax shield approach is helpful in that regard, because it allows us to derive the present value of the tax shield on CCA separately, instead of calculating the actual savings for each year separately. The idea is as follows: Note that CCA savings follows the following pattern Time Undepreciated Depreciation Tax Savings capital cost (CCA) 1 C Cd CdT 2 C-Cd=C(1-d) C(1-d)d C(1-d)dT 2 2 3 C(1-d) C(1-d) d C(1-d)2dT . n C(1-d)n C(1-d)nd C(1-d)ndT 9 IdTc PV tax shield on CCA k d 1 0.5k 1 k S n dTc 1 PV tax shield on CCA n k d 1 k 10 An investment of 300k in a machine lasts for 5 years and then sold for 50k. The CCA rate is 15%, tax rate is 40%, and the discount rate is 20%. What is the PV of tax shields? 11 Ilana Industries, Inc., is considering buying a new machine at a cost of 1M$. The machine will cost $35,000 to run and will generate products at a market value of $125,000 for the next 10 years. The machine is an asset class with a CCA rate of 25%, and Ilana has many other assets in this asset class. The salvage (market value) of the machine after 10 years is 100,000. The discount rate is 10% and corporate tax rate is 35%. Calculate the NPV of buying the machine. 12 Question Bendog’s Franks is looking at a new system with an installed cost of $450,000. This equipment is depreciated at a rate of 20% per year (Class 8) over the project’s six-year life, at the end of which the sausage system can be sold for $100,000. The sausage system will save the firm $105,000 per year in the pre-tax operating costs, and the system requires an initial investment in new working capital of $23,500. If the tax rate is 37 percent and the discount rate is 12.5 percent, what is the NPV of this project? 13 Consider a $10,000 machine that will reduce pretax operating costs by $3,000 per year over a 5-year period. Assume no changes in net working capital and a scrap (i.e., market) value of $1,000 after five years. For simplicity, assume straight-line depreciation to zero. The marginal tax rate is 34% and the appropriate discount rate is 10%. 14 Cash OutFlows in Dollars Project: C0 C1 C2 C3 PV @ 6% Machine D 15 4 4 4 $25.69 Machine E 10 6 6 - $21.00 15 You are operating an old machine which will last 2 more years. It costs $12,000 per year to operate. A new machine costs $25,000 to buy, but is more efficient and can be operated for $8,000 per year. It will last for 5 years. Should you replace this year? Should you replace next year? Cash Flows in Dollars Project: C0 C1 C2 C3 C4 C5 PV @ 6% New Machine Equivalent Annual cost: 25 8 8 8 8 8 $58.70 ? ? ? ? ? $58.70 16 Burnout Batteries ◦ Initial Cost = $36 each ◦ 3-year life ◦ $100 per year to keep charged ◦ Expected salvage = $5 ◦ Straight-line depreciation Long-lasting Batteries ◦ Initial Cost = $60 each ◦ 5-year life ◦ $88 per year to keep charged ◦ Expected salvage = $5 ◦ Straight-line depreciation The machine chosen will be replaced indefinitely and neither machine will have a differential impact on revenue. No change in NWC is required. The required return is 15% and the tax rate is 34%. 17 Project interactions: When we do NPV calculations, the idea is to decide between pursing a project or not pursuing the project. For example: we can construct the building on a land we own, or we can sell the land. For simple comparisons between alternative, we typically do a comparison in one step. For more complicated cases, it is sometimes easier to do 2 NPV calculations. However, we should always realize that we can construct a project that includes both alternatives. 18 Capital budgeting Aqua-Products currently manufactures a wide range of equipment for water sports. The company is re-evaluating its rubber rowboat product line to determine whether it will continue to be profitable or whether it should be discontinued. Net operating revenues before tax (i.e., sales minus all operating costs) are estimated to be $180,000 per year for each of the next 10 years. It is estimated that the rubber rowboat product line has a useful life of 10 years; that is, after year 10 no further revenues are anticipated from this particular product line and the economic value of all machinery used to produce the rubber rowboats will be zero. Continued production of this product line requires that finished goods inventory of rubber rowboats be maintained at a level of $64,000 throughout the ten year life of the project. (If this product line were discontinued, obviously the level of finished goods inventory of rubber rowboats would be reduced to zero.) If the rubber rowboat product line were shut down, there would be immediate expenses (100% tax deductible) of $270,000. On the positive side, machinery formerly used in the production process could be sold for $720,000. This machinery is in asset class 39, which is allowed a CCA rate of 25%. The firm also has many other assets in this class. The floor space that is vacated by the shutdown could be leased out at $75,000 per year. The firm’s tax rate is 40%, and the appropriate discount rate is 14%. Based on an NPV analysis, should Aqua-Products continue to manufacture rubber rowboats or close down this one product line? Explain all the steps taken to reach your conclusion: structuring of the problem and analysis should be explained in words as well as given by calculations. Simply providing a numerical answer is not sufficient. 19 How do we determine if cash flows are relevant to the capital budgeting decision? What are the different methods for computing operating cash flow and when are they important? What is equivalent annual cost and when should it be used? 20 A five year project has an initial fixed-asset investment of $210,000, an initial NWC investment of $20,000, and an annual OCF of -$32,000. The fixed asset is fully depreciated over the life of the project and has no salvage value. If the required return is 15 percent, what is this project’s equivalent annual cost, or EAC? 21